Oral Healthcare Sector Surges with Over $7 Billion Raised in First Half of 2026 as Sequoia, China Renaissance, Matrix Partners, and ByteDance Enter the Fray

The dental care sector sets a new historical record.

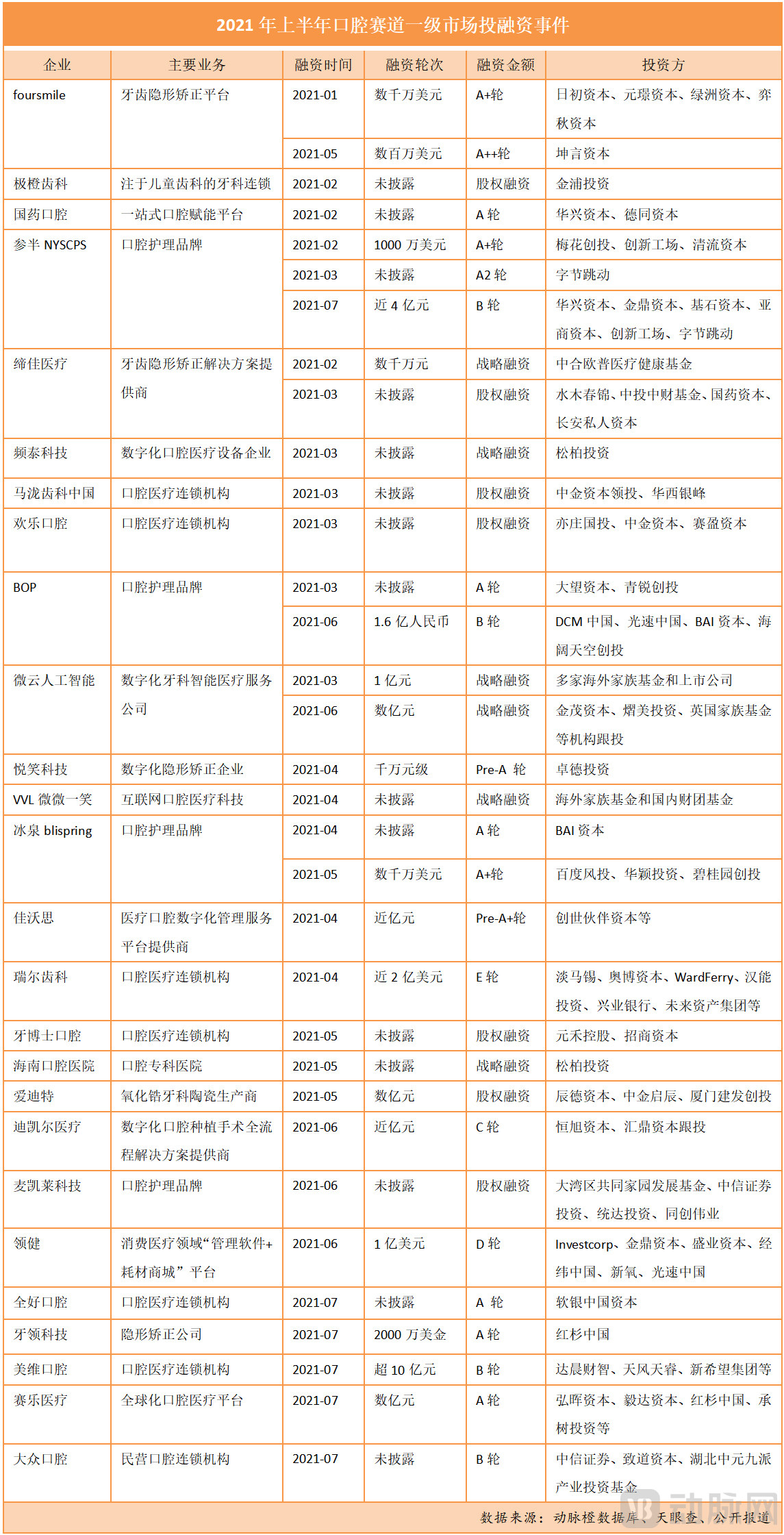

In the first half of this year, the dental healthcare sector demonstrated exceptional capital-attracting prowess, with both the frequency and volume of financing rising steadily. Statistics from VCBeat reveal that,In the first half of this year, a total of 33 financing deals occurred in the primary dental market, with the total amount exceeding RMB 5 billion, reaching an all-time high.(The total financing amount for the full year of 2018 was RMB 3.913 billion, ranking second.) Among these, there were three large-scale financing rounds exceeding USD 100 million, and six companies secured two or more rounds of financing within half a year.

(Data source: Qichacha, Arterial Orange Database; graphic by VCBeat)

In the secondary market, Angelalign (06699.HK), a provider of clear aligner orthodontic solutions, listed on the Hong Kong Stock Exchange, triggering frenzied buying by investors. Its shares surged 132% on the first day of trading, pushing its market capitalization to over HK$70 billion. Meanwhile, other players in the dental care sector, including Henglun Medical, Arrail Dental, and China Oral Health Care Group, have also filed their prospectuses.

Notably, investment firms such as Sequoia China, China Renaissance, and Matrix Partners China have all increased their investments., indicating continued optimism about this sector.Taking Sequoia China as an example, it participated this year in a $20 million financing round for Shenzhen Yaling Technology, a clear aligner company, and in a multi-hundred-million-yuan financing round for Saile Medical, an oral healthcare platform company. Last year, Sequoia China also served as the lead investor in a multi-hundred-million-yuan financing round for Fissen Technology, a provider of comprehensive digital dentistry solutions.

Not only that,ByteDance, an internet giant, is also actively expanding into the dental care sector.In ByteDance’s recently launched offline clinic, “Xiaohe Clinic,” consumer dental services such as professional teeth cleaning have become a key business segment. Additionally, ByteDance invested twice this year in Canban, an oral care brand.

Capital and industry giants are vying for position, driving a surge in interest in the dental care sector. A significant influx of capital is expected to flow into this field in the second half of the year, undoubtedly providing a major boost to its development.

Does the current surge in popularity signal that the oral care sector is on the verge of an explosion? What new trends and changes are emerging? To address these questions, VCBeat has analyzed the industry’s current landscape across the upstream, midstream, and downstream segments, and conducted interviews with senior industry practitioners and investors to gain insights into the answers.

The upstream dental sector continued to maintain the high level of interest seen in previous years, with companies focused on digitalization accounting for over 90% of financing deals.

This is because the dental industry remains largely traditional overall, with low digital penetration across equipment, consumables, and management processes. Therefore, digital transformation aimed primarily at improving diagnostic and treatment efficiency has consistently been a key focus for the industry.

In terms of subcategories,“Invisible Orthodontics” and “Fast-Moving Consumer Brands” Became High-Frequency Terms in First-Half Financing.Given the differing investment logics and trends between the orthodontics sector and fast-moving consumer goods (FMCG) brands, each will be discussed separately.

Invisible Orthodontics: Digitalization Accelerates Industry Transformation, Leading Companies “Make Money Hand Over Fist”

Orthodontic treatment primarily involves two approaches: traditional metal brackets and clear aligner therapy.

In traditional approaches, metal bracket orthodontics is inexpensive; however, its drawbacks—such as compromised aesthetics and the risk of enamel wear due to metal abrasion—have created room for clear aligner therapy to serve as an alternative. On the other hand,Empowered by digital technology, clear aligner therapy enables clinicians to create 3D models of each patient’s dentition, rapidly and accurately capturing precise oral data, thereby delivering a superior orthodontic treatment experience.Against this backdrop, the market for clear aligner orthodontics has experienced rapid growth.

According to the Frost & Sullivan report, in terms of retail sales revenue,The global clear aligner orthodontics market grew from $4 billion in 2015 to $13.1 billion in 2019, representing a compound annual growth rate (CAGR) of 35%.The development of the clear aligner market in developing countries, primarily China, is the main driver of global market growth: In 2019, China’s clear aligner market became the second largest in the world.

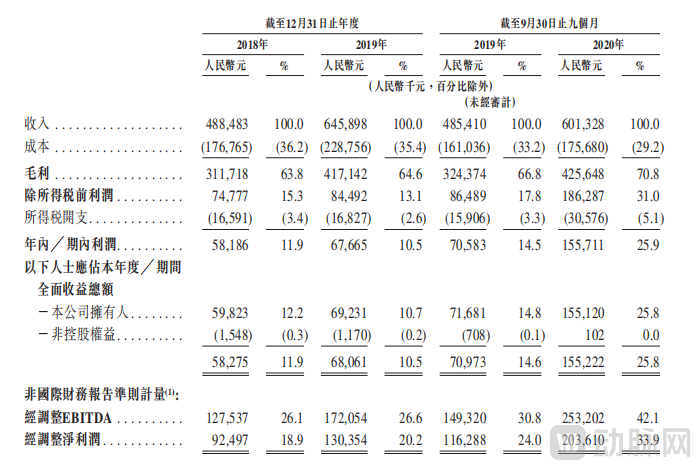

What capital and enterprises value even more is the exceptionally high gross profit margin of invisible orthodontic products.: Driven by high technological barriers and a continuously expanding market, the industry exhibits a high degree of concentration, allowing leading clear aligner companies to reap substantial profits with minimal effort. According to the prospectus of Angelalign, China’s first publicly listed clear aligner company, its gross profit exceeded RMB 400 million in the first nine months of 2020.The gross profit margin was 70.8%.

(Angelalign's financial data, source: prospectus)

(Angelalign's financial data, source: prospectus)

High entry barriers and healthy profit margins have made companies in the clear aligner orthodontics sector increasingly attractive to investors. Notably, in the first half of this year alone, several such companies—including Yaling Technology, Yuexiao Technology, Dijia Medical, and foursmile—secured financing, with individual funding rounds typically approaching RMB 100 million.

Of course, in this field, deep technological innovation is key to entrepreneurship. Taking Yaling Technology as an example, its competitive advantage lies in the independent development of core technologies such as the “Root and Bone Analysis System” and “Intraoperative Deviation Correction,” which have differentiated it from other brands. As a result, within less than two years, its brand “Shimeile” has entered numerous large chain clinics across China.

Certainly, as clear aligner therapy is an interdisciplinary field encompassing five major technological domains—orthodontics, computer science, materials science, modern intelligent manufacturing technology, and biomechanics—it requires seamless integration of technology and clinical practice. Therefore,The overall technical requirements and the difficulty of commercial implementation are significant.Currently, the market is largely dominated by Invisalign, a brand under Align Technology of the United States, with Angelalign following closely behind; other companies hold only small market shares.

Additionally,The sustained penetration of invisible orthodontics heavily relies on talent skilled in the integration of medicine and engineering, yet such physicians are relatively scarce.As the industry leader, Align Technology (Invisalign) places significant emphasis on investment in physician promotion. Its 2019 financial report revealed that sales and general administrative expenses exceeded 43%, covering activities such as physician marketing, training, and patient acquisition support for doctors.

However, as more players enter the clear aligner orthodontics market, industry competition is becoming increasingly fierce. In this process, only companies with significant technological barriers in their products and room for downward pricing adjustment can carve out a path to success.

FMCG Brands: Targeting the New Generation of Young Consumers, Oral Care Products Enter a Period of Explosive Growth

The oral care new-consumption brands have attracted significant attention in the first half of this year. Companies that secured financing include NYSCPS (Canban), Blispring, Maikailai Technology, and BOP. Among them, NYSCPS completed three rounds of financing, with its latest round raising nearly RMB 400 million.

The reason behind the fervor lies in,The rise of the new generation of young consumers, represented by those born in the 1990s and 2000s, has provided ample room for imagination in the development of new consumer brands.“Gen Z (those born between 1995 and 2009) is gradually becoming the key decision-maker in purchasing oral care products. Their upgraded demands for aesthetics and health, their discerning taste preferences, and their choices of media and channels differ significantly from those of the previous generation. Understanding their current choices and shaping their brand perceptions will influence their brand preferences for the next 20 to 30 years,” China Renaissance told VCBeat.

“Specifically, changes in the category structure reveal thatOral care is shifting from simple morning and evening brushing to meeting diverse needs., and as a result, demand for and acceptance of categories such as mouthwash, dental floss, and teeth-whitening strips are rising rapidly。"A migration path for category structure (i.e., from the current situation in the domestic market where toothpaste and toothbrushes account for over 90% to the U.S. market where they account for 64%) has gradually become clear."

Taking BOP as an example, its product line covers categories such as mouthwash, oral sprays, and teeth whitening strips, while NYSCPS’s products also include mouthwash, toothpaste, oral sprays, teeth whitening strips, water flossers, and more. This indicates that,New oral care consumer brands need comprehensive oral health solutions across various scenarios to reach a broader audience and increase user engagement frequency and brand loyalty.。

From this perspective,Essentially, new consumer brands in the oral care sector represent a business model driven by innovation, with core strategic layouts in marketing and distribution channels.For instance, Canban has adopted a unique marketing strategy: it first generates high-quality content to conduct multi-angle, repetitive promotion, reinforcing the selling points of its alcohol-free formula and milder taste for Canban Probiotic Mouthwash. Meanwhile, it engages numerous celebrities and key opinion leaders (KOLs) across various channels for continuous marketing, thereby rapidly reaching a broader user base. After achieving sufficient online exposure, Canban quickly expands its offline presence through omni-channel and full-scenario distribution networks, leveraging its online influence to achieve rapid nationwide coverage in China.

For instance, in terms of sales channels, BOP’s strategy primarily focuses on omni-channel online platforms, enhancing user reach through high-frequency, mid-ticket products. According to its official website, BOP positions itself in the mid-range market, with mouthwash and oral spray products priced between RMB 30 and 40. Currently, nearly 80% of its sales volume comes from online channels. Following its online expansion, BOP is also accelerating its offline presence by entering beauty collection stores, cosmetics shops, convenience stores, and traditional supermarkets, thereby establishing a closed-loop omnichannel sales system integrating both online and offline operations.

By examining the characteristics and strategies of emerging consumer brands in the oral care sector, one can discern the rationale behind ByteDance’s bet on this field:Leveraging its massive user base and traffic, ByteDance enjoys distinct channel and marketing advantages. By strategically investing in a series of new consumer projects primarily targeting young audiences, it can establish effective synergies with emerging consumer brands.

“Unlike the beauty sector, the daily chemical industry typically exhibits a high degree of market concentration. Developed markets such as the United States and Japan have already validated this consolidated landscape in oral care, with the CR2 (the combined market share of the top two companies) reaching 50%. We believe that leading Chinese brands can similarly capture larger market shares and sustain longer-term brand advantages,” stated China Renaissance.

However, the rise and fall of some previous new consumer brands have also shown that companies cannot rely solely on marketing and distribution channels. Doing so may lead to a situation where, after extensive market expansion, poor overall product reputation renders all prior investments of capital and time futile. Therefore,Oral care’s new consumer brands must still adhere to a “long-term development mindset” and establish an integrated closed-loop efficiency across products, branding, channels, and supply chains in order to go further.

The midstream segment of the dental industry can be broadly categorized into two types of players. One type consists of enablers represented by traditional large-scale distributors, such as Sinopharm Dental and Shuangbai Investment. The other type comprises new-generation service providers, including Linker, Fussen Technology, Qiezi Dental Cloud, and Jaworsky. In the first half of the year, both types of players secured financing.

Despite the differences in business models,The core focus of both types of players is to empower and serve dental clinics and dentists. Therefore, their business logic lies in helping enterprises improve management and operational efficiency, as well as strengthening the output of corporate culture and service capabilities.

“The industrial structure of the oral care market is characterized by long-term, persistent fragmentation in both upstream and downstream ecosystems, which highlights the value of midstream integration and has the potential to give rise to major companies in vertical sectors,” stated China Renaissance.The Correct Approach to Midstream Integration: Expanding Scale While Driving Efficiency Gains and Service Innovation to Deliver Comprehensive Empowerment Solutions

Specifically, Sinopharm Dental, which just secured its Series A financing this year, has integrated national channel resources in the dental industry—namely midstream distributors—since its inception. By linking upstream and downstream partners, it provides private dental clinics and medical staff with supply chain finance, insurance, education, SaaS, and other services, thereby facilitating business growth.

“We believe that the future business model in the oral care sector will undoubtedly revolve around providing multi-dimensional, comprehensive services to private clinics and professional dentists. Therefore, we have consistently engaged at the grassroots level to gain a deeper understanding of dentists’ needs, thereby optimizing and launching more products and services that align with market demands,” Lu Sang, Director and General Manager of Sinopharm Oral Care, told VCBeat.

Taking as an example the first dental whitening medical insurance product launched in June by “Aichi Yi,” a brand under Sinopharm Stomatology, the initiative customizes dental services for high-quality dental clinics across China, provides oral health consultations through authoritative teams from public hospitals, integrates clinic settlement systems, implements a standardized specialized customer service team, and offers technical platform services for dental insurance products, thereby constructing a closed loop of “consumers + clinics + services + insurance payment.”

In contrast, LinkCare and Jawoos adopt different strategies. Having secured two rounds of financing within six months, LinkCare has been continuously strengthening its capabilities in both software services and industrial supply chains. Specifically, LinkCare’s solutions encompass single-store and chain management, customer relationship management (CRM), outpatient management, inpatient management, electronic medical records (EMR), inventory and sales management, financial management, insurance payment processing, Picture Archiving and Communication Systems (PACS), Youke SCRM for intelligent marketing, and Youshu business intelligence analytics, thereby fully meeting the operational and managerial needs of clinics. To date, LinkCare has provided SaaS management software to more than 30,000 dental and medical aesthetic institutions, 80% of which are mid-to-high-end dental chain organizations.

In terms of supply chain, Lingjian Mall currently connects with over 300 upstream top-tier brands and offers more than 10,000 SKUs. By integrating the mall with the SaaS system’s inventory management (procurement, sales, and stock), it provides expiration date and batch management functions at key nodes of procurement and consumables/equipment management, helping clinics reduce procurement costs, improve efficiency, and minimize losses.

Looking at Jiawosi, which secured financing in April, it positions itself as an e-commerce platform for dental medical products. It provides procurement and supply chain management systems, e-commerce services, and a training and social networking platform for chain and independent dental clinics as well as suppliers of instruments and consumables. Its product portfolio covers categories such as orthodontics, endodontic (root canal) therapy, direct and indirect restorations, office supplies, extraoral consumables, and equipment/instruments. By doing so, it integrates the ecosystem linking clinics, dentists, and suppliers, thereby empowering operational improvements for standalone dental practices.

“There is a growing trend of integrating online and offline channels, with the core objective of enhancing empowerment capabilities.“Lu Sang, Director and General Manager of Sinopharm Dental, stated, ‘As the business model gradually proves viable, more companies are expected to emerge. Drawing on overseas experience, it is highly likely that two to three leading enterprises will dominate the midstream dental sector over a period of 10 to 15 years.’”

In summary,Although the two types of players follow different paths, their ultimate goal is the same: to help dentists better launch and grow their practices.Therefore, as more players enter the market, the future competition in the oral care sector will hinge on companies’ comprehensive ability to enhance the overall operational efficiency of dental institutions.

Dental Chain Clinics Are Undoubtedly the Top Recipients of Industry Financing in the First Half of This Year, Arrail Dental’s nearly $200 million Series E financing and Meiwei Dental’s financing exceeding RMB 1 billion both rank among the top deals in the dental industry in recent years. Meanwhile, although Malo Clinic China and Happy Dentistry did not disclose their financing amounts,The collective fundraising by leading industry players demonstrates the rapid heating up of the downstream dental sector.

It is worth noting that in recent years, capital markets paid little attention to downstream dental chain institutions. This was partly due to a lack of high-quality investment targets in the market, and partly because the challenge of achieving scalability in the dental chain industry remained unresolved.

Taking Arrail Dental, which is applying for an IPO, as an example, the prospectus shows that its operating revenues for the fiscal years 2019 to 2021 were RMB 1.08 billion, RMB 1.1 billion, and RMB 1.515 billion, respectively,Revenue continues to grow, but losses are also increasing.The losses over the three years were RMB 304 million, RMB 326 million, and RMB 598 million, respectively, totaling RMB 1.228 billion.

Upon reviewing the breakdown of operating costs, it was found that employee benefit expenses for fiscal year 2021 amounted to RMB 585 million, accounting for 50.9%. This indicates that, aside from other factors, the chain operation of dental medical services is highly dependent on talent. It is no easy task to continuously expand the number of clinics while controlling operating costs and achieving stable profitability.

In its prospectus, Arrail Group also stated that future success hinges on the ability to retain, attract, and motivate a sufficient number of qualified and experienced dentists, who are critical to supporting the expanding dental care network and delivering superior dental services and patient experiences.

Although it is difficult to address this issue,The industry-wide consensus is:Enhance workforce efficiency and reduce operational costs through digitalization, while implementing a series of initiatives to engage dentists and retain talent.

Following the completion of its Series E financing, Arrail Dental stated that in addition to continuing to open new clinics, the funds would be allocated to two other key areas: enhancing the digital capabilities of its clinics and strengthening talent reserves and development, including the establishment of training bases and systems.

Meiwei Dental, which recently secured over RMB 1 billion in financing, aggregates dental entrepreneurs and medical institutions through its distinctive “DSO” model., and continue to provide these institutions with comprehensive empowerment spanning strategic investment, standardization, medical technology enhancement, brand management, and digital transformation, thereby helping them achieve rapid, personalized development.

As of now, Meiwei Dental has established nearly 200 dental clinics and hospitals across core urban clusters in China, along with a high-quality network of business partners. Moreover, its operating cash flow and profits have remained positive over the past two years, demonstrating that Meiwei’s distinctive “DSO” model has been successfully validated and has gained significant market recognition.

Under Meiwei Dental’s business partner mechanism, dentist-owners become the managers of new clinics. Empowered by Meiwei’s distinctive “DSO” model, this approach not only helps dental healthcare institutions resolve operational challenges but also supports their expansion and strengthening, enabling them to emerge as regional leaders.

It is not difficult to observe that dental institutions are addressing the challenges of dentist talent shortages and informationalization levels, which will be key factors determining the future growth potential of dental chains.Therefore, dental clinic chains still have a long way to go in these two areas.

The dental care sector has seen exceptional momentum in the first half of this year, with robust financing secured across upstream, midstream, and downstream segments, signaling that the industry has entered a phase of accelerated growth.

During this window period, China Renaissance believes that the continuously fragmented market structure upstream, ongoing product innovation, and the improvement of domestic technology and manufacturing capabilities have provided significant opportunities for new brands, especially Chinese-made brands—A core investment thesis for the future is domestic substitution.Under the theme of domestic substitution,The criteria for target selection are as follows: first, incremental market opportunities driven by high-speed growth; second, foreign brands currently still hold the majority of the market share., while in areas where domestic technologies are adequate and offer outstanding cost-performance ratios—typical examples being dental implants and CBCT. In the orthodontics sector, the upstream market landscape dominated by Invisalign and Angelalign is difficult to disrupt easily; therefore, attention should be paid to differentiated brands that compete through business model innovation and online-offline integration.

Revisiting the oral cavity segment,Integration has become an irreversible major trend, and the leading enterprises that entered the market early undoubtedly possess a first-mover advantage., after all, high-quality distributors and dental clinics (hospitals) in each region are limited, representing non-replicable scarce resources with a certain degree of exclusivity. In addition, SaaS-focused companies are also racing against time, because for B2B businesses, especially those involving informatization, the key lies in data accumulation and in-depth understanding of the industry.

Finally, looking at the downstream segment of the dental industry, more players are expected to enter the market in the future, while industry-wide consolidation will also accelerate. As a result, the number of medium-to-large chain institutions will continue to grow in the short to medium term, whereas small and fragmented dental clinics will either be acquired or go out of business due to weak profitability. However,To establish a mega dental chain with thousands of clinics and nationwide coverage, leading enterprises must continue to strengthen their capabilities in digitalization and talent attraction.

As capital poured in frenziedly, the dental care sector undoubtedly experienced an explosion in 2021, and this trend is set to continue in the second half of the year. ButIt is important to recognize that a surge in capital investment does not necessarily indicate industry maturity. Therefore, companies must continuously iterate their business models and accumulate technical capabilities in response to changing market conditions, while continuing to prioritize the quality of medical services, in order to achieve stable and long-term growth.