Return to Value-Based Healthcare: An Analysis of PBM Medication Cost-Control Strategies

Article selected from the WeChat official account: Jiong Shen Product Perspective, Author: Jiong Jiong Tong Xue, published with authorization from VCBeat.

This chapter serves as the concluding section on returning to value-based healthcare, primarily introducing Pharmacy Benefit Management (PBM) drug cost-control strategies. It is well known that once patients are diagnosed with a disease, the largest portion of treatment expenses often lies in medications and medical supplies. The financial burden is particularly significant for chronic and severe conditions, due to both their prolonged duration and high instantaneous costs. Are there currently any effective healthcare payment models, either domestically or internationally, that can provide patients with relatively reliable coverage while simultaneously reducing their out-of-pocket pharmaceutical expenditures? The following discussion will introduce the PBM model.

When addressing this issue, it is essential to mention Pharmacy Benefit Management (PBM). Emerging in the United States during the 1960s, PBM refers to a category of intermediary management and coordination organizations that operate among patients, insurance providers, pharmaceutical companies, hospitals, and pharmacies.

The primary objective is to control healthcare costs, reduce patient expenditures, improve the efficiency of medical insurance resource utilization, and enhance pharmaceutical benefits, all without compromising the quality of medical services. The core revenue model essentially consists of charging patient management fees, earning margins from pharmaceutical distribution, and receiving rebates.

PBM companies first negotiate with pharmaceutical manufacturers to secure a 3% discount on drug prices. Additionally, upon reaching certain sales thresholds, they receive a 2% rebate on sales revenue from the manufacturers (in the United States, such rebates are legal and therefore permissible; some PBM companies pass these savings on to patients or employers, further reducing drug costs). Finally, they charge employers or patients a 1% membership fee, resulting in an overall profit margin of approximately 6%.

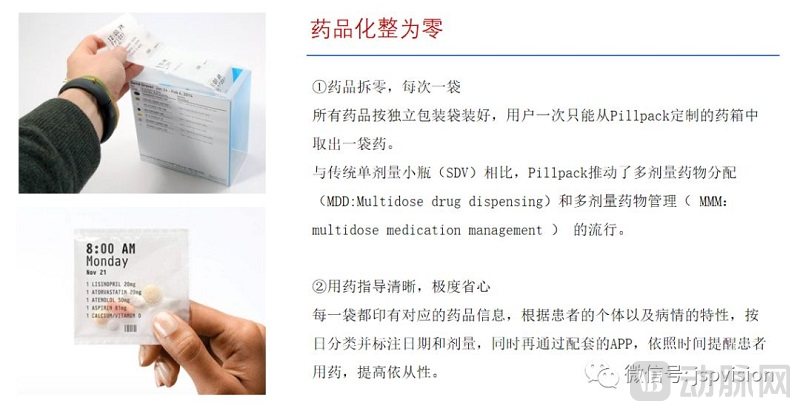

According to earlier U.S. statistics, following the emergence of Pharmacy Benefit Managers (PBMs), consumers’ out-of-pocket cash payments dropped from 96.2% in 1960 to 26.6% in 1998, with the majority shifting to PBM-facilitated payment and reimbursement systems. This transition effectively curbed the rapid growth trend in healthcare and pharmaceutical costs. In the early days, Medco Health Solutions was the largest U.S.-based PBM that did not include mail-order pharmacy services. Later, with the development of internet-based healthcare, online prescription mail-order services emerged, with PillPack standing out as a representative innovator in this sector.

They also offer medication repackaging services, splitting multiple prescribed drugs into individual doses and combining them into single-dose packages to simplify administration for patients and improve medication adherence.

PBM demonstrates particularly significant benefits for patients on long-term medication for chronic diseases, as the inherent nature of chronic conditions necessitates ongoing pharmacological dependence. Consider an offline medication purchase scenario: Due to their long-term medication needs, chronic disease patients regularly visit designated brick-and-mortar pharmacies to “purchase medications” based on their prescriptions. These pharmacies can be regarded as forward-deployed drug warehouses for PBM companies. Patients are required to submit their electronic prescriptions to the PBM company for prior review, with the primary criteria for assessment being:

① Whether medication adjustment is necessary, based on the patient’s prior medication history and current physical condition;

② The patient's current medical insurance status and whether it is in a payable state;

③ Whether the drug offers the optimal balance of price and efficacy within the configurable formulary;

Especially the last point, which is key to cost control. If there are drugs with the same efficacy but at a lower price, substitution is recommended. The medications can be prepared in advance for patients to pick up at pharmacies. Patients pay the co-pay portion directly to the pharmacy, while the remaining costs are reimbursed by commercial insurance or social security (in the U.S., social security refers to Medicare and Medicaid). This system is quite similar to China’s basic medical insurance.

In summary, from a macro perspective on healthcare expenditures, the greatest value of PBMs lies in controlling drug costs, while their diversified profit models are also highly favored by the market.

This is critically important for patient value and Pharmacy Benefit Managers (PBMs), with the primary implementation framework comprising the following four key points:

● Collaborate with relevant medical institutions, academic colleges, and research entities to develop a formulary (somewhat analogous to China’s National Reimbursement Drug List for essential medicines; in effect, it serves as a directory established by non-governmental commercial organizations); mandate that all healthcare providers partnering with the PBM select medications exclusively from this formulary, otherwise claims will not be reimbursed;

● Approval of patients’ medication access rights: In cases involving special medication circumstances, such as new drugs or medications not included in the current formulary, submission for approval is required. A joint review panel comprising the Pharmacy Benefit Manager (PBM) and the insurance provider will conduct the evaluation. Reimbursement eligibility will be determined following the completion of the secondary review. During the selection process, efforts will be made to minimize the use of high-cost medications with limited clinical efficacy.

● Warning on combination drug therapy: After a physician issues a prescription, it should be uploaded to the Pharmacy Benefit Manager’s (PBM) prescription review system to assess potential drug interactions and adverse effects. Such systems, which include prospective prescription review and dual-signature authorization by both physicians and pharmacists, are already implemented in existing hospitals to ensure medication safety for patients.

● Control the overall volume of prescriptions to avoid excessively large ones; encourage physicians to resolve issues with smaller prescriptions. For large prescriptions, individualized consultation between physicians and pharmacists is required to reach a consensus on management.

Generally, patients enrolled in the PBM system bring with them extensive medical records and prescription data, which provides a foundation for PBM companies to design long-term, dynamic health monitoring mechanisms tailored to populations with specific diseases. Common management approaches include:

● Invite doctors and pharmacists to provide long-term health education to patients, enhancing their understanding of diseases;

● Health monitoring, including daily records of patients' blood glucose, blood pressure, diet, and exercise, with comprehensive recommendations to help patients maintain their health;

● Some patients are prone to missing or forgetting doses; medication reminders can be implemented to improve adherence to a certain extent, thereby reducing the risk of severe illness.

● Promptly identify and report any abnormal physical symptoms, and communicate with the attending physician;

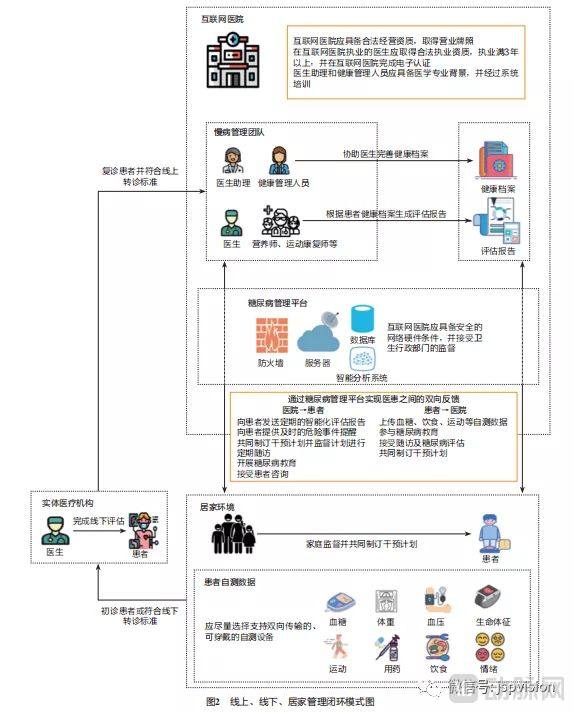

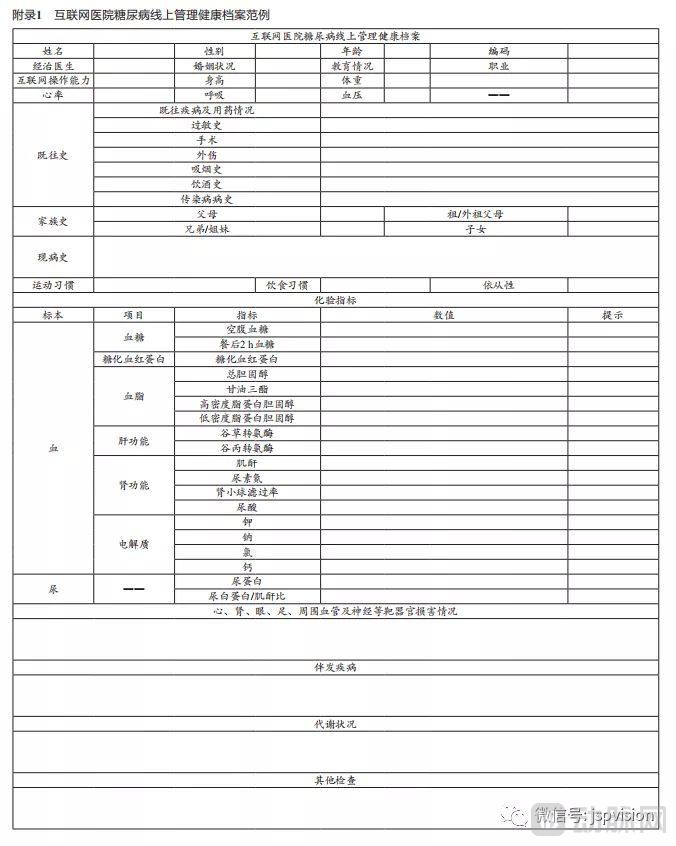

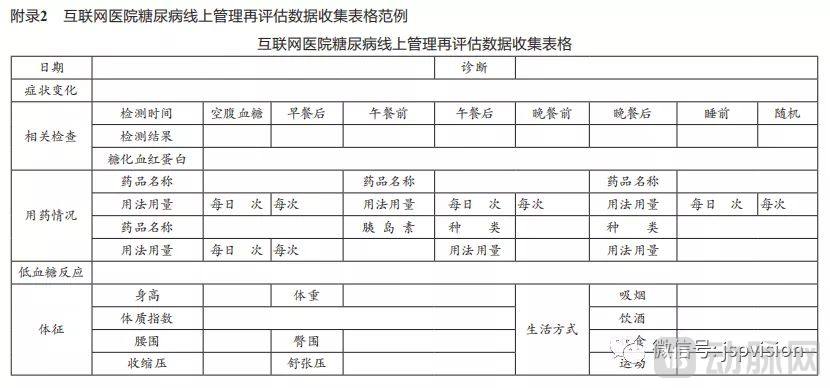

Taking the diabetes management model in the following internet hospital as an example, it basically follows the disease management service process:

Relevant health record data of the patient needs to be collected:

Disease Control Assessment Data:

Note: The management protocol is derived from the Chinese Expert Consensus on Online Management of Diabetes in Internet Hospitals.

PBMs have designed different payment models for various types of prescription scenarios:

● Product restrictions: Different reimbursement ratios are established for originator drugs and generic drugs that have passed the consistency evaluation, with a recommendation to prioritize the use of generic drugs and lower-priced unbranded generics;

● Single-product restriction: The insurance reimbursement rate is dynamically adjusted based on negotiation outcomes with pharmaceutical companies; any excess cost is borne by the patient.

● Total amount limit: The proportion and amount covered by insurance within the total medication cost are capped; any expenses exceeding this limit must be paid out-of-pocket by the patient.

In summary, the core advantage of PBM lies in saving money—saving money, saving money! (emphasizing this crucial point three times)—while ensuring the quality of medical services.

If DRGs are primarily cost-containment organizations serving the public health insurance sector, then PBMs can be essentially equated with cost-containment organizations serving the commercial insurance sector. The former focuses more on cost control during the treatment and medical service delivery phase, while the latter adds supervisory cost control over medication management in disease care. However, in essence, DRGs are a classification standard, whereas PBM is merely a service model; the two can be combined and utilized together. DRGs can be applied to commercial insurance, and the PBM model can also be adopted by public health insurance. For instance, the national “4+7” centralized drug procurement policy currently being implemented is, in effect, a form of PBM that leverages volume to negotiate lower prices from pharmaceutical manufacturers, representing a partial adoption of the PBM model. Therefore, I believe that PBM will become a major direction for all future medical insurance organizations, whether public or commercial, as it is indeed a win-win model that promotes value-based healthcare.

Currently, the U.S. Pharmacy Benefit Manager (PBM) market is primarily divided into three mainstream models. The first model consists of pure-play PBM companies that build their own channels by collaborating with external drug distribution networks. These entities are essentially pure information technology companies, represented by ESI (Express Scripts Holding Company), which controls costs through standardization and informatization. The second model enters the market from the insurance sector, leveraging years of accumulated industry resources and a large user base to create a “PBM + Insurance” model. This approach is exemplified by UNH (UnitedHealth Group), which has established a closed loop for insurance payments. The third model enters from the terminal drug distribution sector, such as CVS Caremark, the largest retail pharmacy chain in the United States. By implementing centralized procurement, it squeezes the profit margins of upstream pharmaceutical manufacturers. Later, through collaboration with the second-largest PBM company in the U.S., it created an integrated “Pharmacy + PBM + Insurance” model.

Currently, the U.S. market leader is the independent third-party company ESI, with approximately 34% market share, followed by CVS Health’s Caremark at 26%. Ranked third is OptumRx, affiliated with UnitedHealth Group, the largest U.S. commercial health insurer, holding a 12% market share. Together, these three companies account for over 70% of the PBM market.

Express Scripts Holding Company (ESI), the largest pharmacy benefit manager (PBM) in the United States and a Fortune 100 company, has handled over 1.4 billion prescriptions annually since 2017, with its market share continuously increasing. In 2018, it was acquired by the health insurance giant Cigna Group for $52 billion. ESI provides commercial insurers with pre-payment health data collection services. On the medical and pharmaceutical utilization front, it influences medication choices by intervening in healthcare provider practices, reducing unnecessary diagnostic and treatment procedures, formulating covered drug formularies, and selecting cost-effective equivalent medications. Additionally, ESI leverages centralized procurement to lower overall drug purchase prices, thereby reducing health insurance expenditures. ESI’s primary revenue models include the following aspects:

(1) For pharmaceutical companies: ESI directly procures drugs from upstream entities (manufacturers and pharmacies) at lower prices, earning revenue through distribution service fees and price differentials.

(2) Insurance Services: Assisting insurance companies with underwriting, claims processing, and payments; designing medical insurance plans for diverse population segments; providing support through a multivariate cost prediction and simulation system; managing drug reimbursement formularies, clinical pathways, and payment models; and charging service fees to insurance companies.

(3) For patients: ESI assists patients with appointment scheduling, physician consultations, health interventions, and science-based health education services, charging a health management service fee.

(4) For hospitals: Provide monitoring and evaluation of medical service data, including physician evaluations, analysis and comparison of physicians’ prescribing patterns, and recommendations for reducing medication costs.

UnitedHealth Group (UNH) is the largest health insurer in the United States, with OptumRx, a pharmacy benefit manager (PBM), operating as one of its Optum subsidiaries. In 2018, OptumRx generated $69.544 billion in revenue, accounting for 37.9% of UNH’s total revenue, representing a year-over-year increase of 9.1%. Throughout the year, it processed 1.34 billion prescription claims, managed $91 billion in healthcare expenditures, and provided PBM services to over 65 million individuals.

OptumRx’s revenue model is similar to that of ESI, encompassing retail pharmacy network management services, mail-order and specialty pharmacy services, pharmaceutical manufacturer discount contracting and administration, benefit plan design and consulting, claims management, certain Medicare-related services, as well as clinical programs for prescription adherence and regulatory compliance, medication review, and disease state medication therapy management services.

CVS Health (CVS), the largest chain of retail pharmacies in the United States, offers services such as insurance plan consultation, claims management, and mail-order pharmacy, in addition to the two models mentioned above. Leveraging its extensive and readily deployable offline pharmacy network, CVS has upgraded a portion of its retail locations into “MinuteClinics,” with over 1,100 such clinics currently in operation. Patients can receive a comprehensive range of services directly at these pharmacy-based clinics, including physical examinations, diagnosis and treatment of minor and common conditions, health consultations, and prescription dispensing. This integration has enhanced customer satisfaction and strengthened patient loyalty to its pharmacies. On one hand, it has generated additional revenue from healthcare service delivery; on the other, due to its scale as a national pharmacy chain, CVS commands greater bargaining power with upstream pharmaceutical manufacturers, resulting in higher profit margins.

In summary, although different players enter the PBM market from varying angles, they ultimately converge on the same model centered around the integration of “healthcare, pharmaceuticals, and insurance.” Many domestic institutions in China are also emulating and experimenting with these approaches. For instance, following the Pillpack model mentioned earlier, a Chinese company named “Wanhu Liangfang” is operating in this space; similarly, Yuanyao Lianhe (PharmaUnion) is adopting the ESI model. In fact, many enterprises have already accumulated the foundational capital necessary for PBM operations, but their progress has been relatively slow due to various policy and market constraints. Basically, it can be said that for every PBM direction implemented in the United States, there are companies in China pursuing similar paths; we are simply unaware of them due to our limited visibility at present.

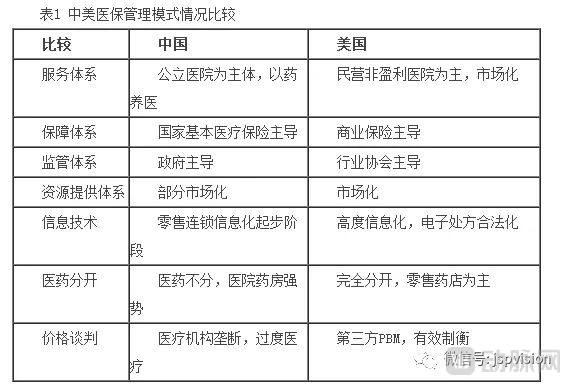

Finally, let’s discuss why there is such strong resistance to promoting PBM. Regarding the differences in the current status between China and the United States, I believe the core issue lies in the differences in national conditions, macro-environments, and stages of development:

PBM requires a data foundation, as well as standardization and interoperability, for effective healthcare cost containment and disease management. Without such data, implementing PBM is untenable. PBM companies need to leverage data models to monitor physicians’ treatment plans and patients’ long-term medication adherence. However, the level of health informatization in Chinese hospitals remains low. It is understood that only after achieving Level 4 in the national Electronic Medical Record (EMR) grading system can data interoperability be realized, enabling comprehensive tracking of the entire patient journey from admission to discharge. As of 2018, the average EMR grading for tertiary hospitals in China was only 2.8. Although there were plans to reach Level 4 by 2020, specific data confirming this achievement are not currently available, leaving the outcome uncertain. Consequently, the current situation remains characterized by information silos across medical institutions and a lack of unified data standards, which fails to provide the necessary support for PBM implementation.

The first point is the lack of significant volume in outflowing prescriptions. Public hospitals in China continue to dominate the core of pharmaceutical sales channels, a position that is estimated to be difficult to dislodge. Although the government is vigorously promoting the separation of medical services from drug dispensing and the outflow of prescriptions, this transition will take time. Consequently, chain pharmacies are not the primary sales terminals for prescription drugs. Without sufficient volume, they cannot negotiate prices or expand their product portfolios, let alone address subsequent issues such as prescription review and medication control.

Second, there is an insufficient number of affiliated outlets. Judging by the expansion trends of pharmacies designated for basic medical insurance or commercial health insurance, even if the network of such designated pharmacies is expanded, its growth rate remains constrained by economic interests and regulatory frameworks. Consequently, in the short term, pharmacies designated for basic medical insurance cannot achieve full coverage of the entire retail network.

The third point is the inability to handle service demand. Pharmacies, primary healthcare institutions, and other entities are not yet fully prepared to accommodate large-scale prescription outflow. This includes issues such as basic staff training, system integration, and optimization of drug formularies. Therefore, more time is needed to continue strengthening infrastructure.

In fact, many medications hold significant value for patients but are not included in the national medical insurance reimbursement list, leaving patients unable to receive coverage. Commercial health insurance can serve as a supplement in these cases; however, such supplementary drug formularies must be developed and reviewed by professional medical evaluation committees. This raises the question: who oversees the reasonableness of the formulated lists? I am currently unaware of the specific laws and regulations governing this area, but it is evident that there are policy hurdles in the development and review processes. In China, the authority to formulate the medical insurance drug list rests with the healthcare security administration, whereas in the United States, Pharmacy Benefit Managers (PBMs) have completely dominated the entire process of formulating prescription drug formularies.

Administrative Division Fragmentation: The real-time medical insurance claims network is constructed independently by each province and municipality, meaning full interconnectivity will take time to achieve. For commercial health insurance, the challenge is even greater.

Although there are many challenges and obstacles, I believe that the industry will ultimately return to the value curve; it is only a matter of time. Therefore, let us finally consider what core elements are required for PBM to succeed.

In an industry analysis jointly authored by Wang Bin, Liu Zeyuan, Zhou Di, Gai Ruijie, and Sun Qisong from the Healthcare and Life Sciences Team at China Renaissance Capital, it is proposed that a localized PBM model in China must possess the following six key success factors:

i. Strong drug price negotiation power: Ensures that PBMs procure drugs from upstream pharmaceutical manufacturers at lower prices

ii. Prescription Issuance and Review Capability: Ensuring that the PBM assists patients in rational medication use based on drug prescriptions

iii. Sufficient patient volume: Ensuring that the PBM has an adequate patient base and pharmaceutical sales volume

iv. Mature supply chain system: Ensuring efficient circulation of pharmaceuticals

v. Robust Payment-Side Safeguards: Ensuring Final Payment for Medications

vi. Continuous medication data for chronic diseases: Ensuring PBMs understand the medication patterns of patients with chronic conditions

Official Account:Healthcare Circle

How Can PBMs Effectively Manage Chronic Diseases Through Localized Implementation in China?

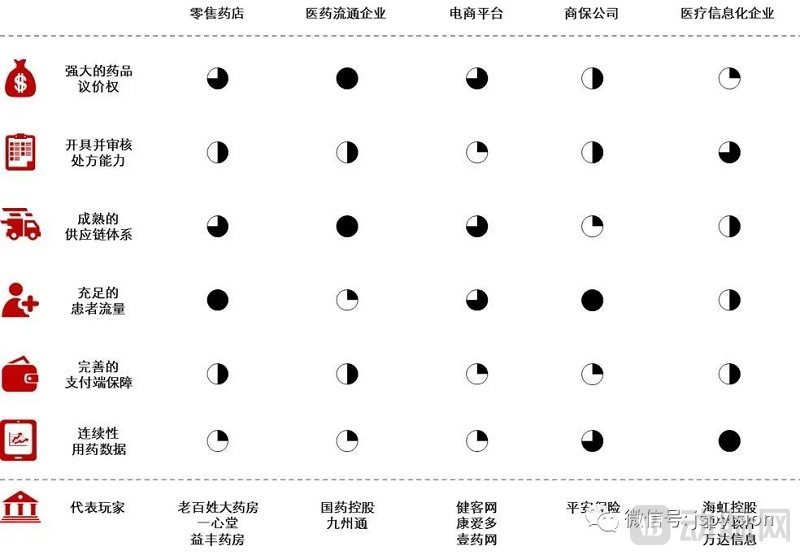

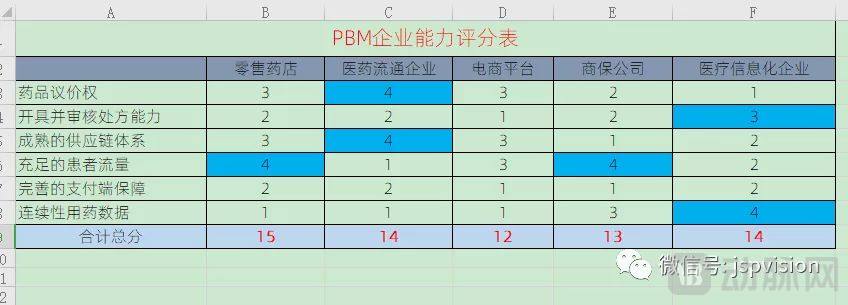

After my personal review, I find the six summarized points to be highly comprehensive and precise. Currently, companies in China emulating the U.S. model to implement Pharmacy Benefit Management (PBM) primarily fall into five categories: retail pharmacy chains, pharmaceutical distribution enterprises, e-commerce platforms, commercial insurance companies, and healthcare IT firms. Through a comparison across six dimensions, members of the Health Group have categorized these entities, scored them on various capabilities, and provided analytical assessments:

Assuming that the weight of each score is identical and the individual item score is 4 points, the following scoring table would be obtained:

Overall, the total scores of each type of enterprise are not significantly different. However, if forced to judge which entity is most likely to achieve PBM scale-up first under current conditions, I must admit that I cannot make such a determination at this time. Nevertheless, a common-sense logical approach suggests that at different stages of industry development, the capability that is relatively scarcest holds the greatest leverage. For instance, pharmaceutical distribution companies score a perfect 4 out of 4 in drug price negotiation and supply chain systems, giving them two leverage advantages. In contrast, commercial insurance companies are weak in these areas, scoring only 1–2 points, and thus tend to partner with pharmaceutical distributors. Meanwhile, healthcare IT enterprises score 3–4 points in prescription review and medication data recording, also securing two leverage advantages; consequently, e-commerce platforms, which are weaker in these domains, may seek partnerships with them. Additionally, there is complementarity among their scores in other categories.

Furthermore, it is essential to identify which players have relatively balanced overall capabilities—meaning no significantly weak areas. Such entities are most likely to bridge their capability gaps through continuous collaboration and external resource integration. The healthcare industry does not revolve around a single service; particularly in disease management, it requires end-to-end engagement. This follows a team-based logic rather than an individual contributor model. For instance, if you offer only health consultations without subsequent prescription services or offline patient navigation, you will likely remain confined to the shallowest segment of the overall medical value chain. Of course, you can initially penetrate the market through a single touchpoint, accumulate user traffic, and then expand your offerings.

In summary, the scarcer one’s competitive advantages are, the more partners will seek collaboration. With no significant weaknesses across capabilities, it becomes easier to rapidly build a closed-loop healthcare service ecosystem. Ultimately, success hinges on which player can develop these capabilities faster, leading to a winner-takes-all outcome.

Although the implementation of Pharmacy Benefit Management (PBM) faces numerous challenges, it has also created new market opportunities. Emerging star enterprises in recent years, such as Yaolian and Medxhealth, have demonstrated rapid growth momentum, and further breakthroughs in this sector are expected in the future.

Well, that concludes the sharing of this entire section. To sum it up in one sentence: only when commercial health insurance and public medical insurance jointly underwrite the payment side, and the service side is strengthened through the deep integration of “Health Management + DRGs + PBM,” can we truly speak of returning to value-based healthcare. This represents a significant benefit to the health of each and every one of us. Let’s look forward to it together~