Peripheral Intervention, Neuro Intervention, or Intraocular Lenses: Which Will Be the Next Blue Ocean Market?

On June 21, the “Announcement on the National Centralized Volume-Based Procurement of Artificial Joints (No. 1)” was released, triggering turbulence in the orthopedic consumables market.

Some institutions believe that the increased sales volume after winning bids in centralized procurement may not necessarily offset the profit losses caused by price reductions, and joint-related enterprises still need to seek other avenues.

Feng Wenmeng, a researcher and director of the research office at the Social Development Research Department of the Development Research Center of the State Council, stated in a media interview: “Based on previous pilot programs, the price reduction from this centralized procurement is expected to be no less than 80%.”

As can be seen, the national centralized volume-based procurement (VBP), leveraging its position as a “super purchaser” with access to a “mega market,” has become one of the core factors influencing the strategic layout of high-value medical consumables companies. On the other hand, the national VBP is gradually becoming “normalized,” which will have a significant impact on the high-value medical consumables industry. Studying the national VBP policies will help assess the industry’s future prospects and identify development opportunities for enterprises.

As is well known, the background of the national centralized procurement is the financial pressure on the basic medical insurance fund, which faces a deficit, and its purpose is to control medical insurance costs. Based on this logic, the General Office of the State Council issued the "Notice on Printing and Distributing the Reform Plan for Governing High-Value Medical Consumables" on July 31, 2019. The "Notice" pointed out: ForHigh clinical volume, high procurement cost, mature clinical application, and manufactured by multiple companiesFor high-value medical consumables, explore centralized procurement by category, encourage healthcare institutions to jointly conduct volume-based negotiated procurement, and actively explore cross-provincial alliance procurement.

The state encourages centralized procurement for high-value medical consumables that exhibit four specific characteristics. Among these,High Clinical DosageIt refers to products with high penetration rates; for example, the annual number of coronary stent procedures had already exceeded one million before centralized procurement.

High Procurement AmountIt refers to products with a large market size, significant consumption of the national medical insurance fund, and a substantial financial burden on patients. For example, prior to the centralized procurement of coronary stents, the market size exceeded RMB 10 billion, with a unit price of over RMB 10,000.

Well-Established Clinical UseIt refers to products that have been in clinical use for an extended period, with well-established procedural techniques. For example, coronary stents had already been present in the Chinese market for approximately 20 years prior to volume-based procurement. The differences in product quality and therapeutic efficacy between domestically produced and imported products are minimal, resulting in low risk for physicians when switching between different brands.

Manufactured by Multiple CompaniesThis refers to products manufactured by multiple companies, indicating robust market competition. For instance, prior to the volume-based procurement of coronary stents, over 10 companies had obtained approval for identical products, with a domestic production rate exceeding 70%.

Given these four key characteristics, the inclusion of coronary stents and artificial joints in the centralized procurement program was a natural progression. So, which products and therapeutic areas will be included in the next round of national centralized procurement?

Since 2019, the centralized procurement of medical consumables has become akin to a competition.

In July, Anhui Province conducted centralized procurement of orthopedic implants (spinal) and ophthalmic products (intraocular lenses); Jiangsu Province launched its first round of centralized procurement for sirolimus- and derivative-eluting stents and dual-chamber pacemakers; in 2020, the nine-province alliance of Beijing-Tianjin-Hebei and surrounding regions carried out centralized procurement of intraocular lenses; Fujian Province procured artificial joints, indwelling needles, ultrasonic scalpels, and analgesic pumps; Jiangsu Province’s third round of centralized procurement covered primary total knee arthroplasty prostheses, artificial dura mater (spinal), and hernia repair materials...

Since Anhui Province initiated the first volume-based procurement (VBP) for high-value medical consumables, provinces and municipalities including Jiangsu, Fujian, Zhejiang, Hubei, and Shanghai have successively conducted independent centralized procurement. Meanwhile, provincial-level alliances—such as the 9-province Beijing-Tianjin-Hebei Alliance, the 4-province Chongqing-Guizhou-Yunnan-Henan Alliance, the 10-province Shaanxi Alliance, the 3-province Guizhou-Chongqing-Hainan Alliance, the 7-province Sichuan Alliance, and the 4-province Sichuan-Chongqing-Tibet Alliance—have gradually implemented centralized procurement on an alliance basis.

As of the end of November 2020, six provincial-level alliance-based centralized procurement programs had been implemented, eleven independent procurement initiatives were conducted by individual provinces and municipalities directly under the central government, and more than thirty procurement programs were carried out by prefecture-level cities and city-level alliances. Among these, provincial or inter-provincial alliances primarily focused on the centralized procurement of high-value medical consumables, while prefecture-level cities mainly concentrated on low-value medical consumables.

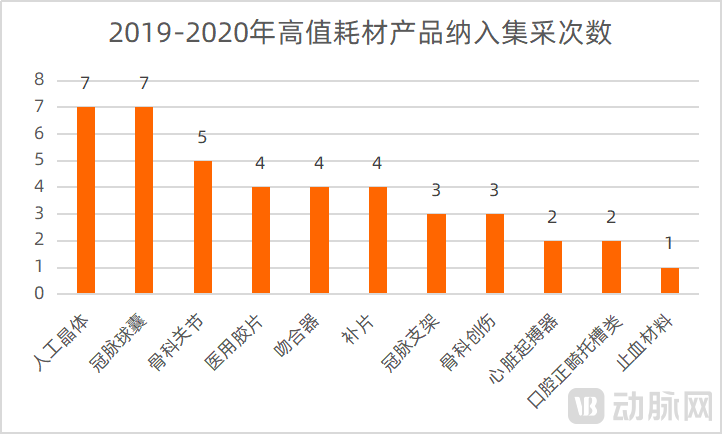

In terms of product categories included in centralized procurement, coronary balloons, intraocular lenses, orthopedic joints, cardiac pacemakers, surgical staplers, and medical films are among the high-value consumables most frequently procured. Centralized procurement products are primarily concentrated in three major fields: cardiovascular intervention, orthopedics, and ophthalmology. This is because these three sectors represent the largest markets by size within China’s high-value consumables industry, characterized by high clinical utilization volumes and high unit prices.

(Data source: Guotai Junan Securities)

Specifically, intraocular lenses, coronary balloons, and orthopedic joints are key targets of provincial, municipal, or alliance-based centralized procurement, making them highly likely to be included in future national-level centralized procurement.

According to data released by Zhiyan Consulting, the market size of intraocular lenses (IOLs) in China grew year by year from 2016 to 2020. In 2019, the market size reached RMB 2.566 billion, and it is projected to reach RMB 2.616 billion in 2020.

According to reports, rigid intraocular lenses (IOLs) are priced at several hundred yuan, while soft IOLs cost over ten thousand yuan. At present, domestic manufacturers occupy the vast majority of the low-end market for rigid IOLs, whereas European and American companies such as Alcon, Johnson & Johnson, Bausch + Lomb, and Zeiss essentially monopolize the soft IOL market. Consequently, the level of import substitution for IOLs remains low, with a domestic production rate of only approximately 20%. In terms of market competition, there are currently 49 imported varieties of monofocal IOLs approved for listing in China, compared to only nine domestically produced varieties.

In addition, intraocular lenses (IOLs) possess multiple functional attributes and can be categorized based on various characteristics, such as foldability, hydrophilicity, monofocal versus multifocal design, and optical surface design.In China, the approved indications for intraocular lenses (IOLs) vary, resulting in limited competition among different companies and products. This has also led to a modest price reduction in the centralized procurement of IOLs.

For example, in 2019, the average price reduction for intraocular lenses (IOLs) through centralized procurement was 20.5% in Anhui Province and 26.89% in Jiangsu Province; in 2020, the average price reduction for IOLs was 54.2% in the Beijing-Tianjin-Hebei “3+N” Alliance centralized procurement and 44% in the Shaanxi-led Ten-Province Alliance centralized procurement.

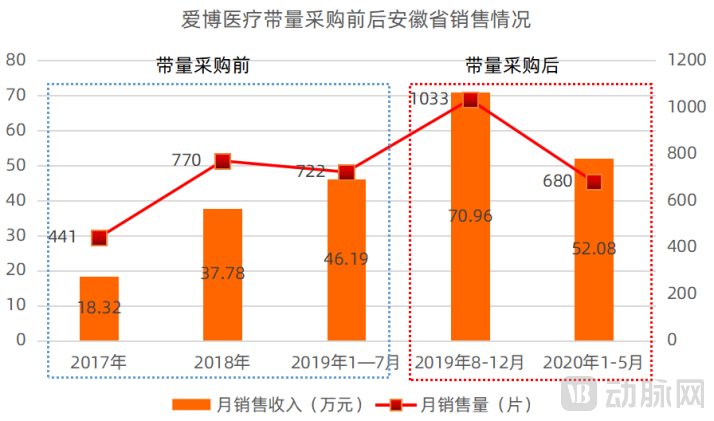

Policy experts stated, “Due to the high barriers to entry for intraocular lenses and the limited number of competitors, the overall price reduction has been relatively moderate. Meanwhile, the successful bids by domestic manufacturers have accelerated the process of import substitution and achieved the goal of exchanging volume for price. Specifically,”Amid gradual price reductions, the acceleration of domestic substitution and increased product penetration have rapidly expanded the market share of Chinese-made intraocular lenses. Consequently, domestic companies have achieved substantial revenue growth, far exceeding their pre-volume-based procurement levels.”

For example, after Anhui Province implemented volume-based procurement for intraocular lenses in 2019, Aier Medical doubled the number of accounts established in public hospitals within the province, and the sales volume of its winning products increased by 1.65 times. Although sales declined in 2020 due to the impact of the pandemic, the average monthly sales revenue remained higher than the pre-procurement level.

Coronary balloons are primarily categorized into semi-compliant and non-compliant types, with a domestic production rate of approximately 40%. According to the medical consumable codes assigned by the National Healthcare Security Administration, there are currently 34 imported coronary balloon models and 34 domestically produced models marketed in China, indicating an equal number of imported and domestic products.

The large number of marketed products and the similarity in their indications have led to intense competition in the coronary balloon market, creating conditions for price reductions through centralized procurement.

In 2020, the centralized procurement of coronary balloon catheters in Guizhou achieved an average price reduction of 85.49% for pre-dilation balloons and 85.15% for post-dilation balloons, with an overall average reduction of 85.32%. In Yunnan, the centralized procurement of coronary balloon catheters resulted in an average price reduction of over 70%. In Hubei, the centralized procurement of coronary balloon catheters saw a maximum price reduction of 96%.

Policy experts stated: “The coronary balloon market is fiercely competitive, with significant overall price reductions. Although this has helped domestic manufacturers accelerate their gain in market share and increase product penetration, the rise in sales volume fails to offset the profit losses incurred by winning bidders, while non-winning companies have lost the majority of their domestic market presence.”

Based on the volume-based procurement status of high-value consumables such as intraocular lenses, coronary balloons, orthopedic joints, medical films, and staplers, we have found that:Currently, high-value medical consumables included in the centralized procurement are primarily those in industries with a market size exceeding RMB 2 billion, a domestic production rate above 20%, and more than three competitors offering single products for the same indication.

Meanwhile, the impact of centralized procurement varies across different industries.For high-barrier, low-competition sectors such as intraocular lenses, centralized procurement will help increase the localization rate, enhance product penetration, and boost the revenue of winning bidders. For highly competitive sectors where technical barriers have already been overcome, such as coronary balloons, centralized procurement will significantly drive down prices and squeeze corporate profits, while simultaneously expanding the market share of winning bidders.

Taking into account factors such as market size, domestic production rate, and competitive landscape, we believe that:In the high-value medical consumables sector, certain red-ocean markets face the risk of substantial price reductions under national centralized procurement and are on the verge of intense “involution.” Conversely, industries characterized by low domestic production rates and few competitors will become investor favorites; even if included in centralized procurement, they are poised for rapid development, akin to the intraocular lens segment.

Currently, the top three segments in China’s high-value medical consumables market by size are vascular intervention, orthopedics, and ophthalmology. In the ophthalmology sector, eye care device companies centered on intraocular lenses have gradually grown, supported by factors such as volume-based procurement (VBP) and technological breakthroughs. In orthopedics, national VBP for artificial joints is imminent, leaving their prospects uncertain. In vascular intervention, coronary intervention has become a widely recognized red-ocean market; products such as coronary stents and coronary balloons have been included in VBP, significantly impacting the industry’s market size. However, within vascular intervention, the niche segments of neurointervention and peripheral intervention remain promising.

The “China Cardiovascular Health and Disease Report 2019” shows that the number of stroke patients in China has reached 13 million, with approximately 2 million new cases each year. Given the large patient population and the high rates of disability and mortality associated with this disease, neurointerventional procedures for treating stroke patients are being gradually promoted, and the market for neurointerventional devices compatible with these procedures is consequently booming.

Public data shows that the market size of neurointerventional medical devices in China increased from RMB 2.6 billion in 2015 to RMB 4.9 billion in 2019, with a compound annual growth rate (CAGR) of 17.3%. It is expected to further increase to RMB 37.1 billion by 2030, representing a CAGR of 20.2% from 2019 to 2030.

Behind the vast market and high growth rate lies fierce competition among at least 24 companies. According to incomplete statistics from VCBeat, to date, there are at least 24 innovative enterprises and 60 investment institutions betting on the neurointerventional field in China. In addition, companies in the neurointerventional sector generally adopt a "full-pipeline layout," which means that there will be many competitors for neurointerventional products launched in the future. It is foreseeable that once these companies' products hit the market, they will face intense competition.Industry insiders believe, “Half of the companies in the neurointerventional field will disappear in the future.”

In response to the impending market competition, companies in the neurointerventional field need to prepare for “close-quarters combat.” Furthermore, given the sector’s characteristics of a large market size and intense competition, these companies must also prepare for the inclusion of their neurointerventional products in centralized volume-based procurement.

Based on prior experience with centralized procurement, neurointerventional products are highly likely to see significant price reductions due to the large number of competitors. Once included in centralized procurement, companies’ profit margins will be substantially impacted, making it difficult to achieve volume-driven compensation for lower prices. Therefore, researching, developing, and promoting innovative products is their only viable path forward.

Overall, before neurointerventional products are included in centralized volume-based procurement (VBP), they will face fierce market competition, leading to the elimination of lower-quality products and companies. After inclusion in VBP, patients will benefit from discounted prices and timely treatment, while healthcare insurance expenditures will decrease. Meanwhile, the penetration rate and market share of domestically produced neurointerventional products will increase; however, it will be difficult for related enterprises to achieve significant profit growth.Therefore, at this stage, selecting the right “racehorses” is particularly crucial for investing in the neurointerventional field.

Peripheral interventions are primarily associated with lower extremity vascular diseases, including lower extremity arterial occlusion, deep vein thrombosis, and varicose veins. According to the "Report on Cardiovascular Health and Diseases in China 2019," there are over 45 million patients with lower extremity arterial disease and nearly 100 million patients with lower extremity venous disease in China. In terms of patient population alone, China has 11 million patients with coronary heart disease, 13 million patients with stroke, and 8.9 million patients with heart failure.The Number of Patients with Peripheral Vascular Disease Is Several Times That of Other Diseases。

According to Frost & Sullivan’s research report, the market size of peripheral vascular interventional medical devices in China was RMB 3.01 billion in 2017 and is projected to reach RMB 30 billion by 2030.

From the perspectives of patient population and market size, there is a possibility that the peripheral intervention sector will be included in centralized volume-based procurement (VBP). In terms of sub-sectors, peripheral interventional lesions are complex, and there is a wide variety of product types. Among these, competition is relatively fierce for products such as peripheral balloon dilation catheters, aortic stents, and general catheters, with multiple products already on the market or numerous companies engaged in R&D. In contrast, competitive pressure is lower for products such as peripheral drug-coated balloons, peripheral radiofrequency ablation catheters, peripheral aspiration catheters, and peripheral thrombectomy catheters, as there are currently few domestically marketed products in these categories, or only imported products are available.

Therefore, in the field of peripheral interventions, certain sub-sectors face significant competitive risks, while others, such as peripheral drug-coated balloons and peripheral aspiration catheters, remain attractive investment opportunities.

According to statistics from VCBeat, only five peripheral drug-coated balloons have been approved in China, manufactured by Acotec, MicroPort Endovascular, Genesis MedTech, and the multinational corporation Medtronic. Notably, Acotec’s first peripheral drug-coated balloon was the earliest to be launched in the Chinese market, and its second peripheral drug-coated balloon, along with three other products, received approval for launch in 2020. Leveraging its first-mover advantage, Acotec has dominated the peripheral drug-coated balloon market, capturing a market share of 86.9% based on 2020 revenue.

Considering multiple factors such as market size, localization rate, and competitive landscape, we judge that products like peripheral drug-coated balloons, bioresorbable stents, heart valves, and radiofrequency ablation catheters are still in the early stages of development. These sectors exhibit significant market potential, have few competitors, and offer substantial room for import substitution with domestically produced alternatives in certain areas. Therefore, as centralized procurement for orthopedics takes effect and competition intensifies in neurointervention, sectors such as peripheral drug-coated balloons and bioresorbable stents are highly likely to become focal points for capital market investment.

Peripheral drug-coated balloons are primarily associated with peripheral artery disease of the lower extremities. It is reported that this condition can cause leg pain and increase the risk of open, infected skin wounds. If not treated early, peripheral artery disease of the lower extremities may lead to tissue necrosis in the legs, potentially necessitating amputation.

According to data released by Frost & Sullivan, the number of patients with lower extremity arterial disease in China increased from 35.8 million in 2015 to 39.6 million in 2019, representing a compound annual growth rate (CAGR) of 2.5%, and is expected to reach 49.8 million by 2030.

In terms of treatment, behavioral modifications and pharmacotherapy are the primary approaches in the early stages of lower extremity artery disease (LEAD). In more advanced stages, such as critical limb ischemia and acute limb ischemia, revascularization via endovascular intervention or bypass surgery is essential to reduce the risk of amputation. Based on the anatomical location of the target lesions, lower extremity endovascular interventions are categorized into above-the-knee and below-the-knee procedures.

Publicly available information indicates that above-the-knee interventions primarily target lesions of the superficial femoral artery and popliteal artery. The main interventional techniques used to treat superficial femoral and popliteal artery lesions include percutaneous transluminal angioplasty (PTA) with balloons, stenting, and drug-coated balloons.

The primary drawback of plain balloon angioplasty (PTA) is the high probability of early post-procedural restenosis. While stent therapy can effectively prevent restenosis, it may lead to complications such as thrombosis, stent fracture, and in-stent restenosis. Drug-coated balloon (DCB) therapy represents an innovative approach; compared with PTA, it can effectively inhibit neointimal hyperplasia, thereby reducing the likelihood of restenosis. Compared with stent therapy, it significantly lowers the risk of thrombosis, avoids stent fracture and in-stent restenosis, and fulfills the value proposition of “intervention without implantation” within the human body.

Driven by the advantages of drug-coated balloon (DCB) therapy, the number of lower-extremity DCB procedures in China increased from zero in 2015 to 12,000 in 2019, and is projected to reach 380,000 by 2030.

From a market perspective, the market size of drug-coated balloons for lower extremities in China was RMB 140 million in 2019 and is projected to reach RMB 1.3 billion by 2024, representing a compound annual growth rate (CAGR) of approximately 55.1% from 2019 to 2024.

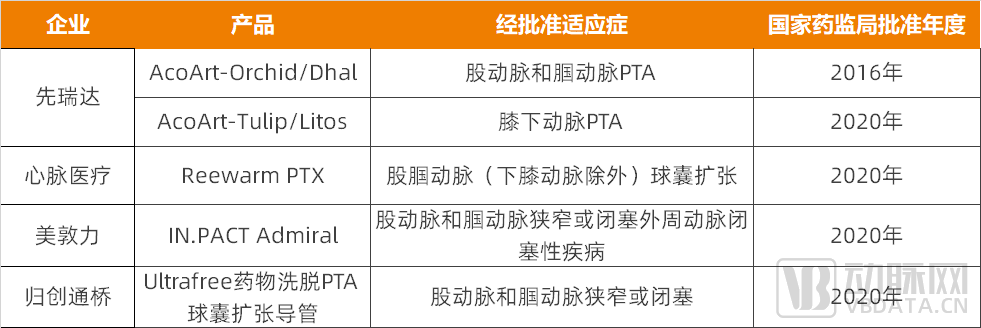

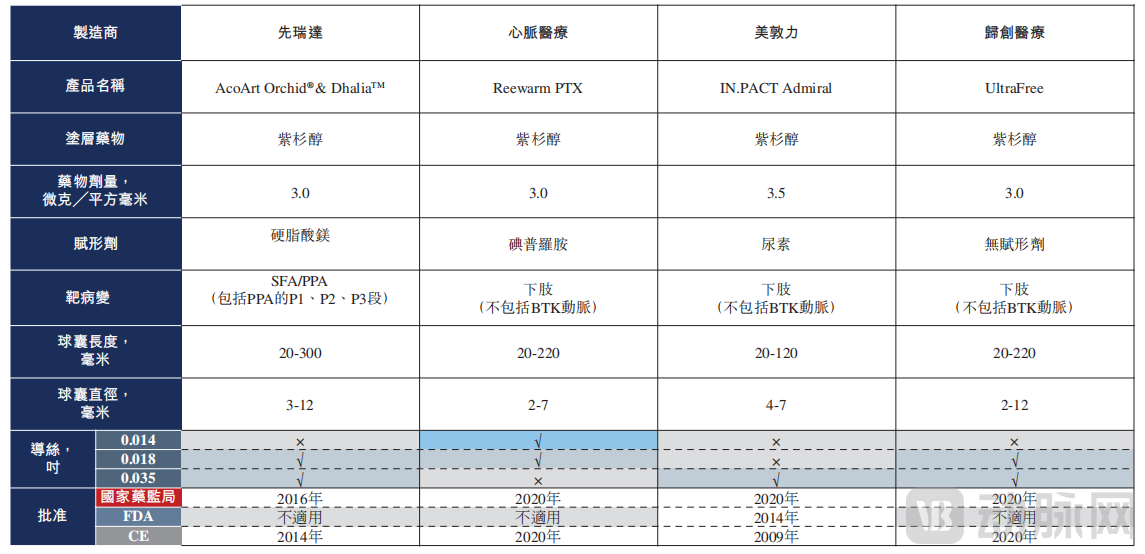

In terms of products, four drug-coated balloon (DCB) products for the treatment of lesions in the superficial femoral artery and popliteal artery have been approved to date. Among them, Acotec’s product was approved in 2016, making it the first to be launched and sold in the Chinese market. Furthermore, the indications for all four approved products do not include below-the-knee arterial lesions, such as those affecting the tibial arteries, peroneal artery, and dorsalis pedis artery.

Clinical experts state that lesions in the tibial, peroneal, and dorsalis pedis arteries require below-the-knee (BTK) interventional treatment. It is reported that such lesions generally have a smaller diameter than above-the-knee arteries and are longer in length; therefore, stent implantation is not suitable for these cases. Currently, low-profile PTA balloons are the mainstream treatment modality for BTK arterial lesions. However, with growing awareness among patients and physicians regarding drug-coated balloons (DCBs), the use of DCBs for BTK interventions is poised for rapid development in China.

Currently, there is only one approved drug-coated balloon product for below-the-knee arterial disease in China, which is owned by Acotec. It is believed that with the demonstration of clinical efficacy and market promotion, drug-coated balloon therapy for below-the-knee arterial disease will gradually become mainstream. According to Acotec’s prospectus, the market size for drug-coated balloons used in the treatment of below-the-knee arterial disease is projected to reach RMB 363 million in 2024 and grow to RMB 1.5 billion by 2030.

According to publicly available information, one of Acotec’s core products is AcoArt TulipTM & LitosTMIt is the first and only drug-coated balloon product approved by the National Medical Products Administration (NMPA) in China for the treatment of infrapopliteal arterial disease. Currently, there are no similar products undergoing clinical trials in China. This indicates that over the next 3–5 years, the likelihood of other drug-coated balloon products for infrapopliteal arterial disease gaining market approval is low, resulting in limited competition and a lower probability of inclusion in centralized volume-based procurement programs.

Based on an analysis of factors such as market size and competitive landscape, we judge that:The peripheral drug-coated balloon sector remains in its early stages of development, making its inclusion in centralized volume-based procurement (VBP) unlikely. Even if included, limited competition and other factors would likely result in modest price reductions. Furthermore, such inclusion could present an opportunity to benefit from national VBP programs by enhancing product penetration and increasing the localization rate.

Consequently, amid the centralized procurement of coronary stents and orthopedic joints, as well as the fierce competition in neurointervention, peripheral drug-coated balloons are highly likely to attract capital interest.