Lepu Bio: A Rising Domestic ADC Leader Focused on First-in-Class, Non-Me-Too Targets

2021 can be regarded as the first year of commercialization for domestically produced ADCs in China.

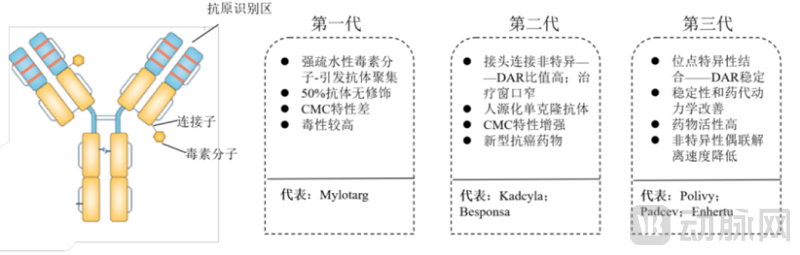

ADC drugs are hailed by the industry as "biological missiles." Unlike traditional chemotherapy agents, which lack tumor specificity, ADCs link biologically active small-molecule drugs to monoclonal antibodies via a chemical linker. The monoclonal antibody serves as a carrier, delivering the small-molecule drug specifically to target cells. This approach enhances the targeting precision of anticancer therapy while allowing for reduced chemotherapy dosages and minimized toxic side effects, earning it the reputation of being "precision-enhanced chemotherapy."

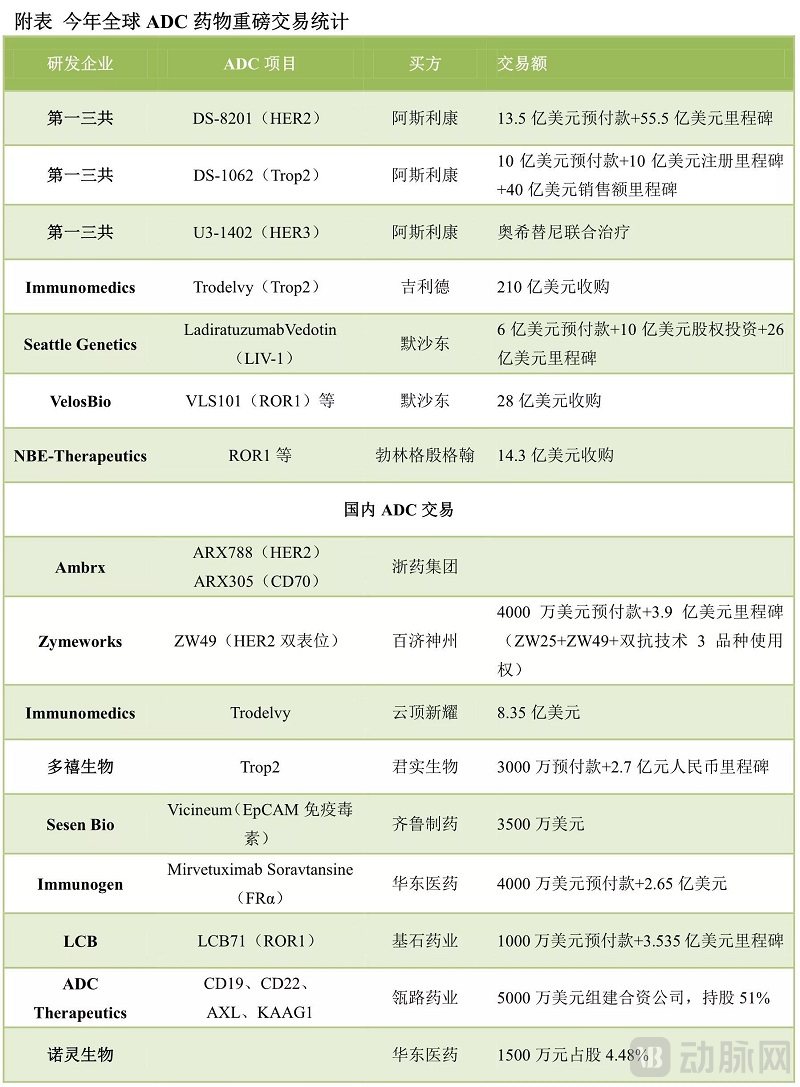

Thanks to the superior mechanism of action of antibody-drug conjugates (ADCs), blockbuster drugs have emerged frequently. Roche’s first ADC, T-DM1, achieved sales of approximately $1.435 billion in 2019, while Daiichi Sankyo’s DS-8201 secured a license-out deal with AstraZeneca valued at nearly $7 billion.

Over the past two years, multinational pharmaceutical giants such as Gilead Sciences, Merck & Co., and Boehringer Ingelheim have intensively completed their ADC (Antibody-Drug Conjugate) asset portfolios, with total transaction values generally exceeding $1 billion. In contrast, leading Chinese pharmaceutical companies are also seeking rapid entry into this high-potential therapeutic area through license-in agreements or equity investments.

(Source: Medical Notes)

Despite the surge in ADC drug development among domestic pharmaceutical companies, the industry is also facing challenges similar to those seen with PD-1 inhibitors and CAR-T therapies:Research on mature targets suffers from severe homogenization.

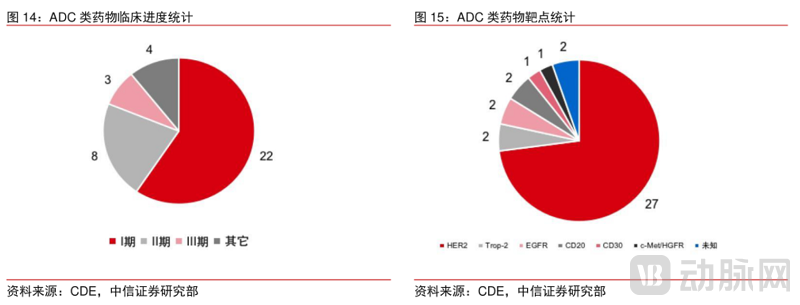

Clinical statistics from the Center for Drug Evaluation (CDE) show that, by the end of 2020, there were 57 ongoing ADC clinical trials in China, with Chinese pharmaceutical companies sponsoring 37 of them. Among these 37 trials, 22 were in Phase I, and only 3 had advanced to Phase III. In terms of targets, 27 trials (73%) targeted HER2, followed by targets such as Trop-2.

(Source: CITIC Securities)

Recently, Bio-Thera Solutions terminated the clinical studies of two ADCs, and the new policies issued by the CDE have sounded an alarm for pharmaceutical companies attempting to “skirt the edges” of regulations. On one hand, this will prompt some me-too drug developers to reevaluate their pipelines and R&D strategies, leading to a sharp decline in the number of ADCs targeting homogeneous indications entering clinical trials in the future. On the other hand, most domestic HER2 ADCs are currently in Phase I; as these pipelines advance to Phase II/III, they may face challenges related to changes in control groups. Among these, faster-moving me-too and me-worse products may secure approvals for niche indications, while slower ones risk repeating Bio-Thera’s fate.

In any case, this is clearly advantageous for ADC developers with strong in-house R&D capabilities and differentiated pipeline target layouts. The release of additional clinical resources facilitates more efficient R&D execution, while also reinforcing the market’s recognition of the value offered by leading players.

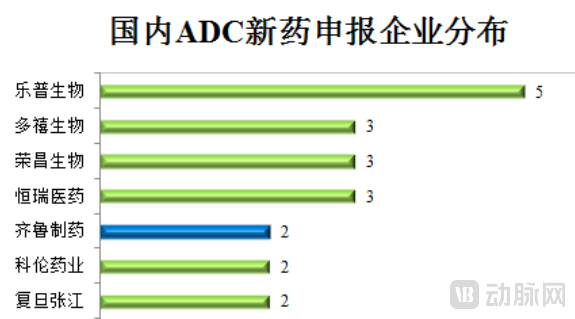

A review of the number of ADC clinical pipelines among domestic pharmaceutical companies shows that Lepu Biopharma leads its competitors with five ADC candidates. However, some skepticism has emerged in the market, stemming from the fact that the company’s ADC platform was acquired from Mayacure.

There is a fundamental distinction between in-licensing and M&A integration. The latter represents a more challenging path, testing not only the vision and boldness of corporate management but also the company’s internal operational integration capabilities. From a return perspective, the value generated by successful M&A integration far exceeds that of in-licensing.

Pharmaceutical companies’ choice of License-in pipelines is essentially a form of “borrowing.” By skipping preclinical R&D steps and directly bridging to clinical trials in China, the market tends to view this approach as an alternative form of CSO (Contract Sales Organization). This is because it not only fails to demonstrate R&D capabilities but also forfeits the core value proposition of Biotech firms: License-out. Currently, it is evident that enthusiasm in the Hong Kong stock market for Biotech companies that cobble together a few License-in pipelines to go public is rapidly waning.

Lepu Biopharma, leveraging its strategic affiliation with the Lepu Group, has pursued a path of “wholly-owned M&A.” For instance, it secured global rights to PD-1 and PD-L1 at a relatively low cost in the early stages by acquiring controlling stakes in Hanzhong Biopharmaceuticals and Houde Aoke. It also acquired Meiyake through two separate transactions, thereby gaining a valuable advanced ADC platform and an in-house R&D team. Compared to the license-in model, this “integration” approach represents a paradigm-shifting advantage: it not only delivers immediate R&D capabilities from the acquired entities but also preserves the core value realization expectations of biotech companies by securing global core rights.

Lepu Biopharma was established in 2018 and has completed three rounds of financing over the past three years, attracting numerous professional investment funds from the pharmaceutical and healthcare industries, including Vivo Capital, Suzhou Danqing, SDIC Chuanghe, Ping An Capital, Sunshine Life/Ronghui Sunshine, China Reform Holdings Corporation, and the Shanghai Bio-medicine Fund.

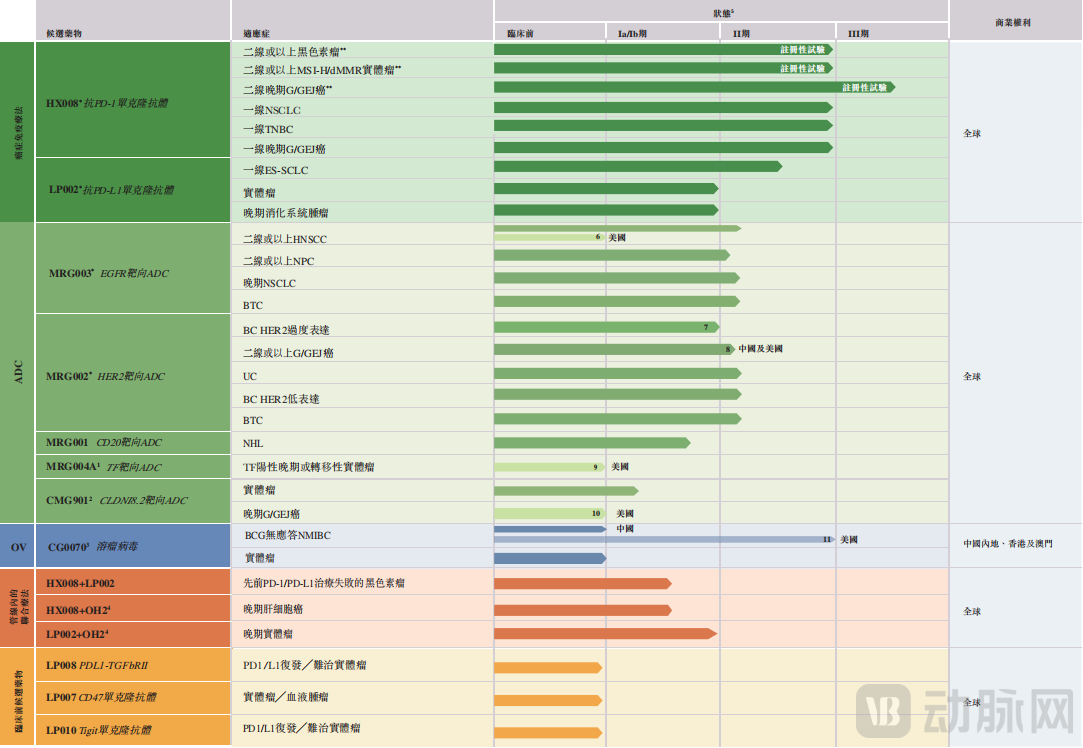

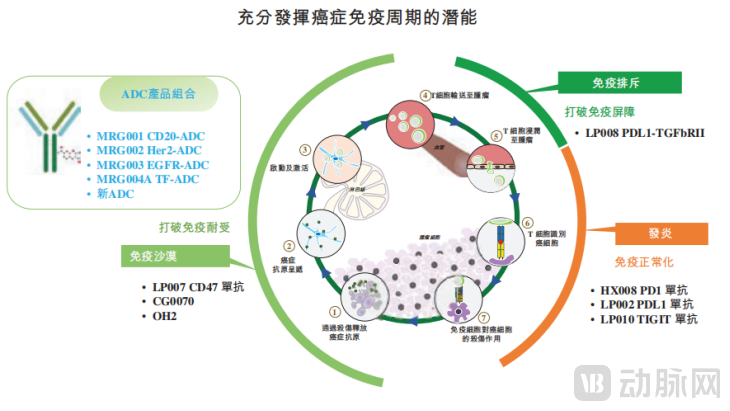

Lepu Biopharma has built a series of differentiated pipeline platforms through a “triple-drive” model comprising independent R&D, strategic collaborations, and investment & M&A. Its areas of strength are concentrated in antibody-drug conjugates (ADCs), positioning it among the top tier in China.

(Source: Lepu Biopharma Prospectus)

●EGFR-ADC (MRG003): This pipeline represents the first-in-class and only EGFR-targeting ADC drug currently in clinical development in China.EGFR is a member of the epidermal growth factor receptor family and is highly expressed in various solid tumors. Consequently, over the past two decades, numerous blockbuster drugs targeting EGFR have been developed. However, both small-molecule inhibitors and monoclonal antibody therapies have encountered resistance during treatment due to various EGFR mutations. This has brought research into more effective therapeutic agents, such as antibody-drug conjugates (ADCs) and bispecific antibodies, to the forefront.

Lepu Biopharma’s EGFR ADC features an innovative design that enables binding to the extracellular domain followed by internalization into cells to exert its therapeutic effect, thereby overcoming various types of drug resistance caused by common EGFR mutations.

Regarding indications, the company is prioritizing the development of three major indications: head and neck squamous cell carcinoma (HNSCC), nasopharyngeal carcinoma (NPC), and non-small cell lung cancer (NSCLC). The latest Phase 1b clinical trial results demonstrated that MRG003 achieved an overall response rate (ORR) of 40% and a disease control rate (DCR) of 80% in the treatment of HNSCC. For NPC, the ORR reached 44%, with a DCR of 78.0%. Taking HNSCC as an example, the current primary treatment modalities in China include cetuximab combined with chemotherapy and pembrolizumab (“Keytruda”) therapy; however, the ORR for pembrolizumab as a second-line treatment for HNSCC is only 18%.[1], in comparison, Lepu’s EGFR ADC has demonstrated certain potential in its preliminary clinical data.

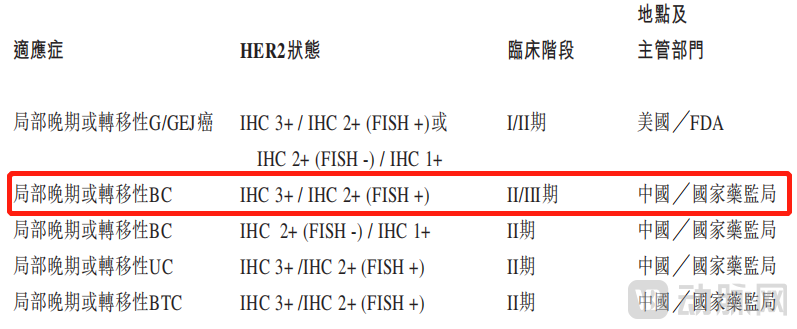

● HER2-ADC(MRG002): In the niche segment of HER2 ADCs, Roche’s T-DM1 and Daiichi Sankyo’s DS-8201 have long been two major hurdles for Chinese R&D manufacturers. Currently, RemeGen’s RC48 has received approval in China; however, data indicate that its safety and efficacy are only comparable to those of T-DM1, placing it at a disadvantage compared with DS-8201.

The latest clinical data demonstrate that MRG002 has a favorable safety profile, with an objective response rate (ORR) of 50.0% and a disease control rate (DCR) of 81.3%. These preliminary efficacy results highlight its potential to be comparable to most leading international antibody-drug conjugates (ADCs). Future indication expansion for MRG002 will focus on breast cancer, urothelial carcinoma, gastric cancer, and cholangiocarcinoma, with the New Drug Application (NDA) in China expected to be submitted as early as 2023.

The differentiated competitiveness of Lepu Biopharma’s MRG002 lies in the fact that both DS-8201 and T-DM1 carry a risk of interstitial lung disease, a serious adverse event, whereas preliminary clinical data for MRG002 have not reported such serious adverse events as interstitial lung disease or ocular disorders, demonstrating an excellent safety profile.

● CD20-ADC (MRG001): This pipeline represents Lepu Biopharma’s strategic focus in the field of hematologic malignancy treatment. Currently, no CD20 ADC products have been approved globally. In China, only two CD20 ADCs have entered clinical stages: Lepu Biopharma’s MRG001 and Tris Pharma’s TRS005, resulting in a relatively moderate competitive landscape.

The combination of CD19 and CD20 targets covers nearly all subtypes of malignant lymphoma; however, resistance commonly emerges during monotherapy with corresponding monoclonal antibodies. Although existing CAR-T products have demonstrated promising efficacy, issues such as cytokine release syndrome, neurotoxicity, and high treatment costs limit the number of patients who can benefit.

Lepu Biopharma’s MRG001, with its unique design, is expected to address the widespread resistance to CD20 monoclonal antibody therapy in non-Hodgkin lymphoma (NHL), and has demonstrated certain efficacy in preclinical studies and preliminary Phase I clinical data.

● TF-ADC(MRG004A): Tissue factor (TF) is a transmembrane glycoprotein essential for hemostasis and is abnormally expressed by tumor cells. TF has been found to be overexpressed in various cancers, including breast cancer, lung cancer, colorectal cancer, pancreatic cancer, and hepatocellular carcinoma. Consequently, TF is widely recognized in the market as a promising frontier therapeutic target. Currently, there are no approved TF-targeted therapies available globally. The only notable development is the TF-directed antibody-drug conjugate (ADC) jointly developed by Seagen and Genmab, for which a Biologics License Application (BLA) was submitted to the U.S. FDA in February of this year for the treatment of recurrent or metastatic cervical cancer following chemotherapy.

(Source: PharmaCube NextPharma Database)

In February this year, Lepu Biopharma’s MRG004A received clinical trial approval from the U.S. FDA. In early June, the National Medical Products Administration (NMPA) formally accepted the Investigational New Drug (IND) application for its Tissue Factor (TF)-targeting Antibody-Drug Conjugate (ADC). The company plans to explore the use of this therapy in TF-positive advanced solid tumors, including cervical cancer, ovarian cancer, and pancreatic cancer.

In addition to the four ADC candidates in its clinical-stage pipeline, Lepu Biopharma has co-developed CMG901, the world’s first anti-CLDN18.2 ADC to enter clinical trials, in collaboration with Keymed Biosciences, which recently listed on the Hong Kong Stock Exchange. Meanwhile, Lepu Biopharma has also built a portfolio of early-stage ADC candidates through in-house R&D and early-stage global rights buyouts.

In addition to its ADC pipeline portfolio, Lepu Biopharma has also made in-depth strategic layouts in the fields of immune checkpoint PD-1 and cutting-edge oncolytic viruses.

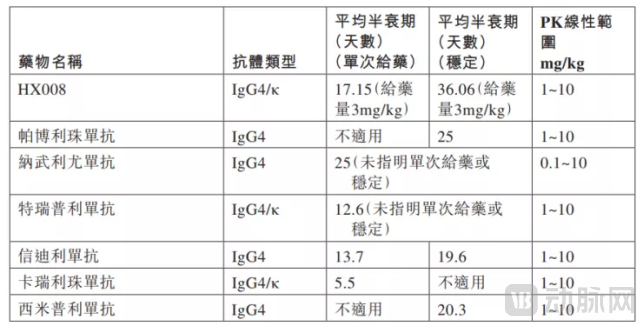

●PD-1(HX008)On July 5, the National Medical Products Administration (NMPA) accepted the marketing application for Lepu Biopharma’s PD-1 inhibitor, putrilimab, for the indication of second-line and later treatment of advanced melanoma. In terms of the current domestic market landscape and overall development progress, Lepu Biopharma’s PD-1 does not hold a first-mover advantage. However, compared with already marketed PD-1 products, it still exhibits certain differentiating features. The differentiation of putrilimab lies in its half-life extension design strategy; it has a longer half-life relative to Keytruda, which is expected to reduce dosing frequency and treatment costs, thereby improving patient adherence.

It is also worth noting that Lepu Biopharma plans to conduct a head-to-head comparison with Keytruda in the first-line treatment of non-small cell lung cancer (NSCLC) as part of its clinical development design, demonstrating the company’s confidence and courage in its own drug.

PD-1 inhibitors are cornerstone products in immunotherapy. Why, then, do international pharmaceutical giants such as Eli Lilly and Novartis, despite lagging significantly behind Keytruda and Opdivo, still invest heavily in licensing PD-1 inhibitors from China? The reason lies in the pivotal role PD-1 inhibitors play in combination therapies with various other drugs, which holds substantial strategic value for pharmaceutical companies in driving the adoption of other agents within their portfolios. “It is acceptable for your PD-1 inhibitor to be second-tier, but you must have one.”

●Oncolytic Virus (CG0070): As a novel cancer immunotherapy, oncolytic viruses have garnered widespread global attention by lysing tumors, releasing tumor antigens, and activating the body’s anti-tumor immune response.

CG0070, licensed by Lepu Biopharma from CG Oncology, is currently in Phase III clinical trials in the United States and has demonstrated significant efficacy in the treatment of bladder cancer.[2]。

Given the potential of combining oncolytic viruses with immunotherapy, CG0070 is also being explored in combination with other drugs to further expand its potential indications and seek more effective treatment options.

Lepu Biopharma holds multiple PD-1 and ADC pipelines nearing commercialization. The true potential for significant growth may lie not only in a few potential first-in-class or best-in-class ADCs, but also in combination therapies.

To cite two examples, in the early-to-mid-stage clinical trials of RemeGen’s RC48 (disitamab vedotin) in combination with toripalimab for the treatment of urothelial carcinoma, the objective response rate (ORR) reached 80%, and the disease control rate (DCR) reached 90%.[3]; Data from a Phase 1b/2 trial of a Seattle-based company’s Nectin-4 ADC in combination with Merck’s Keytruda for first-line treatment of metastatic urothelial carcinoma showed an objective response rate (ORR) of 73.3% and a median overall survival (OS) of 12.3 months.[4]; both cases demonstrated remarkably impressive therapeutic efficacy.

Lepu Biopharma has already initiated a series of clinical explorations into combination therapies centered on PD-1/PD-L1 within its publicly disclosed pipeline. In the future, strategies such as “PD-1 + ADC” or “PD-1 + oncolytic virus” may well prove to be the true “game-changers.”

Backed by the Lepu Group, Lepu Biopharma enjoys inherent advantages in commercialization and the utilization of clinical resources, which is the core reason why it has garnered favor from numerous state-backed funds. Looking ahead, market expectations seem to hinge on waiting for the realization of new milestones in the company’s pipeline; we believe Lepu Biopharma will not disappoint us.

References & Footnotes:

[1] The Next Frontier for EGFR: Bispecific Antibodies and ADCs;

[2] NMPA | Lepu Biopharma Licenses Phase III Oncolytic Adenovirus CG0070;

[3] [Essence Securities] ASCO Preview Series (III): ADC—Latest Data on Therapies (Chinese Companies);

[4] Padcev + Keytruda Approved for Treating Bladder Cancer in Patients Unfit for Chemotherapy: How Effective Is It? How to Seek Treatment Abroad?