Returning to Value-Based Healthcare: What Will the Future Medical Payment Model Look Like?

This article is selected from the WeChat official account “Jiong Shen Product Perspective,” authored by Jiong Jiong Tongxue, and published with authorization from VCBeat.

The healthcare industry is rife with contradictions. This series primarily examines the conflicts on the payment side of healthcare. Due to its extensive scope, it has been divided into three parts—Part I, Part II, and Part III—which will respectively discuss commercial health insurance, DRG-based payment, and the PBM service model.

Setting aside considerations of public welfare and ethics, let us examine the issue of healthcare payment from a commercial perspective. Currently, the largest payer for medical expenses is the national basic medical insurance (whose primary funding sources are actually contributions from employers and employees). However, this insurance scheme currently covers only therapeutic services rendered after individuals have already fallen ill, such as pharmaceuticals, medical devices, and surgical procedures. It does not cover preventive services, such as health management aimed at keeping people from getting sick. Meanwhile, hospitals and physicians generate revenue only by providing medical services to treat patients after they become ill. This creates a paradox between “patients maintaining their health” and “doctors earning income.”

For patients, maintaining health yields the greatest benefit. For physicians, however, improving performance metrics and increasing income often depend on prescribing more medications and performing more surgeries. Although this observation is uncomfortable, it reflects the current reality. This situation is inherently absurd: patients save money by staying healthy, while physicians earn money when others fall ill. These two interests are diametrically opposed and deviate from the core medical philosophy that “the superior physician prevents disease, the competent physician treats impending disease, and the inferior physician treats established disease.” Therefore, I am considering whether a model can be developed to create positive synergy between patients and physicians, rather than a zero-sum game of mutual extraction. Specifically, does a business model exist where “the healthier the patients, the higher the physicians’ earnings”? Consequently, my primary focus is on how innovations in healthcare payment mechanisms can drive reforms in physician performance evaluation systems, thereby incentivizing physicians to prioritize patient health as a pathway to higher income.

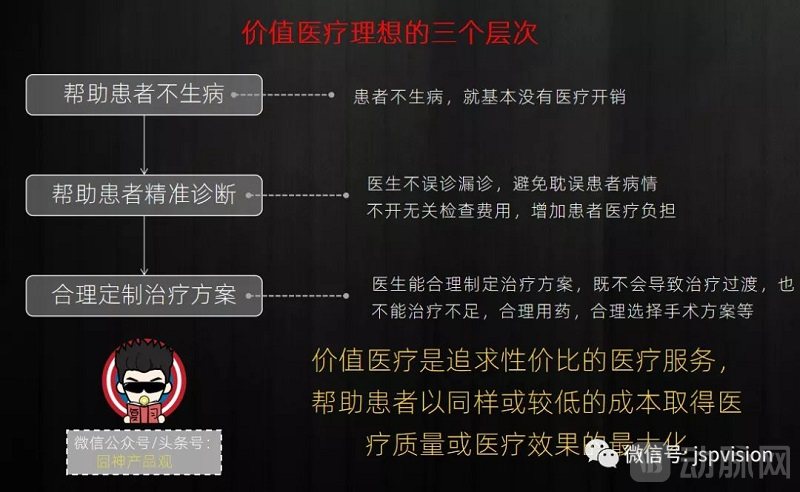

So, what should doctors do to keep patients healthy, achieve higher incomes, and return to value-based healthcare? I believe there are three progressive levels:

① First, prevent disease before it occurs; by helping patients stay healthy or fall ill less often, doctors are effectively helping them save money.

② Second, when illness occurs, physicians can make precise diagnoses, thereby reducing the unnecessary financial and energy expenditures caused by misdiagnosis;

③ Third is the post-diagnosis treatment phase, which aims to minimize medical expenses, develop tailored treatment plans, and assist patients in maintaining long-term health;

The higher the level of care physicians can provide, and the earlier they intervene in the preclinical stages of a patient’s disease, the greater the financial incentives they receive. What I ambitiously envision is that this new model, through the synergistic integration of “commercial health insurance + DRGs + PBM,” will fulfill patients’ three-tiered value-based healthcare needs.

● Commercial health insurance is essentially an innovative prepayment model that, when integrated with health management, incentivizes insurers to help patients reduce disease incidence by focusing on preventive care.

● DRGs are essentially a set of hospital management practices that incentivize physicians to conduct more thorough examinations and make more precise diagnoses, thereby assigning patients to the appropriate case groups during the differential diagnosis phase.

● PBM refers to Pharmacy Benefit Management, which establishes reasonable drug formularies, oversees physicians’ use of medications with better cost-effectiveness, effectively controls drug utilization, and helps patients and insurers reduce costs; it operates during the disease treatment phase.

Of course, each of these three approaches currently has its own limitations, and the conditions for practical implementation are quite stringent. For instance, commercial health insurance can only cover diseases with deterministic medical data; otherwise, it essentially becomes a form of betting. DRGs apply only to a subset of inpatient cases and do not provide comprehensive coverage. PBMs focus solely on pharmaceuticals and have limited ability to control price premiums associated with surgical procedures, given the strong element of human discretion involved. Furthermore, before the full integration of these three models can be realized, two critical prerequisites must be met, both of which are indispensable:

① Public health awareness has reached a certain level, meaning that the general public proactively purchases health insurance (similar to national medical insurance);

② Structured archiving of national health and medical data (including electronic medical records, health vital signs data, medication data, etc.);

The first condition is to ensure a stable payment source for services on the healthcare supply side, guaranteeing that physicians can be adequately compensated. The second is to ensure that digital healthcare and payment processes are traceable, allowing for continuous adjustment of premiums and reimbursement rates based on big data analytics, thereby maintaining payment rationality and enabling the sustainable development of this model. Despite numerous challenges and stringent requirements, this model holds significant promise for the future. It is hoped that the “Healthy China 2030” initiative will accelerate innovation in this payment transformation.

Below, I will conduct an integrated analysis of the “Commercial Health Insurance + DRGs + PBM” model, beginning with a discussion on commercial health insurance.

The most effective approach to preventing disease before it occurs is health management. In the current market, who truly has the incentive to pay for this service? Across the entire healthcare market, the four key stakeholders are patients, healthcare providers, pharmaceutical companies, and insurers. Healthcare providers and pharmaceutical companies, as high-revenue suppliers that have long relied on patient morbidity and mortality, have no incentive whatsoever to fund such reforms. Only two parties are willing to pay: patients, who seek health preservation, and insurance companies, which aim to control costs and reduce claim incidence rates.

According to a set of statistical data from 2018, China's health industry is mainly dominated by the pharmaceutical industry and the healthy elderly care industry, with market shares reaching 50.05% and 33.04%, respectively; the health management service industry has the smallest proportion, only 2.71%, which further illustrates this issue.

Overall, health management services remain immature, yet they hold immense potential for future development, particularly in the wake of the pandemic-driven surge since 2020. In the short term, however, patients are unwilling to pay directly for health management services—note the emphasis on “directly”—primarily due to the following reasons:

① Most people do not make definitive investments to increase the probability of better health.

What consumers are purchasing is health, not health management. The onset of disease is primarily driven by two key factors: innate genetic predisposition and acquired lifestyle behaviors. Health management can only influence the latter, thereby reducing the probability of disease rather than guaranteeing complete immunity with 100% certainty. Consider this analogy: Suppose you currently have a 2% chance of winning a $1 million lottery prize. The organizer then offers to raise your odds to 5% in exchange for an additional $30,000. How many consumers would be willing to pay this premium? From a psychological perspective, there is no fundamental difference between probabilities ranging from 1% to 99%; however, there is a qualitative distinction between 99% and 100%. The former represents a possibility, while the latter signifies certainty. Consequently, many individuals reason that it is more cost-effective to forego spending on health management and instead cover medical expenses if illness occurs. If they remain healthy, they perceive themselves as having gained financially. This mindset prevails among the majority of consumers.

② Most people do not have a strong perception of the benefits of health management.

Drawing an analogy with the stock market, if I invest in a high-quality stock, I can immediately see the returns in the form of increased profits. In contrast, investment in health management merely serves to maintain wellness and prevent illness. Subjectively, patient populations do not perceive any significant benefits, which results in insufficient motivation to engage in health management programs.

③ Individuals whose health needs have already been met are less likely to pay for additional health services.

There is a humorous saying that goes, “People only realize where their organs are when they fall ill.” Health management is akin to a dividend from your body; when you are healthy, you barely notice its existence. Most people in society prioritize money above all else, and only when their health deteriorates do they recognize that health outweighs wealth. Therefore, when you encourage healthy individuals to engage in health management, they often do not care much, thinking, “I am not sick anyway; what is there for you to manage?”

These are, in essence, rooted in psychological issues, which can be inferred from common sense. Therefore, it is extremely difficult for patients to make direct payments. Let us now examine another stakeholder: “insurance,” including both public health insurance and commercial health insurance.

Currently, China’s medical insurance system primarily covers pharmaceuticals, diagnostic tests, and surgical services. Health management interventions, such as dietary adjustment recommendations and behavioral habit monitoring, are generally excluded from coverage. Consequently, healthcare providers lack the incentive to proactively offer these services, as there is no reimbursement mechanism. Patients also tend to undervalue such services. As a result, only a subset of users with advanced health awareness and sufficient financial security are willing to pay for health management services to safeguard their well-being.

However, another interesting point is that while patients are unwilling to pay for health management services, they are willing to purchase commercial health insurance.

Since basic medical insurance only covers fundamental healthcare needs and does not reimburse all expenses, it falls short in addressing the actual medical and pharmaceutical needs of patients. Costs below the deductible threshold or above the coverage cap are not covered; furthermore, high-cost items such as self-paid drugs, imported medications, and ICU stays are entirely excluded from reimbursement. Even when reimbursement is available, it is subject to proportional limits. Therefore, commercial health insurance serves as a robust supplement to basic medical insurance, comprehensively enhancing patients’ health protection. This underscores the rationale for patients to purchase commercial medical health insurance: it transfers the financial risk of high treatment costs following illness to the insurance company.This logic differs fundamentally from that of purchasing health management services. The latter merely reduces the probability of disease onset, whereas the former ensures that, upon payment of premiums, all medical expenses within the policy terms will be covered by the insurer. One represents a probabilistic outcome, while the other offers a deterministic guarantee. Consequently, this model positions commercial insurance as the most likely primary payer for health management services, as insurers have a strong incentive to reduce patients’ disease risks and thereby lower claim expenditures.

The responsibility for helping patients achieve the first tier of health value—“preventive care to avert disease before it occurs”—increasingly falls on commercial health insurance companies. They have strong incentives to do so: when insured individuals’ health is effectively managed, the frequency of claims and payouts naturally decreases, thereby enabling insurers to indirectly secure greater profits. Moreover, expenditures on health management are generally significantly lower than the treatment costs incurred after patients fall ill and seek hospital care. Thus, leveraging the “health management + health insurance” model to deliver patient value is an exceptionally fitting approach.

However, we also observe that many insurance companies have traditionally designed health insurance products with a predominantly financial mindset, entirely lacking an integrated logic for health management. The approach was simply to provide compensation upon illness, leaving patients to navigate the healthcare system on their own. This is fundamentally putting the cart before the horse. True health insurance should prioritize medical care over financial attributes. While it possesses financial characteristics, it is essentially a product of the healthcare industry. Health insurance must return to its core essence. Even today, it remains difficult for the average person to purchase insurance that adequately meets their health protection needs. Not to mention the numerous restrictions based on age and pre-existing conditions, which prevent patients with urgent needs from obtaining coverage. Below is a comparison chart of products in the health insurance market. Take a look and consider whether current health insurers are merely “collecting premiums without regard for health.” It appears they are not focused on health management or medical services, but rather solely on the conditions and amounts of claims payout.

This clearly contradicts the original intent behind the design of this insurance category. However, developing such a product poses greater challenges for insurance designers, including foundational medical data collection and actuarial algorithm design. In the future, the launch of more personalized health insurance products tailored for individuals with pre-existing conditions is essential to drive innovation in commercial insurance and unlock this emerging blue-ocean niche market. According to 2019 data, domestic commercial health insurance claim payouts amounted to RMB 235.1 billion, accounting for only 3.6% of China’s total health expenditure—far below personal health out-of-pocket spending, which reached RMB 1.85 trillion and represented 28.4% of total health expenses. Furthermore, under the “Opinions on Promoting the Development of Commercial Insurance in the Social Services Sector,” jointly issued in December 2019 by the China Banking and Insurance Regulatory Commission (CBIRC) and 12 other ministries and commissions, the goal is for the health insurance market size to exceed RMB 2 trillion by 2025. This indicates substantial growth potential for commercial health insurance, representing at least a tenfold expansion opportunity. The core challenge lies in the fact that most insurers lack deep understanding of the healthcare industry. Therefore, strong collaboration between leading players in both the healthcare and insurance sectors is needed to introduce innovative payment mechanisms, making it possible to design truly “good health insurance” that delivers genuine value to patients. Two exploratory case studies are outlined below.

In the current healthcare services market, there is a vast array of medical service products available for resource integration. These service products can be broadly categorized by their efficacy, such as preventive, therapeutic, and rehabilitative services. Previously, these services were fragmented and lacked a systematic structure. For commercial health insurance, however, it is entirely feasible to integrate them and provide centralized services, thereby controlling overall healthcare expenditures.

Taking dentistry as a vertical sector, commercial health insurance providers can develop health protection products tailored to oral health issues. After paying an annual premium, users are entitled to corresponding insurance benefits and health services. Access criteria for preventive services such as dental scaling, as well as therapeutic procedures including fillings, root canal therapy, and dental implants, can be defined and incorporated into the insurance policy terms. Additionally, policyholders should be encouraged and reminded to undergo regular dental cleanings during the policy period, with incentives such as increased coverage limits offered as rewards. If patients still develop more serious dental conditions beyond these covered services, claims will be assessed and compensated according to underwriting guidelines. This approach helps the majority of patients mitigate the risk of dental diseases through prevention, while ensuring that even the minority who experience more severe issues remain protected.

Therefore, the benefits for commercial health insurance companies to incorporate health management services can be summarized in three points: First, by providing both insurance coverage and health management services, commercial insurers offer customers not only future risk protection but also immediately tangible services. This enhances the product’s market competitiveness and drives higher sales. Second, commercial insurers integrate contracted healthcare providers into their networks while ensuring a steady stream of clients. Policyholders, having paid for these services, are psychologically inclined to fully utilize them; consequently, most engage in regular, long-term dental cleanings. This volume strengthens the insurers’ bargaining power with healthcare providers, thereby reducing service costs (including those for dental cleanings and potential future dental surgeries). Third, regular dental cleanings help prevent serious dental conditions from developing, which reduces the probability of insurance claims to some extent, thereby lowering expenses and increasing profit margins.

This case study examines the current partnership between XX Biopharmaceutical and XX Insurance Company (names withheld to avoid any appearance of advertising). The primary objective of this collaboration is for the insurer and the pharmaceutical company to share the risks associated with patients’ medication use. For drugs with uncertain clinical therapeutic outcomes, an agreement linking therapeutic efficacy to payment—based on factors such as product efficacy, dosage, time points, and indications—has been established, giving rise to an innovative payment model. The agreement comprises three forms: Coverage with Evidence Development (CED), Contractual Trigger Clause (CTC) payments, and Payment by Results (PLR).

① CED—Applicable to drugs that are urgently needed in clinical practice but lack sufficient clinical evidence. Within the agreed period, reimbursement will be provided initially at the price set by the manufacturer. Subsequent decisions on whether to continue, increase, or discontinue payment will be made based on subsequently collected evidence. If the evidence demonstrates that the product has no value, the payer will withdraw the current price and establish a new pricing scheme lower than that of existing standard treatments.

② CTC—Applicable to generic drugs with unclear long-term efficacy. Both parties to the agreement stipulate one or more short-term therapeutic outcome targets, typically surrogate endpoints, biomarkers, or other nodal indicators. During the initial treatment phase, the pharmaceutical manufacturer provides discounts or free medications to the payer. Once patients achieve the therapeutic goals, the payer will reimburse for the medication and include it in the formulary. Similar to installment payments, this approach defers early payment obligations, spreading costs over several months or even years, thereby alleviating the payer’s initial financial burden to some extent. This model primarily addresses payers’ concerns that patients may continue receiving treatment even if the drug fails to deliver clinical benefits.

③ Performance-Linked Reimbursement (PLR): Applicable to pharmaceuticals with sufficient clinical evidence but uncertain real-world effectiveness. Payers encourage high-quality care; if a drug fails to achieve the expected outcomes (health improvements), the manufacturer is required to provide full or partial refunds, or adjust the price. Outcome metrics include short-term clinical results (surrogate endpoints or biomarkers), long-term clinical results (primary endpoints), or adherence. The innovation of this model lies in cost containment through health management based on the therapeutic value of medications. It meets the needs of patients at the third stage of “appropriate treatment” within value-based healthcare. Patients pay premiums to commercial health insurance companies, which then identify the most targeted and effective drugs on the market to help patients maintain their health. These insurers ensure reasonable revenue by reimbursing pharmaceutical companies based on therapeutic outcomes. For models such as the two categories mentioned above, there is still ample room to explore innovative value-based healthcare approaches across various stages of health and disease management. Therefore, the future of commercial health insurance holds significant potential for diverse strategies and innovations—stay tuned.

Commercial health insurance and health management services share aligned interests and boast immense market potential. Once integrated into a systematic framework, they are poised to become a powerful tool on the payment side of the broader health sector in the future.However, these measures alone are insufficient; the formulation of detailed rules for payment standards is of paramount importance. The next two articles will introduce the DRG and PBM models, so stay tuned if you are interested.