Post-Merger-Failure Strategic Outlook: How China's Medical IT Sector Can Prepare Amid Ongoing Consolidation Trends

On July 19, 2021, Winning Health and B-Soft, the leading enterprises in healthcare informatization, issued announcements declaring their merger. The merger was extremely sudden, with no prior indications; rumors only emerged after the Shenzhen Stock Exchange announced the temporary trading suspension of both companies’ stocks that morning. The shock this caused to the entire industry, which was completely unprepared, is imaginable.

Screenshot from Winning Health's announcement

Just as the industry was actively discussing and analyzing the situation in an attempt to identify the trajectory of future market development and formulate response strategies, the situation took a dramatic turn: on the evening of July 23, both parties issued another joint announcement, declaring the termination of the merger.

At this point, only four days had passed since the merger was announced, and the dramatic changes within just a few days were nothing short of astonishing.

What were the reasons behind this merger, why did it ultimately fail, and what subsequent impact will it have on the healthcare informatization market? VCBeat (WeChat ID: VCbeat) has analyzed these issues and attempted to answer these questions.

On the afternoon of July 19, Winning Health Technology Group Co., Ltd. and B-Soft Co., Ltd. separately released their “Announcement on Trading Suspension for Planning Major Asset Restructuring,” which indicated that the two parties had only signed a “Letter of Intent for Merger” and had not yet formulated a specific transaction plan, such as the transaction price, share exchange mechanism, or arrangements for board seats in the post-merger entity. Meanwhile, the risk disclosures explicitly stated that the merger is still in the preparatory stage and remains subject to approval by regulatory authorities.

According to publicly disclosed financial reports, companies with healthcare IT revenues exceeding RMB 1.5 billion include Winning Health and Donghua Software. Companies with healthcare IT business revenues between RMB 1 billion and RMB 1.5 billion include Wonders Information, Neusoft Group, and B-Soft. These five companies rank as the top five players in China’s healthcare IT market.

Specifically, Winning Health reported full-year 2020 revenue of RMB 2.267 billion, while B-Soft recorded RMB 1.633 billion. Following their merger, the combined entity would achieve annual operating revenue of nearly RMB 4 billion, equivalent to the total of the other three competitors. According to IDC data, the new company’s market share would reach approximately 19%, firmly establishing it as an undisputed industry giant.

Thus, the industry was shaken upon its official announcement.

Such a significant change was only revealed on the morning of the day the announcement was released, demonstrating that both parties maintained exceptionally effective confidentiality measures. The announcement terminating the cooperation also stated that, during the period of major asset restructuring, the company “strictly adhered to relevant regulatory requirements, implemented robust confidentiality protocols, tightly controlled the scope of insiders with access to inside information, registered and reported all individuals privy to inside information related to this transaction, prepared a memorandum documenting the progress of the major asset restructuring, and executed confidentiality agreements with the relevant intermediary institutions.”

Furthermore, according to insiders, the collaboration between the two parties was also, to some extent, a spontaneous decision.

In fact, mergers between listed companies mostly occur among state-owned enterprises; mergers between private enterprises face multiple challenges, are subject to stringent legal and compliance requirements, and entail significant integration difficulties.

So, why was the merger terminated?

Both Winning Health Technology Group Co., Ltd.’s “Announcement on Termination of the Planning of Major Asset Restructuring and Resumption of Trading of the Company’s Securities” and B-Soft Co., Ltd.’s “Announcement on Termination of the Planning of Major Asset Restructuring and Resumption of Trading of Shares” stated that the reason for the termination of the merger was “the inability of both parties to reach an agreement on core terms.”

Pursuant to the “Letter of Intent for Merger” jointly executed by both parties, it was agreed to jointly advance the proposed share-swap merger whereby Winning Health Technology Group Co., Ltd. would issue A-shares to all shareholders of B-Soft Co., Ltd. to effect a merger with B-Soft. Under conventional interpretation, this means that Winning Health will merge with B-Soft and serve as the surviving entity of the combined company.

However, this will result in a change of the actual controller of B-Soft and lead to its delisting, with trading suspended for integration into Winning Health, representing a significant transformation.

Meanwhile, in historical merger cases, the acquiring party typically holds greater bargaining power and retains its brand as the primary entity. Even if the brands owned by the acquired company enjoy significant renown, they are gradually replaced by the acquirer’s brand. Such instances have occurred repeatedly throughout history and are far from rare.

In 2005, Seagate, then the top-ranked company in the hard disk drive industry, acquired Maxtor, which was ranked third at the time. Maxtor’s One Touch brand had long been a dominant leader in the external and portable hard drive market. However, following the acquisition, this well-known brand was gradually marginalized, transitioning from a “dual-brand strategy” to increasing positioning in the low-end segment, before being completely phased out.

From the perspective of founders who regard their enterprises and brands as their own, this change is indeed difficult to accept. This is particularly true given the significant overlap in their business domains. Not only do both companies focus primarily on Hospital Information Systems (HIS), big data center construction, interoperability ratings, electronic medical record (EMR) ratings, smart hospital development, and internet hospital construction, but they also share a heavy reliance on customers in East China. Once merged, the overlapping brands and teams will inevitably undergo restructuring.

In fact, a merger that drew global attention as early as 2006 bore striking similarities to the current case. In 2006, ASUS, the world’s largest motherboard brand, joined forces with GIGABYTE, the second-largest motherboard brand globally. Given that motherboards are essential core components of computers and that the two brands collectively held a 45% share of the global motherboard market, the announcement of their merger agreement sent shockwaves throughout the IT industry.

However, due to issues concerning control of the merged entity and brand retention, the collaboration collapsed within just a few days. Subsequently, competition between the two major motherboard brands intensified, becoming increasingly fierce.

Generally, corporate mergers require adherence to specific procedures, including disclosing the intent to cooperate, finalizing detailed plans, submitting the plans for approval at respective shareholders’ meetings, filing with government authorities for review, and engaging accounting firms and investment banks to complete audits. As this merger was terminated immediately after the disclosure of cooperation intent, it remains uncertain whether it would have triggered antitrust regulatory scrutiny.

Although the Anti-Monopoly Law stipulates that a business operator may be presumed to hold a dominant market position if its market share in the relevant market reaches one-half, or if the combined market share of two business operators in the relevant market reaches two-thirds, it also provides that a market position “capable of hindering or affecting the ability of other business operators to enter the relevant market” may likewise be deemed as constituting a dominant market position.

For the specialized healthcare informatics market, whether such mergers will trigger antitrust scrutiny remains to be seen through future potential merger cases.

The merger between Winning Health and B-Soft has caused a stir, largely due to the relatively fragmented state of the healthcare IT market.

After more than 20 years of industry development, the healthcare informatics sector has gradually formed a tiered structure. Companies in the first tier generate annual revenues exceeding RMB 1 billion, with the industry leader holding an estimated market share of around 10%. Firms in the second tier maintain revenues at approximately RMB 500 million, capturing a market share of 1%–4%. In addition, numerous small and medium-sized healthcare IT companies are distributed across China, primarily serving regional markets and lacking the capability to replicate their business models in other regions.

Companies in the first tier each have their own distinctive features, with minimal differences in their overall comprehensive strength. The gap between second-tier and first-tier companies is not insurmountable; with external support, second-tier players can still compete effectively. Although industry concentration has been increasing year by year, the annual increment remains limited, with leading companies seeing a concentration increase of only 0.5%–1% per year.

Although the proposed merger between Winning Health and B-Soft failed, industry consolidation remains highly probable, as evidenced by trends in other sectors. Should leading companies merge in the future, they could gain an overwhelming advantage over small and medium-sized healthcare IT firms, thereby reshaping the competitive landscape of the healthcare IT industry.

VCBeat believes that this will bring two major changes to industry competition: changes in the capital landscape and changes in competitive models.

Shift in Capital Landscape: Absolute Industry Leaders Siphon Off Sector-Wide Capital, Technology, and Talent

Capital refers not only to financing and market capitalization in the capital markets, but also includes operational resources such as human resources and technology. Due to the long-standing fragmentation of the medical IT industry, there is no clear perception of the market landscape that would emerge after an absolute market leader consolidates its position.

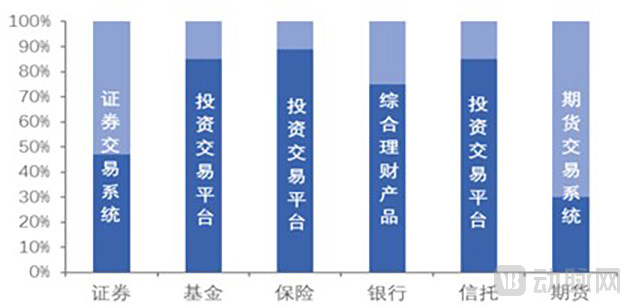

Taking the non-banking IT industry as an example, Hundsun Technologies is the absolute market leader in this sector, with most of its product lines commanding a 70%-80% market share, and even higher in certain areas. Other listed companies in the industry include Kingdom Sci-Tech, Ysstech, and Apex Software.

The dark blue section shows the market share of Hundsun Technologies' main product lines.

From a revenue perspective, in 2020, Hundsun Technologies generated RMB 4.173 billion in revenue, Kingstar Corporation reported RMB 1.734 billion (financial IT revenue), Ysstech recorded RMB 838 million, and Apex Software achieved RMB 350 million, underscoring Hundsun Technologies' absolute leading position.

The disparity in market capitalization is striking: Hundsun Technologies stands at RMB 89.9 billion, while the other companies lag behind by an order of magnitude. In terms of valuation multiples, Hundsun’s P/E ratio of 58.58x is approximately 1.5–2 times that of its peers, and its P/B ratio of 22.86x is roughly 5–10 times higher.

In terms of market capitalization and valuation, the absolute industry leaders enjoy a significant capital premium.

Stock Abbreviation | Market Capitalization (CNY 100 million) | Revenue | PE(TTM) | PB(LF) | Average Annual Salary per Capita (10,000 Yuan/Person) | R&D Expenses (CNY 100 million)) |

Hundsun Technologies | 899 | 41.73 | 58.58 | 22.86 | 25.46 | 14.96 |

Kingstar | 130 | 17.34 | 27.20 | 4.05 | 14.54 | 5.99 |

Yingshisheng | 82 | 8.38 | 36.42 | 2.86 | 16.60 | 3.26 |

Vertex Software | 43 | 3.50 | 39.87 | 3.91 | 14.55 | 0.89 |

Note: Market capitalization and valuation are based on the closing price as of July 20, 2021; revenue, compensation, and R&D expenses are data from 2020.

There are also significant differences in talent attraction and R&D investment. The average compensation level of a company can reflect the average competency of its employees. As the IT industry is a fully competitive market, employee compensation is closely correlated with their performance and capabilities.

According to public information, the average annual salary per employee at Hundsun Technologies is approximately RMB 250,000, which is RMB 100,000 higher than that of its competitors. This disparity significantly enhances its appeal to top talent in the industry. The company’s large scale, strong pricing power with downstream clients, and robust profitability enable it to offer higher compensation to its employees.

A company’s R&D capabilities are closely tied to the scale of its R&D expenditures. Hundsun Technologies invested approximately RMB 1.5 billion in R&D, significantly higher than Kingdom Sci-Tech’s RMB 599 million, and far exceeding the total revenue scales of Ysstech and Apex Software.

An examination of the non-banking IT sector reveals that the emergence of an absolute industry leader has resulted in significantly superior market capitalization and corporate valuation compared to peers. This indicates that such dominant players capture the vast majority of attention from capital markets, thereby facilitating a positive feedback loop between industrial operations and financial engagement.

If each company were to divest a 5% equity stake, Hundsun Technologies could raise RMB 4.5 billion, whereas Kingdom Sci-Tech, Ysstech, and Apex Software would only be able to raise RMB 650 million, RMB 400 million, and RMB 200 million, respectively. The level of support that different funding scales provide for the development of new products and technologies varies significantly. Small enterprises not only face limited fundraising capacity but also encounter greater difficulties in securing financing, with investors often imposing numerous hidden conditions. Moreover, there are already cases in the secondary market where small companies have failed to place their private placement shares. Furthermore, absolute industry leaders possess overwhelming advantages in attracting top-tier talent and mastering advanced technologies within the sector.

From the perspective of the medical IT industry, if an absolute market leader emerges, the industry landscape is bound to evolve toward the current state of the non-banking IT sector. The Matthew Effect in this industry is starkly realistic: superior companies are more likely to attract greater attention, along with increased inflows of capital and talent, thereby further strengthening their technological capabilities.

Downstream medical institutions are also more inclined to select products from absolute market leaders. These leading companies boast a large number of benchmark hospitals, numerous best-practice cases, strong technical capabilities, and a low risk of bankruptcy. Regional distributors will also allocate more resources to them. Consequently, the siphon effect exerted by industry leaders will be reflected in every aspect, reinforcing the principle that the strong grow stronger.

Shift in Competitive Dynamics: From Solution-Based Competition to Product Ecosystem Competition

The term "ecosystem competition" is commonly seen in the internet industry, but it is equally applicable to other sectors. The medical IT industry is generally divided into hospital IT, public health IT, and medical insurance IT. Although large medical IT companies are currently attempting to establish a presence across all three domains, no company has yet achieved comprehensive solutions in all three segments, let alone attained strong competitiveness in each of them.

Fundamentally, leading enterprises typically focus on a specific domain while maintaining a presence in others. For instance, Winning Health and Donghua Software specialize in hospital IT; B-Soft focuses on public health IT and is also a leader in the hospital IT sector; Jiuyuan Yinhai specializes in medical insurance IT; and Medis Technology concentrates on surgical anesthesia and ICU solutions within hospital IT.

Currently, the industry remains at the stage of product or solution competition, with competitiveness hinging on the performance or cost-effectiveness of solutions within specific business lines. In the future, assuming that the merged entities can achieve complementary business advantages, they would possess significant competitive edges in hospital IT, public health IT, and medical insurance IT. By building a robust product ecosystem and establishing themselves as an industry “triathlete,” they would profoundly reshape the competitive landscape.

VCBeat believes that the influence of all-around players on their competitors is immense. Although the merger between Winning Health and Chuangye Huikang ultimately failed, we can still use a hypothetical completed merger as a case study to illustrate the impact of such all-around players.

Taking the East China market in the medical IT industry as an example, this region is a stronghold for both Winning Health and B-Soft. In certain prefecture-level markets within East China, tier-2 and tier-3 hospitals typically adopt Winning Health’s or B-Soft’s Hospital Information Systems (HIS) or Electronic Medical Record (EMR) systems, while regional health information platforms often utilize B-Soft’s public health platform. Other key players in the industry include Donghua Software, Jiahe Meikang, Neusoft Group, and Meditech.

Healthcare IT is inherently a vast ecosystem, requiring data exchange among hospital IT, public health IT, and medical insurance IT systems. In particular, hospital IT and public health IT need to achieve interoperability and seamless connectivity. Products from various enterprises are interconnected, mutually supportive, and yet also constrain one another.

Among these, the Hospital Information System (HIS) and Electronic Medical Records (EMR) constitute the core of hospital information systems, with other systems such as the Laboratory Information System (LIS) and nursing systems interfacing with them. Consequently, in hospitals lacking an dedicated integration platform, the HIS often assumes the role of an information integration platform. It must ensure stable 24/7 operation; otherwise, hospital operations would be significantly impacted. Vendors of these core systems typically hold substantial bargaining power, enabling them to influence the normal operation of other products.

In a previously balanced competitive landscape, such as in the market for core hospital IT systems in a certain region where Winning Health held a 25% market share, B-Soft 30%, and Donghua Software 20%, with the remaining 25% accounted for by other vendors, large enterprises engaged in both competition and cooperation, while small and medium-sized enterprises could pursue differentiated strategies or partner with multiple major players to find their own equilibrium.

However, once market equilibrium is disrupted, market dynamics become increasingly complex. Suppose Winning Health and B-Soft merge; the new entity would command a 55% market share, holding a majority position and further strengthening its bargaining power. The merged company would not only boast numerous benchmark clients within the region and maintain stable downstream customer relationships, but also possess significant leading advantages in both hospital IT and public health IT product solutions.

New companies can compete with single-product firms through low-price strategies, and with solution providers by offering high reliability and a superior price-to-performance ratio. As the gap in market influence between large enterprises and others widens significantly, constraints on the former have weakened, while small and medium-sized enterprises find it increasingly difficult to strike a balance among multiple competing players.

Ecosystem competition operates at a higher dimension than product or solution-based competition, and dimensional reduction strategies deliver overwhelming dominance. The merger between the leading hospital IT provider and the top public health IT player exemplifies this industry-shaping impact. What if the leading medical insurance IT provider in Southwest China were to join this consolidation? The resulting competitive landscape of the healthcare IT sector is easy to envision.

Once an absolute industry leader emerges, the competitive landscape of the sector is bound to change. VCBeat believes that different companies can adopt varying response strategies.

Major Listed Medical IT Company:

(1) The merger of the two companies will inevitably involve a certain period of adjustment; the company is accelerating its development through organic growth and the introduction of external talent and resources.

(2) Accelerate the integration of industrial resources, adopt a unified development model, foster strategic alliances between listed companies to build a product ecosystem.

(3) Acquire single-product companies or small and medium-sized regional firms to strengthen its own capabilities, consolidate its existing strongholds while continuously expanding their scope, or connect different strongholds into a contiguous network for mutual reinforcement.

Prospective Listed Company:

Here, "pre-IPO companies" refer to enterprises that have already filed for an initial public offering (IPO) and either currently meet listing requirements or are expected to do so within the next one to two years. These companies’ products and services have gained market recognition, positioning them as leading players in specific regions or niche market segments. In terms of financial metrics, they generate annual revenues exceeding RMB 300 million and achieve net profits of approximately RMB 30 million.

(1)In ecological competition, going it alone is no longer the optimal strategy. In industries dominated by leading companies, other listed firms have seen a significant decline in capital market attention. Integrating into existing ecosystems or building one’s own ecosystem has become both important and urgent.

(2) Further deepen cultivation in a specific region or product portfolio to build a robust competitive moat. Closely monitor market dynamics and competition among industry leaders, and seize opportunities as they arise.

SMEs:

Such enterprises are typically small and medium-sized businesses in regional markets, or emerging single-product companies.

(1) Undertake strategic adjustments to avoid red ocean competition.

(2) Become a regional distributor or partner for ecosystem enterprises, leveraging the advantage of proximity to customers to retain downstream clients, meet certain personalized needs, and provide basic system operation and maintenance services.

VCBeat predicts that even if an absolute industry leader emerges, new opportunities will still arise. With the advancement of the healthcare sector and emerging technologies, medical technology is rapidly evolving, giving rise to new market segments. This presents fresh development opportunities for industry players. Promising new sectors currently include healthcare business systems, internet-based operations for offline medical institutions, and pharmaceutical IT.

Healthcare Business Systems

Traditional healthcare IT has primarily focused on healthcare management systems, such as Hospital Information Systems (HIS), Electronic Medical Records (EMR), regional health platforms, and core medical insurance systems, with insufficient product coverage in clinical and operational domains. Currently, the healthcare IT penetration rate (defined as healthcare IT investment divided by total healthcare industry investment) stands at approximately 1%. This figure indicates that the healthcare sector has largely completed the digitalization of its administrative and management processes.

Currently, the informatization maturity of China's securities industry is relatively high. According to data from the Securities Association of China, IT spending accounted for 5.82% of total expenditures in 2019, with some securities firms allocating as much as 8%–10%. This is because informatization has been implemented not only in management processes but also in core business operations, such as brokerage trading systems and margin financing and securities lending systems. Investment in the informatization transformation of business operations far exceeds that dedicated to management functions.

Currently, the informatization of the healthcare industry is expanding from non-clinical areas (administrative functions) to core clinical service domains, such as Surgical Anesthesia Information Systems, ICU Management Systems, Clinical Decision Support Systems (CDSS), and electronic Clinical Research Organizations (eCRO). These products constitute a vital component of the future healthcare product ecosystem. They demand deep industry know-how and present significant entry barriers. Consequently, high-quality enterprises in this sector enjoy considerable market viability and possess premium pricing power relative to other ecosystem participants.

Internet Operations of Offline Medical Institutions

Medical services cannot be fully digitized, as diagnostic tests and examinations cannot be conducted entirely online. Internet healthcare is inherently an O2O (Online-to-Offline) model, with the offline component relying on physical medical institutions, particularly public hospitals.

Digital transformation involves more than just launching an internet hospital system; it also encompasses the optimization of online and offline medical processes, the promotion and operation and maintenance (O&M) of internet hospital platforms, the management of physicians’ online consultations, the intelligent upgrading of online consultation systems, and the establishment of pharmaceutical delivery systems. While the core providers of medical services remain offline entities, online operations will increasingly be handled by more specialized institutions. Drawing an analogy to the e-commerce industry, which gave rise to third-party e-commerce operation services, the internet healthcare sector will foster the emergence of specialized internet hospital operation companies. Against the backdrop of increasingly refined industry specialization, professional tasks should be entrusted to professionals.

The healthcare industry is a trillion-dollar market with strong profitability. As the highly specialized, large-scale healthcare sector undergoes digital transformation, it is poised to give rise to major internet-based healthcare operation service providers.

Pharmaceutical Informatics

With the gradual implementation of policies such as the “Two-Invoice System,” zero markup on drug prices, generic drug consistency evaluation, and volume-based procurement, China’s pharmaceutical industry—once characterized by extensive growth—has entered an era of refined operations. Pharmaceutical companies now prioritize efficient R&D, precision manufacturing, and compliant sales practices. These diverse operational needs clearly reflect a strong demand for digitalization and information technology solutions. In the overseas market, the CRM sector for the pharmaceutical industry has even given rise to Veeva Systems, which boasts a valuation of $50 billion. Moreover, AI-driven new drug discovery systems and pharmaceutical production management platforms offer even broader market potential.

Despite the dramatic changes surrounding the merger between Winning Health and B-Soft, market sentiment holds that industry consolidation will inevitably intensify. Indeed, judging by trends in the healthcare IT sector in recent years, business integration and mergers and acquisitions among IT enterprises have become the norm. Companies are striving to build comprehensive, integrated solutions to secure more valuable targets, a trend that has become irreversible.

Looking at other industries, all have undergone such a process of consolidation. Although the healthcare IT market is somewhat unique, it is ultimately no exception. Proactively planning for collaboration and mutual success may well be a positive and forward-thinking move. So, who will be the next pioneer to brave the unknown? We shall wait and see.

We extend our sincere gratitude to Mr. He Bingyu, Computer Industry Analyst at Zhongtai Securities Research Institute, for his invaluable support of this article.