Hillhouse and Lilly Asia Lead Capital Back into Clinical Diagnostics with Digital PCR Resurgence

From the perspective of many investment firms, by 2019, the growth potential of digital PCR was nearly exhausted. However, just two years after being removed from their watchlists, digital PCR made a strong comeback to its former peak, prompting some investors to admit they had been proven wrong.

By mid-July, when Leading Genes announced the completion of its RMB 120 million Series A+ financing round, four financing deals had already taken place in the digital PCR (dPCR) field during the first seven months of 2021. Among them, New羿 Biotechnology,锐讯 Bioscience, and Leading Genes, which had performed exceptionally well during the previous wave of dPCR investment, successively secured new funding. Notably, New羿 Biotechnology’s RMB 150 million Series B financing set a new record for fundraising in the vertical dPCR sector. The investor landscape during this period featured prominent firms such as Hillhouse Capital and Lilly Asia Ventures, making the scene quite remarkable.

In fact, signs of a resurgence in digital PCR (dPCR) had already emerged a year earlier, when Caydy and Serenabio completed new rounds of financing. In September 2020, Serenabio, leveraging its extensive expertise in cell separation technologies, closed its Series B funding round and entered the dPCR market based on high-throughput single-cell and DNA analysis technologies, aiming to develop miniaturized, high-performance instruments. Three months later, Caydy completed a RMB 600 million Series D financing round. Coincidentally, in May 2019, several years after launching its flagship products, the Flash Test™ FLAH and Mini 8, Caydy obtained registration certification for its independently developed biochip analyzer, the DX100, thereby entering the dPCR market with a comprehensive solution-based approach.

In March 2020, Dapu Bio completed a RMB 20 million angel round of financing;

In March 2021, Darui Microbiology completed its Pre-A round of financing, with investors including Qingkong Jinxin Capital and Maccura Biotechnology.

In July 2021, NextCode Genetics completed a RMB 120 million Series A+ financing round, with investors including Sharing Investment and Puxin Capital;

In February 2021, Raybiotech completed a Series B1 financing round worth tens of millions of yuan, with investors including Zero2IPO Asset Management, Cathay Capital, Mingshi Capital, and Volcanic Stone Capital;

In January 2021, NewEra Bio completed a Series B financing round of RMB 150 million, with investors including Lilly Asia Ventures, Huachuang Capital, Hillhouse Venture Capital, Qingdao Yufeng, and Chongyuan Huichen.

In December 2020, Cayudi completed a Series D financing round of RMB 600 million, with investors including Hillhouse Venture Capital, Jinhe Capital, Huiyuan Capital, and FreeS Fund.

In September 2020, Serenata completed a Series B financing round amounting to tens of millions of yuan, with investors including Hanyi Capital, Jinhe Capital, Chende Capital, and Celula-HK.

Between 2017 and 2018, as leading medical device manufacturers such as Bio-Rad, Thermo Fisher Scientific, Roche, Qiagen, and Illumina invested heavily in mergers, acquisitions, or strategic layouts in digital PCR, this technology—known as the third-generation PCR for its superior resolution and precision compared to mainstream fluorescent PCR—was considered to have reached an inflection point in industrialization, poised to largely replace fluorescent PCR, which had long dominated clinical laboratory testing.

Investment firms have entered the market in force. During this period, companies such as Leadgene, Ruisun Biotech, and New Yier Biotechnology each completed at least one round of financing. More molecular diagnostics companies have incorporated digital PCR into their business plans, while investment institutions have intensified their engagement with digital PCR-related projects. In 2017, when the molecular diagnostics sector was experiencing unprecedented hype, digital PCR emerged as an exceptionally hot subfield.

However, the shortcomings of digital PCR (dPCR) have been exposed earlier amid its rapid expansion. Although dPCR is more precise than fluorescence-based PCR, it is more difficult to operate and incurs higher costs. While it is cheaper than next-generation sequencing (NGS), it can only detect known gene sequences, similar to fluorescence-based PCR, placing dPCR in an awkward position. In fields such as COVID-19 testing, pathogenic microorganism detection, tumor companion diagnostics, and non-invasive prenatal testing (NIPT), dPCR faces intense competition from products based on different methodologies. Due to the inability to identify optimal application scenarios and secure a strategic position to deliver unique clinical value, the dPCR market has gradually cooled down. More investment institutions have adopted a wait-and-see approach, while companies have begun to delve deeper into technology, focusing on cost reduction, efficiency improvement, and equipment development. Those companies that had initially entered the market merely to capitalize on the hype have quietly exited.

For a time, whether digital PCR could leverage capital to replace fluorescent PCR and take hold in clinical laboratory departments remained uncertain.

“The advantages of digital PCR technology itself are widely recognized in the market. However, industry players are continuously exploring its market and product positioning while striving for breakthroughs in technological iteration. Therefore, companies that achieve genuine breakthroughs in overcoming technical barriers continue to gain capital recognition, with overall investor sentiment becoming more rational,” Fang Weicheng, Investment Director at Qingtong Capital, told VCBeat.

Another industry practitioner told VCBeat that the renewed market enthusiasm for digital PCR is closely tied to breakthroughs in both technology and the market. “It is evident that companies such as Genetalks, New羿 Biotechnology, and Leadgene, which have secured additional financing, have been focusing on digital PCR technology for many years and have made many valuable explorations in engineering optimization and market promotion.”

Take New Yier Biotechnology as an example. In 2020, after obtaining national medical device marketing authorization, New Yier Biotechnology’s instrument products officially went on sale. According to co-founder Yang Wenjun, data research conducted via the bidding and tendering network at the end of 2020 showed that New Yier Biotechnology’s instruments ranked second in market share among all brands, trailing only Bio-Rad.

For another example, in February 2021, Leading Gene’s CS-series biochip reader officially received approval from the Zhejiang Provincial Medical Products Administration. This marked the industry’s first complete set of equipment—comprising premix reagents, sample preparation instruments, PCR amplifiers, and biochip readers—to gain such regulatory certification for Leading Gene. It is also currently the only commercially available digital PCR product with seven-color fluorescence channels and independent intellectual property rights, filling a gap in multi-color fluorescence channel digital PCR technology. Amidst intense competition from multinational brands, Leading Gene’s technological and engineering capabilities are being translated into market advantages.

For digital PCR (dPCR), the question of how to maximize its advantages and establish it as a widely recognized first-line methodology in the industry is what capital and the market are most concerned about. “On one hand, many dPCR companies are continuously breaking through bottlenecks such as high operational complexity and considerable costs by improving technology R&D and building automated system equipment. On the other hand, against the backdrop of China’s encouragement of clinical innovation, application scenarios for dPCR have been expanded and innovated, restoring confidence among investors,” pointed out Fang Weicheng.

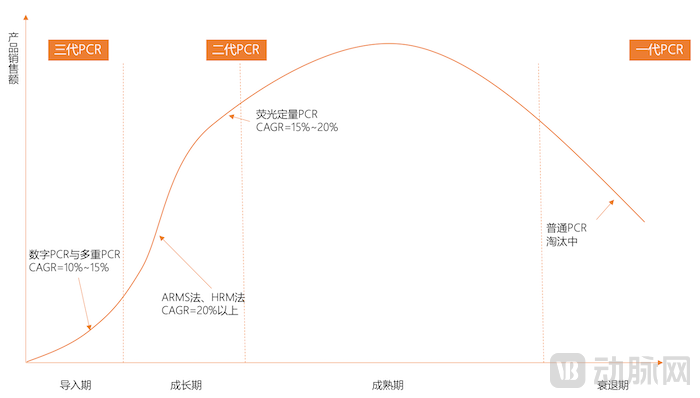

PCR, short for Polymerase Chain Reaction, originated in the 1970s and 1980s. Up to the emergence of digital PCR, it is widely recognized to have undergone three major technological iterations. Among these, second-generation PCR, characterized by quantitative fluorescence, is currently the most mature and mainstream molecular diagnostic technology in clinical applications. It is extensively used in various fields, including pathogen detection for infectious diseases, tumor gene testing, blood screening, and genetic disease gene testing, accounting for approximately 40% of China’s molecular diagnostics market.

PCR Sub-Technology Lifecycle (Data Source: Guoyuan Securities Research Center; Chart by VCBeat)

During this period, with the optimization of nanofabrication and microfluidics technologies, digital PCR—a technology offering more refined control over the reaction process than quantitative fluorescent PCR—has gradually achieved commercialization.

The principle of digital PCR (dPCR) technology is straightforward. The sample undergoes limited dilution and is partitioned into tens of thousands of nanoliter (nL)-scale reaction units. Each unit performs an independent PCR amplification, and the instrument analyzes the endpoint fluorescence signal from each unit individually. Units exhibiting a fluorescent signal are scored as “1,” while those without are scored as “0.” These binary results are then statistically analyzed based on the Poisson distribution to calculate the initial copy number or concentration of the target molecules.

Digital PCR Workflow (Source: Zhihu; Graphic by VCBeat)

In the early stages of development, sample partitioning remained a persistent technical bottleneck for digital PCR. Initial researchers attempted to use 96-well, 384-well, or even 1536-well plates as carriers for digital PCR partitioned reactions, or adopted bead-based emulsion amplification methods similar to flow cytometry techniques, such as BEAMing (Beads, Emulsion, Amplification, and Magnetics). However, the challenge of effective sample partitioning was never adequately resolved.

Fluidigm and Germany’s Inostics launched dPCR detection systems based on chip technology and magnetic bead methods in 2006 and 2008, respectively. However, these approaches failed to meet more stringent requirements in terms of partitioning resolution and data population size, while time and consumable costs severely constrained the development of dPCR technology. It was not until QuantaLife developed droplet digital PCR (ddPCR) technology using water-in-oil emulsion droplet generation that the first relatively mature digital PCR platform emerged, achieving commercial viability in terms of operational costs and experimental result stability.

In 2011, Bio-Rad Laboratories swiftly acquired QuantaLife and rebranded its droplet digital PCR instrument as the QX100 system, which continued to be marketed commercially. This early model played a pivotal role in popularizing the concept of dPCR and expanding its applications. In 2013, the company launched the upgraded QX200 model.

In 2012, RainDance Technologies launched the RainDrop digital PCR system. This instrument leveraged its existing next-generation sequencing library preparation platform technology and adapted it to the digital PCR platform. Driven by high-pressure gas, the system partitions each standard reaction mixture into a reaction emulsion containing 1 million to 10 million picoliter-scale droplets (5–10 million droplets per 25–50 µL, which is 250–500 times that of Bio-Rad’s system). This approach provides a wider dynamic range for detection, making it suitable for processing samples with substantial differences in concentration.

In April 2013, Thermo Fisher Scientific acquired Life Technologies for $13.6 billion. In June of the same year, Life Technologies launched the QuantStudio 3D Digital PCR System, positioned as a digital PCR system suitable for all molecular biology laboratories. Utilizing high-density nanoliter microfluidic chip technology, the system evenly distributes samples into 20,000 individual reaction wells. Throughout the entire workflow, samples remain completely isolated, effectively preventing cross-contamination, reducing pipetting steps, and simplifying operational procedures. Additionally, the chip-based design avoids the tubing clogging issues that may be encountered in droplet-based systems.

In January 2017, Bio-Rad acquired RainDance for $87 million. Subsequently, Illumina, Roche, and Qiagen successively announced their entry into the digital PCR market, driving market enthusiasm to a peak.

On November 20, 2018, Illumina Ventures led the investment in Stilla Technologies. The latter’s Naica Crystal droplet digital PCR system is the easiest-to-operate on the market and the only digital PCR system capable of simultaneous three-color detection. It serves as the official supplier of digital PCR systems to multiple hospitals in France.

That month, Roche reported on the progress of its in-house digital PCR instrument development. A company representative stated that the system, which was then in the prototype development stage, comprised two instruments: a compact desktop partitioning unit and a larger benchtop analyzer. The complete system also included analysis software capable of running on local laptops or desktop computers. However, in terms of composition, Roche’s digital PCR system bore a striking resemblance to Bio-Rad’s QX200.

In January 2019, QIAGEN announced the acquisition of Formulatrix’s digital PCR technology, marking its official entry into the digital PCR market. At that time, QIAGEN stated its plan to develop a handheld, battery-powered digital PCR system based on Formulatrix’s technology. This portable system was intended to facilitate the use of the QuantiFERON-TB Gold assay for detecting latent tuberculosis infection in resource-limited settings.

The first wave of commercial applications of digital PCR reached China in less than five years.

In April 2017, Nanjing Covaris’s chip-based digital polymerase chain reaction (dPCR) analysis system was officially included in the “green channel” for special approval of innovative medical devices, as publicized by the China Food and Drug Administration (CFDA). In July of the same year, the CFDA formally approved the market launch of Novogene Bioinformatics Technology Co., Ltd.’s Digital PCR NG, a digital PCR chip reader. This device is indicated for the detection of T790M mutations in cell-free DNA samples from human plasma and can be used in conjunction with Novogene’s EGFR Gene T790M Mutation Detection Kit. Novogene independently developed supporting software for its digital PCR system, which features a fully Chinese-language interface and allows for easy reading of test results without manual threshold adjustment. A few months later, the Chongqing Municipal Food and Drug Administration formally approved the market launch of Genetron Health’s biochip reader (Digital PCR)—the GENETRON 3D—which is capable of detecting rare mutation sites with mutant allele frequencies as low as 0.1% in blood cfDNA.

However, the aforementioned three digital PCR products were co-developed with Thermo Fisher.

In September, Turtle Tech launched its chip-based digital PCR product, the BioDigital System, which comprises a microdroplet generator, an image acquisition and analysis instrument, chips, and reagents. The system can generate over 20,000 microdroplets, each with a volume of 0.79 nL, on a dPCR chip within two minutes, and the entire detection process can be completed in approximately 1.5 hours.

The following month, Yongnuo Biotech launched its independently developed MicroDrop™ Droplet Digital PCR system. Utilizing water-in-oil emulsion droplet technology, the instrument employs air pressure drive within microchannels to generate 100,000 droplets from a mere 20 µL sample, with individual droplet volumes as low as the nanoliter scale. It offers a linear dynamic range spanning six orders of magnitude and a sensitivity as low as 0.01%. The system is widely applicable in fields such as scientific research, clinical medicine, and entry-exit inspection and quarantine.

Enthusiasm for the commercialization of digital PCR in China persisted throughout 2018.

In January, AccuBioTech launched the AccuOne™ chip-based digital PCR system, which features independent intellectual property rights and includes an automated dispenser, a thermal cycler, and an analyzer. Its core technologies encompass micro-nano fabrication, precision instrumentation, image recognition, and algorithmic software. The company claims that, when combined with its self-developed molecular diagnostic reagents, key performance indicators such as droplet count, fluorescence channels, precision, accuracy, and sensitivity have reached or surpassed those of mainstream international products. On January 18, 2021, AccuBioTech announced that its self-developed AccuONE Reader for digital PCR biochips and its digital PCR master mix had obtained registration certificates issued by the National Medical Products Administration (NMPA).

In April, Cayudi launched its self-developed digital PCR product, a multiplexing-capable and user-friendly platform that meets the clinical and research demands for high sensitivity as well as the stringent cost requirements of research institutions.

In July, the iScanner24 biochip reader, developed by Leading Gene, obtained the Medical Device Product Registration Certificate from the Zhejiang Provincial Food and Drug Administration (Zhejiang Medical Device Registration No. 20182400319). The intended use of this product is “to be used with compatible chips for the detection of target genes in samples.”

In the same month, New Yier Biotechnology launched the TD-1 Digital PCR System, which features fully independent intellectual property rights. The company also released trial kits of its droplet generation oil, detection oil, PCR Master Mix, and EGFR mutation detection kit. Independent evaluations by dozens of institutions across China have demonstrated that these reagents are highly compatible with imported digital PCR platforms, with quality comparable to imported products and certain performance indicators even surpassing them.

Although digital PCR systems that have truly entered clinical laboratory use are still dominated by overseas brands such as Bio-Rad, the years of accumulation by domestic manufacturers in technology, engineering, and marketing have provided a sufficiently rational industrial foundation for the current resurgence of investment in digital PCR.

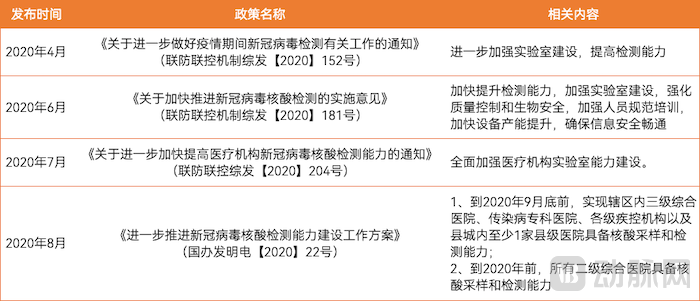

In addition to the proactive efforts within the industry, China’s supportive environment for clinical innovation has provided fertile ground for the commercialization of domestically produced digital PCR systems, thereby raising their market ceiling. In the aftermath of the COVID-19 pandemic, shortcomings in primary-level testing capacity became apparent, prompting policy mandates to launch new healthcare infrastructure initiatives and leading to a large-scale construction of PCR laboratories in primary healthcare institutions.

In April, June, and July 2020, the National Health Commission repeatedly issued policies requiring the strengthening of laboratory construction. In September, the Joint Prevention and Control Mechanism of the State Council issued the “Work Plan for Further Advancing the Construction of Nucleic Acid Testing Capacity for COVID-19,” which emphasized that “by the end of September 2020, all tertiary general hospitals, specialized infectious disease hospitals, disease prevention and control institutions at all levels, and at least one county-level hospital within each county should have nucleic acid sampling and testing capabilities. By the end of 2020, all secondary general hospitals should have nucleic acid sampling and testing capabilities, and the construction of urban testing bases and public testing laboratories should be completed.” The decentralization of PCR laboratory resources has become a key focus in strengthening grassroots testing capabilities.

Policies on Strengthening Laboratory Construction in Medical Institutions (Compiled by VCBeat from Public Information)

Historically, the stringent environmental requirements for PCR testing have led to a concentrated distribution of laboratory resources. Conventional PCR technology necessitates continuous heating and cooling cycles during the reaction process. The evaporation and subsequent condensation of sample liquids can easily form aerosols carrying substantial amounts of sample DNA into the air, thereby contaminating other samples. Consequently, PCR testing requires dedicated PCR laboratories that segregate operational workflows—including reagent preparation, specimen processing, amplification, and analysis—and maintain air cleanliness by controlling airflow direction. These requirements impose high standards for both facilities and personnel. As a result, laboratories are predominantly concentrated in tertiary hospitals (Grade III Class A) and major third-party testing centers, which has, to some extent, constrained the commercial growth potential of digital PCR.

According to mid-2020 statistics, China currently has 2,831 tertiary hospitals, 9,901 secondary hospitals, 1,102 specialized hospitals, and 3,402 disease control and prevention institutions. In the long run, the decentralization of PCR laboratory resources holds greater significance in expanding grassroots access to various molecular diagnostic tests, bridging the gap between molecular diagnostics and primary-care patients, and supporting the surge in demand for digital PCR in clinical laboratory testing.

VCBeat’s analysis of bidding and tendering information reveals that since 2020, numerous medical institutions across various regions have procured digital PCR-related equipment. In addition to overseas brands such as Bio-Rad and Illumina, which remain mainstream, domestic suppliers like New羿 Biotechnology and Ruixun Biotechnology are increasingly winning bids. These domestic companies are steadily penetrating the clinical laboratory departments of primary healthcare institutions by offering higher cost-effectiveness.

Therefore, to some extent, the renewed enthusiasm of capital for digital PCR will ultimately translate into adoption in clinical laboratory departments. This wave of interest is clearly still ongoing; while its future trajectory remains uncertain, its underlying rationale is at least sufficiently sound.

Reference Article:

The Mysterious Zone of the Hospital—The PCR Laboratory

Digital PCR Attracts Global Giants: How Does New羿 Biotech Navigate the Waves?

Major Breakthrough! Linghang Gene Accelerates Its Expansion into the Digital PCR Market, Securing Medical Device Approval for Seven-Color Fluorescence Channel Digital PCR

Are CT Reports Always Accurate? Are Absolute Quantification Results Using Digital PCR Always Accurate?

Xinyi Bio Official Website