Is Neurointervention Worth the Bet? Over RMB 1.5 Billion Invested in One Year

Capital begins to target the neurointerventional sector.

Since 2020, the concept of neurointerventional therapy has surged in popularity within the capital markets. Not only have listed companies such as MicroPort Medical, Peijia Medical, and Weixin Medical (a subsidiary of Wego Group) flocked to enter the field, but other enterprises—including ZendoVasc, HeartCare Medical, AcoMed, and Vobi Medical—have also secured their entry tickets, having received backing from top-tier venture capital firms and completed multiple rounds of substantial financing.

According to incomplete statistics from VCBeat, at least 24 innovative enterprises and 60 investment institutions have invested in the neurointerventional field in China to date. Since 2020, there have been more than 15 financing events in this sector, with cumulative funding exceeding RMB 1.5 billion. Additionally, Zhejiang Jumpcan Medical Technology has recently passed the listing hearing, with its margin subscription oversubscribed by more than 300 times, demonstrating capital market confidence in the neurointerventional sector.

Publicly listed companies, top-tier venture capital firms, and innovative enterprises are actively positioning themselves in the neurointerventional field. What strategic calculations lie behind their moves? Why did the neurointerventional sector experience an explosive surge starting in 2020? Given that many neurointerventional companies have adopted similar strategies, what will the future market landscape look like?

To address the aforementioned questions, VCBeat conducted research among investment institutions, innovative enterprises, and listed companies, culminating in this article for our readers.

According to incomplete statistics from VCBeat, more than 60 investment institutions, including Hillhouse Capital, Chende Capital, SDIC Innovation, Anlong Fund, Honghui Capital, Sequoia Capital China, Huagai Capital, Lifeline Capital, Qianhai Fund of Funds, and Cowin Capital, have invested substantial amounts in the neurointerventional field, while many other investment firms continue to closely monitor this sector.

An anonymous source from a financial advisory (FA) firm revealed, “Over the past two years, the neurointerventional field has garnered significant attention. Companies in this sector are highly favored by numerous investment institutions, with intense competition even emerging as multiple firms vie for equity stakes in leading neurointerventional companies.”

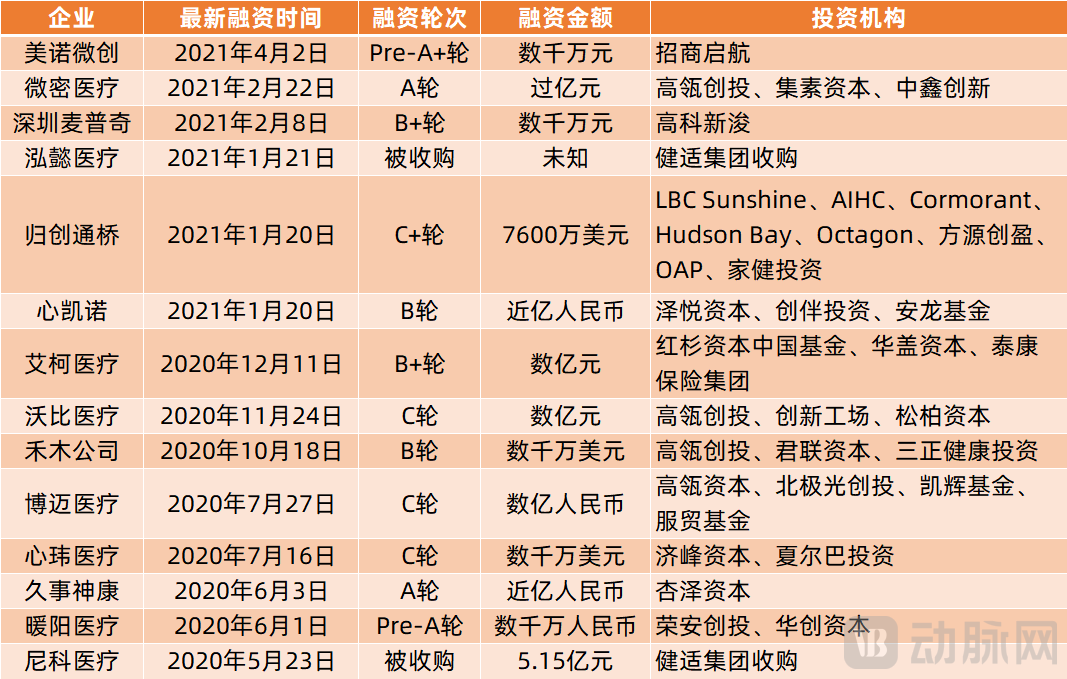

(Neurointerventional financing and investment events, compiled by VCBeat. Please contact the author if any are omitted.)

The neurointerventional field has garnered significant attention due to its large market size, rapid growth rate, upstream technology-driven development, and national policy support. Furthermore, there is a high probability that the neurointerventional sector will replicate the path of import substitution seen with coronary stents. Currently, the market, capital, and policy environments for the neurointerventional industry are more favorable than those of the coronary stent sector two decades ago.

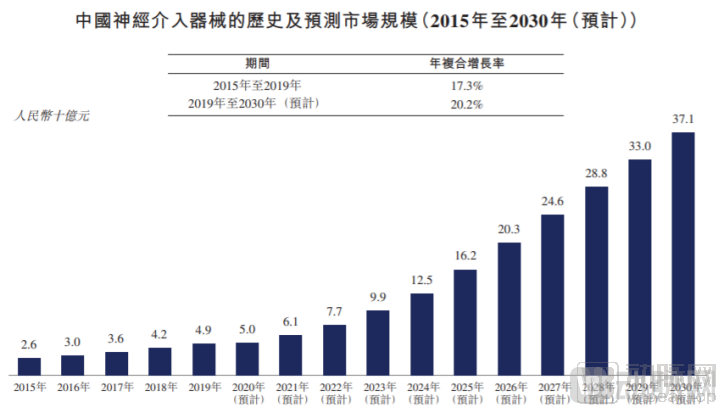

In terms of market size, the prospectus submitted by Jointcare Medical shows that China’s neurointerventional medical device market grew from RMB 2.6 billion in 2015 to RMB 4.9 billion in 2019, representing a compound annual growth rate (CAGR) of 17.3%. It is projected to further increase to RMB 37.1 billion by 2030, with a CAGR of 20.2% from 2019 to 2030.

(Historical Overview and Projected Market Size of Neurointerventional Devices in China; Data Source: Prospectus of Zebra Medical)

The vast market potential is underpinned by a large patient population.The "Report on Cardiovascular Health and Diseases in China 2019," released by the National Center for Cardiovascular Diseases, shows that there are 13 million stroke patients in China, with approximately 2 million new cases annually. In 2019, cerebrovascular diseases accounted for more than 20% of all deaths among Chinese residents. Due to the large patient population and high mortality rate, cerebrovascular diseases such as stroke are receiving increasing attention, and the ensuing rise in health awareness will further drive the expansion of the neurointerventional market.

An investor who has long followed the neurointerventional field told VCBeat, “Currently, China has a large number of stroke patients, and there remain significant unmet clinical needs. This is one of the key reasons why investment firms are optimistic about the neurointerventional sector. In addition, the sustained high-speed growth of the neurointerventional market is another factor driving investor confidence. According to multiple data sources, including market research and third-party industry reports, the ischemic segment of the neurointerventional market is expected to maintain an annual growth rate of over 25%–30%.”

The sustained rapid growth of the neurointerventional market is driven by the rising prevalence of stroke and the widespread adoption of neurointerventional techniques. The latest population data released by the National Bureau of Statistics shows that China’s population aged 60 and above exceeds 264 million, accounting for 18.7%, while those aged 65 and above number 190 million, representing 13.5%. According to data from the National “Stroke High-Risk Population Screening and Intervention Program,” the prevalence of stroke among individuals aged 40 and above increased from 1.89% in 2012 to 2.32% in 2018, with the number of patients reaching 13.18 million. Moreover, stroke incidence is showing a trend toward affecting younger populations. It is evident that, influenced by population aging and the younger age of onset, stroke will maintain a high prevalence rate in China.

From the perspective of the promotion and widespread adoption of neurointerventional techniques, neurointerventional procedures have been extensively applied in clinical practice over the past two years. Chen Chong from Zhongtian Medical stated, “Neurointerventional procedures for ischemic stroke are developing rapidly, with a significant increase in surgical volume. Currently, some county-level hospitals in China are already capable of performing neurointerventional procedures to treat patients with ischemic stroke. It is believed that, with further technology dissemination, an increasing number of primary-care hospitals will be able to offer these interventions in the future.”

The third reason why investment institutions are bullish on the neurointerventional field is the continuous innovation in upstream technologies, with technology-driven products progressively revolutionizing the treatment of cerebrovascular diseases. For instance, the shift from open surgery to minimally invasive therapy, from mechanical thrombectomy to aspiration catheter thrombectomy, and the extension of the therapeutic window from 6 hours to 48 hours—each technological innovation and product launch has advanced treatment modalities. Moreover, the clinical efficacy of these innovative therapies is non-inferior to, and often superior to, the previous gold standard. These continuously evolving innovative technologies also present significant growth opportunities for the neurointerventional industry.

From a macro perspective, the Chinese government attaches great importance to cerebrovascular diseases such as stroke, providing substantial financial and policy support. For instance, the country is actively promoting the establishment of Stroke Centers to meet the needs of stroke patients who require rapid treatment due to the fast onset of symptoms and narrow therapeutic time windows.

Taking these factors into account, more than 60 investment institutions have already bet on the neurointerventional field, with many more preparing to enter the market.

So, is now the right time to enter?

An investor told VCBeat, “Currently, capital surplus has driven up corporate valuations, resulting in a certain degree of premium. However, historically, high-quality companies have not only generated substantial profits in the primary market but also continued to deliver solid investment returns in the secondary market. Therefore, even with a current valuation premium of 10%–20%, these companies still hold investment value. We believe that neurointerventional companies are growing at an annual rate of over 30%, and their true value will gradually be realized in the coming years. The only consideration for investment institutions is how to identify and invest in the right neurointerventional companies.”

Zhao Han, Investment Director of Shaanxi Investment Capital Growth Fund, expressed his agreement: “From a long-term perspective, the rising incidence of cerebrovascular diseases driven by population aging, coupled with the enhanced clinical benefits for patients offered by innovative interventional devices, will inevitably accelerate the development of the neurointerventional industry. High-quality investment targets will also deliver substantial returns to investors. If short-term gains are the priority, it is essential to comprehensively consider valuation levels and capital exit strategies. For Shaanxi Investment Capital, we view the neurointerventional sector as a track with immense growth potential, and we are confident that leading companies in this field will achieve robust development.”

VCBeat’s statistics reveal that the neurointerventional sector has remained a hot spot in the capital market since 2020. So, why did this surge begin in 2020? And how long will the neurointerventional field continue to thrive?

An anonymous investor told VCBeat, “The increase in financing and investment activities in the neurointerventional field since 2020 is mainly due to factors such as the implementation of centralized procurement for high-value consumables, the rapid growth rate of neurointerventional procedures, the trend toward domestic substitution, the demonstrated clinical efficacy of neurointerventions, competition among companies within the sector, and herd behavior among investment institutions.”

First, in 2020, the Chinese government launched centralized volume-based procurement (VBP) for high-value medical consumables. In November, the national VBP for coronary stents was implemented, resulting in an average price reduction of over 90%. This suddenly dampened the coronary intervention sector, which had remained hot for more than a decade, prompting investment institutions to gradually shift their focus to other areas. The VBP for coronary stents and subsequent policies demonstrate the government’s firm determination to regulate high-value consumable prices against the backdrop of broader healthcare cost containment. Judging by subsequent provincial alliance VBP initiatives, centralized procurement of high-value consumables will become normalized and continuous. Based on the categories selected for VBP at both the provincial alliance and national levels, products such as coronary balloons, intraocular lenses, surgical staplers, and orthopedic consumables have been included. Meanwhile, the future price trends for drug-coated balloons and peripheral intervention consumables do not look promising.

Zhao Han from the Growth Fund of Shaanxi Investment Capital, who has long studied and focused on the field of neurointervention, stated: “Under such circumstances, investment institutions need to seek new investment directions. Due to early-stage development accumulation, the neurointervention sector has achieved breakthrough progress in clinical outcomes and product advancement. Consequently, the neurointervention field is increasingly coming into the spotlight for investment institutions.”

Secondly, the volume of neurointerventional procedures is growing rapidly, and the neurointerventional market is projected to maintain an annual growth rate of over 25%-30%, indicating significant investment value. Chen Chong from Zhongtian Medical corroborated this, stating, “Data from market research and third-party industry reports show that in the past two years, the volume of neurointerventional procedures, particularly in the ischemic segment, has increased substantially.”

Third, the neurointerventional market in China is currently dominated by foreign enterprises such as Medtronic, Johnson & Johnson, and Stryker, which collectively hold a 93% market share, while domestic companies are building complete product portfolios from scratch. Based on the development history of individual medical devices, localization of neurointerventional devices is inevitable, leading to the replacement of imported products. Under this overarching trend of import substitution, certain neurointerventional companies are poised for leapfrog growth, presenting strong appeal to investment institutions.

Fourth, numerous domestic innovative enterprises in the neurointerventional field have been intensively engaged in R&D and technological reserves for neurointerventional products. Many of these products have advanced to clinical stages, with several companies already obtaining medical device registration certificates for products such as coils. On the other hand, the clinical efficacy of neurointerventional procedures has been validated both domestically and internationally, and they have become recommended therapies in stroke prevention and treatment guidelines worldwide. Meanwhile, domestically produced neurointerventional products have gradually matched the quality of imported counterparts, demonstrating favorable outcomes in clinical practice. Zhao Han from Shaanxi Investment Capital Growth Fund stated, “From the perspectives of product development progress and clinical efficacy, 2020 presented an excellent opportunity for investment and strategic positioning in the neurointerventional sector.”

Fifth, from the perspective of startups, amid the wave of domestic substitution and technological innovation, numerous neurointerventional companies broke through technical barriers around 2020, achieving the research, development, and production of products such as balloons and catheters. On the other hand, the national regulatory authorities have lowered the market entry thresholds for neurointerventional devices; for instance, Class II passive products under Subcategory 03 (Neurological and Cardiovascular Surgical Instruments), including occlusion balloon catheters and distal protection devices, are exempt from clinical trials. This has significantly shortened the time-to-market for neurointerventional products and reduced costs for neurointerventional enterprises. Such policy requirements have also accelerated the development of the neurointerventional field, bringing it more rapidly into the focus of investment institutions.

Sixth, the neurointerventional field began to heat up in 2020, which was partly driven by intensifying competition among companies within the sector and the herd mentality of investment institutions. An anonymous investor told VCBeat, “When a company in the neurointerventional space secures financing and achieves accelerated growth, its competitors are compelled to initiate their own fundraising rounds under competitive pressure. Consequently, other players in the field will also actively pursue financing to avoid falling behind their rivals. As for investment institutions, some lack a deep understanding of the neurointerventional sector or have not clearly identified its development trajectory; nevertheless, they follow the lead of prominent venture capital firms and join the ranks of investors bullish on the neurointerventional field.”

Seventh, with the listing or IPO filings of neurointerventional companies such as MicroPort NeuroTech, Peijia Medical, and Genesis MedTech, the industry has demonstrated robust exit channels.

In light of the aforementioned factors, the neurointerventional field began to attract significant favor from the capital market in 2020. Meanwhile, numerous drivers—including policy support, technological innovation, market education, product development progress, and the trend toward domestic substitution—are unlikely to change in the short term. Indeed, certain factors such as technological innovation and product advancement are poised for even stronger growth. Therefore, it can be projected that the neurointerventional sector will maintain robust development over the coming years, with its position in the capital market becoming increasingly solidified.

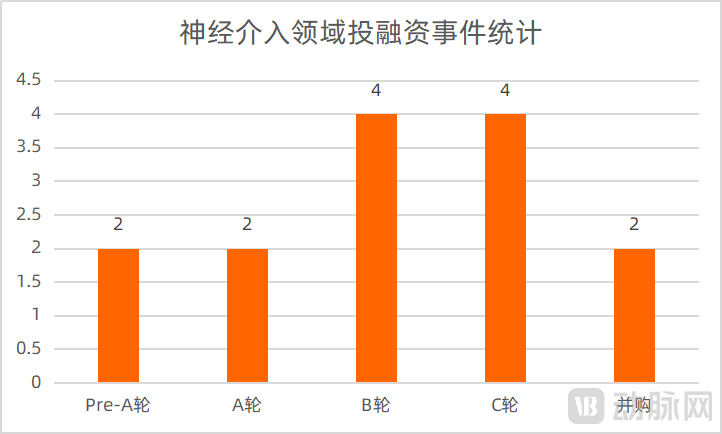

Based on an analysis of current investment and financing activities in the neurointerventional sector, approximately 30% of companies have completed Series B or C funding rounds, while about 17% are at Series A or earlier stages. These data, combined with industry development trends, indicate that the neurointerventional field is progressing smoothly. Leading companies such as MicroPort NeuroTech, Xinwei Medical, Peijia Medical, and Genesis Medtech have established themselves in the first tier, either already listed or preparing for initial public offerings. Companies that have completed Series B or C financing are closely following behind, while those at the Series A stage may accelerate their growth by leveraging differentiated innovative products.

(From 2020 to June 18, 2021, statistics by VCBeat)

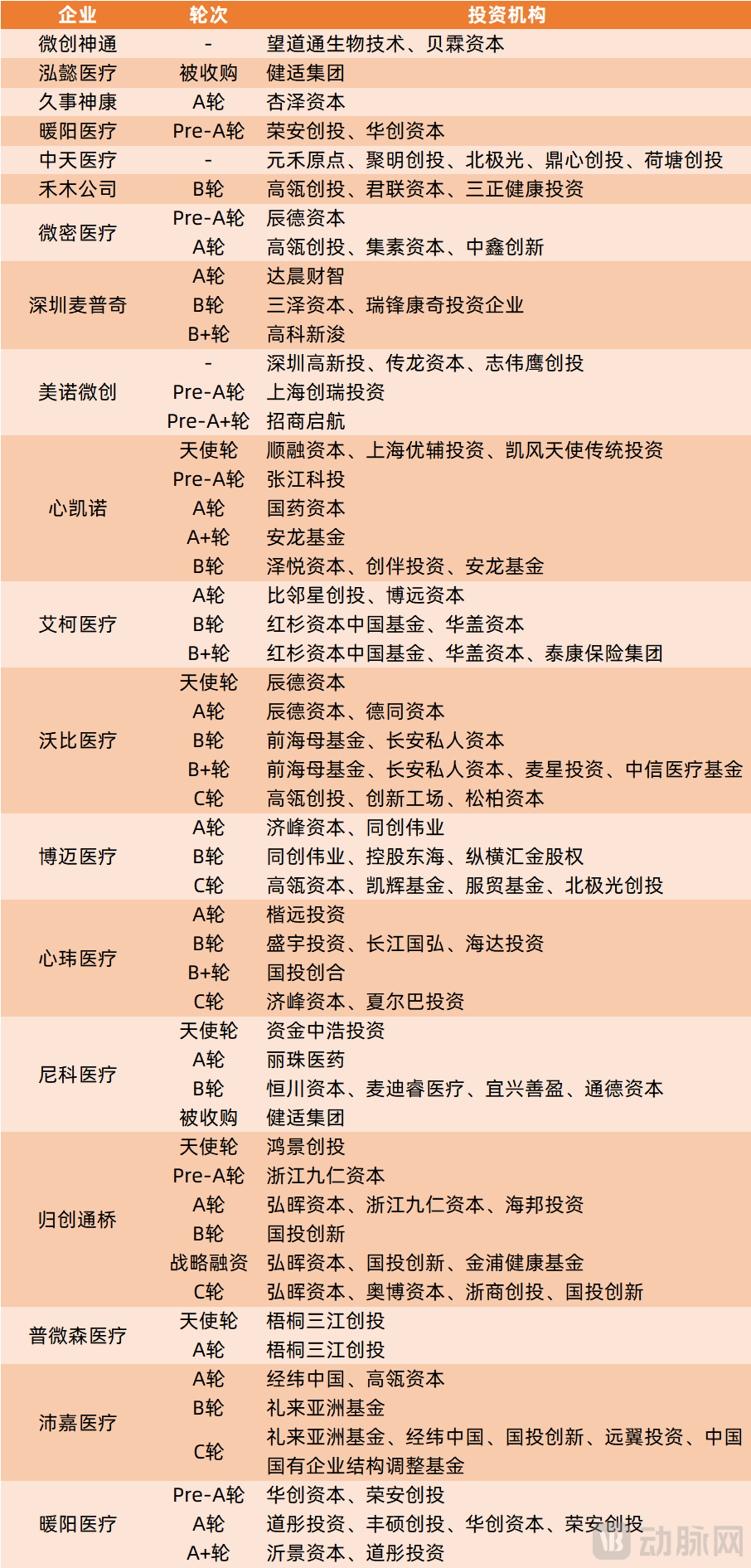

Meanwhile, a statistical analysis of investment activities reveals that Hillhouse Capital has been the most active investor in the neurointerventional sector, backing companies such as Hemu Medical, Weimi Medical, Wobi Medical, Bomai Medical, and Peijia Medical. Sequoia Capital has maintained a strong bullish stance on Aike Medical, while Matrix Partners China and Lilly Asia Ventures have both expressed consistent confidence in Peijia Medical, continuing to increase their investments.

VCBeat Consults Investors in the Neurointerventional Sector: How to Select Neurointerventional Companies for Investment? Investment Firms Give a Surprisingly Consistent Answer: Products.

An investor stated, “The neurointerventional field is primarily subdivided into hemorrhagic and ischemic categories. We first select companies within these subsectors that demonstrate exceptional product innovation capabilities and superior clinical outcomes, and then consider their comprehensive core competitiveness. In the medical industry, product quality is paramount. In future competition characterized by homogenization, inferior products will inevitably be eliminated by the market. Beyond product innovation and a company’s R&D strength, we also focus on comprehensive competitive advantages, including long-term strategic planning, platform-based design, the team’s vision and perspective, their dedication to technology and understanding of the industry, patent portfolio layout, and execution capability. Additionally, we pay close attention to more cutting-edge and innovative products and therapeutic approaches, specifically those that serve as substitutes for existing market offerings.”

Zhao Han of Shaanxi Investment Capital Growth Fund candidly stated, “Our primary criterion for target screening is to select teams with a global perspective and products that demonstrate breakthrough innovation in the neurointerventional field. We also place significant emphasis on companies’ product pipeline layouts and strategic planning. Currently, under the pressure of centralized volume-based procurement (VBP) for high-value medical consumables, innovation is the key factor enabling sustainable corporate growth. A diverse product portfolio ensures resilience—‘if one avenue fails, another may succeed’—allowing companies to exchange price for volume through VBP while securing high-margin profits from innovative products.”

VCBeat’s statistics reveal that at least 24 companies are currently deeply engaged in the neurointerventional field, with most adopting a platform-based development model and offering comprehensive portfolios of neurointerventional products.

With the rapid advancement of various companies, a large number of neurointerventional products are expected to hit the market before 2023. This will lead to intense competition for most companies right from the product launch, and more seriously, there is a potential for centralized procurement of neurointerventional products at any time in the later stages.

In this regard, investors believe: “Currently, competition in the neurointerventional field is disordered, which we define as Competition 1.0. In this phase, the core objective for companies is to obtain medical device registration certificates as quickly as possible. At present, many enterprises are pursuing platform-based development strategies. Furthermore, since certain devices are exempt from clinical trials, investors sometimes find it difficult to assess the true value of these companies. However, once products receive approval and begin to enter the market, Competition 2.0 commences. In this phase, the core objective for companies is to gain market recognition, secure high-level profits, and capture market share. Compared to Phase 1.0, Competition 2.0 is more brutal, with product quality being the ultimate determinant. In the neurointerventional field, clinical demands for product quality are high; inferior products will inevitably be gradually eliminated from the market, resulting in natural selection where the superior survive. Therefore, the future market landscape will be shaped by the combined effects of product approval timelines and product quality.”

Therefore, investors place greater emphasis on a company’s products and innovation capabilities, while market and marketing capabilities serve as supplementary factors. As one investor stated, “Market and marketing efforts correspond to close-quarters combat, addressing immediate survival needs, whereas innovation is the key to resolving long-term development challenges.”

So, how will the landscape of the neurointerventional market evolve in the future? How should innovative enterprises respond to market changes?

Investors believe that in the short term, the neurointerventional market will exhibit a diverse and competitive landscape, with companies leveraging their respective resources to capture market share. However, as time progresses, the relative merits and drawbacks of each company’s products will become increasingly apparent. At that stage, the market will naturally favor high-quality products while eliminating weaker players, leading to gradual market consolidation among top-tier enterprises that will firmly dominate the neurointerventional sector.

Amidst homogeneous competition, innovative enterprises also have opportunities for development. For instance, companies can optimize, iterate, and update their offerings to address clinical pain points, or directly engage in innovative product R&D. Through differentiated innovation, enterprises can meet specific market demands and thereby seize opportunities for growth.

Vobi Medical acknowledged this, stating: “To address future homogeneous competition, Vobi has adopted a three-pronged strategy. First, we enforce strict quality management to ensure our products and services reach industry-leading standards. Second, we pursue globalization, leveraging our international R&D team and sales talent to export our products overseas. Third, we commit to innovation, striving for originality rather than imitation in the face of homogeneous competition.”

Therefore, in the current market environment, small enterprises have their own paths to survival and development, while large enterprises have their own growth trajectories. As for which neurointerventional company will emerge as the industry leader, only time will tell.