Top-Tier Investment Firms Including GV and OrbiMed Target Overseas Medical Innovators Amid Global Healthcare Expansion

"If you can't invent the future, the second-best option is to invest in it."

——John Doerr,KPCB

In recent years, driven by the combined effects of global economic development, population growth, an aging society, and heightened health awareness, healthcare expenditures across countries and the global pharmaceutical market size have steadily increased. Against this backdrop, with growing global emphasis on healthcare, total healthcare spending has also risen steadily in recent years.

According to statistics from the World Health Organization, total global healthcare expenditure grew from approximately $6.8 trillion in 2015 to about $7.3 trillion in 2018, representing a compound annual growth rate (CAGR) of approximately 2.5% during this period. As indicated in IQVIA’s March 2020 report, “Global Medicine Spending and Usage Trends: Outlook to 2024,” net revenues in the global pharmaceutical market reached $955 billion in 2019 and are projected to exceed $1.115 trillion by 2024, with a CAGR of 3.15%.

Particularly against the backdrop of the global pandemic’s spread in 2020, the healthcare sector experienced rapid advancement. The extraordinary circumstances heightened public awareness of the essential nature of pharmaceuticals and medical services, bringing specialized terms such as nucleic acid testing, mRNA vaccines, and gene editing into everyday life. Meanwhile, healthcare reform policies, including centralized drug procurement and DRG/DIP payment systems, have continuously impacted healthcare delivery and public welfare.

In the post-pandemic era, the global landscape has been reshaped by COVID-19. As an essential need, healthcare continues to advance, with various new pharmaceutical technologies coming to fruition. As a major and powerful player in the pharmaceutical industry, China is striving to keep pace with cutting-edge global medical technologies and even plans to surpass them in the future. However, in innovative fields such as biopharmaceuticals, China is still working hard to align itself with the advanced international standards.

How can we break through the ceiling of the pharmaceutical industry in the future? What emerging technologies in the healthcare sector are worth exploring? Let’s examine the investment strategies of top-tier firms such as Google Ventures and OrbiMed in the overseas healthcare market over the past year and a half (institutional investment data covers the period from January 1, 2020, to June 20, 2021, compiled based on the VCBeat database).

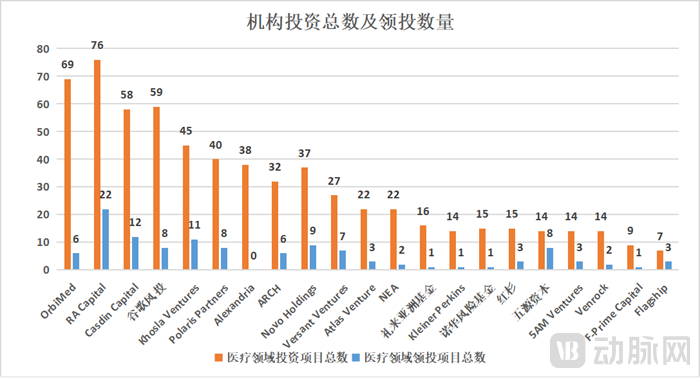

Investment Data of Several Top Investment Institutions in the Past Two Years, Source: VCBeat Database

The investment stages covered by the aforementioned institutions are extensive (including early-stage, growth-stage, expansion-stage, profitability-stage, and others), and their founding years span a wide range (from 1946 to 2011).

Among them, there are 10 comprehensive investment firms (including GV, NEA, Venrock, Kleiner Perkins, Sequoia Capital, ARCH Venture Partners, Khosla Ventures, Polaris Partners, Novo Holdings, and 5Y Capital), with investment scopes covering various sectors, stages, and regions, such as internet, software, clean technology, biotechnology, healthcare, media, and energy.

The other 11 are investment firms specializing in the life sciences and healthcare sector (including RA Capital, Versant Ventures, F-Prime Capital, Atlas Venture, Novartis Venture Fund, Lilly Asia Ventures, Flagship Pioneering, OrbiMed, Alexandria Real Estate Equities, Casdin Capital, and 5AM Ventures). Their teams possess extensive industry and business development experience across investment, operations, and scientific expertise.

Total Number of Institutional Investments and Lead Investments

The total number of investments made by the aforementioned institutions ranges from 7 to 76. Among them, nine institutions have invested in 30 or more projects: OrbiMed, RA Capital, Casdin Capital, Google Ventures (GV), Khosla Ventures, Polaris Partners, Alexandria Real Estate Equities, ARCH Venture Partners, and Novo Holdings. Their respective investment counts are 69, 76, 58, 59, 45, 40, 38, 32, and 37, while all other institutions have fewer than 30 investments. The ratios of lead investments to total investments for these institutions are 9%, 29%, 21%, 14%, 24%, 20%, 0%, 19%, 24%, 26%, 14%, 9%, 6%, 7%, 7%, 20%, 57%, 21%, 14%, 11%, and 43%, respectively (ordered from left to right as shown in the table above).

Three firms—RA Capital, Casdin Capital, and Khosla Ventures—each led ten or more investment rounds; seven firms led between five and nine rounds; and the remaining firms each led between zero and three rounds.

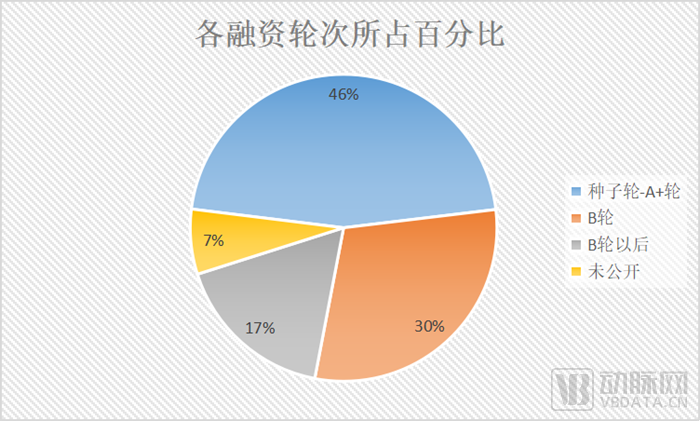

Number and Percentage of Financing Rounds

An analysis of the lead investment projects by the aforementioned institutions reveals that investment rounds are predominantly concentrated from the Seed round to the A+ round, accounting for 46% of total lead investments. Series B financing accounts for 30%, post-Series B financing represents 17%, and undisclosed rounds constitute 7%. This indicates that while most investment institutions favor early-stage investments, they also engage in mid-to-late stage investments.

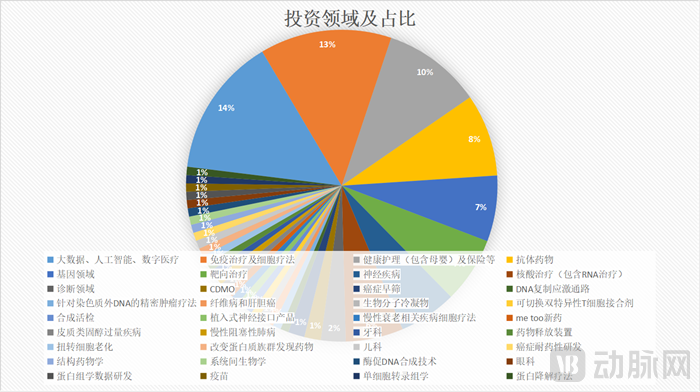

Investment Areas and Proportions

As can be seen from the figure above,A total of 36 specialized medical sectors were identified (with some cross-disciplinary areas affecting the count). Among these, eight key tracks have gained significant traction: Big Data, Artificial Intelligence, and Digital Health; Immunotherapy and Cell Therapy; Healthcare (including maternal and child care) and Insurance; Antibody Drugs; Genomics; Targeted Therapy; Neurological Disorders; and Nucleic Acid Therapies (including RNA therapies). Notably, investments in Big Data, Artificial Intelligence, and Digital Health alone accounted for 14% of the total, while the combined share of these eight major tracks reached as high as 72% of all investments., its popularity is evident.

AI Applications Rely on Known Data: Can They Achieve Autonomous Exploration in the Future?

According to data provided by Nature, the development of a new drug costs approximately $2.6 billion, takes about 10 years, and has a success rate of less than one in ten. In contrast, AI can screen target compounds from libraries containing hundreds of millions of molecules within just a few days, aggregate and learn from vast amounts of medical big data, thereby significantly reducing both the time required for innovative drug development and the scope of trial-and-error.

With the advent of the internet era, big data and artificial intelligence (AI) have been widely applied in medicine. Tasks such as computer-aided diagnosis, health management, new drug development, and rehabilitation therapy can be completed more accurately and rapidly through AI. Whether in terms of shortening the cycle and reducing the cost of new drug development, improving data accuracy, or enabling AI-driven therapies, the prospects are highly promising.

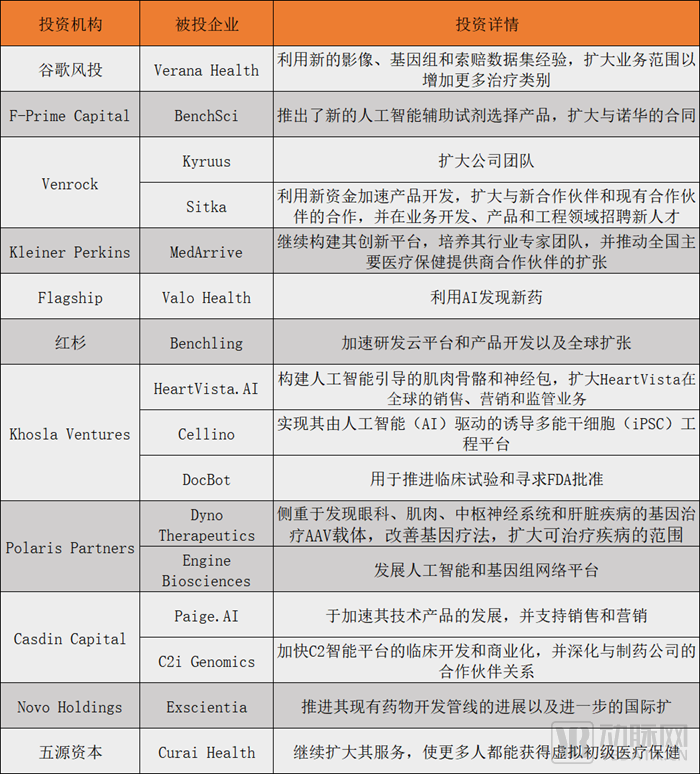

The vast potential of AI has inevitably attracted significant attention from investment firms: In February 2020, Google Ventures invested in Verana Health, a medical big data service provider; in February 2020, F-Prime Capital invested in an R&D company specializing in AI-assisted reagent selection instruments; in April 2021, Sequoia Capital invested in Benchling, a software development company...

Venrock, a veteran venture capital firm that has previously invested in star companies such as Apple, Intel, Gilead Sciences, and Tudou, has also entered the big data arena by investing in Sitka, a company offering customizable telemedicine platforms, this February. Bob Kocher, a partner at Venrock, stated, “We are delighted to collaborate with such a knowledgeable team. We look forward to observing the role telemedicine will play in expanding access to specialist providers within U.S. communities.”

However, the application of AI depends on the models constructed, and the data used to build these models is derived from existing knowledge. Shifting from humans leveraging existing knowledge to construct AI, to AI guiding humans to proactively explore the unknown, may represent a more advanced direction for the future development of AI.

Statistical Overview of Investments in Big Data, AI, and Digital Health Sectors by the Above-mentioned Investment Institutions

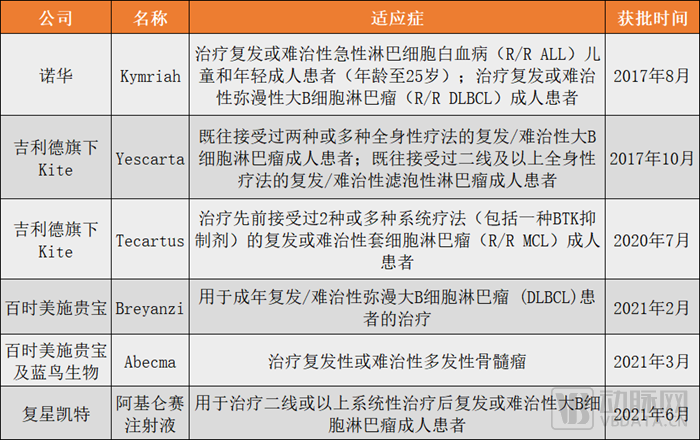

Thousands of CAR-T Clinical Trials: How Many Will Emerge as Future Winners?

Cell therapy is categorized into immune cell therapy, stem cell therapy, and other cell therapies. Among these, immune cell therapy has evolved to the sixth generation of CAR-T cell therapy, which offers advantages such as high specificity and durable efficacy. The CAR-T cell therapy sector has witnessed significant momentum in recent years, with a surge in global clinical projects. Currently, there are six CAR-T cell therapy products approved for market launch worldwide, and over one thousand clinical research projects are underway.

Currently Approved CAR-T Cell Therapy Products on the Market

However, the upfront R&D costs, coupled with the complexity of personalized treatment and the lengthy cycle required for cell culture, mean that the price of personalized CAR-T cell therapy is unlikely to be affordable for the general public. Currently, the cost of personalized CAR-T therapy ranges from approximately $373,000 to $475,000, equivalent to roughly RMB 2.38 million to RMB 3.04 million.Amid a crowded competitive landscape and high treatment costs, the development of off-the-shelf CAR-T therapies is bound to become the prevailing trend in the evolution of CAR-T technology.

Furthermore, while the primary indications for CAR-T cell therapy are currently in hematologic malignancies, there remains significant market potential for its application in solid tumors, which account for 90% of the overall oncology market.

The overcrowding and homogenization resulting from an excess of players in popular sectors are issues that companies must resolve to sustain their growth. Conversely, it may be more worthwhile to explore niche emerging fields that are either nascent or still in their early stages.

Novartis, Pfizer, and Merck Jointly Invest in FoRx to Develop the DNA Replication Stress Pathway Relied Upon by All Cancer Cells

In 2018, a Cell sub-journal published findings that the stress response during DNA replication can induce the formation of cancer stem cells; on October 1, 2019, FoRx Therapeutics (hereinafter referred to as “FoRx”), the first company to develop a drug pipeline targeting cancer-related DNA replication stress, was established;In April 2020, Novartis Venture Funds, Pfizer Venture Investments, Merck, Omega Healthcare Investors, and LSP jointly invested in FoRx, entering the field of DNA replication stress.

Genomic stability is directly linked to whether cells undergo carcinogenesis. Among cellular processes, DNA replication is the most susceptible to alterations and poses the highest risk for carcinogenesis. Any condition that leads to high levels of DNA damage can also induce replication stress, which is a source of genomic instability and a hallmark of both pre-malignant and malignant cells.

Replication stress is a mechanism that has been studied relatively recently. Nearly all cancer cells rely on the break-induced replication pathway associated with replication stress for proliferation. Given the widespread presence of replication stress in cancer cells, there is significant potential for developing anticancer drugs by targeting the replication stress pathway.

Three of the world’s leading pharmaceutical companies have jointly invested in FoRx, likely recognizing the growth potential of the nascent DNA replication stress sector and the prevalence of DNA replication stress in cancer cells.

RA Capital Invests in Boundless to Develop Precision Oncology Therapies Targeting Extrachromosomal DNA

In November 2019, Professor Paul Mischel’s team published an article titled “Circular ecDNA promotes accessible chromatin and high oncogene expression” in Nature, revealing for the first time the structure and function of extrachromosomal DNA (ecDNA).This study demonstrates that circular extrachromosomal DNA (ecDNA) is prevalent in tumors and, due to the absence of centromeres, does not follow Mendelian inheritance patterns. These characteristics make ecDNA a key mechanism driving tumor heterogeneity.

In August 2020, researchers at the University of California, San Diego published an article titled “Extrachromosomal DNA is associated with oncogene amplification and poor outcome across multiple cancers” in the journal Nature Genetics, providing the first confirmation that extrachromosomal DNA promotes the growth of multiple aggressive tumors.

This study performed computational analyses using whole-genome sequencing data from 3,212 cancer patients. The results indicated that ecDNA amplification frequently occurs across most cancer types but is absent in blood or normal tissues. Compared with patients whose cancers are not driven by ecDNA-based oncogene amplification, cancer patients harboring ecDNA exhibited significantly shortened survival, even after controlling for tissue type. In the future, this mechanism is expected to facilitate the development of precision oncology therapies targeting ecDNA.

In April 2021, Boundless Bio secured $105 million in Series B financing led by RA Capital to develop innovative therapies targeting extrachromosomal DNA (ecDNA) for aggressive cancers.Boundless Bio integrates its proprietary Spyglass platform, combining ecDNA model systems with customized analytical tools, to interrogate ecDNA in cancer and uncover key therapeutic targets in tumors driven by ecDNA-mediated gene amplification, thereby elucidating the role of ecDNA in oncogenesis.This technology is expected to provide transformative, next-generation precision oncology therapies for cancer patients who were previously difficult to treat.

In addition to the nascent fields mentioned above, niche emerging areas such as implantable neural interface products, switchable bispecific T-cell engagers, synthetic biopsy, reversing cellular aging, enzymatic DNA synthesis technology, drug discovery through modulation of protein populations, inter-systems biology, and cell therapies for chronic age-related diseases are gradually coming into the view of investment institutions.

IDG Enters the Single-Molecule Detection Arena: Can It Surpass Chemiluminescence to Become the Mainstream Technology?

Compared to the aforementioned statistics on overseas investment layouts, there are also some nascent, niche sectors within China that warrant our exploration.

As IDG’s strategic entry into the single-molecule detection sector last December. Single-molecule detection is an ultra-sensitive assay technology that has rapidly advanced over the past decade. Compared with conventional techniques such as chemiluminescence and enzyme-linked immunosorbent assay (ELISA), it offers several advantages, including high resolution (at the femtogram level), high sensitivity (1,000 times more sensitive than ELISA), low background signal (with a dynamic detection range 10–100 times greater), reduced sample volume requirements (decreasing sample consumption by at least 50%), and shorter analysis time (reducing reaction time by at least 50%). This technology enables the detection of low-abundance proteins in complex samples, facilitating the differentiation between health and disease states and the monitoring of disease onset and progression.

Currently, there are a total of six companies in the global single-molecule detection technology sector: Quanterix, Singulex (under Merck), Light & Biology, YuCe Bio, CaiKe Bio, and Mecwins.

In China, there are three single-molecule technology companies: Guangyu Shengwu, Yuce Bio, and Caike Bio. Compared with their international counterparts, Chinese enterprises started relatively late. Among them, Caike Bio is the earliest established, founded in 2018. In December last year, IDG invested tens of millions of yuan in its Series A financing round. Currently, Caike Bio focuses on the field of multiplex protein detection. The company possesses core technological platforms—the ultra-high-sensitivity biomolecular detection platform and the multiplex magnetic-fluorescent encoded microsphere platform—as well as the Medivh series of reagents and equipment products.

Although single-molecule detection technology holds a "dimensionality-reduction" advantage over traditional techniques such as chemiluminescence, chemiluminescence immunoassay and enzyme-linked immunosorbent assay (ELISA) still dominate the current market for immunoassays. One reason is that conventional methods are currently sufficient to meet testing demands; another is that instruments for single-molecule detection are significantly more expensive than their traditional counterparts.

Addressing the issues of substitutability and cost in single-molecule detection technology is the fundamental determinant of its potential for large-scale adoption.

Mature technologies that remain static are effectively regressing; in today’s healthcare sector, where emerging technologies abound, such stagnation amounts to self-imposed obsolescence. The only way to keep pace with the rapidly evolving healthcare landscape is to upgrade mature technologies and identify emerging ones. However, the development of emerging technologies is often accompanied by skepticism, requiring sustained commitment and significant resource investment from the initial formulation of scientific hypotheses through to the final translation into clinical products.

Healthcare: An Eternal Essential Need Accompanying Humanity.In times of peace, it is a fundamental necessity for improving the quality of human life; in times of war, it is the vital source of salvation for the wounded and dying. It continuously gives rise to new innovations as society develops, science advances, and human needs evolve.

References:

1. China Business Industry Research Institute, “Analysis of Operating Data in China’s Pharmaceutical Industry in 2020 and Trend Forecast for 2021.”

2. “Blue Book of the Big Health Industry: Report on the Development of China’s Big Health Industry.”

3. National Bureau of Statistics, “Main Data from the Seventh National Population Census.”

4.DJ Mcgrail,CJ Lin,D Hui,M Wei,SY Lin.《Defective Replication Stress Response Is Inherently Linked to the Cancer Stem Cell Phenotype》.

5. Xuantai Pharmaceutical IPO Prospectus.

6.Hoon Kim,Nam-Phuong Nguyen,Kristen Turner,Sihan Wu,Amit D. Gujar,Jens Luebeck,Jihe Liu,Viraj Deshpande,Utkrisht Rajkumar,Sandeep Namburi,Samirkumar B. Amin,Eunhee Yi,Francesca Menghi,Johannes H. Schulte,Anton G. Henssen,Howard Y. Chang,Christine R. Beck,Paul S. Mischel,Vineet Bafna&Roel G. W.Verhaak.《Extrachromosomal DNA is associated with oncogene amplification and poor outcome across multiple cancers》.

7. Others: VCBeat Database, IQVIA Analysis, National Health Commission of the People's Republic of China, Chinese Center for Disease Control and Prevention, National Institutes for Food and Drug Control, U.S. Centers for Disease Control and Prevention website, World Health Organization, National Bureau of Statistics of China.