Neurointervention Continues to Surge: Global High-Value Medical Consumables Market Trends Report 2010–H1 2021

Editor's Note

VBInsight’s latest report, “Global Value Trends in High-Value Medical Consumables (2010–H1 2021),” focuses on cardiovascular interventional consumables, blood purification consumables, neurological consumables, dental consumables, ophthalmic consumables, orthopedic consumables, and medical aesthetics consumables.

The following video distills the key insights from the full report, showcasing a decade of changes in the high-value medical consumables sector through 60 seconds of dynamic data.

Global investment and financing in the high-value medical consumables sector have been on an upward trend since 2010, with explosive growth driven by the pandemic and favorable policy incentives in 2020, continuing into the first half of 2021.

In H1 2021, the high-value medical consumables sector witnessed an IPO boom, with 10 companies worldwide going public, including six from China, setting a new historical record.

Niche sectors such as cardiac valves and neurointerventional devices are attracting significant capital interest in China, driving up investment sentiment across the entire high-value consumables sector. In the cardiac valve field, domestic companies are actively striving to break through competitive barriers. The neurointerventional sector has a high likelihood of replicating the path of import substitution seen with coronary stents, as Chinese manufacturers build comprehensive product portfolios from the ground up.

The government has intensified its efforts to promote centralized procurement of high-value medical consumables, benefiting domestic industry leaders. Meanwhile, with the volume-based procurement policy for artificial joints already released, the orthopedic consumables sector is poised for a major reshuffle.

High-Value Consumables - Industry Overview

High-value medical consumables refer to medical supplies that act directly on the human body, are subject to stringent safety requirements, are used in large clinical volumes, have relatively high prices, and impose a significant financial burden on patients.

This report focuses on the analysis of consumables for cardiovascular intervention, blood purification, neurology, dentistry, ophthalmology, orthopedics, and medical aesthetics.

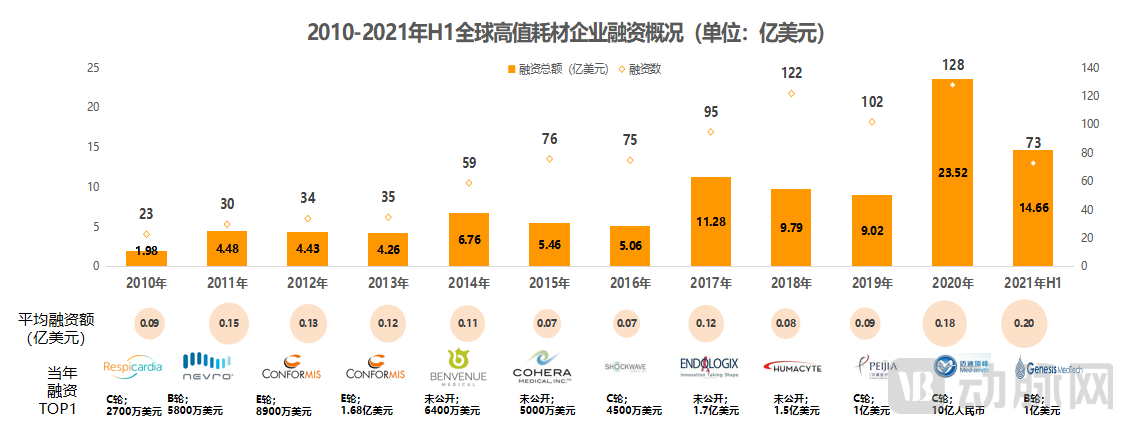

Financing Trends of Global High-Value Medical Consumables Companies, 2010–H1 2021

Globally, investment and financing in the high-value consumables sector have shown a trend over the past decadeRiseTrends: In 2020, a total of 128 financing deals were completed, with the total funding amount reaching $2.351 billion, a 161% quarter-on-quarter increase. The total funding in the first half of 2021 alone exceeded the annual funding of any year prior to 2020.

In China, the capital market experienced a brief downturn after the government piloted centralized procurement of high-value medical consumables in 2017; however, spurred by the pandemic in 2020, financing in the high-value medical consumables sector sawPhased Outbreaks, attracting more capital investment; by 2021, the momentum remained strong, with 73 financing deals in the first half of the year alone, totaling $1.466 billion.

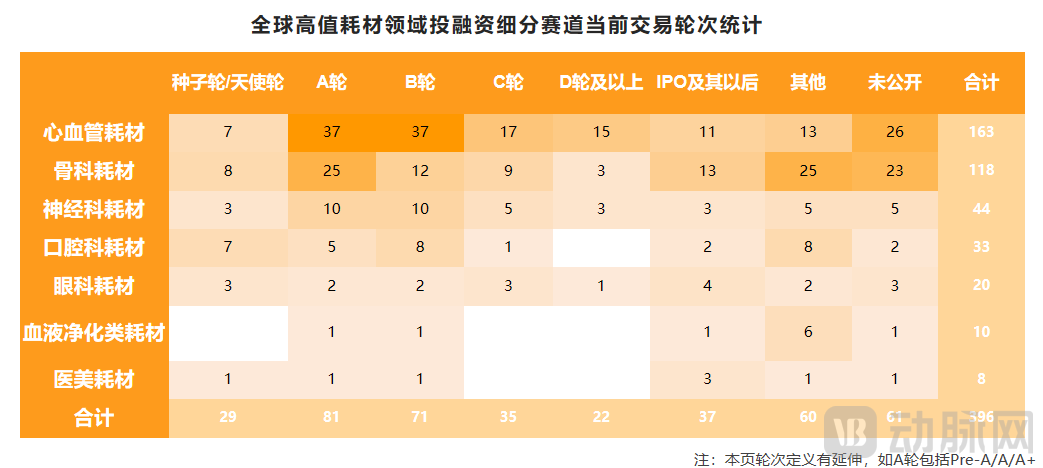

Statistics on Current Funding Rounds by Sub-sector in the Global High-Value Medical Consumables Industry

From the perspective of financing rounds, high-value consumables companies are currently concentrated in Series A and Series B. Combined with the previous charts, it is evident that many companies have remained in the early stages. This is due to the excessively high technical barriers in the high-value consumables sector, which requires companies to possess independent innovation capabilities. Furthermore, the international market has long been dominated by giants, leading other small and medium-sized enterprises to experience “High Quantity, Small Scale” landscape, industry competitive landscapeRelatively Dispersed。

From the perspective of specific sub-sectors,Cardiovascular ConsumablesCardiovascular consumables generated the highest level of interest, followed by orthopedic and neurological consumables. Compared with other niche sectors, many cardiovascular consumable companies have entered the maturity stage, whereas orthopedic consumable companies are more likely to pursue initial public offerings (IPOs). As of June 30, 2021, 15 cardiovascular consumable companies had reached Series D or later financing rounds, while 13 orthopedic consumable companies had gone public.

Capital Trends in the Global High-Value Consumables Sector in H1 2021 (1): Neurointerventional Market in China Remains Hot, with Investors Heavily Betting on It

According to incomplete statistics from VCBeat, as of the first half of 2021, at least 24 innovative companies and 60 investment institutions had invested in the neurointerventional field in China. Furthermore, since 2020, two companies have successfully gone public, and two others have filed prospectuses.

The neurointerventional sector continues to heat up, which is closely tied to its large market size, rapid growth rate, upstream technology-driven innovation, and national policy support. Meanwhile, domestically produced neurointerventional products are gradually matching the quality of imported counterparts. For instance, Peijia Medical’s chemically detachable coils, mechanically detachable coils, and access devices have received regulatory approval and are commercially available; its thrombectomy and aspiration devices are in clinical trials, while a range of complementary products for hemorrhagic and ischemic stroke are under accelerated development.

Capital Trends in the Global High-Value Consumables Sector in H1 2021 (2): Ten High-Value Consumables Companies Went Public Within Six Months, Setting a New Record

In 2020, only five high-value medical consumables companies went public, possibly due to the pandemic disrupting their listing plans; however, in the first half of 2021 alone, ten such companies completed their initial public offerings (IPOs), setting a new historical record.

MicroPort has consistently demonstrated strong performance, spinning off MicroPort Endovascular, MicroPort CardioFlow, MicroPort EP MedTech, and MicroPort MedBot to establish a presence in fields such as aortic and peripheral vascular interventions, heart valve therapies, and cardiac electrophysiology interventions. Two of these spin-offs have already gone public. Meanwhile, on the last day of the first half of 2021, Weigao Group also listed its spun-off entity, Weigao Orthopedics.

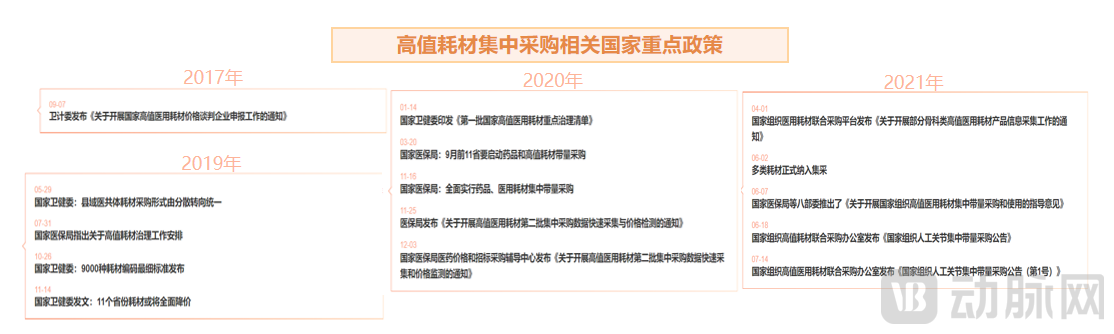

Hot Topics in China’s High-Value Medical Consumables Sector (2010–H1 2021) (1): Centralized Procurement

VBInsight has compiled over 100 policies related to the centralized procurement of high-value medical consumables. Notably, on June 21, the National Office for Joint Procurement of High-Value Medical Consumables released the "Announcement on the National Centralized Volume-Based Procurement of Artificial Joints." The products included in this volume-based procurement are primary total hip arthroplasty prostheses and primary total knee arthroplasty prostheses. The release of this announcement is expected to increase the market share of domestically produced orthopedic products, thereby further expanding the market presence of Chinese orthopedic companies.

In the long run, centralized procurement will inevitably increase the market share of domestically produced high-value medical consumables, benefiting leading Chinese manufacturers and further enhancing industry consolidation.

From a financing perspective, against the backdrop of normalized centralized procurement, capital is likely to flow into other sectors with high technical barriers and low current domestic production rates, such as the neurointerventional and peripheral interventional fields, which were gaining significant traction in 2021.

Hot Topics in China’s High-Value Consumables Sector (2010–2021) (Part 2): The Rapid Emergence of the Heart Valve Track, with TAVR Products Undergoing Commercialization

As the most closely watched subsector within the cardiovascular field, China’s heart valve sector has witnessed multiple large-scale financing rounds in recent years. In the first half of 2021 alone, six heart valve companies secured funding exceeding USD 100 million each, while MicroPort CardioFlow, spun off from MicroPort Scientific Corporation, listed on the Hong Kong Stock Exchange.

From a product perspective, a wave of domestic companies has emerged in China, making the substitution of imported heart valves with domestically produced ones an unstoppable trend. For instance, Venus Medtech’s second-generation transcatheter heart valve system, VenusA-Plus, has received approval from the National Medical Products Administration (NMPA) for market launch, becoming China’s first transcatheter heart valve system with retrievability features. Additionally, its transcatheter pulmonary valve system, VenusP-Valve, has gained early market access in the United Kingdom through special use authorization.

Five TAVR products have been approved and commercialized in China: MicroPort HeartFlow’s VitaFlow™, Venus Medtech’s VenusA-Valve and VenusA-Plus, Suzhou JieCheng’s J-Valve, and Peijia Medical’s TaurusOne. In addition, several other TAVR products in China are in or have completed clinical trials, such as MicroPort HeartFlow’s VitaFlow™ II, Venus Medtech’s VenusA-Plus, and Peijia Medical’s TaurusOne and TaurusElite.

Related Reports

Below is the full version of the report——

Scan the QR code below to watch the video on your mobile device.