Nearly RMB 4 Billion Invested: What's Fueling the Boom in Cell and Gene Therapy CDMO? — An Industry Overview (Part I)

WuXi AppTec

New Drug R&D and Production Service Provider

Pharmaron

Life Science R&D Service Provider

Recently, the cell and gene therapy (CGT) sector received more good news: On July 22, bluebird bio announced that the European Commission (EC) had granted marketing authorization for its one-time gene therapy Skysona (elivaldogene autotemcel, also known as Lenti-D) for the treatment of patients under 18 years of age with early cerebral adrenoleukodystrophy (CALD) carrying ABCD1 gene mutations.

Skysona is the first gene therapy approved by the European Union (EU) for the treatment of CALD. The successful approval of this product has further energized the rapidly advancing field of cell and gene therapy (CGT).

Since 2017, the cell and gene therapy (CGT) industry has continued to achieve breakthrough progress. Landmark CGT products such as Kymriah, Luxturna, and Zolgensma have been successively approved by the U.S. Food and Drug Administration (FDA) for market launch, while investment and financing in related fields have remained robust. Currently, the CGT industry has become one of the most promising global frontier sectors in pharmaceuticals.

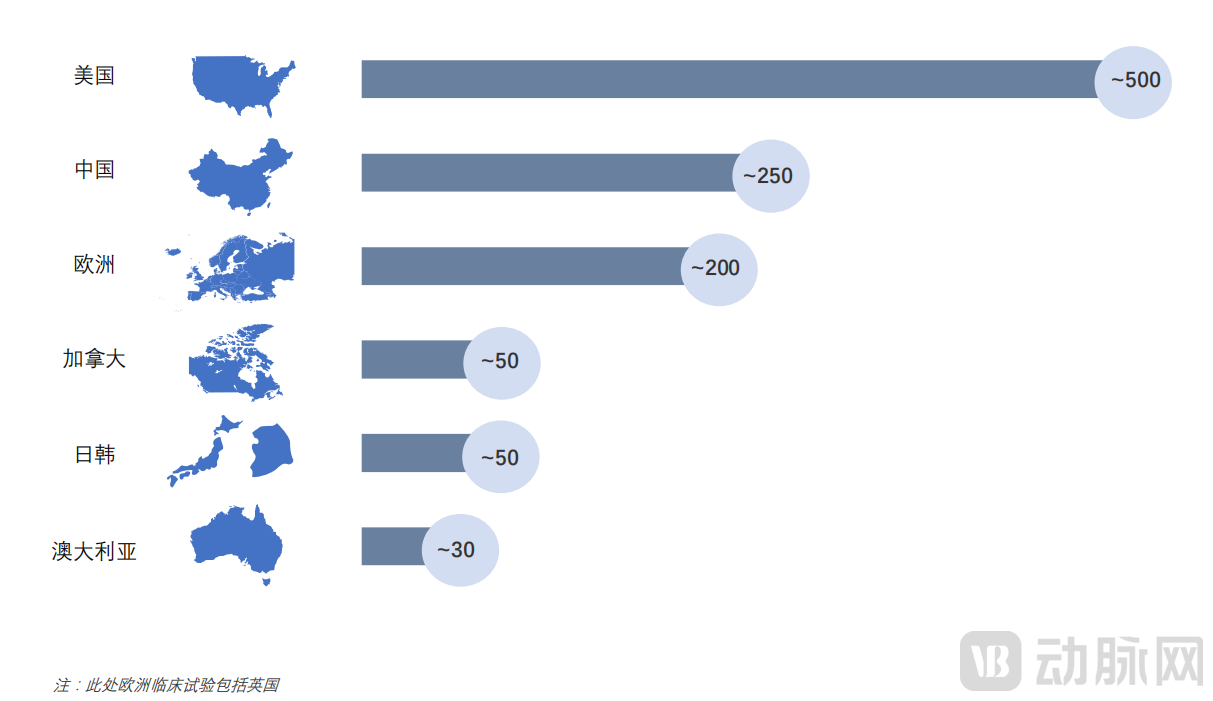

China has demonstrated remarkable agility in advancing within this frontier field. Since 2015, the number of clinical trials related to cell and gene therapy (CGT) in China has grown rapidly. According to data from Frost & Sullivan reports,Between 2015 and 2020, China conducted approximately 250 CGT clinical trials in total, becoming the region with the second-highest number of clinical trials after the United States. With a compound annual growth rate (CAGR) exceeding 60%, it ranked first globally.Currently, there are approximately 100 cell and gene therapy (CGT) clinical trials underway in China, involving around 80 companies of varying sizes, with the market exhibiting robust growth momentum.

Comparison of the Cumulative Number of Global Cell and Gene Therapy Clinical Trials Conducted from 2015 to 2020

(Source: ClinicalTrials.gov, compiled by Frost & Sullivan)

Amid a flurry of intensive research efforts, 2021—widely hailed by industry insiders as the “Year of Gene and Cell Therapy”—began to witness a series of remarkable breakthroughs.

In June 2021, Fosun Kite’s FKC876 (axicabtagene ciloleucel injection) received marketing approval, marking the launch of China’s first CAR-T product. WuXi Juntai submitted a marketing application for its CAR-T product JWCAR029 to the National Medical Products Administration (NMPA) in 2020, and this therapy is also expected to gain approval this year. Meanwhile, Cilta-cel, a CAR-T therapy developed by Nanjing Legend Biotech in collaboration with Johnson & Johnson for the treatment of relapsed or refractory multiple myeloma, is currently undergoing priority review by the U.S. Food and Drug Administration (FDA) and accelerated assessment by the European Medicines Agency (EMA). With impressive clinical trial data—specifically, a median long-term follow-up of 18 months in Phase 1b/2 trials, an objective response rate (ORR) of 98%, and an overall survival (OS) rate of 81%—this product has directly ignited strong expectations within China’s cell and gene therapy (CGT) industry for global market expansion.

As the research achievements of China’s first wave of gene and cell therapy companies gradually come to fruition, the market’s eager anticipation, intertwined with high hopes for future development, has attracted a large number of “gold diggers.” CGT R&D enterprises have sprung up like mushrooms after rain, and at this moment, the spring season for the “water sellers”—CGT CDMOs—has quietly arrived.

Compared with traditional drug development, gene therapy and cell therapy require higher R&D investment. According to a report by Frost & Sullivan,R&D costs for cell and gene therapies range from $900 million to $1.1 billion during the discovery and preclinical stages, and from $800 million to $1.2 billion during the clinical stage. Consequently, there is a strong demand in the gene and cell therapy R&D sector to leverage specialized contract research, development, and manufacturing organizations (CRDMOs) to reduce costs.Driven by rapid industry growth and a limited number of players, the gene therapy CDMO sector is currently experiencing a supply-demand imbalance.

The CGT CDMO market resembles an untapped blue ocean, attracting countless elite talents to enter the field. Everyone is eager to be the first to discover the great treasures hidden beneath this blue ocean. Consequently, industry giants are strategically positioning themselves, while startups are racing to expand, making the current CGT CDMO sector remarkably vibrant. Meanwhile, a large number of Chinese entrepreneurs find themselves at a crossroads, grappling with a dilemma: should they join the high-risk, high-reward “gold rush” of CGT, or opt for the CDMO “shovel-selling” model, which is currently at an earlier stage of development and carries lower risk, yet holds significant promise?

The “dilemmas” and “confusion” of these Chinese entrepreneurs are directly reflected in the vibrant tapestry of the current CGT CDMO industry. We can see that the current CGT CDMO sector is not only continuously giving rise to waves of new players, but also witnessing some peculiar industry phenomena—where certain companies act as both “gold diggers” and “water sellers.”

CGT clients, as the service recipients, have begun to worry that the “water sellers” might pry into their “gold-mining” secrets during close interactions. On the other hand, some CDMOs in their early stages of development have not yet fully clarified their future business models and growth paths. While navigating this temporary phase of “uncertainty,” they also face other minor annoyances: calls received by their employees may not be orders but rather poaching attempts from competitors offering three to five times the current salary, or even offers to purchase their company’s procurement lists at high prices. They lament that due to the higher technical barriers and greater scarcity of talent in the CGT industry, competition among the “small fish” in the large CDMO market remains intense.

With the CDMO market so bustling, it is only natural to want to explore it in depth. VCBeat aims to help readers gain a better understanding through this article:

1. How hot is the CGT CDMO market right now?

2. Why Is CGT CDMO Needed? What Are the Intrinsic Drivers of Demand?

3. Is the future market demand for CGT CDMOs sustainable? What is the estimated size of the “pie”?

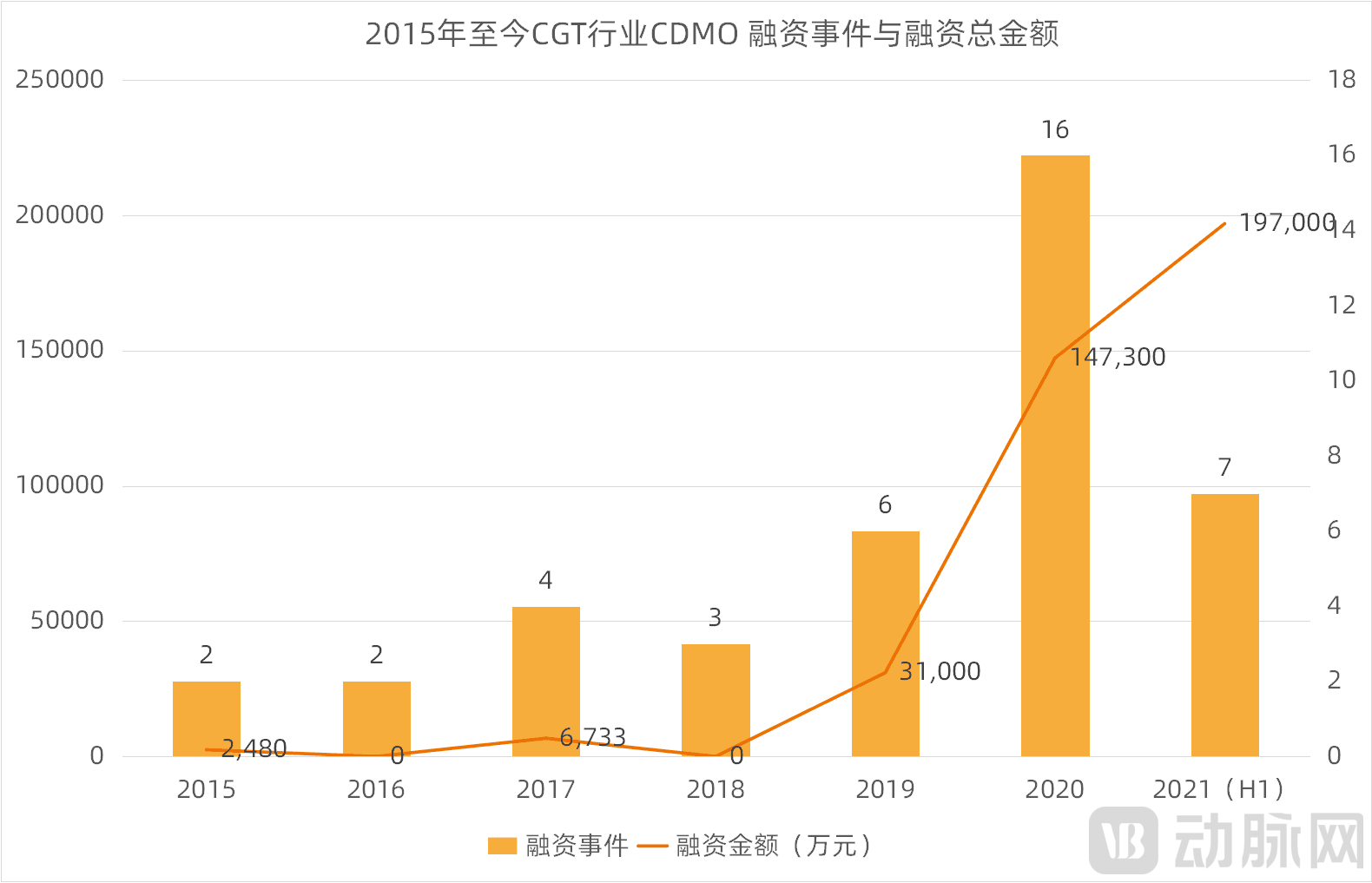

The simplest way to gauge the heat of a market is to understand the willingness of capital markets to pay for it, and the CGT CDMO market is no exception. VCBeat has compiled incomplete statistics and created a chart on the historical financing in the primary market for CGT industry CDMOs since 2015 (when the first financing event for a CGT industry CDMO occurred):

Note: In this statistical analysis, funding amounts for undisclosed financing events are recorded as zero; financing amounts described as "tens of millions of yuan" or "over ten million yuan" are standardized to 10 million yuan; and amounts described as "hundreds of millions of yuan," "over 100 million yuan," or "exceeding 100 million yuan" are standardized to 100 million yuan.

Financing in the Primary Market for CDMOs in the CGT Industry from 2015 to the First Half of 2021

(Data source: VBInsight Database, Tianyancha, Qichacha)

From 2015 to the present, there have been approximately 40 financing events in the CGT CDMO sector, with a total financing amount of around RMB 3.84513 billion. Among the 40 financing events compiled by VCBeat, 17 did not disclose the specific amounts raised; therefore, the total financing figure presented below is likely underestimated.

CGT Industry CDMO Financing Events and Total Financing Amount from 2015 to Present (Chart by VCBeat)

Judging from the trend in related financing events, the number of such events has generally shown a continuous upward trend since the first investment in a CGT CDMO company occurred in 2015. Among them,The Strongest Growth Momentum in 2020—There were 16 CGT CDMO-related financing events in 2020, representing a 166.7% increase compared to the 6 financing events in 2019.

There were seven financing events in the first half of 2021. If the number of financing events in the second half of 2021 remains on par with that of the first half, it would appear that the total number of financing events in 2021 decreased compared to 2020. However, the actual situation is that there were two and five financing events in the first halves of 2019 and 2020, respectively, while the second halves saw four and eleven financing events, respectively. Therefore, we can hypothesize that 2021 may follow a similar pattern to the previous two years. Financing activity in the second half of 2021 may further intensify, ensuring that the overall number of financing events in 2021 continues to show an upward trend.

In terms of financing amount, the total financing in the CGT CDMO sector also saw extremely rapid growth in 2020. The total financing amount in the CGT CDMO sector in 2020 increased by 375.2% compared to the full year of 2019. To date,Although there were only seven financing events in the CGT CDMO sector in the first half of 2021, the total amount raised in these seven deals (RMB 1.97 billion) exceeded the total funding from all 16 financing events throughout the entire year of 2020 (RMB 1.473 billion).

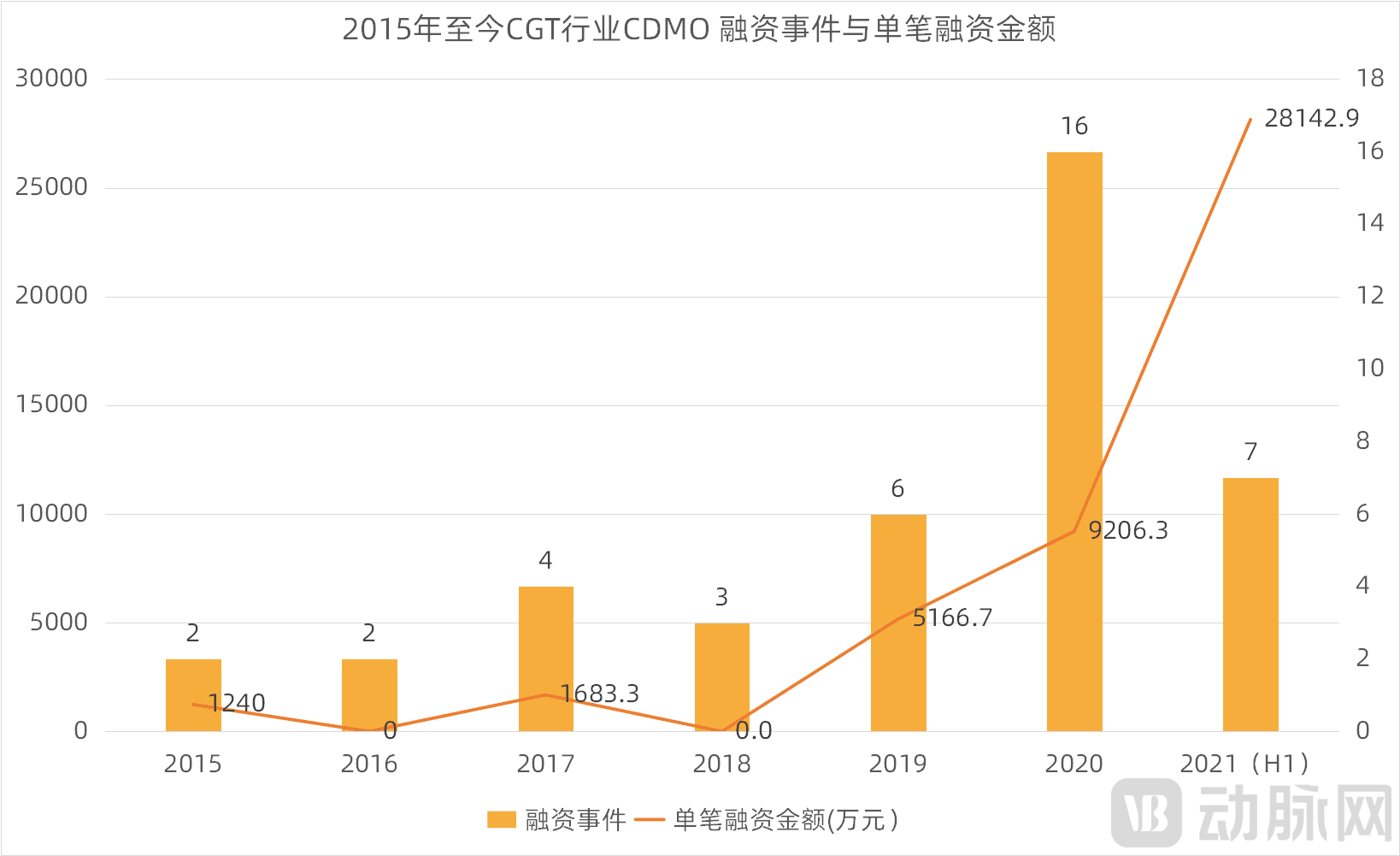

In terms of the average amount per financing transaction annually, there has been a continuous upward trend from 2015 to present. Currently, the first half of 2021 witnessed the most remarkable performance in the average amount per financing transaction annually in the CGT CDMO sector. The average amount per financing transaction annually in the CGT CDMO sector during the first half of 2021 reached RMB 281.43 million, representing a 205.7% increase compared to that of 2020 (RMB 92.06 million).

CGT Industry CDMO Financing Events and Average Annual Financing Amount per Deal, 2015–Present (Chart by VCBeat)

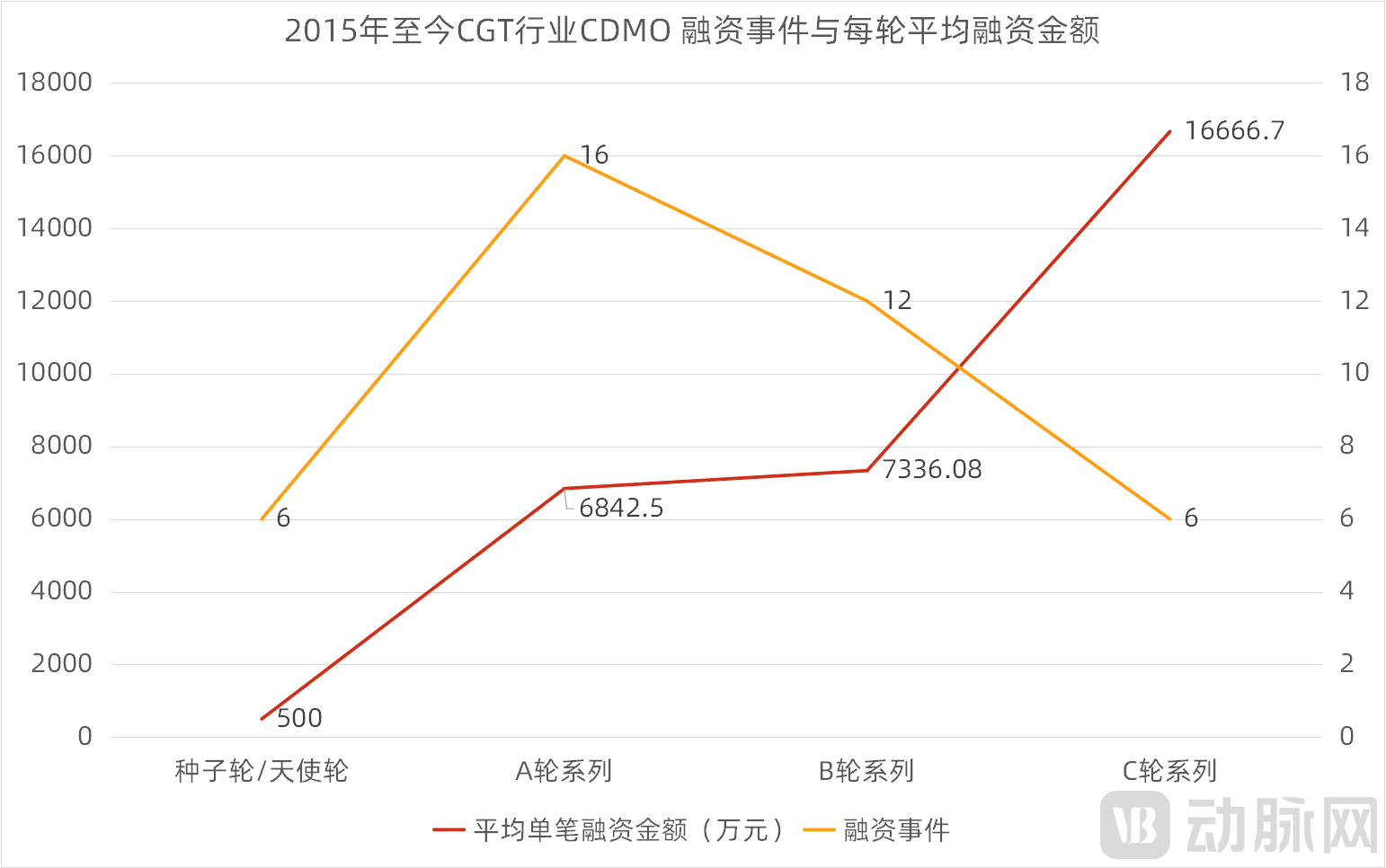

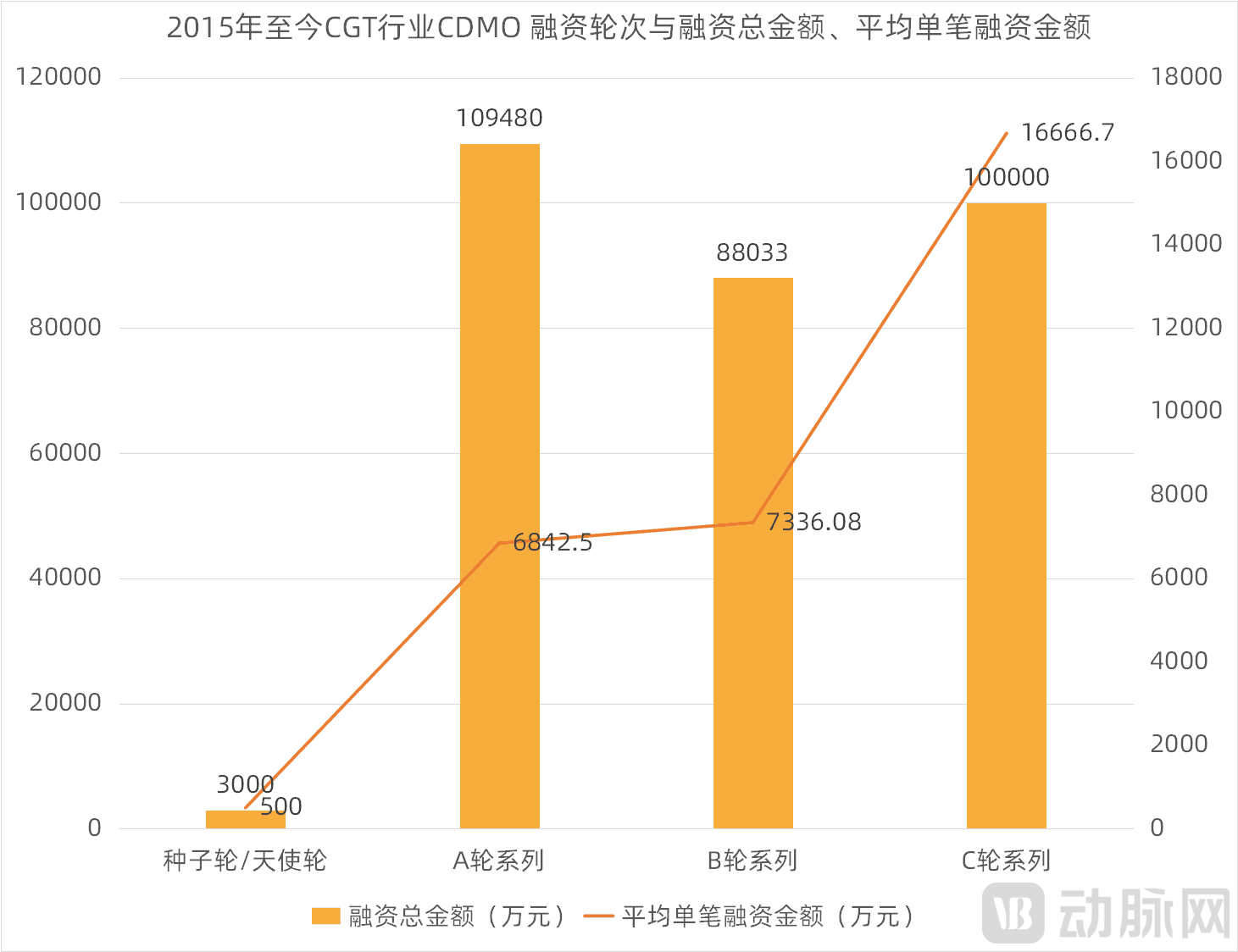

Let us further examine the relationship between financing rounds and funding amounts. From the Seed/Angel round to Series C, there is a positive correlation between the amount raised per transaction and the financing round: as the financing stage advances, the average funding amount per deal increases. Series C deals recorded the highest average funding, with an average of RMB 170 million across six related financing events. The average funding amounts for Series A and Series B were relatively similar, at RMB 68.425 million and RMB 73.3608 million, respectively. The Seed/Angel round had the lowest average funding amount per transaction, at RMB 5 million.

CGT Industry CDMO Financing Events and Average Funding Amount per Round, 2015–Present (Chart by VCBeat)

2015–Present: CGT Industry CDMO Financing Rounds, Total Financing Amount, and Average Single-Round Financing Amount (Chart by VCBeat)

In terms of the correlation between financing rounds and financing events, Series A has seen the highest number of deals since 2015, with 16 transactions; it also recorded the highest total financing amount, approximately RMB 1.09 billion. The number of Series B financing events follows closely behind, totaling 12. Series C ranks second in total financing amount, at approximately RMB 1 billion. The number of Seed/Angel round financing events is on par with that of Series C, with 6 deals each. The Seed/Angel round had the lowest total financing amount, approximately RMB 30 million. In summary, it can be observed that the CGT CDMO sector has gradually transitioned from its initial development stage to a mid-stage mature development phase.

Based on the disclosed text and graphical data above, we can see that the CGT CDMO sector has experienced rapid growth in recent years. This also indicates, to some extent, that market demand for CGT CDMO services is continuing to rise. So, what are the underlying drivers of this market demand?

For startups, deficiencies in funding, team composition, and prior experience are common during the early stages of development. Consequently, entrepreneurs’ primary concern is how to mitigate drug development risks, enhance R&D efficiency, and accelerate pipeline progression to secure financing successfully. Addressing these challenges constitutes the primary motivation for cell and gene therapy (CGT) companies to outsource related operations to contract development and manufacturing organizations (CDMOs).

Several anonymous executives from CGT companies briefly explained to VCBeat their reasons for outsourcing production, which mainly include:

1. Reduce risks and costs in early-stage R&D and manufacturing.For startups, risk control is the top priority. In the early stages of research and development, there are often many uncertainties; high levels of uncertainty lead to significant cost risks. CGT CDMO companies typically maintain large cell or vector libraries, which can help pharmaceutical companies select and optimize suitable cells or vectors, thereby reducing trial-and-error costs and improving the success rate of R&D.

2. Shorten the R&D cycle for enterprises.Due to the high diversity and complexity of viral vectors used in cell and gene therapies, their large-scale manufacturing is not only extremely time-consuming but also requires several years to build the necessary body of expertise. Few startups possess facilities of sufficient scale or the specialized expertise required to manufacture viral vectors for clinical trials.

3. Meet regulatory compliance requirements for product quality and safety.If companies build their own production platforms without sufficient experience and professional expertise, many of the resulting products may fail to meet the regulatory standards. Professional CDMOs, leveraging their robust production platforms and stringent quality control measures, can address corporate concerns regarding product compliance. Thus, a professional CDMO with mature technologies plays a significant role in advancing the research, development, and manufacturing of gene and cell therapies.

Certainly, the aforementioned reasons largely apply to the application scenarios of CXOs in other fields as well. However, CGT CDMOs differ in that the production outsourcing rate in the CGT sector is significantly higher than in other areas, and CGT CDMOs also “outperform” in addressing the continuity of market demand.

According to J.P. Morgan statistics, the outsourcing rate in the CGT CDMO industry is estimated to exceed 65%, whereas the outsourcing rates for small-molecule and large-molecule CDMOs currently hover around 40%. Not only do startups have strong demand for CGT CDMO services, but established CGT R&D companies are also actively seeking professional CDMO support. The prosperity and future prospects of the CGT sector provide substantial growth potential for the continued development of CGT CDMOs.

As mentioned at the beginning of this article, compared with traditional drug development, the CGT industry requires higher R&D investment. Therefore, CGT companies have a strong demand for leveraging professional outsourced R&D and manufacturing teams to reduce costs.

So, what are the reasons behind the high R&D costs in the CGT industry?——One of the primary reasons is the higher R&D and manufacturing requirements for CGT products compared to traditional small-molecule drugs.Gene and cell therapy research was stalled for a long period in the past due to safety concerns. Following the industry's resurgence in recent years, extremely high standards have been imposed on the establishment of Good Manufacturing Practice (GMP) systems to ensure product safety. Consequently, the CGT sector faces far more stringent requirements for research and development and manufacturing than traditional pharmaceuticals.

Taking CAR-T therapy as an example, it possesses numerous characteristics distinct from traditional small-molecule drugs and biologics. It imposes stringent requirements on cell culture and genetic stability, is highly sensitive to the environment, and is susceptible to various factors such as temperature, carbon dioxide concentration, and humidity. As vectors for delivering exogenous genes, viral vectors must simultaneously meet several criteria, including strict control over exogenous gene expression, achievement of sustained and controllable therapeutic effects, target cell specificity, and low toxicity and side effects.

Currently, one of the major bottlenecks in CGT product development isViral vector processes and large-scale GMP manufacturing are characterized by process complexity, capacity shortages, and lengthy production cycles.This also constrains the development of the entire CGT industry and is one of the primary reasons why CGT products are priced at “astronomical” levels.

The production of viral vectors is widely recognized as a major challenge and a key focus for breakthroughs in the cell and gene therapy (CGT) industry, impacting whether CGT companies can successfully transition from small-scale trials to large-scale commercial manufacturing. Dr. Scott Gottlieb, former Commissioner of the U.S. Food and Drug Administration (FDA), stated, “The capacity for industrial-scale mass production of viral vectors is one of the bottlenecks constraining the development of gene therapies.” He further pointed out that approximately 80% of the standard review time for gene therapies is spent on manufacturing and quality issues.

Complex technical mechanisms, high-barrier process development and large-scale manufacturing, stringent regulatory requirements, and limited industrialization experience have made CGT products more reliant on CDMOs than traditional pharmaceuticals.So, how is the sustained superiority of CGT CDMO outsourcing demand over other sectors manifested?

This is reflected in the strong demand for CDMO services from mature cell and gene therapy (CGT) companies. Take Novartis, the multinational pharmaceutical giant that launched the world’s first CAR-T product, as an example. Novartis signed a multi-year contract with Oxford BioMedica, a CDMO company, to supply the viral vectors required for manufacturing its marketed gene therapy product, Kymriah. Similarly, Kite/Gilead, which jointly launched CAR-T products such as Yescarta and Tecartus, has also prominently entered into CDMO outsourcing service agreements.

By outsourcing certain key reagents and non-core excipient products, pharmaceutical companies can focus their efforts on drug R&D and clinical trials, without having to spend additional time establishing GMP-compliant production facilities and other resources.

Beyond the inherent demand for CDMO services from CGT startups and publicly listed companies, another key factor in assessing the sustainability of market demand for CGT CDMOs lies in the future development trends of the CGT industry.

Cell and Gene Therapy (CGT) offers novel therapeutic concepts and modalities for cancer, rare diseases, chronic conditions, and other refractory disorders. It holds the potential for durable, curative effects that conventional drugs may not achieve, raising hopes for complete disease eradication. Consequently, extensive research into CGT has been underway for many years. The sequential regulatory approvals of several CGT products abroad have further galvanized global enthusiasm for CGT product development.

According to data from the Alliance for Regenerative Medicine,In 2020, the number of cell and gene therapy drugs in clinical development reached 1,220, doubling from 631 in 2015.We can directly perceive the explosive growth in the number of research studies within the cell and gene therapy industry. Literature predicts that the number of clinical programs for cell and gene therapy drugs could reach 11,000 by 2026. If this projection is realized, it will signify that both the cell and gene therapy sector and the related contract development and manufacturing organization (CDMO) industry will enter a phase of explosive development.

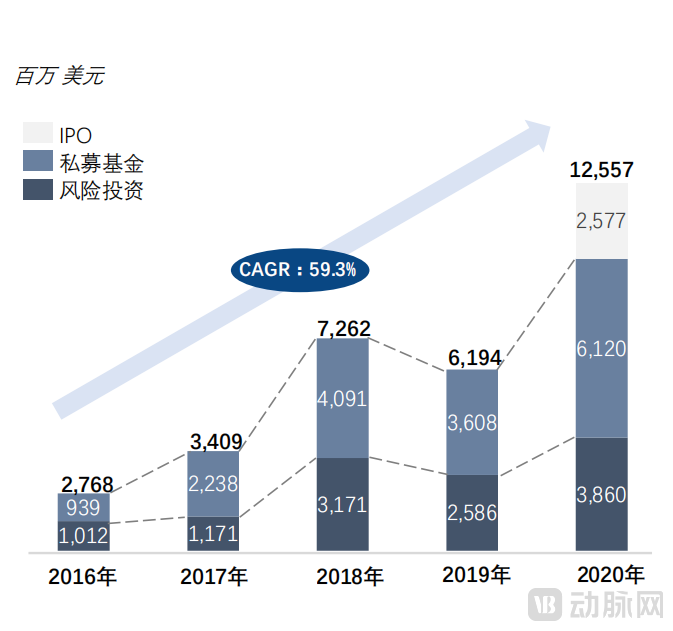

Let’s examine the data on the development of domestic CGT enterprises in China.According to financing transactions in China’s CGT sector, the total amount of funding in 2020 was approximately $12.6 billion, with a compound annual growth rate (CAGR) of 59.3% from 2016 to 2020.IPO and private equity funding amounts increased significantly in 2020. Industry insiders predict that CGT companies will continue this growth momentum in 2021.

2016–2020 Financing Transactions in China’s CGT Sector (Source: Frost & Sullivan, “White Paper on the Development of China’s Cell and Gene Therapy Industry”)

Thus, we can see that the promising growth prospects of the CGT industry provide ample room for future expansion in the CGT CDMO market.

According to Frost & Sullivan data, the market size of cell and gene therapy CMO/CDMO in the United States increased from $500 million in 2016 to $1.1 billion in 2020, with a compound annual growth rate (CAGR) of 23.8%. Similar to the U.S. market, Europe's cell and gene therapy CMO/CDMO market grew rapidly from $300 million in 2016 to $700 million in 2020, with a CAGR of 20.6%.

As CGT-related research and clinical trials expand, Frost & Sullivan estimates thatBy 2025, the global CMO/CDMO market for cell and gene therapy will reach $10.1 billion, with a compound annual growth rate (CAGR) of 34.9% from 2020 to 2025.China’s cell and gene therapy CMO/CDMO market will be the fastest-growing market, with a projected compound annual growth rate (CAGR) of 51.1% from 2020 to 2025.

From this perspective, compared with CGT R&D enterprises that focus on “gold digging,” CGT CDMOs that specialize in “selling water” not only significantly reduce development risks but also boast promising future market prospects. Moreover, teams engaged in the “water-selling” business within the CGT sector are more sought-after than those in other fields, benefiting from greater access to customer resources, stronger customer dependency, and end-to-end demand that spans the entire development lifecycle.

So, in such an alluring market, which “shovel sellers” have already entered the fray? What are the core businesses of each CGT CDMO? How can one understand the specialized services and corresponding capabilities of each CDMO? How are various CGT CDMOs currently performing in the capital markets? Which ones are more favored and cherished by investors? Why has there been an industry phenomenon of business overlap between CGT “gold diggers” and “shovel sellers”? Where will entrepreneurs who remain “torn” at this crossroads ultimately head?

In the following article, VCBeat will provide a systematic overview and analysis of startups in China’s CGT CDMO market. Stay tuned.