Alibaba Health Releases '2021 Tmall Wellness Trends Insight Report': Women's Hair Loss Anxiety Is Three Times That of Men

As niche subcultures such as Hanfu, Lolita fashion, and blind boxes have moved from the fringes into the mainstream spotlight, creative wellness practices have gradually emerged as a new trendsetter among young consumers. On June 16, Alibaba Health Research Institute released the “2021 New Insights into Tmall Wellness Trends” (hereinafter referred to as the “Insights”), based on data from the Tmall Pharmacy Pavilion, to decode the latest trends in health consumption.

Insights reveal that by the end of May 2021, health-related consumer spending had increased by 50% year-on-year, giving rise to four emerging schools of thought in the wellness economy: the “Survival Amidst Intense Competition” cohort, the “Appearance Anxiety” cohort, the “Tech-Driven Wellness” cohort, and the “Cultural Renaissance” cohort. Furthermore, health services such as vaccine appointments, medical check-ups, and online pharmaceutical purchases have all experienced hundred-fold growth this year, emerging as dark horses in the new health consumption landscape.

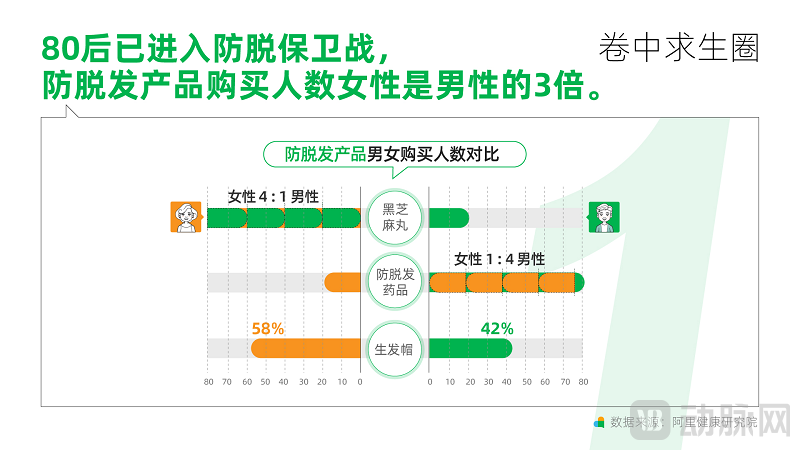

Insights reveal that contemporary professionals widely experience anxiety over hair loss and sleep. Those born in the 1980s have entered a “battle to prevent hair loss.” Surprisingly, women outnumber men by three to one among purchasers of anti-hair-loss products.

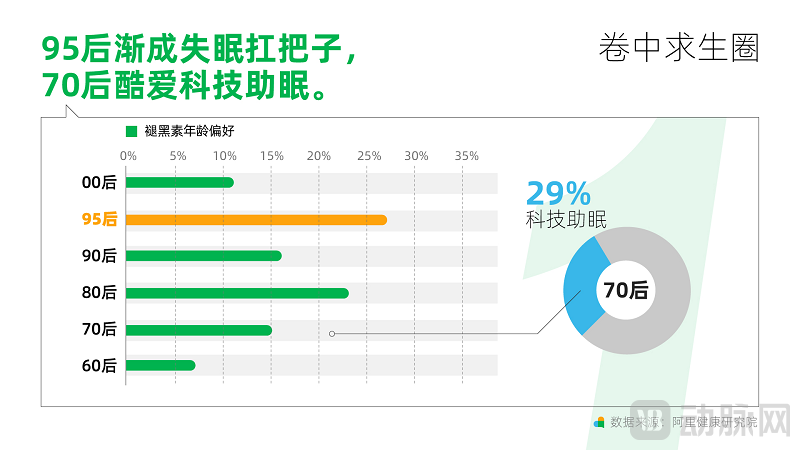

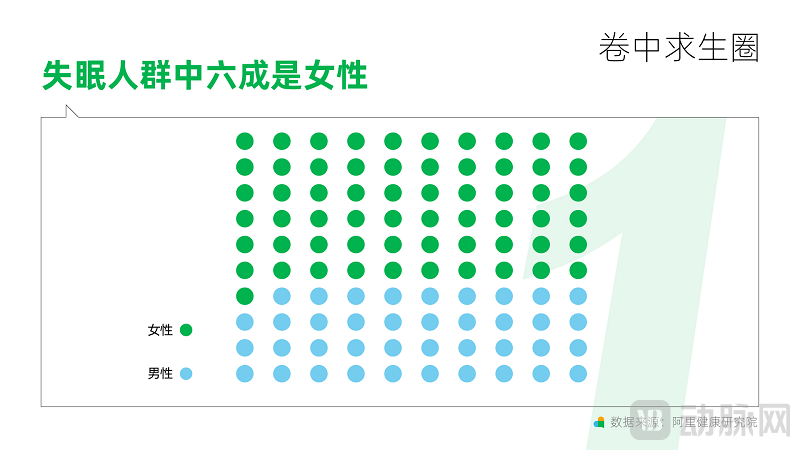

Another major concern for working professionals is insufficient sleep. According to VBInsight, sales of sleep-related products in 2021 surged by 220% year-on-year compared with 2020, with women accounting for 60% of these purchases. In 2021, individuals born after 1995 contributed 30% of melatonin sales, emerging as the group most affected by insomnia. Meanwhile, those born in the 1970s showed a stronger preference for technology-assisted sleep solutions, opting more frequently for novel sleep aids such as anti-insomnia patches and sleep devices.

It can be observed that as the time of working professionals becomes increasingly fragmented, wellness practices are also trending toward fragmentation. According to VBInsight, consumption of ready-to-eat products grew by 56% year-on-year in 2021. Pocket-sized, grab-and-go wellness products such as goji berry puree, instant bird’s nest, and black sesame pills are gaining popularity among young consumers.

Taking Bairuiyuan’s Guo Xiaofan Goji Berry Puree as an example, the Bairuiyuan Tmall Flagship Store, which launched on Tmall in 2003, had become the top seller in the goji berry category by 2016, with its online sales surpassing the RMB 100 million mark for the first time. This year, following the launch of Bairuiyuan’s new goji berry puree product, sales surged by 450%.

Among buyers of goji berry puree, women account for 70%, with post-90s generations showing a particular preference for this product. Additionally, member consumption represents a significant share; members constitute 30% of the goji berry puree user base, and the number of members this year has increased by 40% compared to last year.

Goji berry puree is merely a microcosm of the fragmented wellness practices adopted by professionals in the workplace. As the market expands, an increasing number of new players are gradually entering this space…

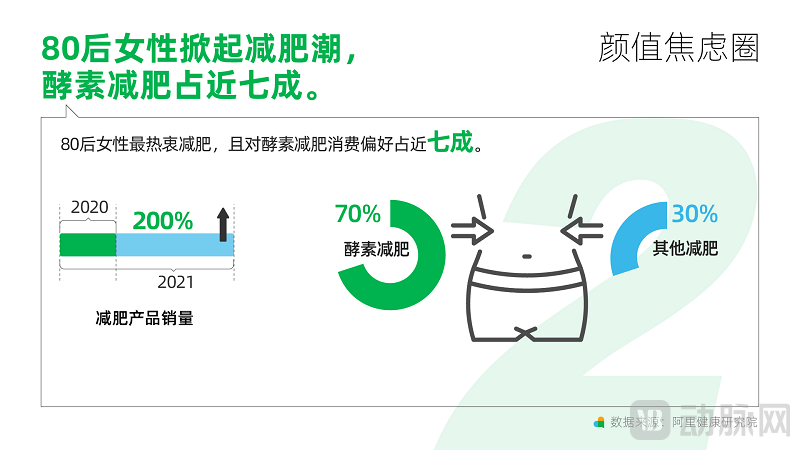

“VBInsight” has found that in the traditional appearance economy sector, sales of weight-loss products surged by 200% in 2021 compared to 2020, maintaining a trend of high growth. However, with the upgrading of the appearance economy, beauty-conscious consumers are no longer satisfied with mere weight loss for aesthetic improvement. Instead, they have embraced a new approach termed “cosmetic-style beautification,” incorporating various cosmetic concepts or ingredients into health products. Cosmetic ingredients and their efficacy have become deeply integrated with wellness practices, emerging as new industry blockbusters.

Taking the Ketang contact lenses launched in March last year as an example, the brand successfully introduced the makeup concept of “highlight” into colored contact lenses, resonating deeply with beauty-conscious consumers and achieving a dual boost in brand equity and sales. During this year’s 618 Shopping Festival, its opening sales surged by 2,500% year-on-year, securing the top spot on multiple leaderboards, including those for premium colored contact lenses. This evolution from “highlight” in traditional cosmetics to “highlight” in contact lenses demonstrates that beauty enhancement through makeup-inspired approaches is becoming increasingly diverse and multifaceted.

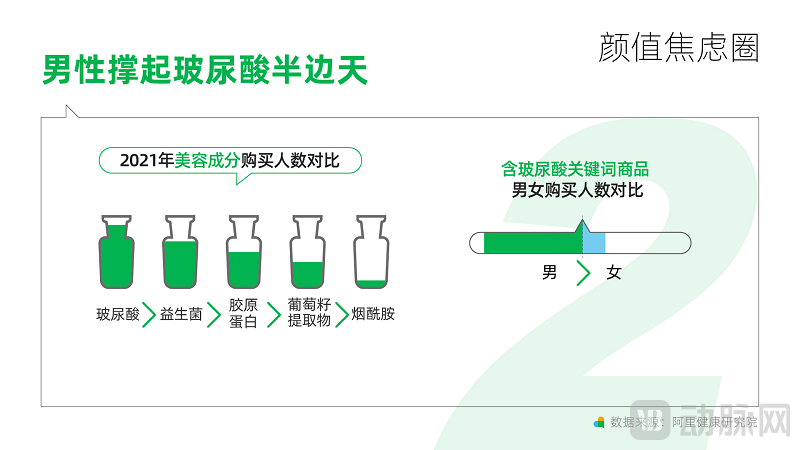

In addition, VBInsight found that the post-80s generation are the most loyal consumers of all beauty ingredients. In terms of spending on products containing “hyaluronic acid,” the number of male consumers is surpassing that of females. The post-00s generation, eager to keep up with beauty trends, shows a stronger preference for grape seed extract.

Interestingly, nicotinamide has emerged as a rising star this year, gaining significant popularity within the health and wellness community. A prime example is Zimeitang’s Nicotinamide “Xiaobai” Drink. Since its founding in 2009, Zimeitang has achieved exponential growth on the Tmall Health Pharmacy platform, with its total store sales in 2021 doubling year-over-year. As a new product launch this year, the Nicotinamide “Xiaobai” Drink is projected to surpass RMB 15 million in sales during Tmall’s 618 Shopping Festival, with its primary consumer base being women born after 1995 and 2000. The novel combination of “nicotinamide + wellness,” representing a “beauty-infused wellness” approach, has become a trendy choice among young, beauty-conscious women.

Technological advancements have, to some extent, catered to the “lying flat” wellness mindset of today’s young generation. With just one minute at home, they can self-test their health status, measuring blood glucose, blood pressure, and uric acid levels all in one step. Health monitoring devices, originally intended for elderly family members, are increasingly favored by younger consumers, thereby expanding the emerging “lying flat” wellness market.

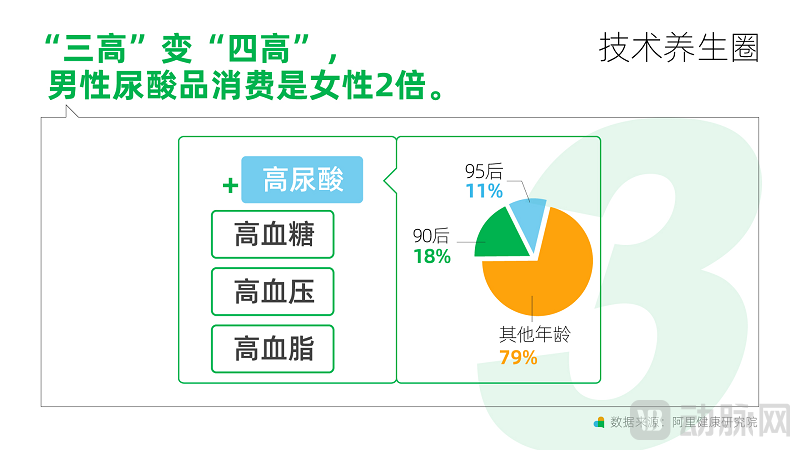

“Insights” has found that uric acid meters are gradually becoming essential high-tech products for home self-testing, following blood pressure monitors and blood glucose meters. In 2021, male purchasers of smart uric acid meters outnumbered females by a ratio of 2:1, and the consumer base is showing an increasing trend toward younger demographics, with those born in the 1990s and 1995–1999 accounting for 18% and 11%, respectively.

Taking Sinocare as an example, since its establishment in 2002, the company has expanded from blood glucose monitoring products to various home-based intelligent self-testing devices, such as uric acid meters, becoming an essential option for “lying-flat” youth to monitor their health without leaving home.

Sinocare’s smart uric acid monitoring products and smart blood glucose products on the Tmall Health Pharmacy platform have consistently ranked first in sales. Notably, in the uric acid monitoring segment, an increasing number of consumers have turned to home-use self-testing devices in recent years in pursuit of more convenient testing options. In 2021, Sinocare’s uric acid meter sales surged by 220% year-on-year compared with 2020, with its smart uric acid products capturing 87% of the market share.

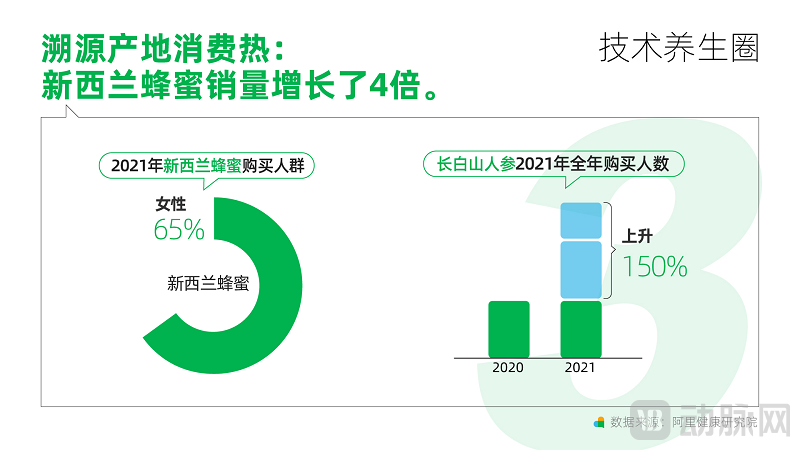

Of course, for tech-savvy wellness enthusiasts, besides their research into cutting-edge products, they are also quite persistent in pursuing high-quality goods from their sources. Ningxia red goji berries, Qinghai black goji berries, Shandong Dong'e donkey-hide gelatin... In 2021, the sales volume of tonics from their original places increased by 60% compared to 2020. The sales volume of New Zealand honey brands from their origin quadrupled, and the number of people purchasing Changbai Mountain ginseng source brands throughout 2021 rose by 150%.

It is not difficult to observe that today’s young people are keeping abreast of the latest technological trends while simultaneously dusting off their parents’ vintage blazers to hit the streets. This fusion of technology and retro aesthetics has unleashed new cultural momentum, driving continuous innovation for brands and industries alike amidst this cultural convergence.

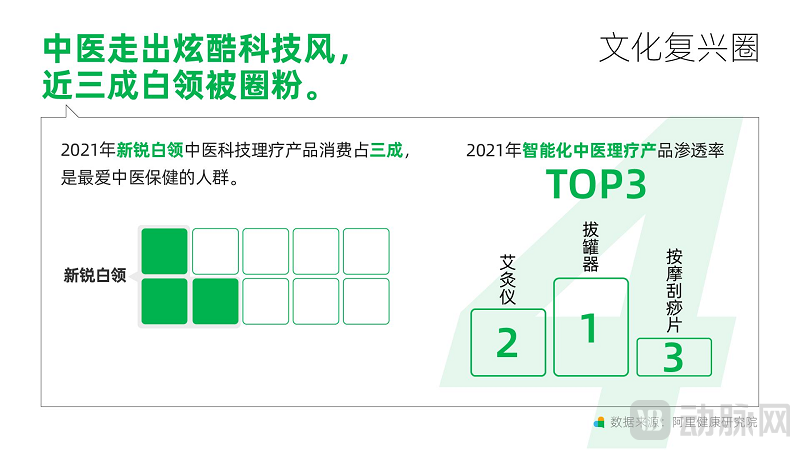

“VBInsight” shows that sales of high-tech TCM physiotherapy products continued to rise in 2021, with the three most popular intelligent TCM physiotherapy devices being cupping devices, moxibustion instruments, and massage gua sha boards. Among these consumers, emerging white-collar workers accounted for 30% of spending on tech-enabled TCM physiotherapy products, making them the demographic most keen on TCM wellness.

Taking the Zuodian brand, established in 2014, as an example, it is an innovative technology brand in the field of smart wellness. By creating a retro-chic aesthetic, it has captured the central spotlight among young consumers. In 2018, its sub-brand Zuodian Xiaoai ranked first in its category on Tmall’s Double 11 Shopping Festival. In 2020, it collaborated with the Palace Museum to launch a special moxibustion gift set commemorating the museum’s 600th anniversary.

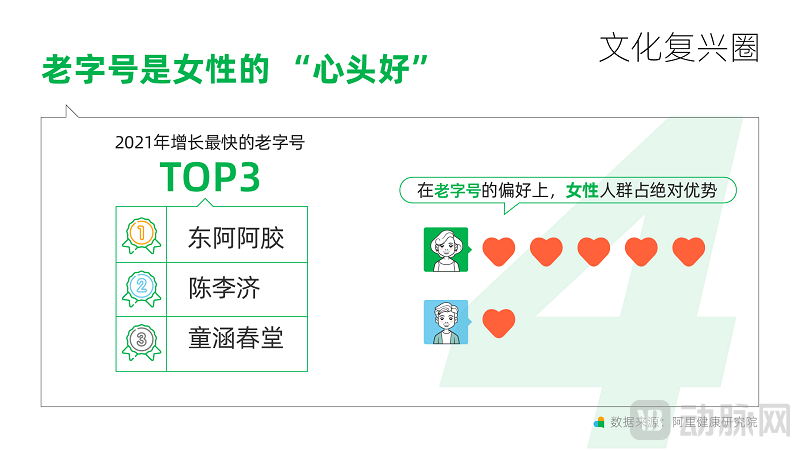

In addition, young consumers also show a preference for time-honored brands. The three time-honored brands with the fastest sales growth are Dong-E-E-Jiao, Chen Li Ji, and Tong Han Chun Tang. Women are more inclined than men to prefer health and wellness products from time-honored brands.

Amidst rapid societal changes, two trends cannot be ignored: the trendification of traditional brands and the retrofication of trendy brands. Innovation is no longer monotonous; with mutual integration becoming the norm, this blend may well emerge as a new approach to health and wellness.

Overall, the record-high sales of health products such as anti-hair loss, anti-insomnia, and anti-aging solutions are positively correlated with the growing health awareness among contemporary consumers. In addition, the Ali Health Research Institute has found that demand for health service products is also surging. In 2021, online appointments for HPV vaccines increased by 550% year-on-year, sales of medical checkup packages rose by 2,700% year-on-year, and sales of prescription drugs and over-the-counter (OTC) medications grew a hundredfold year-on-year. Notably, during this year’s Tmall 618 main event, health service products emerged as dark horses in various livestreaming rooms. According to data from the Ali Health Research Institute, from May 24 to June 3, an average of more than 1,500 key opinion leaders (KOLs) promoted health products daily, representing a threefold increase compared to the same period last year; on average, more than 10 of the top 100 KOLs hosted dedicated health-themed livestream sessions each day, marking a fivefold year-on-year increase.

As terms like “involution,” “lying flat,” and “hyper-parenting” become buzzwords, the living conditions and lifestyles of young people have become a focal point of social discussion, and healthy living has emerged as an essential consumer need for contemporary society. With health-related consumption scenarios continuously expanding, Alibaba Health, as a leader in health consumption trends, is witnessing various schools of wellness economics evolve into emerging mainstream trends within the health sector.