HTDK Medical Files for Hong Kong IPO: Is Being a High-Value Medical Device Distributor a Viable Business?

7Month27Recently, Huatang Medical, a global provider of commercialization solutions for medical devices, quietly filed its prospectus with the Hong Kong Stock Exchange. Despite its relatively lengthy corporate positioning, Huatang Medical provided3A rather impressive figure: China’s second-largest cross-border commercial solutions platform for high-value medical devices, the largest domestic commercial solutions platform for imported ophthalmic products, with a market share twice that of its closest competitor.3times.

Clearly, Huatang Medical positions itself as a leading player in a niche market—small yet exquisite. While the specific functions of this sector remain to be discussed, the background of Huatang Medical is already rich with narrative appeal.

Huatang Medical is one of the few cases that have embarked on a new growth trajectory by leveraging post-investment services after being acquired by private equity (PE). Its predecessor was the healthcare business under Dah Chang Yang Hang, a renowned international trading company. In 2018, it was acquired by Warburg Pincus, a top-tier domestic investment bank, and officially renamed Huatang Medical in 2019. The scope of its operations rapidly expanded from primarily health supplement brands to focusing on high-value medical devices. Specifically, from 2018 to 2020, Huatang Medical’s revenue from medical device-related businesses grew from just over RMB 200 million to more than RMB 500 million. In the first five months of 2021 alone, it achieved the same level of medical device revenue as the entire previous year. The proportion of related business in total revenue surged from 28.9% to 71.2%, demonstrating strong vitality.

In early 2018, Xiong Chao, a director at Warburg Pincus, predicted that the sector in which Huatang Medical operates, and even Huatang Medical itself, would become an “invisible champion” in the medical enterprise industry. “Per capita spending on medical devices in China is only one-ninth of that in the United States, and the market is entering a phase of rapid development. Huatang Medical provides market expansion services; it serves as the infrastructure for the medical device market and acts as the ‘hands, feet, and eyes’ for medical device companies.” Based on this rationale, Xiong Chao persuaded his team and Huatang Medical to allow Warburg Pincus to acquire a 100% controlling stake.

Following its acquisition, Warburg Pincus has continuously infused Huatang Medical with healthcare and supply chain resources, driving the standardization and digitalization of business processes. The team, composed largely (90%) of former personnel from DKSH’s Healthcare division, quickly adapted to the new operational rhythm and rapidly emerged as a leader in its niche segment. According to the prospectus, Huatang Medical currently serves 28 brand partners, including Alcon, MicroVention, Illumina, Smith & Nephew, Roche, Abbott, and Procter & Gamble (Clearblue). Its primary service model is distribution, with agency products covering high-value medical devices across multiple specialties, such as ophthalmology, in vitro diagnostics, orthopedics, cardiology, neurology, maternal health, vascular surgery, endocrinology, and respiratory care. Prior to this IPO, Huatang Medical divested its health supplement operations to focus exclusively on commercial solutions for high-value medical devices.

A closer look at the business reveals that Huatang Medical carved out a path from the cracks by adopting an aggressive, high-profile strategy.

Huatang Medical focuses on high-value medical devices with higher barriers to entry. High-value medical devices require localized teams to possess highly specialized handling and care capabilities, are subject to stricter regulatory oversight, sometimes contain hazardous substances, and demand more rigorous environmental controls—such as temperature, humidity, and cleanliness—during storage and transportation. When entering clinical settings, high-value medical devices typically require the configuration of kits or sets with varying sales attributes, tailored to different patient conditions, physician preferences, and operational needs, rather than being provided as standardized single items. All of these factors pose greater challenges to the compliance and professional capabilities of commercial solution providers.

Meanwhile, given that high-value medical device companies typically represent only a portion of multinational brands’ product portfolios, it is difficult for these multinationals—during the early stages of commercialization when they lack familiarity with Chinese regulations and policies, are unaccustomed to communicating with government authorities, and have limited in-depth understanding of the domestic market—to formulate appropriate strategies for distributor management, selection of supply chain warehousing and transportation service providers, and engagement with local sales channels. Furthermore, for multinational brands, internalizing commercial operations results in low efficiency and poor cost-effectiveness. Merely establishing an in-house commercial operations team with both medical expertise and commercial operational experience entails substantial resource consumption. When considering the procedural aspects of daily operations, liaison, and oversight within the vast organizational structures of multinational corporations, the workload generated by cross-border commercialization is disproportionate to the returns. Huatang Medical’s commercial solutions have rapidly captured market share by addressing users’ critical needs.

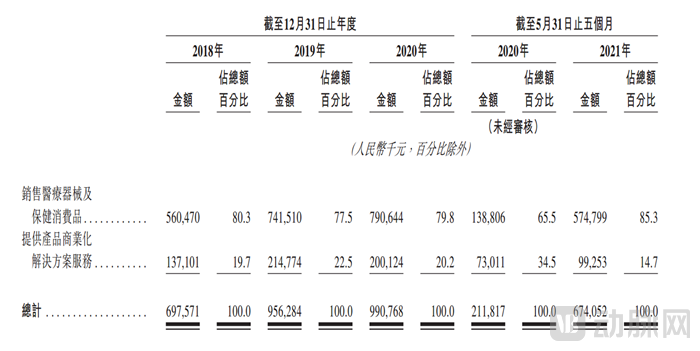

In fact, the globally focused provider of commercialization solutions for high-value medical devices (hereinafter referred to as the “Commercial Solutions Provider”), whose full title is somewhat cumbersome to read, is essentially a primary distributor for cross-border brands. This is evident from its financial data: at present, Huatang Medical’s primary revenue stream stems from acting as the domestic general agent for brand owners, purchasing goods to build inventory, and reselling them to secondary distributors, healthcare institutions, pharmacies, and other channels, with revenue recognized upon collection of payments following product sales.

Huatang Medical Revenue Data (Source: Prospectus)

According to the prospectus, since 2018, excluding the brief period of global trade stagnation caused by the COVID-19 pandemic, the revenue from medical device and healthcare consumer product sales has consistently accounted for approximately 80% of Huatang Medical’s total revenue, with an even higher proportion observed in the first five months of 2021. This indicates that Huatang Medical’s aggressive growth strategy still relies on support from its traditional business model.

Broadly speaking, this is a niche sector long dominated by industry giants. National leaders in medical device distribution, such as Jointown Medical Device, Sinopharm Medical Device, and Guoke Hengtai, have all established their presence here, securing national general agency rights for multiple multinational brands. Meanwhile, lower-tier markets are controlled by regional leaders that focus on differentiated strategies.

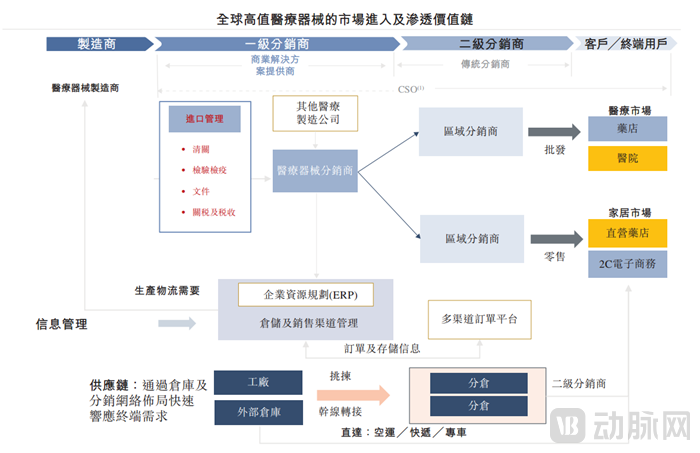

Diagram of Cross-Border Circulation of Medical Devices (Source: Prospectus)

However, Huatang Medical chose to enter a niche, high-quality market. In the early stages of its business transformation, Huatang Medical focused on upstream operations. Its commercial solutions served cross-border brand owners and extended to secondary distributors, but it rarely engaged in on-site marketing activities or communicated directly with hospitals and pharmacies. In other words, since this segment of the cross-border medical device distribution chain does not involve establishing offline stores or online sales platforms, nor does it require building an in-house medical team to develop hospital-based resources, Huatang Medical entered the asset-light segment driven by service capabilities.

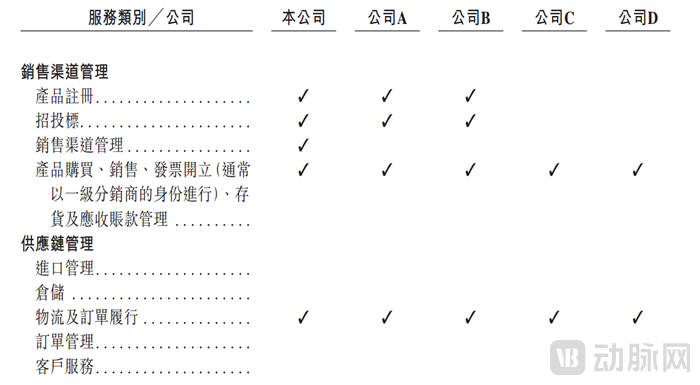

Comparison of Business Layouts Among Industry Peers (Source: Prospectus)

As previously mentioned, Huatang Medical originated from the healthcare division of Jebsen & Co., which had already achieved annual revenues in the hundreds of millions of yuan and established long-term, stable relationships with client brands. In deciding to acquire Huatang Medical, Warburg Pincus primarily valued its capability to serve multinational medical device companies, thereby providing a solid foundation for Huatang Medical’s core business logic.

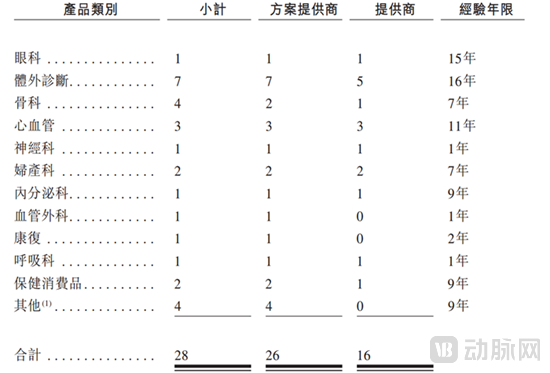

Huatang Medical Specialty Coverage (Source: Prospectus)

As of the filing of the prospectus, Huatang Medical had become the national general distributor in China for 26 imported medical device products, covering ophthalmology, in vitro diagnostics (IVD), orthopedics, and other fields, among which it held exclusive general distribution rights for 16 products.

As previously mentioned, Huatang Medical was founded by an international trading company. Transforming its cross-border enterprise service capabilities—rooted in trade—into commercial solutions for medical devices is no easy feat. Therefore, the transformation of Huatang Medical’s fate under Warburg Pincus involves not only a new business narrative but also fundamental changes to its core operations. This may well be the most critical factor in how private equity reshaped Huatang Medical’s destiny.

In the view of Lin Zhihong, Senior Vice President of Post-Investment Management at Warburg Pincus, this process is akin to a complete physiological reconstruction, requiring the sequential replacement of aged organs without disrupting the patient’s daily life. “Therefore, which organ to replace first, how to incise and anastomose the blood vessels—all these steps must be meticulously planned and repeatedly verified. Any error in detail could have significant consequences.”

Warburg Pincus chose to start with informatization, logistics, and warehousing, gradually helping Huatang Medical build end-to-end solution capabilities.

Huatang Medical’s clients are large medical device manufacturers from the United States and Europe, which are subject to stringent compliance requirements. Consequently, there is a strong demand for building comprehensive information systems to support a series of business processes, including order management, warehousing, sales, service, channel management, and e-commerce. In this process, Warburg Pincus assisted Huatang Medical in clarifying its development strategy and redefining the implementation roadmap for each module of its information systems. As of the filing of its prospectus, Huatang Medical had launched and operationalized multiple efficiency-oriented systems, fully integrating data across order processing, warehousing, transportation, sales, and distribution. This integration has enabled information sharing between upstream and downstream entities within the system and facilitated the introduction of business intelligence analytics.

As part of the extension of its business chain, Warburg Pincus assisted Huatang Medical in establishing logistics and distribution infrastructure across China. This infrastructure provides specialized warehousing services tailored to the needs of different categories of medical devices, while integrating professional transportation systems—such as cold-chain packaging materials and temperature control—to connect logistics centers with first- and second-tier cities nationwide. According to the prospectus, Huatang Medical operates eight warehouses in Shanghai, Beijing, and Guangzhou capable of storing various product categories. Its transportation network covers nearly 3,000 counties across China, enabling next-day delivery for certain orders.

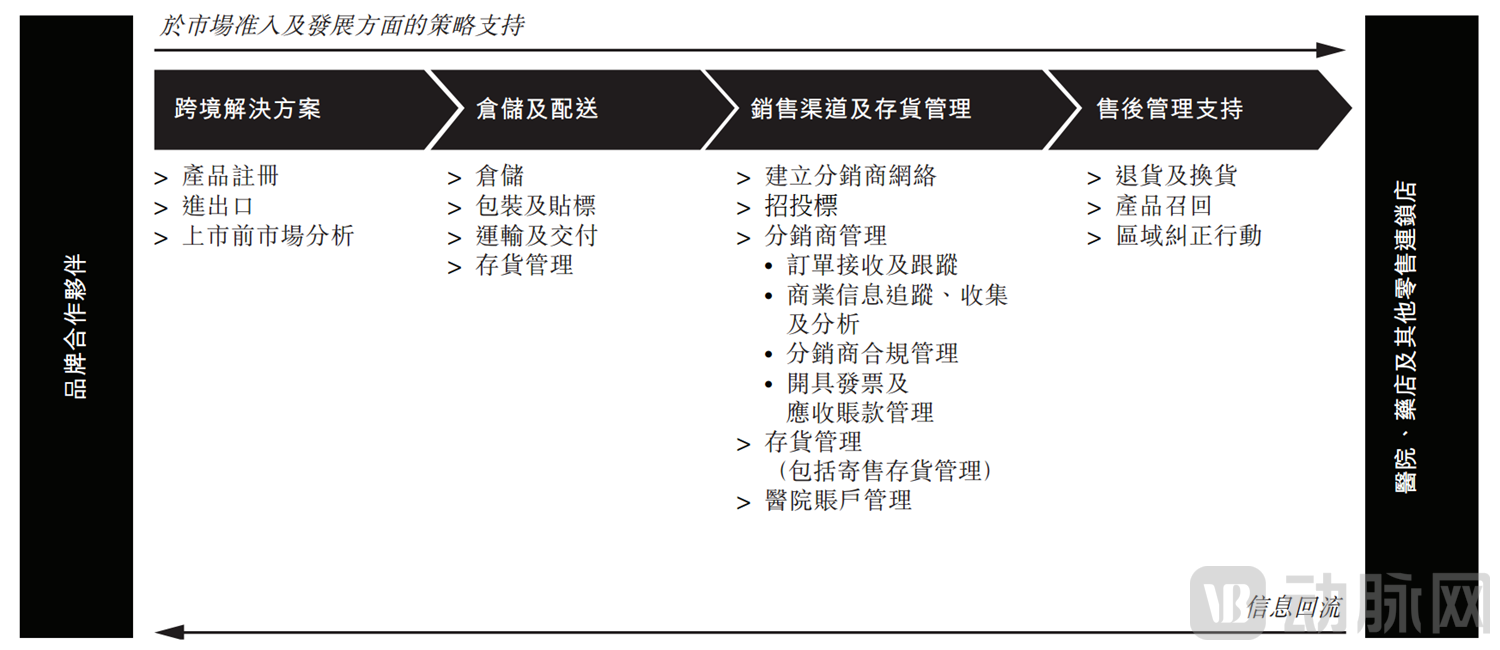

Thus, Huatang Medical has established a comprehensive framework that connects every stage from the commercialization of medical devices to their final implementation. According to the prospectus, Huatang Medical can tailor solutions to meet the needs of its brand partners by combining services from its portfolio, which includes cross-border solutions, warehousing and distribution, sales channel and inventory management, and after-sales support.

Business Modules Provided by Huatang Medical (Source: Prospectus)

For example, Illumina’s gene sequencing platform received its initial medical device registration certificate in 2018 and established a dedicated logistics center in the Shanghai Waigaoqiao Free Trade Zone. Huatang Medical served as its primary commercial solutions provider, designing and providing cold rooms, refrigerated rooms, and controlled ambient temperature facilities for Illumina, while also handling product importation, inbound processing, warehousing, and distribution, thereby rapidly expanding its business presence to multiple cities across China. Subsequently, the domestic distribution of Illumina’s sequencing platforms and diagnostic reagents has repeatedly leveraged Huatang Medical’s services, including warehousing, transportation and delivery, and inventory management.

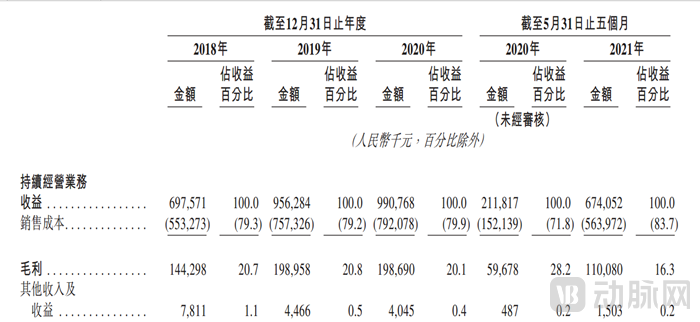

It is evident that Huatang Medical experienced a notable surge in development after Warburg Pincus took control. Although focused on niche, high-quality segments, its annual revenue of nearly RMB 1 billion pales in comparison to the hundreds of billions generated by Jointown Pharmaceutical’s medical device division, and even falls significantly short of Guoke Hengtai’s tens-of-billions level. Nevertheless, its gross profit margin of approximately 20% remains an achievement that many medical device distribution companies struggle to attain.

Huatang Medical Financial Data (Source: Prospectus)

So, is a business solution anchored by the general distributor model a good business? The answer requires a longer time horizon to assess.

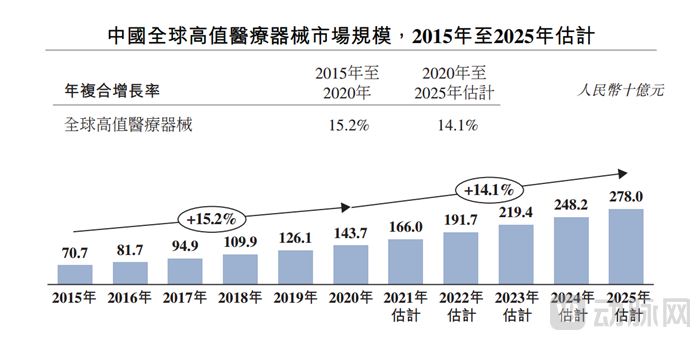

First, amid the rapid growth of the medical device market, this business model has created substantial value and driven its own development. From 2015 to 2020, the market size of high-value medical devices in China maintained a robust annual growth rate of 19.6%, expanding from RMB 105.3 billion to RMB 257.5 billion. Among these, high-value medical devices from global brands have consistently held a significant market share, growing from RMB 70.7 billion in 2015 to RMB 143.7 billion in 2020.

National Trends in the High-Value Medical Device Market (Source: Prospectus)

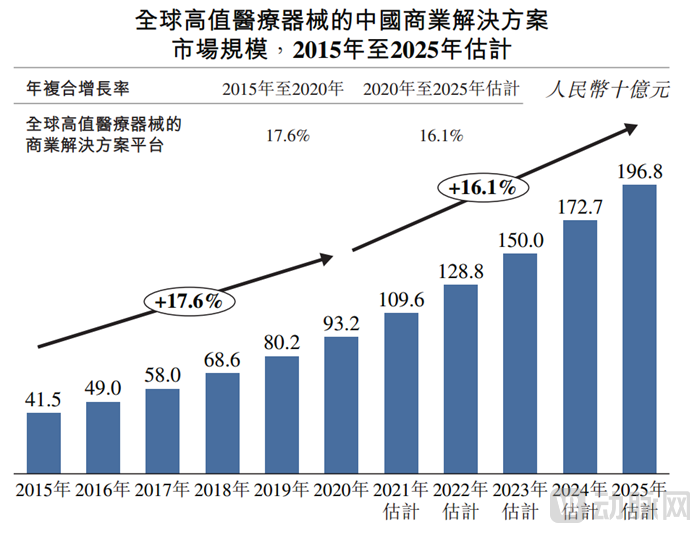

Driven by the compounding effects of an aging population, consumption upgrades, heightened healthcare awareness, and the continuous development of innovative medical devices, coupled with the innovation spurred by domestic medical device reforms, China’s medical device market is highly likely to sustain growth for a period, steadily narrowing the gap with overseas markets in terms of the pharmaceutical-to-medical-device ratio. In this process, the global market for commercial solutions for high-value medical devices has also flourished, reaching a total size of RMB 93.2 billion in 2020, and is projected to maintain a rapid growth rate of 16.1% through 2025.

China's Commercial Market Trends for High-Value Medical Devices (Source: Prospectus)

However, the other side of the coin to growth driven by medical devices is the weak independent growth capability of the general agency industry. Once the growth of medical devices slows down, or if market acceptance of innovative medical devices declines—as seen with Huatang Medical—business growth could be adversely affected.

Furthermore, for the general distributor of medical devices, distribution policies remain a Sword of Damocles constantly hanging overhead.

First is the Two-Invoice System. Following its implementation in pharmaceutical distribution, certain provinces and municipalities in China have begun piloting the “Two-Invoice System” for medical devices, which requires that one invoice be issued by the manufacturer to the distributor and a second invoice be issued by the distributor to the healthcare institution. On July 19, 2019, the General Office of the State Council released the Notice on Issuing the Reform Plan for Governing High-Value Medical Consumables, encouraging local governments to implement the “Two-Invoice System” based on local conditions to reduce resales of high-value medical consumables and enhance transparency in procurement and sales. As many general distributors conduct their business through sales to other distributors, the “Two-Invoice System” may necessitate adjustments to their business models, which will undoubtedly impact business growth.

Meanwhile, following the 2019 reform proposal that advocated exploring the classification and centralized procurement of high-value medical consumables based on the principles of volume-based procurement, price-volume linkage, and fostering market competition, a number of high-demand high-value medical consumables have already been incorporated into the volume-based procurement system. This development poses a challenge to all manufacturers and distributors of medical devices. Since the vast majority of medical device applications occur within hospitals, failing to win bids in the public tendering process for centralized procurement—while competitors secure contracts with lower prices and sufficient production capacity—effectively means being forced to abandon the market for a specific product. For certain teams within general distributors, this product line often represents their lifeline.

It is thus evident that the general agency model, as a business paradigm with extremely high long-term risk, functions more as a strategic tool than a standalone business. Once this tool has been leveraged to gain market access, it becomes imperative to introduce richer operational substance. This also helps explain why Guoke Hengtai, despite its sustained performance growth, has faced criticism for lacking self-sustaining profitability.

Just as Jointown Medical Devices continuously expands its business boundaries toward the consumer end, and Guoke Hengtai focuses on building in-hospital service capabilities, leading general distributors are also attempting to break away from single-model operations in pursuit of incremental growth. According to the prospectus, Huatang Medical has chosen to further strengthen its front-end capabilities, focusing on scaling up the early commercialization of cross-border innovative branded medical devices while exploring licensing-in opportunities from companies listed directly overseas. Being a general distributor is the starting point of the story, but long-term, stable performance growth requires core businesses that are more closely aligned with clinical details.