Three Companies File for IPO in Booming Peripheral Intervention Sector, Unleashing a $30B+ Market Dark Horse

In 2021, the medical device industry was booming, with domestic interventional companies going public one after another, ushering in a wave of IPOs.

Amid this wave of IPOs, the peripheral intervention sector is an easily overlooked high-potential track. Historically, most people have perceived this sector as being in its early stages of development, with low penetration rates and a small market size.

But today, peripheral interventions have already supported multiple IPOs.In the peripheral intervention sector, MicroPort Endovastec has emerged as a dark horse with a market capitalization of RMB 30 billion. Since its listing in 2019, MicroPort Endovastec’s stock price has surged by over 600%, pushing its market cap beyond RMB 30 billion.

MicroVascular is not the only listed company in the peripheral intervention sector. On the 5th of this month, JetMed also listed on the Hong Kong Stock Exchange, with its share price surging over 40% on the first day and its market capitalization reaching nearly RMB 20 billion. Meanwhile, Acotec, the third leading player in peripheral intervention, has recently passed the listing hearing and is poised for its IPO on the Hong Kong Stock Exchange.

In terms of revenue-generating capability, peripheral intervention has also shown impressive performance. For LifeTech Scientific, which is already listed on the Hong Kong Stock Exchange, half of its revenue comes from the peripheral vascular business, with the segment generating RMB 410 million in 2020.

The market size of peripheral interventions is comparable to that of neurointerventions, with the market expected to reach RMB 30 billion by 2030. However, competition in this sector is far less intense than in neurointerventions, making it a high-growth blue-ocean market. How much untapped potential remains in the undervalued peripheral intervention sector? How will the IPOs of several leading domestic players reshape the competitive landscape? VCBeat has conducted an in-depth analysis of this sector.

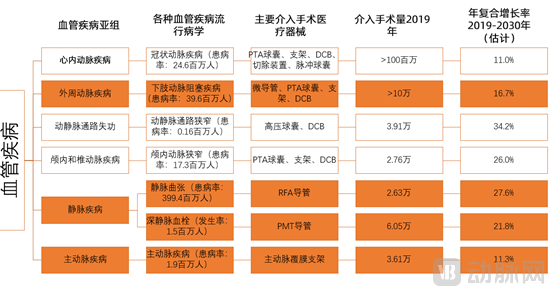

The vascular system is the largest system in the human body. In the treatment of vascular diseases, endovascular interventional therapy has developed rapidly in recent years and is gradually replacing traditional surgery. Endovascular interventions are divided into three major fields: coronary intervention, neurointervention, and peripheral intervention. (Note: The peripheral intervention discussed in this article does not include aortic intervention.)

Among the three major sectors, the first to take off was the coronary intervention market, which gave rise to four major brands: MicroPort, Lepu Medical, Jiwei Medical, and Sino Medical. However, with the implementation of centralized procurement for coronary stents, growth in the coronary intervention market has entered a plateau phase. In contrast, neurointerventional and peripheral interventional markets have only begun to take off in recent years.

Neurointervention is primarily associated with cerebrovascular diseases, involving numerous participants and intense competition.

Peripheral interventions are primarily associated with lower extremity vascular diseases, including lower extremity arterial occlusion, deep vein thrombosis, and varicose veins. Peripheral interventional procedures involve complex pathologies and a wide variety of product types. Currently, the market is dominated by multinational corporations, with few domestic players capable of entering this sector. The market size for peripheral interventions is comparable to that of neurointerventions and is projected to reach RMB 30 billion by 2030.

It has become a global consensus in the medical device industry that the peripheral intervention sector is experiencing rapid growth and will serve as the primary pillar for the expansion of the entire intervention market. Multinational medical device companies such as Medtronic, Boston Scientific, Cordis, and BD are continuously launching new products in the field of peripheral interventions, which has become a major driver of their revenue growth.

Boston Scientific offers solutions for lower extremity arterial, venous, and thrombotic conditions, with a diverse product portfolio. According to Boston Scientific’s 2020 annual report, although revenue from multiple business segments declined due to the global pandemic impact in 2020, its peripheral intervention business bucked the trend, achieving revenue of USD 1.577 billion, a year-on-year increase of 13.1%, and accounting for 15.9% of total revenue.

In the annual report of Medtronic, another medical device giant, peripheral interventional products were also frequently highlighted as a key growth driver. The revenue from Medtronic’s Coronary and Peripheral Vascular segment reached $2.354 billion. While its coronary business was impacted by China’s volume-based procurement (VBP), the growth in drug-coated balloons and peripheral embolization coils partially offset this impact. Furthermore, drug-coated balloons used to treat venous access stenosis in dialysis patients became the primary growth engine for Medtronic in the second quarter of fiscal year 2020.

What are the growth drivers for peripheral interventions in the future?

First, the impact of population aging,Most vascular diseases have a higher prevalence in the elderly population, and the incidence of peripheral vascular diseases will rise with the advent of an aging society. As shown in the figure below, while the patient base for peripheral-related diseases is substantial, the current treatment penetration rate remains low due to the insidious nature of early-stage disease and its relatively low case fatality rate. With increasing health awareness and the implementation of early screening for chronic diseases, the penetration rate of peripheral interventional therapies is expected to further increase.

The second major driver is the decentralization of peripheral interventional procedures to primary care institutions.VCBeat previously interviewed Dr. Zhang Qiang, a leading vascular surgery expert in China. He stated that vascular surgery departments are virtually nonexistent in China’s third-tier cities, and physicians’ understanding of peripheral vascular diseases remains inadequate.

Currently, the Chinese government places significant emphasis on strengthening vascular surgery capabilities at the primary care level. Tier-1 and Tier-2 hospitals are increasingly establishing vascular surgery departments, with peripheral interventional therapy becoming a core service for these grassroots units. Taking venous interventions as an example, deep vein thrombosis (DVT) is clinically recognized as the leading cause of pulmonary thromboembolism (PTE), which carries a high case fatality rate of 25%–30%. The establishment of VTE Prevention and Control Management Centers at various levels represents the fourth major national disease prevention and control initiative, following Pain Centers, Chest Pain Centers, and Stroke Centers. With the widespread setup and development of vascular surgery departments in hospitals across China, the volume of venous interventional procedures is rapidly increasing, and its market potential is expected to be no less than that of coronary interventions.

According to relevant research reports by Frost & Sullivan, the market size of peripheral vascular interventional medical devices in China was RMB 3.01 billion in 2017, and is projected to reach RMB 30 billion by 2030. Currently, multinational corporations account for more than 90% of the domestic peripheral vascular intervention market.

Which products have driven the rapid growth of the peripheral intervention market? Where is the main battlefield for domestic substitution?

To answer this question, it is first necessary to understand the structure of the entire peripheral intervention market. Peripheral interventional devices are divided intoPeripheral Arterial Interventional Devices, Peripheral Venous Interventional Devices, and Access Consumables。

Peripheral Artery Disease (PAD) primarily includes lower extremity artery disease (LEAD), characterized by stenosis or occlusion of the arteries in the legs. Peripheral artery disease is the third most common cause of atherosclerotic vascular disease, following coronary heart disease and stroke.The main products for peripheral artery interventional therapy include: drug-coated balloons, stents, and atherectomy.

Drug-coated balloons are the primary battlefield for competition in peripheral arterial intervention.In the field of peripheral arteries, plain balloon angioplasty and bare-metal stents are two relatively traditional minimally invasive interventional devices for treating stenotic lesions in the lower extremities, yet both have certain limitations. For peripheral arterial disease, the development trend of minimally invasive interventional devices is focused on better addressing the challenges of recanalizing difficult lower-extremity vascular lesions and reducing the high rate of post-procedural restenosis.

The advent of drug-coated balloons has brought a better solution.

Drug-Coated Balloon (DCB) is an angioplasty balloon coated with antiproliferative drugs (mostly paclitaxel). The drug can inhibit the proliferation and migration of smooth muscle cells, thereby further reducing the likelihood of arterial restenosis.

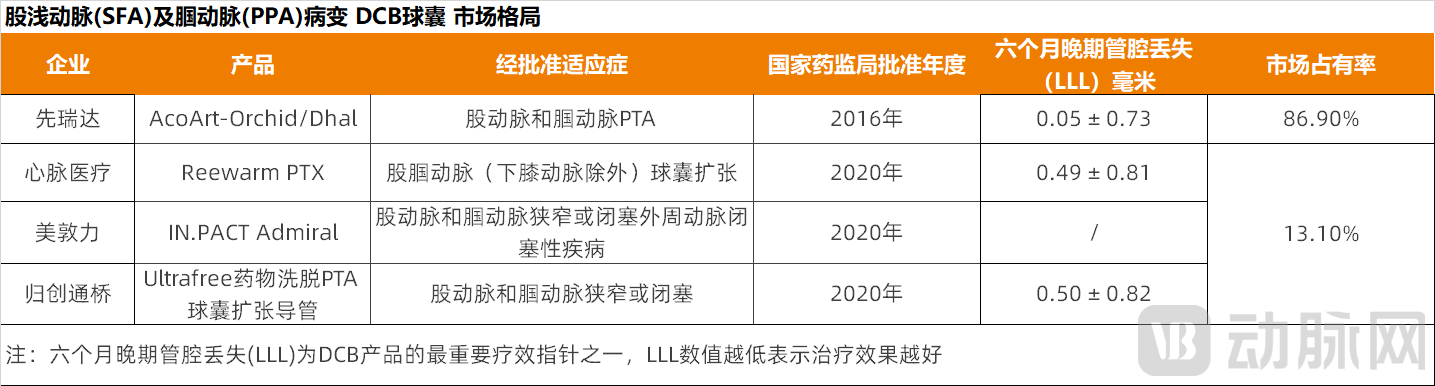

Currently, there are five approved peripheral drug-coated balloons in China, manufactured by three domestic companies—Acotec, MicroPort Endovascular, and JetMed—and one multinational corporation, Medtronic.

Acandis’s first peripheral drug-coated balloon (DCB) was launched four years earlier than competing products. Leveraging this first-mover advantage, Acandis has dominated the overall peripheral DCB market, capturing an 86.9% market share based on 2020 revenue. Furthermore, Acandis is the only company with a DCB indicated for below-the-knee arteries, a product that has also received the FDA’s Breakthrough Device Designation.

In Europe, drug-coated balloons (DCBs) are widely used in coronary and peripheral interventions, whereas in China, drug-eluting balloons have been approved for application inThree Major Application Scenarios: Coronary Artery Disease, Lower Extremity Arterial Disease (LEAD), and Intimal Hyperplasia in Dialysis Patients' Vascular Access.

All three major markets are experiencing rapid growth.

Interventional therapies for lower extremity atherosclerosis (LEAD) are classified intoAbove-the-Knee Intervention and Below-the-Knee (BTK) InterventionIn the above-the-knee (ATK) interventional drug-coated balloon (DCB) market, Acotec started from scratch, launching its product in 2016 and achieving RMB 200 million in revenue by 2020. In 2020, Acotec introduced the AcoArt-Tulip/Litos drug-coated balloons for below-the-knee (BTK) interventions, filling the gap in the BTK DCB segment. The overall peripheral DCB market is expected to accelerate its growth, with its market size estimated to reach RMB 1.3 billion by 2024 (including RMB 363 million from BTK DCB products).

Above-the-Knee Interventional DCB Market Landscape

Why are BTK DCBs held in such high regard, with their market size expected to grow from zero to nearly RMB 400 million within four years?

The primary driver is the large number of diabetic foot patients in China, which reached 7.4 million in 2019. With the market launch of Acotec’s below-the-knee (BTK) drug-coated balloons (DCBs) and the continuously growing population of diabetes patients, the BTK DCB market in China is expected to experience rapid growth.

The use of drug-coated balloons (DCBs) in interventional procedures to treat stenosis caused by arteriovenous fistulas (AVFs) used in hemodialysis (HD) represents a vast, untapped market. Current product supply fails to meet the substantial potential demand.

The number of interventional procedures for treating stenosis in arteriovenous fistulas for hemodialysis in China increased from 7,700 cases in 2015 to 39,100 cases in 2019, and is projected to reach 994,500 cases by 2030. Currently, the only drug-coated balloon for dialysis available on the Chinese market is the APERTO OTW, jointly developed by Grand Pharma and Germany’s Cardionovum GmbH.

Rapidly Growing Demand Amid Product Scarcity: Who Has the Opportunity to Fill the Gap?

VCBeat has found that domestic companies with drug-coated balloon (DCB) products are entering this market by expanding their indications. Taking Acotec as an example, the company expanded the indications for its peripheral drug-coated balloons, AcoArt Orchid® & Dhalia, to nephrology for the treatment of arteriovenous fistula (AVF) stenosis, with the product expected to launch in 2023.

In addition to drug-coated balloons, the peripheral artery field also includes products such as plain balloons, stents, and atherectomy devices. Overall, the market size for peripheral arterial intervention devices grew from RMB 1.4 billion in 2015 to RMB 2.4 billion in 2019. The peripheral arterial intervention market alone is projected to become a multi-billion yuan market by 2030, reaching RMB 12.2 billion, with a compound annual growth rate (CAGR) of 15.7% from 2019 to 2030.

Compared to the already well-established peripheral artery market, the peripheral vein intervention market is at an earlier stage of development. The core product portfolio for peripheral vein interventions is diverse.

Common peripheral venous diseases include deep vein thrombosis, iliac vein compression syndrome, and varicose veins. Each of these three major conditions has its corresponding primary therapeutic products.

Varicose Veins

First, let’s look at the condition with the largest patient population.Varicose Veins. The number of patients with varicose veins reached 390 million in 2019, accounting for 28.4% of the total population. The corresponding blockbuster product for varicose veins is the radiofrequency ablation system.

Radiofrequency ablation utilizes energy generated by laser, microwave, or radiofrequency ablation to destroy and ultimately occlude veins for the treatment of varicose veins.

Supported by a large patient population and the relatively shallow learning curve for physicians performing radiofrequency ablation (RFA), the procedure is well-positioned for rapid adoption in hospitals. The overall RFA market has exhibited robust growth, with the annual number of procedures increasing from fewer than 3,000 in 2015 to 26,300 in 2019, representing a compound annual growth rate (CAGR) of 76.9%. The volume is projected to reach 384,300 procedures by 2030.

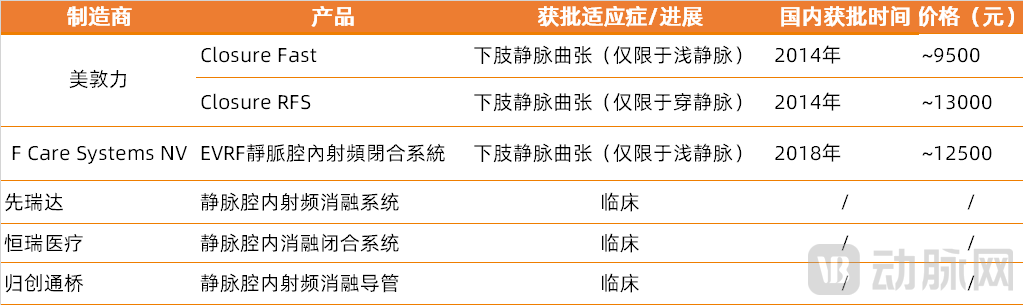

This rapidly growing market is currently dominated by imports; all peripheral radiofrequency ablation products marketed in China are imported, with no domestically produced products yet available. Three domestic products have entered clinical trials: the radiofrequency ablation systems (comprising a radiofrequency ablation generator and catheter) from Acotec and Hengrui Medicine, as well as the peripheral radiofrequency ablation catheter from JetMed.

Deep Vein Thrombosis

Deep vein thrombosis is also a common peripheral venous disease. The number of deep vein thrombosis cases in China increased from 1.1 million in 2015 to 1.5 million in 2019, with a compound annual growth rate of 8.3%.

Interventional therapy has become the preferred treatment for deep vein thrombosis of the lower extremities in China,The four main types of procedures are: catheter-directed thrombolysis (CDT), percutaneous mechanical thrombectomy (PMT), percutaneous transluminal angioplasty (PTA) combined with stent implantation, and inferior vena cava filter (IVCF) placement.

Catheter-directed thrombolysis involves the catheter-based injection of thrombolytic agents to dissolve clots and restore vessel patency. Mechanical thrombectomy primarily utilizes rotational turbine or hydrodynamic principles to fragment or aspirate thrombi, thereby rapidly eliminating or reducing clot burden. While mechanical thrombectomy demonstrates efficacy comparable to catheter-directed thrombolysis, it offers a superior safety profile and shorter procedural duration. Currently, percutaneous mechanical thrombectomy (PMT) catheters marketed in China are manufactured by seven multinational companies: Goodman, Kaneka, Medtronic, Minvasys, Terumo, Straub Medical AG, and Boston Scientific.

An inferior vena cava (IVC) filter is a retrievable, umbrella-shaped device inserted into the large veins to capture large thrombi, preventing them from traveling to the heart and lungs, thereby reducing the incidence of pulmonary embolism, which has an extremely high mortality rate. There are seven marketed retrievable IVC filters in China, with average prices ranging from RMB 10,000 to RMB 20,000. Among these, two models are produced by domestic companies, Weixin Medical and Lifetech Scientific.

However, in recent years, there have been no significant technological breakthroughs in the filters themselves, leading to persistent clinical issues such as inaccurate positioning, filter tilt, and difficult retrieval. To this day, neither international nor Chinese guidelines for the treatment of deep vein thrombosis recommend them as a first-line therapy.

Iliac Vein Compression Syndrome

The primary product for iliac vein compression syndrome is the iliac vein stent.

The primary function of iliac vein stents is to be implanted into compressed iliac veins to restore their original diameter and maintain unimpeded venous blood flow. Currently, only two iliac vein stent products have been approved in China: Zilver Vena by Cook Medical and Venovo by BD Medical. Meanwhile, five domestic iliac vein stents are in clinical trials and are expected to reach the market soon.

Overall, the market size of venous interventional devices in China was only RMB 370 million in 2013. However, the growth rate cannot be overlooked. By 2017, the market size for venous interventions had grown to RMB 890 million. This rapid growth trend will continue to climb quickly alongside the increase in clinical applications of venous interventional procedures. By 2022, the market size is projected to reach RMB 3.1 billion, with a compound annual growth rate (CAGR) of 28.4%.

Access consumables are foundational materials in interventional surgery. Access products represent the first step in physicians' interventional procedures, serving functions such as establishing and constructing vascular access, as well as delivering interventional therapeutic devices. These products include microcatheters, guiding catheters, angiographic catheters, microwires, sheaths, and arterial compression hemostatic bands.

Due to constraints in materials science and manufacturing processes, it is not easy for domestic companies to achieve fully independent research, development, and production of guidewire catheters.Most of the guidewires and catheters currently used in hospitals are still imported from developed countries such as Japan, Europe, and the United States.

In terms of R&D layout for access-related consumables, Acotec, the domestic leader in the peripheral vascular field, has developed peripheral microcatheters. Acotec’s ability to independently manufacture these products is primarily attributed to its mastery of polymer material technology, with its Shenzhen-based R&D team mainly responsible for the design and development of polymer materials.

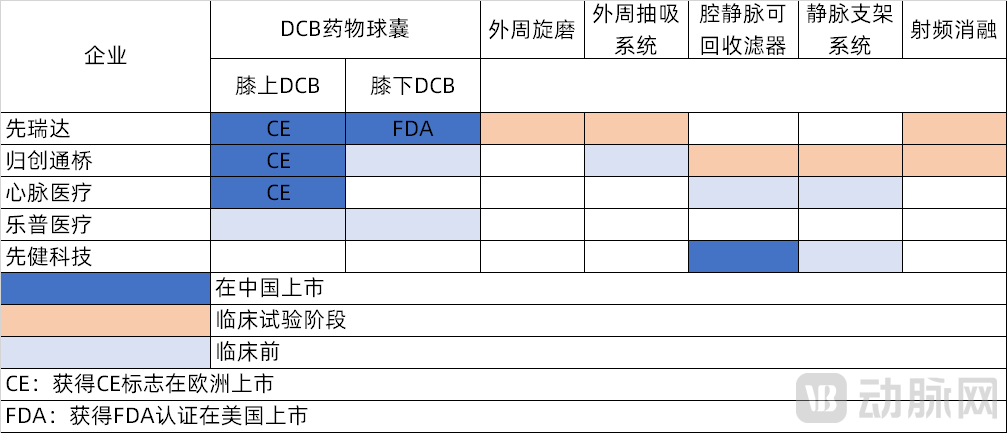

In the existing peripheral intervention market, domestic companies have established portfolios covering all core products. However, it is worth noting that the field of peripheral interventions is still in a relatively early stage of development; the product diversity and specialization lag behind those of other vascular intervention sectors, leading to frequent off-label use by clinicians in practice. Peripheral intervention products continue to undergo optimization.

From the perspective of future trends, what are the development trends in the overall peripheral intervention market?

First, from the perspective of product development trends, the concept of “intervention without implantation” will lead the overall market development.The “intervention without implantation” concept will directly influence clinical practice patterns, thereby reshaping the landscape of the medical device market. For products already on the market in the peripheral intervention field, the most immediate impacts are the expansion of the drug-coated balloon market and the increased use of atherectomy devices.

Drug-coated balloons (DCBs) can effectively inhibit neointimal hyperplasia, thereby reducing the risk of vascular restenosis. Compared with stents, DCB therapy can significantly lower the risk of thrombosis and avoid stent fracture and in-stent restenosis. Drug-coated balloons are regarded as a viable alternative to stent implantation, and the market for drug-coated balloons is expected to expand further in the future.

So-called atherectomy devices do not involve implanting products into blood vessels but rather remove plaque from within the vessels. Currently, the most widely used atherectomy devices in China primarily include directional coronary atherectomy, laser plaque ablation, mechanical thrombectomy, and orbital atherectomy.

The market for vascular debulking devices listed in China is predominantly dominated by imported brands. Few domestic companies have a pipeline of vascular debulking devices. Acandis introduced a peripheral aspiration platform through an acquisition in 2019, establishing a comprehensive solution ranging from aspiration pumps to aspiration catheters. Acandis’ peripheral aspiration system is expected to be the first domestically produced peripheral aspiration system approved by the National Medical Products Administration (NMPA).

From the perspective of market landscape, the development trend of peripheral intervention shows that domestic substitution is a major trend.Currently, the domestic peripheral intervention market is dominated by imported products. Data from 2019 shows that international players held a 90.3% market share in China's peripheral arterial intervention market. There is substantial room for import substitution with domestically produced alternatives. The price advantage of Chinese-made products will drive rapid expansion of the peripheral intervention market and increase its penetration rate.

With the IPOs of multiple companies in China’s peripheral intervention sector, the competitive landscape is undergoing a significant transformation. Who will emerge as the dominant player in the peripheral intervention market? VCBeat has compiled a list of key commercialized products from listed and soon-to-be-listed companies in China’s peripheral intervention field.

Acotec has structured its product portfolio around the “intervention without implantation” philosophy. Its core product, the drug-coated balloon (DCB), has achieved successful commercialization and scaled revenue generation, with both of its flagship products continuously expanding their indications. In its R&D pipeline, Acotec has 24 products under development at various stages, positioning the company to potentially offer a comprehensive suite of intervention-without-implantation solutions in the future.

Gechuang Tongqiao’s core product, the DCB drug-coated balloon, was launched in 2020. Its product portfolio primarily covers stents, balloons, filters, and other related products.

MicroPort Endovascular, a spin-off subsidiary of MicroPort Scientific, focuses on the field of aortic intervention and currently offers products such as peripheral vascular stent systems and peripheral balloon dilation catheters.

Lifetech Scientific has three major business segments: structural heart disease, peripheral vascular disease, and pacemaker electrophysiology. The peripheral vascular business mainly includes vena cava filters and covered stents.

Overall, most domestic high-value medical consumable companies are capable of following trends to develop one or two hotspot products, but few can provide comprehensive solutions for peripheral interventions. The majority remain at the stage of developing single products. While differences in corporate strength may not be apparent from individual products, a gap becomes evident when assessing comprehensive capabilities. Some companies attempt to develop multiple products simultaneously, yet their technical prowess in cross-domain product development is limited. After two to three years of development, these companies are likely to fall significantly behind.

Therefore, completing the product portfolio and diversifying product offerings have become key competitive advantages in the field of peripheral vascular intervention.

Taking Acotec as an example, as a leading provider of peripheral drug-coated balloons both domestically and internationally, Acotec has deeply penetrated its established areas of strength, continuously expanding the indications for its drug-coated balloon products and broadening their application scenarios into nephrology, andrology, neurology, and cardiology.

Meanwhile, Acotec is also expanding horizontally, with a focus on establishing four major technology platforms: drug-coating technology, aspiration platform technology, polymer material technology, and radiofrequency ablation technology.Establish comprehensive product lines across five therapeutic areas on four major platforms, offering a full suite of “intervention without implantation” vascular solutions.

In terms of drug-coating technology, Acotec’s excipient-based coating technology significantly enhances the stability of the drug coating and improves drug retention and absorption in tissue, ensuring that the drug acts on the target lesion without being washed away by blood flow, while also enabling prolonged drug residence time within the lesion tissue. Regarding product portfolio, Acotec is one of the few companies in China capable of developing a diverse range of balloon products, with its R&D pipeline including scoring balloons, cutting balloons, and high-pressure balloons.

On the aspiration platform, Acotec has developed an aspiration pump and aspiration catheters in its R&D pipeline to maximize therapeutic outcomes for physicians performing peripheral thrombectomy procedures. Internal testing conducted by Acotec has demonstrated that its aspiration catheters exhibit excellent performance in terms of aspiration force and kink resistance.

In the field of radiofrequency ablation technology, most domestic companies are limited to manufacturing radiofrequency ablation catheters and lack the capability to independently develop and produce radiofrequency generators. Acandis has independently developed an advanced radiofrequency generator, enabling it to provide physicians with a comprehensive solution for surgical procedures in the future.

Furthermore, Acotec’s peripheral rotational atherectomy device for the treatment of chronic total occlusion (CTO) features a burr specifically designed with a high-speed rotating abrasive head. The device is equipped with one central abrasive head and one eccentric abrasive head, enabling it to open CTOs and remodel the vascular intima. According to Frost & Sullivan, Acotec’s peripheral rotational atherectomy device is the first intravascular debulking device in China to offer both of these functions.

In addition to extensively building its product technology platform, Acandis has extended its industrial chain upstream to achieve broader independent development capabilities, mastering the core technology of balloon and catheter manufacturing: polymer material technology. While most domestic companies rely on imported polymer materials for upstream raw materials, mastering this core technology enables Acandis to accelerate product iteration cycles and develop a more diverse range of products. This lays the foundation for Acandis to become a globally competitive minimally invasive interventional medical device company.

Peripheral intervention market penetration is continuously increasing, yet challenges are mounting. Emerging therapeutic concepts impose higher demands on product development, while growing clinical needs call for greater product diversification. Although securing dominance in the peripheral intervention market is no easy feat, the substantial patient base undoubtedly paves the way for the emergence of multiple leading domestic manufacturers in this sector in the future.