Record-Breaking Fundraising and Surge in Mega-Deals: H1 2021 Global Healthcare Investment Report

Core Views

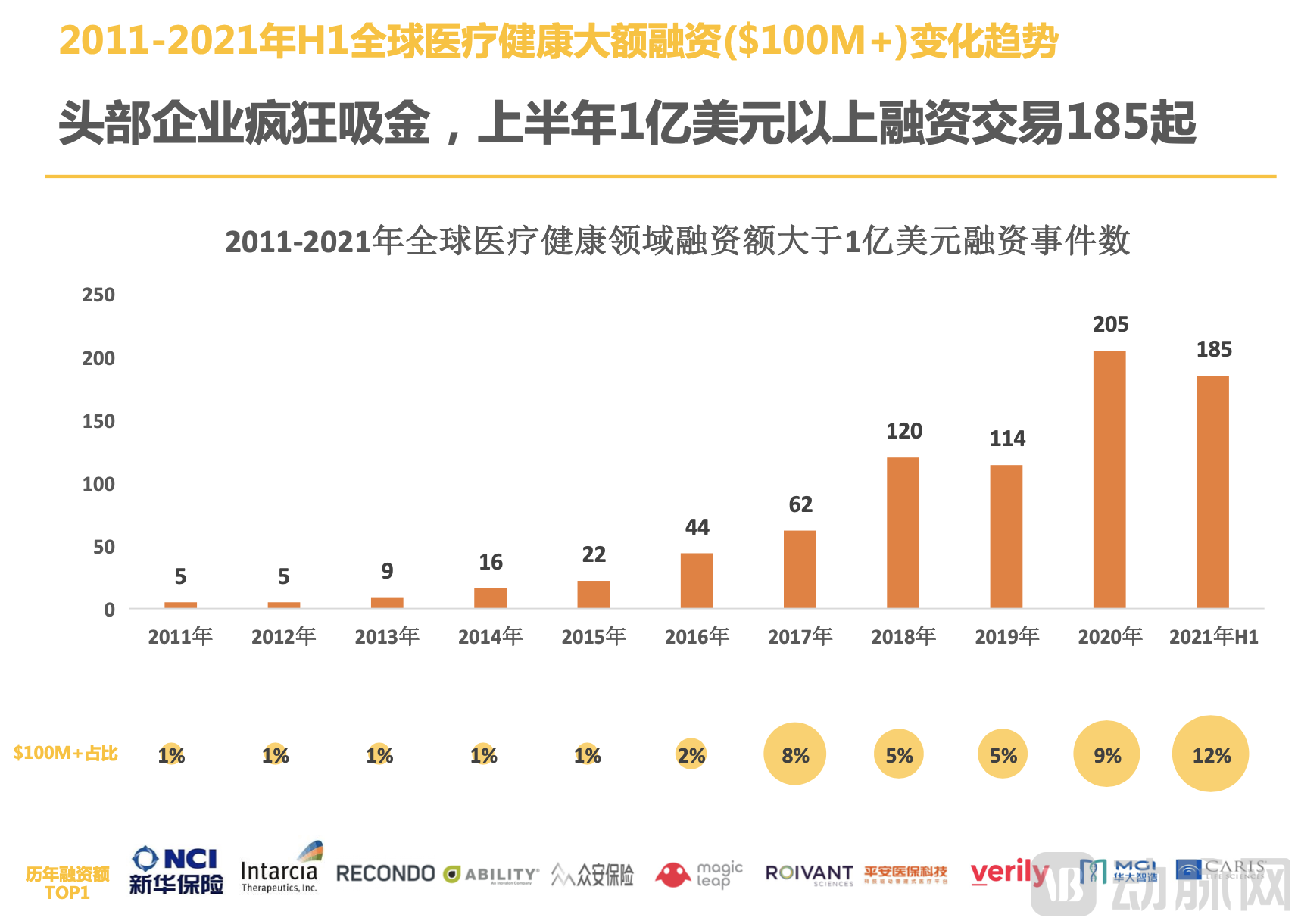

I. Financing in H1 2021 hit a record high, surpassing the total for all of 2019; leading companies attracted capital at an unprecedented pace, with 185 financing deals exceeding $100 million in the first half of the year.

II. In H1 2021, overseas healthcare financing doubled year-on-year, marking a remarkable growth rate; total domestic healthcare financing reached a record high for any first half of the year, with a 70% year-on-year increase.

III. Biopharmaceuticals ranked first in financing amount, consistently dominating the annual financing landscape. Its share of total financing has remained at 40% for years, exceeding the combined total of digital health and medical devices.

IV. Digital Health Becomes the Hottest Sector Abroad; Frequent Financing Rounds for Medical Devices and Consumables in China.

V. AI-driven drug discovery is gaining momentum, with H1 financing volumes already approaching last year’s full-year total; funding for medical robotics remains as robust as last year, and Chinese companies are accelerating their fundraising efforts.

VI. Among investment institutions, Hillhouse Capital set a new global record with 46 investments in the first half of the year, while top-tier firms maintained a high frequency of deal-making. Hillhouse’s domestic venture capital arms continued to exert strong momentum, with five entities each completing more than 20 investments over the six-month period. The investment frequency of active institutions is highly likely to witness another leapfrog increase in 2021.

VII. The three major stock markets welcomed 165 IPO projects, concentrated in the biopharmaceutical sector; China saw 48 healthcare companies go public in the first half of the year, hitting a new record high.

VIII.The United States leads globally, with China and the US together accounting for 81% of global financing; Shanghai remains firmly at the top, while Jiangsu, Zhejiang, and Shanghai collectively represent half of China’s total financing in the first half of the year.

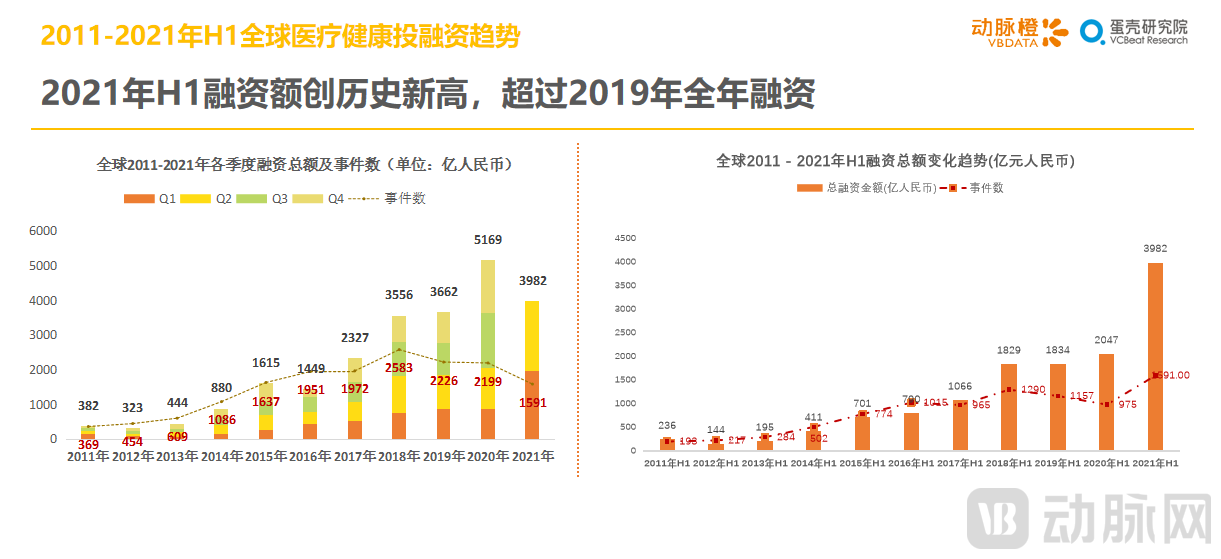

1.1 H1 2021 Financing Hits Record High, Surpassing Full-Year 2019 Total

In H1 2021, a total of 1,591 financing deals occurred in the global healthcare industry, with the total funding amount reaching a new high for any first half on record, even surpassing the full-year total of 2019. The amount reached $61.26 billion (approximately RMB 516.93 billion), representing a year-on-year increase of about 94%; the number of financing deals reached 1,591, a year-on-year increase of 63%.

Interestingly, when measuring the impact of the pandemic over a longer time horizon, the brief panic and market decline in early 2020 appear negligible. The long-term benefits initially predicted began to materialize within a shorter timeframe. More importantly, the COVID-19 pandemic has, in a sense, reshaped the development landscape of the life sciences industry. Institutional investors are drawn to the defensive nature of the life sciences sector while simultaneously pursuing the burgeoning fields of biotechnology and digital health, resulting in a continuous influx of capital.

1.2 Top Players Attract Massive Capital: 185 Financing Deals Exceeding $100 Million in the First Half of the Year

1.3 H1 2021 Overseas Healthcare Financing Doubles Year-on-Year, Showing Remarkable Growth

In line with global financing trends, the COVID-19 pandemic has accelerated responses to many unmet medical needs, driving increased investment in areas such as telemedicine, in vitro diagnostics, home care, and vaccine development. Coupled with the further intensification of global monetary easing, foreign venture capital has also significantly increased its investments in the healthcare industry.

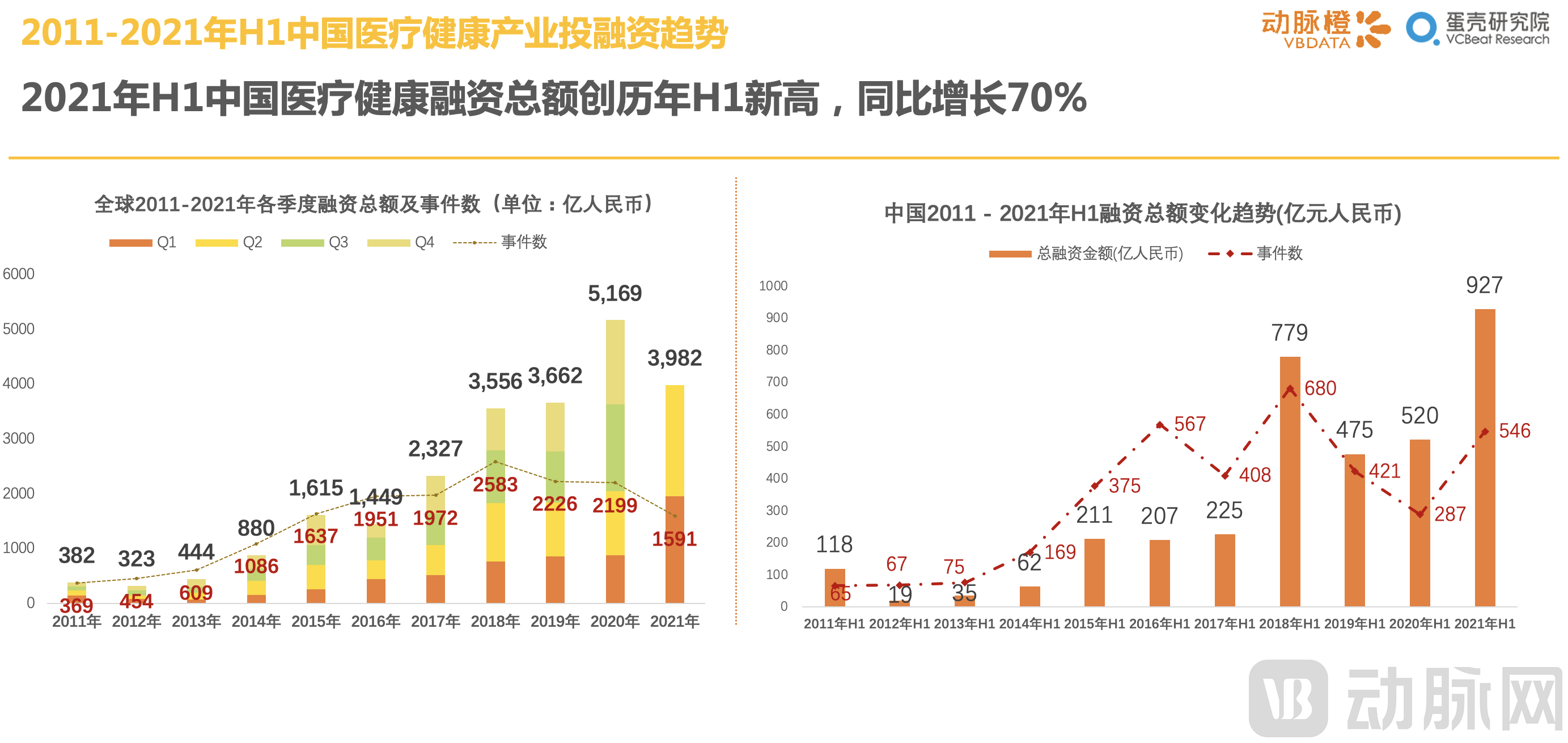

1.4 Total Healthcare Financing in China Reached a Record High for H1 in 2021, with a Year-on-Year Increase of 70%

In H1 2021, the total investment and financing in China's healthcare industry reached a record high of RMB 92.7 billion, a year-on-year increase of 70%;Similar to the situation abroad, the expansion in the year-on-year growth of financing is closely related to the tightening and subsequent rebound of capital during the pandemic.However, it is encouraging that the financing transactionThe number of deals also nearly doubled, reversing the trend observed over the past two years, where funding amounts increased while transaction volumes slowed or even declined.This signifies a shift in the financing landscape, which is becoming less skewed toward leading enterprises, potentially easing the funding challenges faced by small and medium-sized startups.

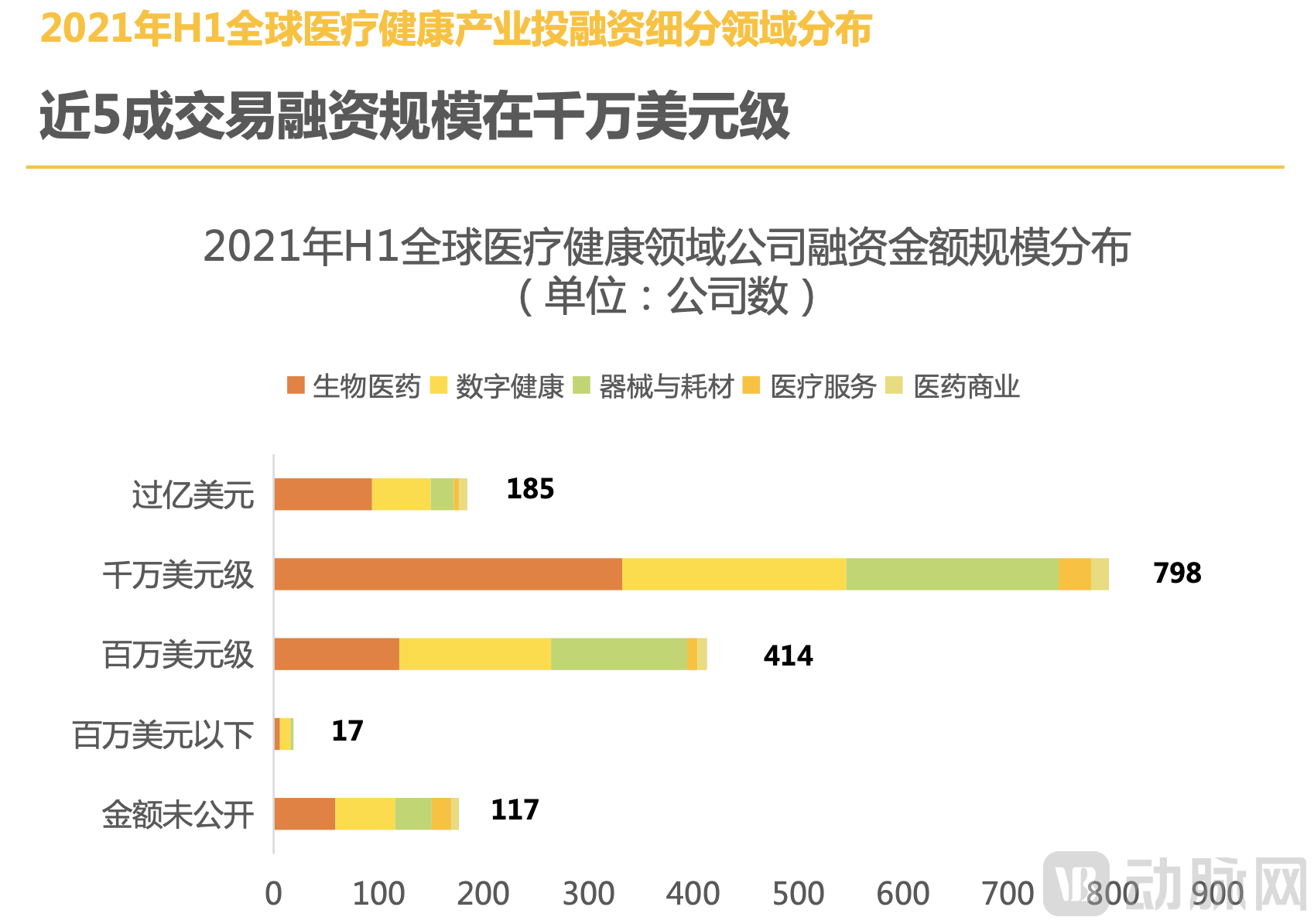

1.5 Nearly 50% of financing deals are valued in the tens of millions of US dollars.

In H1 2021, in addition to 185 financing deals exceeding $100 million, nearly 50% of companies secured funding at the tens-of-millions-of-dollars level.

II.Global Hot Sectors in Healthcare Investment and Financing in H1 2021

2.1 Biopharmaceutical Funding Tops the List, Surpassing the Combined Total of Digital Health and Medical Devices

2.2 Digital Health Becomes the Hottest Sector Abroad; Frequent Financing Rounds for Medical Devices and Consumables in China

In H1 2021, there were significant differences between domestic and international financing projects in specific sectors.

In China, the biopharmaceutical sector continues to lead in both transaction volume and financing amount. Internationally, digital health has sustained the momentum seen in 2020, with its number of financing deals slightly surpassing that of biopharmaceuticals.

Meanwhile, medical devices and consumables—sectors that have shown lackluster performance abroad—continue to attract strong investor interest in China. The rising prominence of domestic medical devices and consumables is driven by two main factors: first, the post-pandemic boom in the in vitro diagnostics (IVD) sector; and second, the growing momentum in innovative device segments such as cardiovascular, neurointerventional, and orthopedic devices following the implementation of volume-based procurement (VBP). In contrast to overseas markets dominated by industry giants, China offers substantial opportunities for import substitution and boasts a vast market potential for domestically produced devices. Furthermore, given their relatively lower risk and higher certainty compared to innovative drugs, medical devices have once again become a key target for capital allocation.

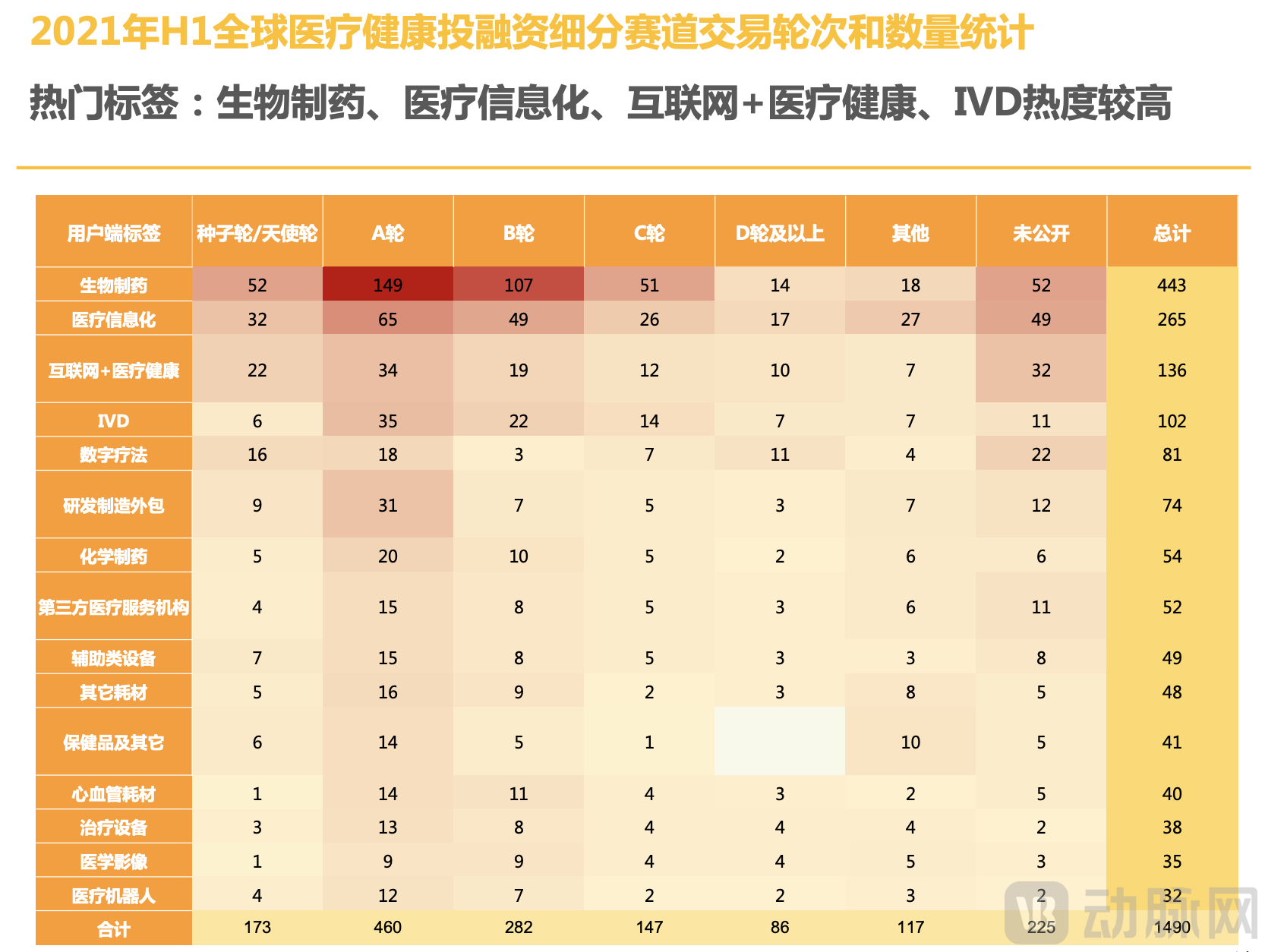

2.3 Trending Tags: Biopharmaceuticals, Healthcare Informatics, Internet+ Healthcare, High Interest in IVD

Note:The definitions of funding rounds on this page are extended; for example, Series A includes Pre-A, Series A, and Series A+.

In H1 2021, tags such as biopharmaceuticals, healthcare informatization, Internet+ healthcare, and IVD garnered high levels of interest.

In terms of funding round distribution, Series A financing events occurred most frequently, totaling 460; there were 173 seed/angel round deals, indicating that medical innovation continues to maintain a certain level of vitality.

From the perspective of specific sectors, early-stage financing projects at Series A and earlier are more concentrated in biopharmaceuticals, R&D and manufacturing outsourcing, medical robotics, and assistive devices; whereas "Internet + Healthcare" and healthcare informatization see more transactions in later funding rounds, with industry competition largely entering its second half.

2.4 AI+Drug Discovery Is Gaining Momentum: H1 Funding Nears Last Year’s Full-Year Total

In the global AI-driven drug discovery sector, 33 deals were completed in the first half of 2021, with total financing reaching $2.57 billion—nearly matching the full-year funding amount of 2020. Based on this trend, financing in 2021 is highly likely to hit a new record high.

Specifically, in the first half of 2021, AI+drug discovery transactions were dominated by foreign companies, with 21 deals raising a total of $2.083 billion, each exceeding $100 million; in contrast, both the number and scale of domestic transactions in China were significantly lower than those abroad.

2.5 Medical Robot Financing Remains Hot as Last Year, with Accelerated Funding Processes for Domestic Enterprises

Globally, the medical robotics sector witnessed 32 financing events in the first half of the year, with total funding amounting to approximately $1.7 billion. Among these, there were 10 transactions abroad and 22 in China.

In the first half of the year, the number of transactions in China’s medical robotics sector has already surpassed the 23 financing deals recorded for the entire previous year, with a total transaction value of RMB 3.6 billion. Edge Medical Robotics, Keya Robotics, and Fourier Intelligence, each of which completed two rounds of financing in 2020, have all secured new funding in the first half of this year. The scarcity of investment targets in this sector, combined with its vast future market potential, has accelerated the financing pace for domestic medical robotics companies, particularly those specializing in surgical robots.

III. Analysis of Active Healthcare Investment Institutions in H1 2021

3.1 Hillhouse’s 46 Investments Set a New Global H1 Record, with Top Firms Maintaining High-Frequency Deal Activity

In the first half of 2021, Hillhouse Group was the most active investor in global healthcare, making a record-breaking 46 investments in just six months, with its portfolio primarily focused on biopharmaceutical and medical device companies.

In the first half of 2021, most companies matched their full-year 2020 investment counts in just six months. This demonstrates that investment firms have sustained, and even intensified, the fervor for healthcare investments that emerged in 2020.

Hillhouse, Sequoia Capital China, Matrix Partners China, and Lilly Asia Ventures have entered the global top 10, underscoring the increasingly significant role of Chinese institutions in the global healthcare investment market.

3.2 Prediction: In 2021, the investment frequency of active institutions is highly likely to witness another leapfrog increase.

3.3 Hillhouse FlagVCBeat Continues to Exert Strong Momentum: Five Firms Make Over 20 Investments in Half a Year

In the first half of 2021, leading domestic investment firms, including Hillhouse Capital and Sequoia Capital China Fund, increased the frequency of their investments in Chinese healthcare companies.

Hillhouse Group Ranked First Among Domestic Institutions with 46 Investments in the First Half of the Year. Of these, Hillhouse Ventures made 35 investments, while Hillhouse Capital made 11. Since the establishment of Hillhouse Ventures in 2020, Hillhouse Group has significantly increased its focus on the primary market in the healthcare sector.

IV. Review of Healthcare IPOs Listed in H1 2021

4.1 Major Stock Markets Welcome 165 IPOs, Concentrated in the Biopharmaceutical Sector

In H1 2021, the three major stock markets—U.S. stocks, A-shares, and Hong Kong stocks—welcomed 165 newly listed companies, a year-on-year increase of 146%.

Among them, 122 companies listed on U.S. stock exchanges continue to hold an absolute lead across the three major stock markets, with 30 listed on the A-share market and 13 on the Hong Kong stock market.

Among the five major subsectors, biopharmaceutical IPOs led by a wide margin with 98 deals. The amount of capital raised also remained high; the medical devices and consumables sector followed closely with 41 transactions.

4.2 48 Healthcare Companies in China Went Public in the First Half of the Year, Setting a New Record

In the first half of 2021, a total of 48 healthcare companies in China listed on secondary markets. Among them, 30 were listed on the A-share market, followed by the Hong Kong stock market and the US stock market, with 12 and 6 companies respectively.

Compared with the 32 IPOs in China during the first half of 2020, healthcare companies have delivered a more impressive performance in the secondary market this year, with the number of IPOs reaching a new historical high for the first half of the year.

Last year, we judged that the surge in healthcare IPOs in China was a phased outbreak driven by multiple factors, including policy dividends from the STAR Market and the Hong Kong Stock Exchange, as well as the impetus of the pandemic. The sustained heat in the first half of 2021 may signal that the healthcare industry is transitioning from phased fervor to normalized, high-speed development.

V. Regional Distribution of Global Healthcare Investment and Financing Hotspots in H1 2021

5.1 The US Leads the World, with China and the US Together Accounting for 81% of Global Financing

In H1 2021, the five countries with the highest number of global healthcare and medical financing events wereThe United States, China, the United Kingdom, Germany, and Switzerland。

In H1 2021, the five countries with the highest number of global healthcare and medical financing events wereThe United States, China, the United Kingdom, Germany, and Switzerland。

H1 2021,The United States recorded 770 financing deals, raising $35.46 billion (RMB 230.417 billion).Leading globally, with China close behind; the United States and China together account for 81% of total financing across all countries and 83% of financing deals.

From a global geographic perspective, beyond China and the United States, Europe’s medical innovation sector is on the rise. In particular, healthcare financing activity in the UK has surged dramatically; in just the first half of the year, total funding in the UK already exceeded the approximately RMB 10 billion raised throughout all of 2020.

5.2 Shanghai Remains at the Top, with Jiangsu, Zhejiang, and Shanghai Accounting for Half of China’s H1 Financing

The five regions with the most concentrated healthcare investment and financing activities in China in 2021 were, in order:Shanghai, Beijing, Guangdong, Jiangsu, and Zhejiang。

The five major regions remain consistent with those in 2020,ShanghaiA total of 137 financing events occurred, raising up to RMB 24.766 billion,Nearly RMB 5 billion ahead of Beijing, which ranks second.Thus, the data showing that Shanghai surpassed Beijing in 2020 to become the leading province/municipality for healthcare venture capital investment is by no means coincidental.

The Jiangsu-Zhejiang-Shanghai region has emerged as a cornerstone of healthcare innovation, accounting for half of all H1 healthcare industry financing deals with 283 transactions. Beyond macroeconomic factors, the rise of this region is largely attributable to the support of medical innovation industrial parks, exemplified by Zhangjiang Pharma Valley.

5.3 California Remains Dominant, with Massachusetts and New York Emerging as Secondary Hubs

In H1 2021, California, USA, recorded a cumulative total of 239 financing deals, raising $12.7 billion (approximately RMB 82.744 billion), making it the most active region globally for healthcare venture capital investment transactions.

Leveraging its renowned biotechnology industry cluster and abundant medical resources, Massachusetts has surpassed the more economically developed New York to become the second-largest U.S. state for healthcare investment and financing, although its scale still lags far behind that of California.

VI. Top Financing Deals for Healthcare Companies in H1 2021

6.1 Precision Medicine: Caris Life Sciences Leads Globally with $830 Million Funding Round; Two Chinese Internet Healthcare Companies Make the List

6.2 Yuanxin Technology Tops H1 Domestic Financing Rankings; Internet Healthcare and Pharmaceutical E-commerce Companies Dominate