Cooling U.S. SPAC Issuance Fails to Dampen HKEX's Enthusiasm for New Rules: How Far Can SPACs Go?

In early June, news emerged that the Hong Kong Stock Exchange (HKEX) would explore the introduction of a Special Purpose Acquisition Company (SPAC) listing framework in the third quarter. Previously, in March, John Lee, the Financial Secretary of the Hong Kong Special Administrative Region, had requested the HKEX and regulatory authorities to study the promotion of SPAC listings in Hong Kong and propose a framework tailored to the local market. It was projected that the first SPAC could list on the HKEX as early as the end of 2021. If implemented, this would mark another major reform of the HKEX’s listing regime, following its 2018 move to open the doors to pre-revenue biopharmaceutical companies.

In early July, rumors circulated that Singapore-based acquisition company Novo Tellus was considering joining Vertex, a Temasek subsidiary, to co-sponsor Singapore’s first Special Purpose Acquisition Company (SPAC). In response, Xie Caihan, Chief Trading Representative of the Singapore Exchange (SGX) in Beijing, shared this news on her WeChat Moments and invited potential issuers to engage with SGX in exploring how to list SPACs in Singapore. It is understood that SGX has been studying and drafting SPAC listing regulations, and has already established a regulatory framework covering aspects such as market capitalization thresholds and warrant rules.

However, in the U.S. capital markets, where this wave of SPAC frenzy initially emerged, despite the number and amount of SPAC IPOs in 2020Hit a new high,For the first time surpassing traditional IPOs, 296 SPACs were successfully issued in the first quarter of 2021, equivalent to more than 120% of the total issuance volume for the entire year of 2020. Influenced by a new regulation introduced by the U.S. Securities and Exchange Commission (SEC) in mid-April that strengthened risk control over the accounting treatment of public warrants in SPACs, SPAC issuances across the United States cooled down abruptly. Only slightly more than 10 SPACs were issued in April and May, respectively. Nevertheless, the market largely remained prosperous due to the nearly 300 SPACs accumulated from previous periods that were still under application or awaiting subscription.

Today’s SPACs are no longer merely the “shells” originally designed to facilitate exit listings for underperforming targets. With an influx of high-quality capital and deepening integration with industry sectors, SPACs themselves are undergoing significant transformation.

“Many of my friends on Wall Street have told me that the SPAC landscape is changing rapidly; this year’s SPAC transactions may be an entirely different beast compared to last year’s,” Bob Zhang, founder of a Chinese firm providing comprehensive financial services to SPAC sponsors, told VCBeat.

Bob was formerly a senior executive at a publicly listed company in China. For the majority of his career, he traveled between Wall Street in the United States and China, providing professional support to companies pursuing cross-border listings, which led to his early involvement with SPACs. However, it was not until 2019, when Bob observed the rapid surge of SPAC IPOs in the U.S. market and recognized the knowledge gap among Chinese investors, that he returned to China to establish a specialized SPAC services team. The day before his interview with VCBeat, Bob and his team had just completed SPAC advisory work for an investment firm in Shenzhen. Such engagements are becoming increasingly frequent, leaving Bob’s team struggling to keep up with the demand.

It was once predicted that by the end of 2021, every well-known private equity (PE) firm globally would have served as a sponsor for at least one special purpose acquisition company (SPAC). In Bob’s view, this prediction may well come true given current trends; however, the lack of professional teams and talent is becoming a bottleneck. “Very few individuals in China have hands-on experience spanning the entire process from SPAC initiation to merger and acquisition. Yet such expertise is crucial for first-time SPAC sponsors or potential target companies.”

To some extent, even among a handful of top-tier investment firms in China, SPACs remain a game for only a select few. Since 2021, leading institutions such as Qiao Capital, Hony Capital, Hillhouse Capital, and Primavera Capital have all begun to position themselves in the SPAC space. It is reported that Shenzhen Capital Group has also started researching SPAC strategies. Notably, Qiao Capital filed an S-1 registration statement with the U.S. Securities and Exchange Commission (SEC) in May for its SPAC, Summit Healthcare Acquisition, which went public the following month. The speed of SPAC IPOs is even significantly faster than private equity fundraising.

Despite a lackluster post-IPO performance, Summit Healthcare, as China’s first SPAC focused exclusively on biotechnology, already exhibits the mainstream structural characteristics of biotech SPACs in the U.S. market. Fu Wei, founder of QiaoYing Capital and known for his “ten entrepreneurial ventures,” serves as Honorary Chairman and Senior Advisor, while Tan Bo, former President and CFO of Sino Biopharmaceutical, holds the positions of Chief Executive Officer and Co-Chief Investment Officer. Their appointments respectively underscore the SPAC’s strong capabilities on both the capital and industry fronts.

Fu Wei founded Qianqiao Capital in 2014, focusing on private equity investment in the healthcare sector, with assets under management exceeding $2 billion. He facilitated the public listings of innovative pharmaceutical companies such as I-Mab Biopharma and Evergreen Therapeutics. Fu Wei previously held positions at Temasek Holdings, the Investment Division of Macquarie Bank, Standard Chartered Private Equity, and Goldman Sachs. During Tan Bo’s tenure at 3SBio, the company underwent privatization and subsequently listed on the Hong Kong Stock Exchange. He also led the acquisition and integration of notable targets including Saiboer, Wansheng Pharmaceutical, and CITIC Guojian Pharmaceutical.

In the evolving SPAC landscape, the integration of capital and industry is almost the most common characteristic of consecutive sponsoring teams.

SPAC investor Kevin told VCBeat that although SPACs are relatively novel, the technical complexity is not significant; many decision-making logics are consistent with traditional investment. The real challenge lies in integrating capital with industry. Since 2021, his investment firm has established a dedicated team for SPAC-related business. Composed of four investors with backgrounds in both investment and industry, this team is identifying investment opportunities across various stages, including SPAC IPOs, existing listed SPACs, and PIPE transactions. In Kevin’s view, domestic SPAC investment in China is still in its very early stages, and the broader environment remains imperfect. Nevertheless, genuine investment opportunities do exist within the pool of existing SPAC capital and rapidly growing new-economy projects in China.

Kevin told VCBeat that for most participants, SPACs are no longer merely shell vehicles used to facilitate the listing and exit of underperforming projects. With an increasing influx of high-quality capital, SPACs have also become attractive assets in their own right.

At its core, the SPAC boom since 2019 is closely tied to the persistent abundance of capital coupled with a relative scarcity of high-quality assets in the U.S. market. The influx of low-cost, long-term capital has enabled SPACs to exercise greater prudence in selecting truly promising targets for mergers and acquisitions.

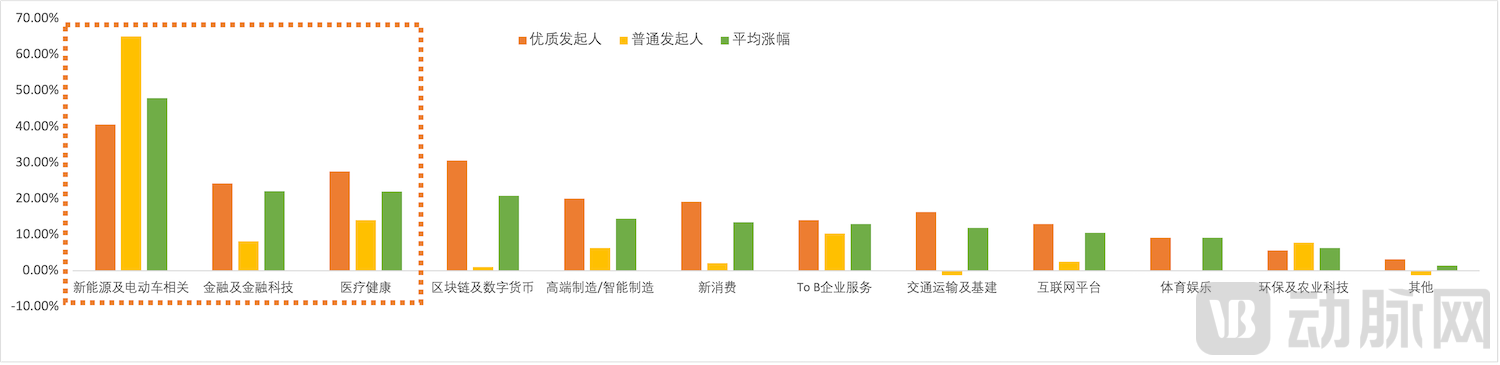

Kevin previously conducted a statistical analysis, which revealed that the capital market responded very positively to news of SPACs selecting merger targets, as evidenced by stock price movements before and after the announcement of such deals. “Since 2020, SPAC stocks have generally experienced a surge after finalizing merger targets. Among these, companies in the new energy, fintech, and healthcare sectors have seen the most significant stock price increases when chosen as merger targets.”

SPAC Stock Price Changes Following the Announcement of Merger Targets (Data Source: ANLAN CAPITAL and Public Data)

In fact, in the years following the completion of SPAC mergers, stock prices have generally maintained steady growth. This is particularly true for biotechnology SPACs that have continued to surge in the U.S. stock market. In the table below, VCBeat has compiled the latest market performance of ten biotechnology companies that went public through SPAC mergers since 2019. Among them, DermTech, a dermatological genomics company listed in August 2019, boasts the highest market capitalization and the largest stock price increase. It is also the earliest observable case of a biotechnology company going public via a SPAC. DermTech’s latest market capitalization is nearly $1.3 billion, representing a relatively high valuation level compared to unprofitable biotechnology companies that have gone public through traditional IPOs.

Selected Biotech SPAC Merger Targets and Latest Market Performance (Data Source: Compiled by VCBeat from Public Data)

In a sense, the influx of high-quality capital, coupled with recognition from the capital market, has enabled SPACs to develop traceable and stable strategies in the relatively mature U.S. stock market, giving rise to several influential SPAC brands. This trend is particularly evident in biotech SPACs. VCBeat’s further observation reveals that over the past two years, U.S. biotech SPACs have rapidly integrated into the capital and industrial ecosystems.

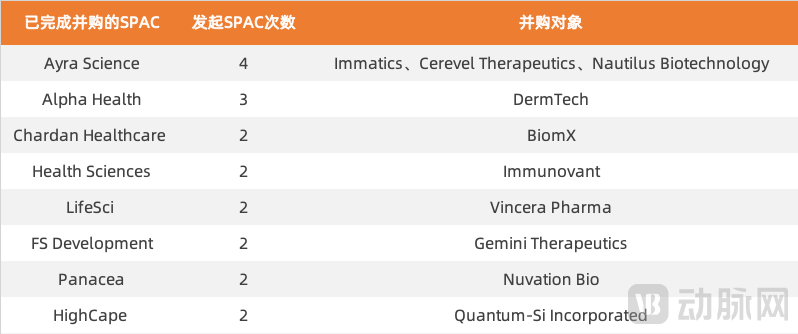

On one hand, all biotech SPAC sponsors that have completed mergers and acquisitions have launched multiple similar biotech SPACs in quick succession. For instance, the Ayra Science series has sequentially launched four biotech SPACs, with three successfully completing mergers; among the targets were companies with strong market performance, such as Cerevel Therapeutics and Nautilus Biotechnology. Meanwhile, Chardan Healthcare, Health Sciences, FS Development, and others swiftly initiated new rounds of SPAC fundraising after successfully completing the cycle from SPAC IPO to de-SPAC transaction.

Major Biotech SPACs and Issuance Overview (Source: VCBeat, compiled from public data)

Continuous capital operations have built strong credibility for SPAC sponsors, thereby driving up SPAC IPO pricing and shortening the merger and acquisition cycle.

A typical example is Indian investor Shukla, who previously worked at Pfizer. Since 2017, he has repeatedly invested in biotech SPACs. His SPAC debut was the acquisition of DermTech. Between 2001 and 2006, Shukla served as a Senior Director at Pfizer, where he assisted the company in completing multiple acquisitions, including those of Pharmacia, Meridica, Vicuron Pharmaceuticals, Idun Pharmaceuticals, and Rinat Neuroscience.

DermTech is a leading genomics company in the field of dermatology. It uses adhesive patches instead of scalpels to analyze non-invasively collected skin samples, enabling early detection of skin cancer, assessment of inflammatory diseases, and facilitation of personalized pharmacotherapy. Leveraging extensive experience in investing in and operating early-stage biotechnology ventures, Shukla keenly recognized DermTech’s potential and acted swiftly. Following its initial public offering, DermTech’s stock price grew steadily, with its market capitalization increasing nearly fivefold within two years.

Following DermTech’s public listing, Shukla issued SPACs at a pace of one per year on average. The Alpha series of biotech SPACs he established has already gained considerable influence among investors. After Shukla’s second SPAC confirmed its merger with Humacyte, the private placement round targeting private equity funds saw oversubscription, prompting Shukla to temporarily expand the offering size. Humacyte is a startup engaged in the research and development of vascular regenerative medicine products, having previously secured substantial investment and new product orders from Fresenius, a leading hemodialysis manufacturer. Another significance of this transaction lies in integrating top-tier medical device manufacturers like Fresenius into the biotech SPAC ecosystem.

Currently, Shukla is busy launching his third biotech venture, with plans to raise $150 million. Having raised nearly $400 million in the capital markets through biotech SPACs, Shukla’s single-round fundraising amounts continue to increase.

On the other hand, the boundaries among SPAC sponsors, investors, and even merger targets have become increasingly blurred, with their investment relationships becoming progressively intertwined. Some SPAC investors, having gained financial returns and operational experience from merger transactions, have stepped forward to sponsor their own SPACs. Meanwhile, some SPAC sponsors simultaneously participate in multiple biotechnology SPACs as PIPE or public investors.

In October 2019, BiomX, a microbiome company engaged in the development of natural and engineered phage therapies, went public through a merger with CHAC. One year later, the second biotech SPAC launched by CHAC’s sponsor team was approved for listing.

In addition to consecutively launching biotech SPACs, this team has also made significant investments in three other biotechnology SPACs, including ARYA Sciences Acquisition Corp, Health Sciences Acquisitions Corporation, and LifeSci Acquisition Corp, and served as an advisor for the merger transaction between Health Sciences Acquisitions Corporation and Immunovant Sciences.

As is well known, the development of many original new drugs in the U.S. market is a continuous relay process, wherein capital with differing objectives and teams with varying capabilities come and go, gradually transforming new drugs from conceptual technical pathways into commercialized products. Currently, some biotechnology companies are attempting to introduce SPACs (Special Purpose Acquisition Companies) into this relay game of new drug research and development.

Listed via a SPAC transaction in late 2019, Immunavant is cited as a typical example of a biotechnology company going public through this route. Focused on autoimmune diseases, Immunavant is a pre-profit, clinical-stage biopharmaceutical company with significant potential. It is developing IMVT-1401, a fully human anti-FcRn monoclonal antibody with the potential to treat IgG-mediated autoimmune diseases. According to Phase I clinical trial results, in healthy subjects receiving weekly injections for four weeks, IMVT-1401 reduced mean IgG levels by 63% at a dose of 340 mg and by 78% at a dose of 680 mg.

However, in late May, Roivant, the former parent company of Immunovant, announced that it would regain controlling interest in Immunovant. Interestingly, the funds Roivant plans to use for the acquisition also stem from a biotech SPAC sponsorship. In March 2021, Roivant announced its public listing via a SPAC transaction with Montes Archimedes Acquisition Corp. The deal valued the company at $7.3 billion, raised $611 million, and was expected to close in the third quarter.

The background of this acquisition is even more thought-provoking.

In February, Immunovant announced the voluntary suspension of clinical trials for its drug IMVT-1401 due to adverse effects observed in patients with thyroid eye disease and warm autoimmune hemolytic anemia, causing its stock price to plummet by more than 60%. Based on public data estimates, Roivant paid an acquisition premium for Immunovant as high as 70%. Roivant’s rationale to persuade investors was that, as Immunovant’s parent company, it possessed more detailed information on the pipeline under development than external parties, thereby enabling it to identify investment opportunities amidst uncertainty.

In fact, integrating innovative drug pipeline development with capital operations is the unique business strategy that has enabled Roivant to rapidly grow into an influential biotechnology company. Roivant acquires investigational pipelines from large pharmaceutical companies that have encountered development bottlenecks, refines certain strategies to transform them into new drug projects with clearer commercialization prospects, and then licenses or sells these assets to other biopharmaceutical enterprises. This relay-style approach accelerates the efficiency of new drug development.

For example, Roivant’s Dermavant conducted two successful Phase III clinical trials for tapinarof, an investigational topical treatment for psoriasis licensed from GlaxoSmithKline. In addition, Roivant’s Urovant licensed Gemtesa (vibegron), a treatment for overactive bladder, from Merck, and Myovant licensed Orgovyx (relugolix), a therapy for prostate cancer, from Takeda Pharmaceutical Company.

In December 2019, Roivant spun off five Vants—Myovant, Urovant, Enzyvant, Altavant, and Spirovant—to the Japanese pharmaceutical company Sumitomo Dainippon Pharma. The latter established a new subsidiary, Sumitovant Biopharma, to drive the commercialization of the development pipelines encompassed by these five Vants. Under this $3 billion deal, Sumitomo Dainippon Pharma acquired a 10% equity stake in Roivant and secured priority rights to purchase up to six additional Vants before the second half of 2024. Subsequently, Urovant and Myovant, both under Sumitovant Biopharma, received FDA approval for market launch, for the treatment of overactive bladder and prostate cancer, respectively.

Capital serves as an essential lubricant in the circulation of different Vants and new drug pipelines between Roivant and pharmaceutical companies. The distinction lies in the increasing maturity of biotech SPACs, which provides more abundant funding options for this relay-style business model, potentially accelerating the new drug development process.

On the night of July 11, videos of Virgin Galactic’s spaceflight flooded WeChat Moments. As the architect behind this quintessential SPAC case, Chamath Palihapitiya and his Social Capital have also been active in the biotech SPAC sector. Reportedly, Chamath has registered four biotech SPACs with the ticker symbols DNAA, DNAB, DNAC, and DNAD, designated respectively for investing in innovative projects in neurology, oncology, “organ space,” and immunology.

However, whether through continuous offerings or integrated operations, the SPAC model in the U.S. stock market is complex and dynamic, and its suitability for Chinese institutions remains to be carefully evaluated. Our aim here is not to argue that SPACs are already a sufficiently effective tool, but rather to offer a more rational analysis of SPACs from the perspective of integrating capital with industry.