Father-Son Doctor Duo Leads Chaoju Eye Care to IPO: Can It Be the Next Aier Eye Hospital?

Another Ophthalmology Chain Successfully Goes Public.

Today, Chaoju Eye Care (02219.HK) officially listed on the Main Board of the Hong Kong Stock Exchange. Its opening price was HK$10.6, in line with its issue price. As of 9:57 a.m., Chaoju Eye Care’s share price stood at HK$12.96, representing a 22.26% increase, with a market capitalization of HK$8.91 billion.

(Image source: Tiger Brokers)

According to the prospectus, Chaoyu Eye Hospital generated revenues of RMB 633 million, RMB 715 million, and RMB 794 million in 2018, 2019, and 2020, respectively, representing year-on-year growth rates of 12.95% and 11.05%. The net profit attributable to shareholders of the parent company amounted to RMB 39 million, RMB 76 million, and RMB 124 million, respectively, demonstrating stable revenue-generating and profitability capabilities.

Notably, more than 80% of Chaoju Eye Care’s revenue over the past three years was derived from Inner Mongolia and neighboring regions. Among these, the Baotou Hospital, Hohhot Hospital, and Chifeng Hospital collectively accounted for approximately 60% of the total revenue during this period.It can be seen that Chaoju Eye Care’s revenue structure exhibits distinct regional characteristics.

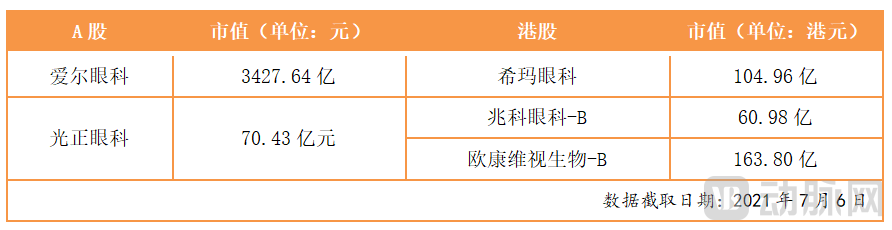

All along,Ophthalmology, as a high-growth sector, represents a scarce investment theme in China’s domestic stock market.For instance, in the A-share market, there are currently only Aier Eye Hospital (300015.SZ) and Guangzheng Eye Hospital (002524.SZ); meanwhile, Chaoju Eye Care’s listing on the Hong Kong Stock Exchange joins a sector that previously included only C-MER Eye Care (03309.HK), Zyklopharma-B (06622.HK), and Ocumeris Biologics-B (01477.HK).

It is precisely this scarcity in the stock market that has drawn significant investor attention to the initial public offerings (IPOs) of ophthalmology-related companies. Last year, regional leaders in the ophthalmology sector, including Huaxia Eye Hospital Group, He Shi Eye Hospital, and Purui Eye Hospital, sequentially filed their prospectuses, sparking widespread debate about the listing of private ophthalmology enterprises. However, a year later, none of these three companies have yet received regulatory approval for their IPOs. In contrast, Chaoju Eye Care, which filed its prospectus in January this year, has become the first to list on the secondary market.

From a single outpatient clinic at its inception to 17 ophthalmic hospitals and 23 optometry centers, culminating in a successful IPO today, what has been the developmental journey of Chaoju Eye Care? Can regional chain institutions expand nationwide? Is there still an opportunity for the next Aier Eye Hospital to emerge in the ophthalmology sector? VCBeat will analyze these questions in the following article.

The Development History of Chaoju Eye Care: A Multi-Generational Entrepreneurial Saga of a Medical Dynasty

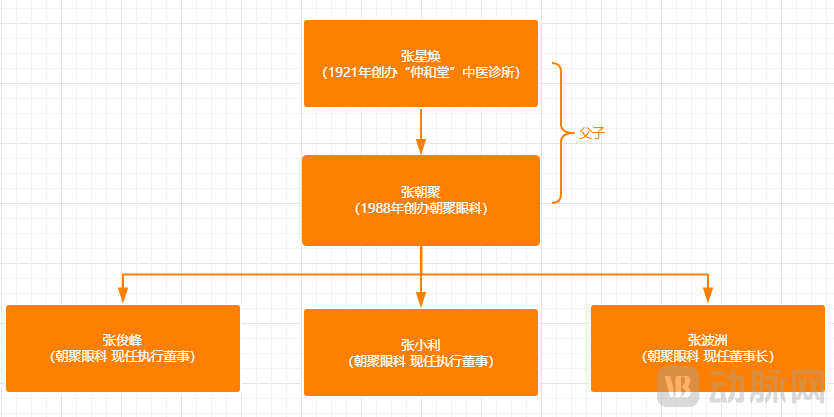

According to the prospectus, Zhang Xinghuan (the grandfather of Zhang Bozhou, current chairman of Chaoju Eye Care), who was born in 1893, gained medical knowledge and training through study tours in his youth. In 1921, he founded a traditional Chinese medicine clinic named Zhonghe Tang, employing an integrated approach combining traditional Chinese and Western medicine.

Influenced by his upbringing, Zhang Chaohui, the son of Zhang Xinghuan, also embarked on a career in medicine, becoming a physician at the Shirenshan Forest Farm Health Center in Henan Province before the age of 20. Later, to acquire specialized knowledge and skills in ophthalmology, Zhang Chaohui was admitted to Henan Medical College. In 1976, he was appointed as the Director of the Department of Ophthalmology at the Dalad Banner People’s Hospital.

Following the launch of China’s reform and opening-up policy, Zhang Chaoju, driven by entrepreneurial spirit, decided to start his own business. In 1988, he joined forces with his eldest daughter, Zhang Xiaoli, and his son, Zhang Bozhou, to establish the predecessor of Chaoju Eye Care in Baotou City, Inner Mongolia Autonomous Region—a clinic spanning approximately 350 square meters and staffed by three or four ophthalmologists. Through the collective efforts of the family, Chaoju Eye Care gradually gained momentum, evolving from a single clinic into a growing network of hospitals.

(Relationship Diagram by VCBeat)

Prior to its IPO, Chaoju Eye Care also attracted significant capital interest and underwent three rounds of financing, with investors including Hui Capital, Lanxin Asia, Jingxu Venture Capital, and Ronghui Capital.

After more than 30 years of development, Chaoju Eye Care, which originated in Inner Mongolia, now spans five provinces or autonomous regions across China, primarily covering the North China region. As of the date of the prospectus, Chaoju Eye Care operates a chain network consisting of 17 ophthalmic hospitals and 23 optometry centers.In terms of workforce size, Chaoju Eye Care currently has 257 registered physicians (including 69 multi-site practicing physicians who are not full-time employees).

Based on total revenue in 2019, Chaoju Eye Care ranked first in Inner Mongolia and second in North China within the domestic ophthalmic medical services sector. In terms of clinical ophthalmology revenue specifically, Chaoju Eye Care ranked fifth nationwide in China.

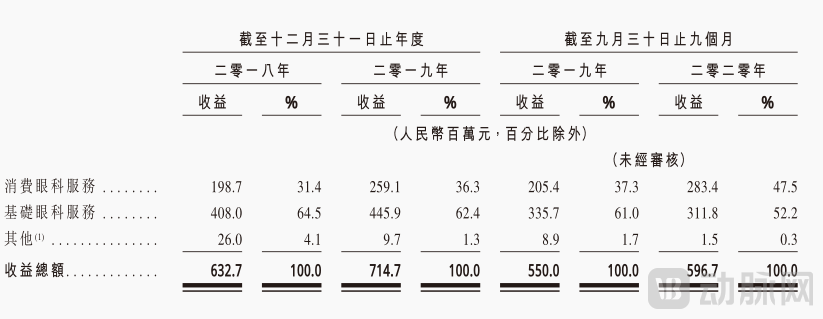

In terms of operations, Chaoju Eye Care’s revenue is currently derived primarily from two segments: “consumer ophthalmic services” and “basic ophthalmic services.”

(Revenue Structure of Chaoju Eye Care; Source: Prospectus)

First, consumer ophthalmology services include refractive correction (including presbyopia correction), myopia prevention and control, optometric myopia prevention and control, as well as optometric products and services. According to the prospectus, this category of services accounted for 46.5% of total revenue in 2020, with a gross profit margin of 50.5%.

Furthermore, basic ophthalmic services encompass the treatment of various common eye conditions, including cataracts, glaucoma, strabismus, fundus diseases, ocular surface diseases, orbital diseases, and pediatric eye disorders, which may be covered by public medical insurance plans. These services accounted for 53.2% of total revenue in 2020, with a gross profit margin of 38.2%.

From the perspective of development trends, consumer ophthalmology services are experiencing the most rapid growth.It is worth noting that in 2018, consumer ophthalmic services accounted for approximately 30% of Chaoju Eye Care’s total revenue, a figure that rose to 46.5% last year.

The reasons behind this are twofold: on one hand, the high gross margins of consumer ophthalmology services, coupled with their consumer-oriented nature, offer greater growth potential; on the other hand, basic ophthalmology services are prone to medical disputes, which compels companies to prioritize the relatively safer consumer ophthalmology segment.

It should be noted that,Chaoju Eye Care’s net profit has maintained steady growth, approaching the level of industry leader Aier Eye Hospital (which had a market capitalization of RMB 342.764 billion on July 6).According to the prospectus, Chaoju Eye Care’s net profit margin increased from 4.6% in 2018 to 9.9% in 2019, and further rose to 17.2% in the first three quarters of 2020. During the same period, Aier Eye Hospital’s net profit margin was approximately 18%.

Of course,The growth in net profit is directly linked to the increase in average spending per patient at Chaoju Eye Hospital.Data show that from 2018 to the first nine months of 2020, the average cost per patient visit was RMB 434, RMB 488, RMB 504, and RMB 657, respectively, exhibiting a rapid upward trend.This indicates that Chaoju Eye Care has continued to expand its efforts in tapping into the spending power of its patient base.Among these, the Optometry Center has seen sustained growth in its customer base, with annual patient visits totaling 73,935, 79,903, and 91,660 over the three-year period.

In summary, it is evident that Chaoju Eye Care has experienced rapid growth in recent years, evolving from a small clinic into a publicly listed ophthalmology chain group. This success stems from both the founding family’s sustained deep-rooted commitment to the local market and Chaoju Eye Care’s continuous efforts in strategic business direction and market expansion capabilities.

However, as the leading regional ophthalmology chain, can Chaoju Eye Care replicate the development path of Aier Eye Hospital with this IPO? The answer may be found by examining the strategic layouts of other leading regional ophthalmology players.

Not only Chaoju Eye Care, which went public today, but also Huaxia Eye Hospital, He Eye Hospital, and Purui Eye Hospital, which had previously filed for IPOs, all exhibit distinct regional characteristics: Chaoju Eye Care is rooted in North China, Huaxia Eye Hospital has deeply cultivated the Southeast, He Eye Hospital focuses on Liaoning Province, and Purui Eye Hospital is based in Southwest China. These four ophthalmic hospital groups have expanded from their respective regional strongholds to establish a nationwide presence across China.

From the perspective of financing needs for public listing, the four companies primarily intend to use the raised funds to build new hospitals or expand existing ones, thereby facilitating their large-scale expansion.

According to the prospectus, Chaoju Eye Care intends to use the funds raised to build two new eye hospitals in Hohhot, one eye hospital and a refractive surgery center in Hangzhou, and one eye hospital in Zhoushan. He Eye Hospital plans to allocate half of the proceeds to the expansion project of Shenyang He Eye Hospital, as well as to the establishment of new hospitals in Beijing and Chongqing. Huaxia Eye Hospital plans to invest the funds in the Tianjin Huaxia Eye Hospital project. Purui Eye Hospital plans to use the funds for the new construction of Changchun Purui Eye Hospital and the renovation of Harbin Purui Eye Hospital.

It is evident that the expansion strategy adopted by the four ophthalmic hospitals involves establishing self-owned facilities, thereby continuing to advance their objective of scaling from a regional presence to a nationwide footprint across China.

In terms of specific strategies for advancing their business layouts, the four companies are largely similar, all adopting a point-to-area approach. Taking Chaoju Eye Care as an example,When expanding into new regions, Chaoju Eye Care typically begins by conducting in-depth research into the characteristics of the local market. It then concentrates resources on establishing its first hospital in areas that align with its anticipated market positioning and local demand. Subsequently, it continuously expands outward from this initial facility, gradually creating a cluster effect.

According to the prospectus, when expanding into eastern Inner Mongolia and neighboring areas, Chaoju Eye Care’s team learned from early surveys that the local population was densely concentrated primarily in county-level urban centers. Consequently, the company established its first hospital in Chifeng, rapidly building a strong local reputation within a short period. Leveraging Chifeng as a strategic hub, Chaoju Eye Care subsequently opened multiple eye hospitals in Chengde, Tongliao, and Hulunbuir.

It is worth noting that Chaoju Eye Care was the first to introduce advanced medical equipment in Inner Mongolia, such as the Optos ultra-widefield fundus camera, vitrectomy system, phacoemulsification device for cataracts, excimer laser, VisuMax SMILE laser, optical coherence tomography (OCT) with blood flow quantification, microperimeter, and corneal confocal microscope. This initiative has significantly enhanced Chaoju Eye Care’s control over the quality of its medical services.

Driven by the continuous increase in the number of hospitals, Chaoju Eye Care has begun to promote multi-site practice among high-level physicians through a cluster-based model, while strengthening regional collaboration, synergies, and resource sharing among its hospitals. For instance, each hospital in the region develops its own specialized clinical focus, and cross-hospital staff training has become easier to implement.

From Points to Surface: Chaoju Eye Care’s Regional Deepening Gradually Yields Results.As of the data cutoff for the prospectus submission, Chaoju Eye Care’s hospitals in Inner Mongolia have treated more than 43 million patients from across China and performed over 560,000 surgical procedures.

In addition, Chaoju Eye Care is actively participating in local public welfare initiatives to build a strong reputation. For instance, its Baotou Hospital is a designated medical institution for national health screenings. It was recognized as a National Demonstration Unit for Scientific Testing and Standardized Treatment of Specialized Ophthalmic Diseases in 2007, and was designated as a National Key Clinical Specialty Construction Project Unit (Ophthalmology) in 2012.

Moreover, Chaoju Eye Care has undertaken multiple government and corporate social responsibility initiatives. Between 2015 and 2020, it promoted the “Journey to Light” public welfare campaign in Inner Mongolia, successfully restoring sight to over 27,000 impoverished patients, thereby further strengthening its brand influence in the region.

As can be observed from the above, leading regional ophthalmology chains attract users by establishing a strong local presence. Once sufficient brand momentum is accumulated, they expand from individual points to broader areas. Subsequently, by leveraging the collaborative advantages of clustered operations, they facilitate synergy between hospitals and talent, thereby achieving expansion under the benefits of scale.

However, although nationwide expansion is a strategic path that leading regional ophthalmology chains all aspire to pursue, these four companies must also confront the management risks inherent in such growth. For instance, as their operational scale continues to expand, they will face significant challenges in resource integration, medical management, financial management, talent management, and market development. The complexity and difficulty of management will gradually increase; if these companies fail to enhance their management standards and service capabilities in the future, it will adversely affect their business operations.

Throughout its development, Aier Eye Hospital has undergone a strategic transition from a regional to a nationwide layout.This lies in the fact that by expanding into external markets, chain enterprises will bring greater potential for revenue growth. Behind this is a significant test of the company's replicability, including management capabilities, quality control abilities, brand strength, and other aspects.

Can regional ophthalmology leaders successfully expand nationwide? Or will another Aier Eye Hospital emerge within the ophthalmology sector? To answer this question, we must return to the ophthalmology chain model for insights.

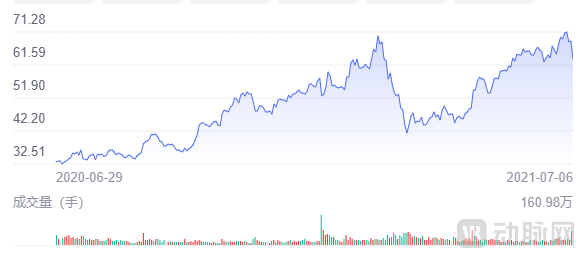

In the ophthalmic chain industry, or indeed across the entire private healthcare services sector, Aier Eye Hospital stands as a quintessential representative. This is becauseAier Eye Hospital has surged more than 60-fold in the decade-plus since its listing on the ChiNext board, with a current market capitalization of nearly RMB 350 billion.

(Chart of Aier Eye Hospital's Stock Price Changes Over the Past Year Source: East Money)

Faced with such a formidable competitor, do other ophthalmic chains still have opportunities? This requires us to examine where the ceiling of the ophthalmic chain industry lies.

As is well known, “golden eyes, silver teeth” has become a default consensus in the healthcare industry. This is because vision, which serves as the input source for 90% of human information, significantly impacts people’s quality of life. Consequently, eye health has garnered widespread public attention.In terms of treatment, the market in the field of ophthalmology is mainly concentrated on medical service institutions.

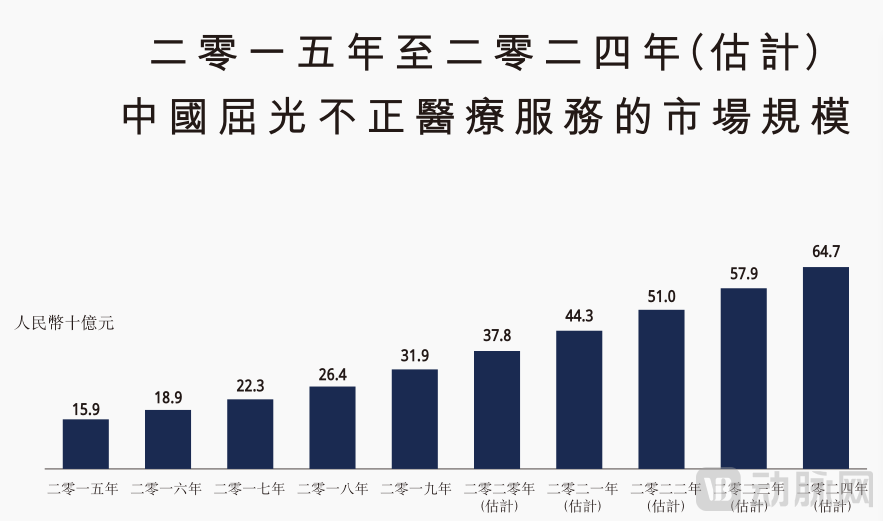

According to Chaoju Eye Care’s prospectus, China’s ophthalmic medical services market has experienced rapid growth, with the industry size expanding from RMB 73 billion in 2015 to RMB 127.5 billion in 2019, representing a compound annual growth rate (CAGR) of 15%. The market is projected to further grow to RMB 223.1 billion by 2024.

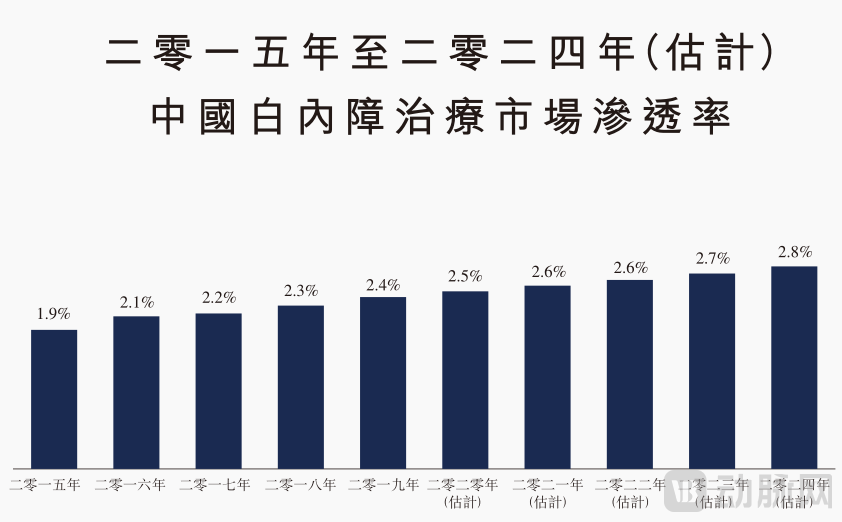

In this vast market,The two segments with the most rapid demand growth are, first, age-related ocular diseases predominantly represented by cataracts, and second, adolescent eye disorders primarily driven by myopia.

Specifically, according to the National Visual Health Report released by Peking University, the incidence of cataracts among elderly individuals aged 60 to 89 is 80%, while it exceeds 90% in those aged 90 and above. Given the large population of cataract patients in China coupled with a relatively low surgical rate, there is substantial room for growth in cataract surgery services.

(Image source: Chaoju Eye Care prospectus)

Regarding data on myopia patients, a report released by the National Health Commission this June showed that the overall prevalence of myopia among children and adolescents in China is 53.6%, with 81% among high school students and 90% among college students. According to earlier statistical data from the World Health Organization, the number of myopia patients in China reached 600 million in 2018, with the adolescent myopia rate ranking first globally.

(Image source: Chaoju Eye Care IPO prospectus)

It can be seen that,The ophthalmic medical services market continues to be driven by robust demand, affording leading regional ophthalmology chains considerable room for future growth.However, what should these companies do to seize this opportunity?

First,Need to continue pursuing the path of chain expansion, thereby reducing costs through economies of scale and strengthening the standardization of medical services. Taking equipment investment as an example, in the ophthalmology industry, the cost of large-scale ophthalmic equipment is generally high, resulting in significant entry barriers. Therefore, for ophthalmic service providers, adopting a chain-based model to amortize equipment and marketing costs is highly feasible.

Second,Enhance operational efficiency and intensify talent acquisition efforts.. As private ophthalmology chains are financially self-sufficient and operate under significant pressure, they are able to offer slightly lower prices than public hospitals while providing consumers with better equipment and superior services, resulting in a distinct competitive advantage. However, this also requires these chain institutions to make substantial efforts to improve operational efficiency and continuously cultivate high-quality medical service talent.

Third,Build Strong Academic Capabilities and Continuously Invest in Medical Development.Although the proportion of R&D expenditure in the medical service industry differs significantly from that in other healthcare subsectors, as companies scale up, possessing unique and industry-leading medical technologies has become a critical factor for sustained success. Taking Aier Eye Hospital as an example, the company has established a comprehensive medical-educational-research system comprising “three hospitals,” “seven institutes,” and “two stations.” It has also founded the Aier Eye Hospital Affiliated with Wuhan University, the Aier School of Ophthalmology at Wuhan University, and the Aier Institute of Ophthalmology at Wuhan University, thereby building industry-leading academic and medical capabilities.

Beyond the aspects mentioned above, leading regional ophthalmology chains still have many capabilities to develop. After all, the market potential is substantial; the scale a company can achieve largely depends on its ability to expand progressively.

Of course, the essence of healthcare lies in returning to its true purpose of saving lives and healing the wounded, as well as embracing humanistic care. Therefore, for Chaoju Eye Care, which is currently going public, and other ophthalmic service providers that are applying for listings,Going public is not the end goal, but rather the starting point on the journey to becoming a great company.