Zylox-Tonbridge Medical Makes Hong Kong Debut, Unlocking Growth Potential in Neurovascular and Peripheral Interventions

Zylox-Tonbridge

Innovative R&D, Production, and Sales of Medical Devices in the Vascular Intervention Field

Today, Zylox-Tonbridge officially listed on the Hong Kong Stock Exchange, marking another addition of a publicly traded company to the vascular intervention sector. The IPO price was HK$42.7, with an opening price of HK$55. As of 9:51 AM, Zylox-Tonbridge’s share price stood at HK$53.15, representing a 24.47% increase, and its market capitalization reached HK$17.2 billion.

Over the past two years, the sector of high-value consumables for interventional procedures has witnessed a surge in initial public offerings (IPOs). In the valve segment, Venus Medtech, Peijia Medical, and MicroPort CardioFlow have already listed on the Hong Kong Stock Exchange, while Hanyu Medical, Jian Shi Technology, and HeartCare Medical have initiated their IPO processes. In the field of vascular intervention, in addition to companies such as MicroPort Endovastec and Zylox-Tonbridge that are already listed on the Hong Kong Stock Exchange, Saisida and Xinwei Medical, having passed the listing hearing, are poised to list on the Hong Kong Stock Exchange shortly.

What Makes Zylox-Tonbridge Stand Out in a Dazzling Array of Enterprises?

In terms of disease treatment, Zylox-Tonbridge’s current therapeutic areas include acute ischemic stroke (AIS), intracranial aneurysms, carotid artery stenosis, peripheral arterial and venous diseases, and dialysis-related conditions, all of which represent large markets with substantial patient populations.

In terms of domain coverage, Zylox-Tonbridge exhibits a certain degree of scarcity, occupying the two major tracks of neurointerventional and peripheral interventional procedures.In the Hong Kong stock market, domestic players in the neurointerventional field also include Peijia Medical and MicroPort NeuroTech; domestic players in the peripheral interventional field also include Acotec Scientific and MicroPort Endovascular MedTech.

Moreover, Zylox-Tonbridge has long been a favorite among investors, completing five rounds of financing prior to its IPO. Honghui Capital made significant investments starting from the Series A round, while renowned institutions such as OrbiMed, SDIC Innovation, and Qingchi Capital also placed their bets. The cornerstone investor lineup included prominent firms such as Hillhouse, Fidelity, Boyu Capital, and AIHC Lingjian.

Why has Zylox-Tonbridge repeatedly attracted the favor of top-tier investment firms? In the highly competitive interventional field with numerous enterprises, what share of the market does Zylox-Tonbridge have the opportunity to capture?

Vascular intervention has emerged as one of the hottest sectors in the medical device industry in recent years. Taking the neurointerventional field, which saw a surge in popularity in 2020, as an example, VCBeat reported that at least 24 innovative companies and 60 investment firms had bet on the neurointerventional sector in China.

However, Zylox-Tonbridge was not established in response to this recent surge. As early as 2012, Dr. Zhao Zhong returned to China to found Zylox Medical, which focuses on peripheral vascular interventional products. In 2016, he established Tonbridge Medical, which specializes in neurovascular interventional products.

Nine years ago, the fields of neurointerventional and peripheral interventional procedures chosen by Dr. Zhao Zhong were considered “niche.” In contrast to the relatively mature coronary intervention sector, where domestically produced products account for over 70% of the market, the research, development, manufacturing, and marketing of domestic peripheral and neurovascular interventional devices were just getting started. To this day, imported products still dominate an absolute 90% share of the neurointerventional and peripheral interventional markets.

Dr. Zhao Zhong’s decision to launch ventures in these two niche sectors is also linked to his prior R&D experience at multinational corporations.

Dr. Zhao Zhong is a native of Mianyang, Sichuan Province. With a passion for chemistry, he graduated from Sichuan University in 1988 with a bachelor’s degree in Polymer Chemistry and Synthesis. After completing his graduate studies, instead of continuing to pursue organic synthesis during his overseas education, Dr. Zhao ventured into biomedical engineering—a field that intersects with chemistry but leans more toward medicine. In May 1997, Dr. Zhao earned his Ph.D. in Biomedical Engineering from the School of Medicine at Johns Hopkins University in the United States.

After graduation, he joined Guilford Pharmaceuticals Inc., a biopharmaceutical company founded by his mentor that specialized in targeted and site-specific cancer therapies. In 2002, he joined Cordis, a subsidiary of the multinational giant Johnson & Johnson, as Chief Scientist and Researcher, where he was primarily responsible for developing combination drug-device products. Cordis is a global leader in the development and manufacturing of interventional vascular technologies.

Dr. Zhao Zhong spent ten years at Johnson & Johnson, where he participated in the development of multiple key products at Cordis. In 2003, the Cypher stent, which he helped develop, became the first drug-eluting stent to receive FDA approval. However, by June 2011, facing diminishing competitive advantages in the cardiovascular stent market, Johnson & Johnson announced that its subsidiary Cordis would cease production of the existing Cypher product by the end of the year. In March 2015, Johnson & Johnson announced the sale of its subsidiary Cordis for $1.9 billion, marking its complete exit from the cardiovascular stent sector.

Following the Cypher incident, Dr. Zhao Zhong decided to return to China to start a business. On November 6, 2012, Zhejiang Zylox Medical Device Co., Ltd. was established in Hangzhou Haichuang Park, with “Zylox” signifying “returning to China to start a business.”

Dr. Zhao Zhong, who returned to China to start a business, quickly gained recognition from the investment community. Honghui Capital has been bullish on Zylox-Tonbridge since its Series A round. In 2016, Zhuhai Tonbridge, a subsidiary of Zylox-Tonbridge, was established and entered the high-end medical device sector for neuro-implant interventional procedures.

As one of the key forces driving the import substitution of high-end medical devices, Dr. Zhao Zhong stated in an interview that “overtaking on a bend” is a false premise; only by working diligently can companies seize opportunities and compete on equal footing with industry giants. Leveraging its forward-looking strategic layout, innovative R&D capabilities, and strong execution, Zylox-Tonbridge has garnered widespread recognition.

In 2018, Zylox Medical reached a critical turning point in its development by merging with Tonbridge Medical. The merged entity, Zylox-Tonbridge, completed its Series B and Series B+ financing rounds in 2019, raising a total of RMB 180 million in the Series B round.

As the neurointerventional sector gained significant traction, Zylox-Tonbridge completed its Series C financing in 2020, raising a total of RMB 325 million. The round was led by Orbimed, with existing investors Hui Capital (Series A), SDIC Innovation (Series B), and Zheshang Venture Capital all participating as follow-on investors. In 2021, Zylox-Tonbridge closed its Series C+ round, securing USD 76 million in funding.

In terms of shareholding, parties related to Honghui Capital collectively hold approximately 11.11% of the shares, making it the largest external institutional shareholder of Zylox-Tonbridge. OrbiMed holds 9.62% of the shares, and SDIC Innovation holds 7.77%. Other shareholders, including Qichi Capital, AIHC Lingjian, CITIC Securities, and Xiamen C&D New Xin, collectively hold approximately 34.95% of the shares.

In the highly competitive vascular intervention sector, a major advantage of Zylox-Tonbridge is its first-mover advantage in this field. Vascular interventions are categorized into three main areas: coronary intervention, neurointervention, and peripheral intervention. Upon returning to China to start his business, Dr. Zhao Zhong initially chose two sectors dominated by overseas companies: neurointervention and peripheral intervention.

Coronary InterventionThe primary associated diseases are cardiovascular diseases, and the main products are widely recognized coronary stents and balloons. Centralized volume-based procurement has already been implemented in the coronary artery sector, where domestic companies such as MicroPort have captured a significant market share, indicating a relatively mature market.

andNeurointerventional and Peripheral InterventionalAll are still in the early stages of development. Neurointervention is primarily associated with cerebrovascular diseases, including intracranial hemorrhage, cerebral infarction, and cerebral arterial occlusion and stenosis. Key products include thrombectomy stents, coils, and flow-diverting stents;

Peripheral InterventionPrimarily associated with lower extremity vascular diseases, including peripheral arterial occlusion, deep vein thrombosis, and varicose veins. Key products include peripheral drug-coated balloons, stents, radiofrequency ablation systems, and inferior vena cava filters.

The two major sectors selected by Dr. Zhao Zhong share the common characteristics of low penetration rates but rapid growth.

For example, mechanical thrombectomy (MT) is an advanced minimally invasive treatment technique for ischemic stroke. However, in 2019, the penetration rate of MT procedures was 3% in the United States, compared to only 0.6% in China. In the same year, the penetration rate of peripheral artery disease-related surgeries was 5.4% in the United States, whereas it was merely 0.2% in China.

The primary constraint on the increasing penetration rates of neurointerventional and peripheral interventional procedures in China is price. Both markets are dominated by imports; in 2019, foreign companies held a 93.3% market share in China’s neurointerventional device market, making imported products prohibitively expensive for most patients. For instance, the Solitaire Platinum stent retriever, launched by Medtronic in the Chinese market in 2019, was priced at RMB 55,000.

Low penetration rates indicate that the market is far from saturated. In recent years, neurointerventional and peripheral interventional procedures have begun to grow rapidly. According to data from its prospectus, the compound annual growth rate (CAGR) for neurovascular and peripheral vascular interventional procedures was 24.8% from 2015 to 2019. The market size for both segments is projected to exceed RMB 30 billion by 2030.

Let us first examine neurointervention, a sector fiercely pursued by capital. The market size of neurointerventional medical devices in China increased from RMB 2.6 billion in 2015 to RMB 4.9 billion in 2019, representing a compound annual growth rate (CAGR) of 17.3%. It is projected to further grow to RMB 37.1 billion by 2030, with a CAGR of 20.2% from 2019 to 2030.

Turning to peripheral interventions, a sector where Medtronic, Boston Scientific, and BD Medical are competing to launch new products, the combined volume of peripheral arterial and peripheral venous intervention procedures in China has already reached hundreds of thousands. In the peripheral arterial segment alone, the market size for interventional devices for peripheral artery disease in China grew from RMB 1.4 billion in 2015 to RMB 2.4 billion in 2019, representing a compound annual growth rate (CAGR) of 15.7%. It is projected to further increase to RMB 12.2 billion by 2030, with a CAGR of 15.7% from 2019 to 2030.

Of course, as the market takes off, the number of new entrants is also increasing.What competitive products does Zylox-Tonbridge have in these two major fields? How strong is the commercialization capability of its core products?

It is understood that Zylox-Tonbridge’s two core products are the Jiaolong Intracranial Thrombectomy Stent and the Ultrafree Drug-Eluting PTA Balloon Dilation Catheter, both of which have been launched in China.

The Jiaolong Intracranial Thrombectomy Stent, a device in the field of neurointervention, is a minimally invasive instrument that utilizes microcatheter technology to capture and remove thrombi from occluded vessels, thereby alleviating cerebrovascular diseases such as ischemic stroke.

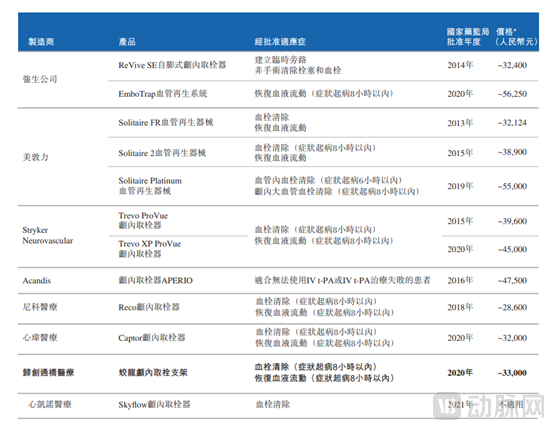

Thrombectomy stents constitute a major product category with numerous offerings. In China, there are currently 12 marketed thrombectomy stents, manufactured by four overseas companies—Johnson & Johnson, Medtronic, Stryker, and Acandis—as well as four domestic companies: Zylox-Tonbridge, Niko Medical, Xinwei Medical, and Xinkainuo Medical. Furthermore, it is noteworthy that thrombectomy stents from Peijia Medical, MicroPort Medical, and Jianshi Medical are in clinical trials and are poised to enter commercialization.

Thrombectomy Stents Listed in China

The market competition for thrombectomy stents is akin to that of PD-1 inhibitors in the pharmaceutical industry.Zylox-Tonbridge’s Jiaolong stent retriever was launched in September 2020, securing a first-mover advantage among domestic competitors. In 2020, Zylox-Tonbridge reported total revenue of RMB 19.94 million from its neurointerventional devices, primarily driven by sales of its core products, the Jiaolong intracranial stent retriever and intracranial support catheters.

How Will Zylox-Tonbridge Maintain Its First-Mover Advantage in the Future?Zylox-Tonbridge has adopted a strategy of benchmarking against multinational corporations, expanding its product portfolio, and providing comprehensive solutions.

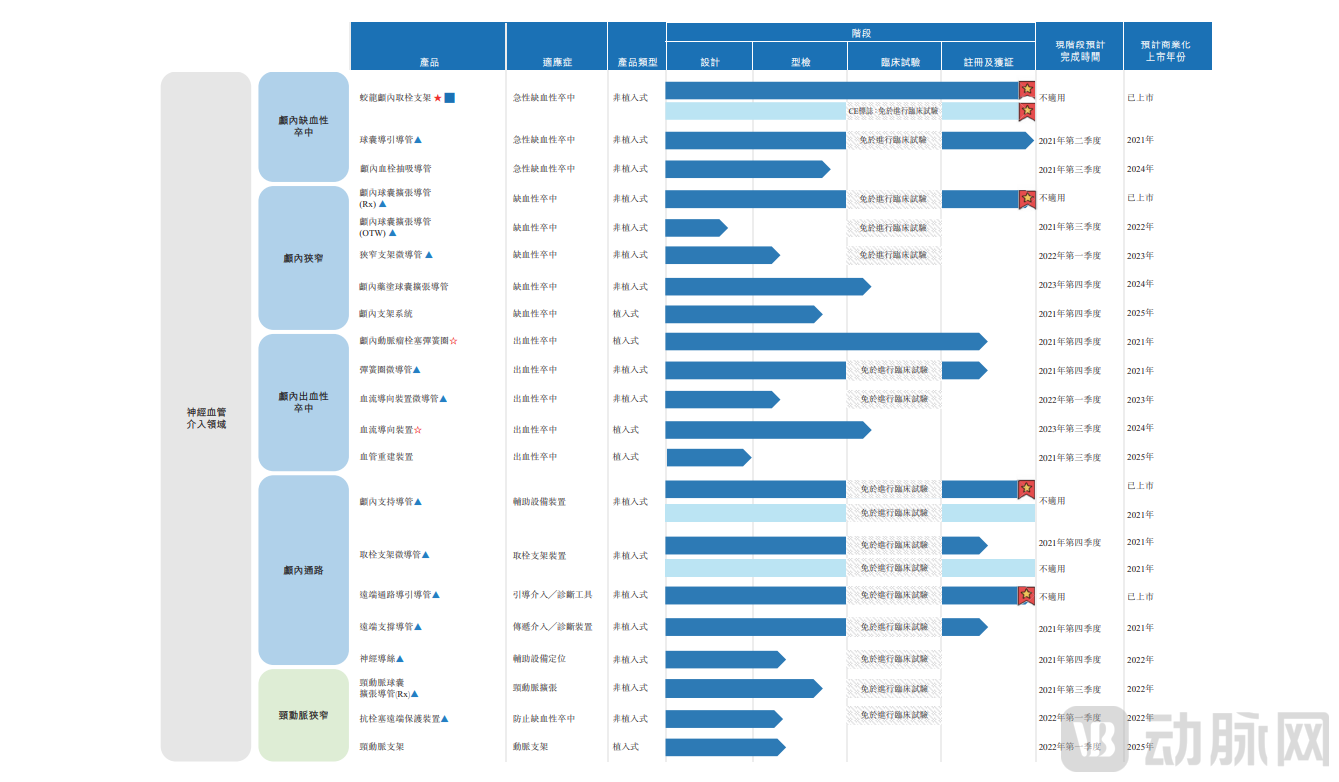

Unlike companies that develop single products, prospectus data shows that Zylox-Tonbridge is the only domestic company in the field of neurovascular interventional medical devices currently developing a full suite of products across major neurovascular categories (namely, ischemic, hemorrhagic, stenosis, carotid, and vascular access devices). Product singularity and the lack of capability for full-line product development are weaknesses common to most Chinese-made enterprises; Zylox-Tonbridge aims to address this shortcoming through a diversified product portfolio.

Zylox-Tonbridge Neurointerventional Pipeline

In the field of peripheral interventions, Zylox-Tonbridge’s core product is the Ultrafree Drug-Coated PTA Balloon Dilation Catheter (Ultrafree DCB).

Drug-Coated Balloon (DCB) is an angioplasty balloon coated with antiproliferative drugs (mostly paclitaxel). The drug can inhibit the proliferation and migration of smooth muscle cells, thereby further reducing the risk of arterial restenosis.

In the field of drug-coated balloons (DCBs), four manufacturers have received approval in China: Acotec, Medtronic, Zylox-Tonbridge, and MicroPort Endovastec. Although there are fewer commercially available domestic DCB products than thrombectomy stents, the challenges remain significant.

In the peripheral drug-coated balloon market, Acotec’s drug-coated balloon, approved in 2016, has dominated the sector by leveraging its first-mover advantage, while products including Ultrafree DCB were only approved for launch in China in 2020.

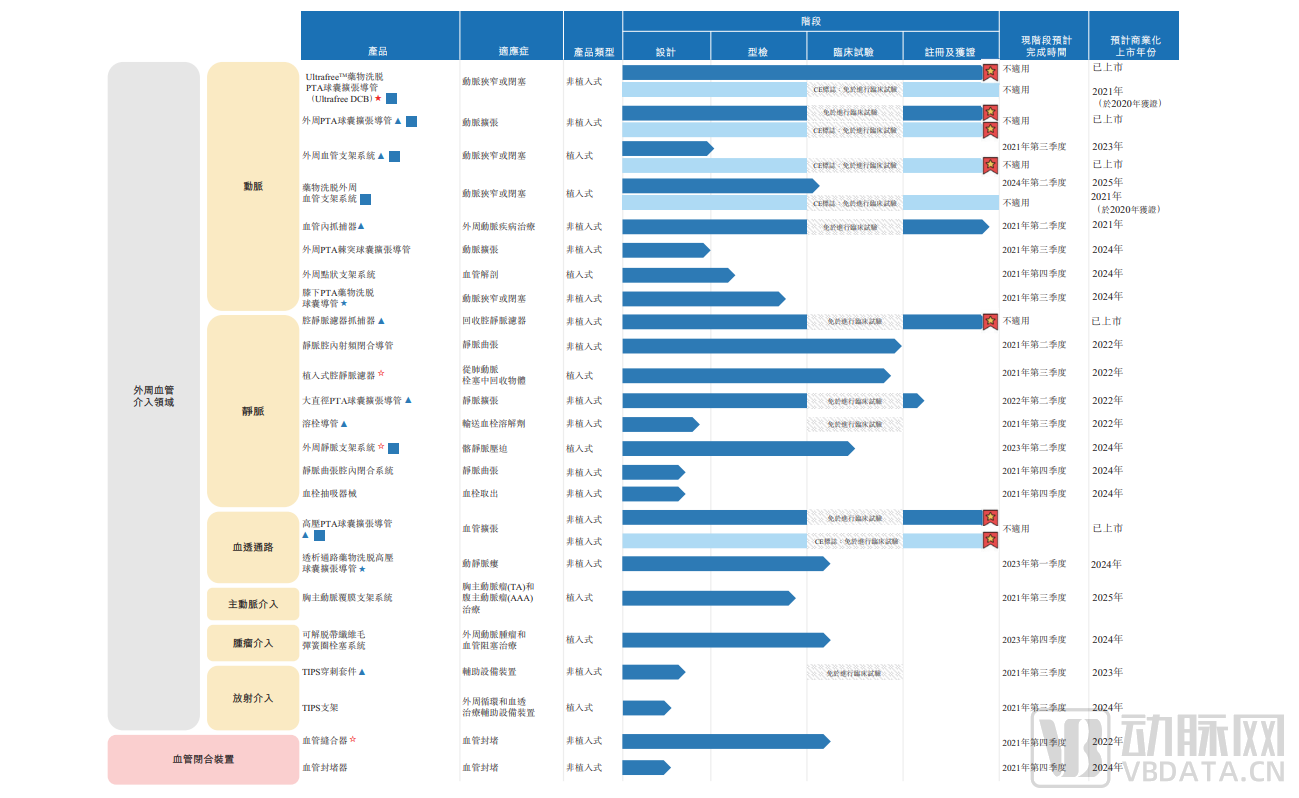

How will Zylox-Tonbridge break through? The diversified product line strategy mentioned in the neurointerventional field has also been applied by Zylox-Tonbridge to the peripheral intervention sector. Its product portfolio covers a full range of arterial and venous products, including stents, balloons, catheters, and filters, as well as two vascular closure devices currently under development.

Peripheral Interventional Catheters

It is worth noting that although domestic products have exhibited a certain degree of homogenization, the coronary intervention sector has given rise to four major players: MicroPort, Lepu Medical, Jiwei Medical, and Sino Medical. By analogy, the neurointerventional and peripheral vascular intervention markets, supported by a large patient base, should similarly be able to accommodate multiple listed companies in the future. Currently, both the neurointerventional and peripheral vascular intervention sectors are dominated by overseas enterprises. As emerging forces in the medical device industry, Chinese companies’ primary growth potential lies in leveraging cost-effectiveness to tap into incremental market space and enhance market penetration.

From a financial perspective, Zylox-Tonbridge reported revenue of RMB 4.917 million and a net loss of RMB 66.647 million in 2019; in 2020, its revenue rose to RMB 27.631 million, with a net loss of RMB 100 million. Although Zylox-Tonbridge remains unprofitable at present, it undoubtedly possesses strong competitiveness in the fields of neurointerventional and peripheral interventional devices, and its management team boasts extensive experience in the research, development, and commercialization of medical devices.

In terms of R&D capabilities, Zylox-Tonbridge is a full-line solution provider with a comprehensive product portfolio among domestic neurovascular and peripheral vascular interventional medical device companies. In terms of R&D expenditure, Zylox-Tonbridge invested RMB 53.028 million in 2019 and RMB 72.065 million in 2020. Over the nine years since its establishment, Zylox-Tonbridge has systematically and comprehensively developed 45 products and products in its pipeline. Its rich product pipeline positions it with the potential to become a leading manufacturer of Chinese-made medical devices in the future.

In the field of cardiovascular intervention, although coronary intervention has been impacted by centralized procurement, leading to a stabilized market landscape, high-barrier segments such as Cardiac Rhythm Management (CRM), pacemakers, cardiac electrophysiology, and Implantable Cardioverter Defibrillators (ICDs) remain dominated by imported products. These sectors are experiencing rapid growth, offering substantial potential for domestic substitution. Beyond vascular intervention, minimally invasive interventional fields such as pulmonary and tumor interventions are also on the rise. We believe that with the public listings of several domestic interventional device companies, including Zylox-Tonbridge, the interventional sector is poised for another wave of significant gains. However, this does not represent the final growth ceiling for vascular intervention; related interventional fields will continue to attract substantial capital investment.