Giants Enter and Startups Sprint: Which of the 16 CGT CDMOs Will Reach the Finish Line First? — Part II of the CGT CDMO Industry Review

Since 2017, the cell and gene therapy (CGT) industry has continued to achieve breakthrough progress. Milestone CGT products such as Kymriah, Luxturna, and Zolgensma have successively received FDA approval for market launch, while investment and financing in related fields have remained robust. Currently, the CGT industry has become one of the most promising global frontier sectors in pharmaceuticals.

China is closely aligning its strategic layout in this frontier field with international developments. Since 2015, the number of clinical trials related to cell and gene therapy (CGT) in China has grown rapidly. Under a series of intensively conducted studies, the research achievements of China’s first generation of cell and gene therapy companies have gradually been translated into practical applications, leading industry insiders to widely refer to 2021 as the “Year of Cell and Gene Therapy.”

The booming CGT market has not only attracted a wave of “gold diggers”—with CGT R&D companies springing up like mushrooms—but also quietly ushered in a golden age for the “water sellers,” namely CGT CDMOs.

However, due to the complex technical mechanisms underlying product research in the cell and gene therapy (CGT) industry, high barriers to process development and large-scale manufacturing, stringent regulatory requirements, and limited industrialization experience, the CGT sector relies more heavily on contract development and manufacturing organizations (CDMOs) than traditional pharmaceuticals, with more sustained demand. The continued boom and promising outlook of the CGT industry have further fueled the market growth of CGT CDMOs.

Due to the rapid growth of the industry and the limited number of companies, gene therapy CDMOs are currently experiencing a supply shortage.The CGT CDMO market resembles an untapped blue ocean, attracting countless elite talents to enter the field. Everyone is eager to be the first to discover the great treasure hidden beneath this blue ocean. Consequently, industry giants are strategically positioning themselves, while startups are racing to expand, making the current CGT CDMO sector remarkably vibrant.

Meanwhile, a large cohort of Chinese entrepreneurs finds themselves at a crossroads, grappling with a strategic dilemma: should they join the high-risk, high-reward “gold rush” in cell and gene therapy (CGT), or opt for the “water-selling” model of CGT contract development and manufacturing organizations (CDMOs)—a sector that is currently in an earlier stage of development, carries lower risk, and holds considerable promise? We sense the hesitation and uncertainty among these entrepreneurs. The current CGT CDMO landscape is not only witnessing a continuous influx of new players but also exhibiting some peculiar industry phenomena—where certain companies act as both “gold diggers” and “water sellers.”

CGT clients, as the service recipients, are growing concerned that “shovel sellers” may pry into their “gold-mining” secrets during close interactions. On the other hand, some CDMOs in the early stages of development have not yet fully clarified their future business models and development paths.

“Nearly $4 Billion Injected! How Did Gene and Cell Therapy CDMOs Become So Hot? — A Review of the CGT CDMO Industry (Part I)”In this article, VCBeat systematically reviews and analyzes the historical financing landscape of the primary market for CGT CDMOs since 2015, when the first financing event in the CGT CDMO sector occurred. The article also identifies the internal and external drivers fueling the sustained growth of the CGT CDMO market, and explores issues such as the sustainability of future market demand and estimates of the total addressable market.

In this article, VCBeat will continue to focus on the topic of CGT CDMOs, striving to answer the following questions:

1. Who are the current players in China’s CGT CDMO market? How is each CGT CDMO performing in the capital markets? Which companies are more “favored” and “cherished” by investors?

2. Why Is There an Industry Phenomenon of Business Overlap Between CGT “Gold Diggers” and CDMOs as “Water Sellers”? Where Will Entrepreneurs Who Are Still “Hesitant” at the Crossroads Ultimately Go?

3. What are the core businesses of each CGT CDMO? What are their respective production capacities? Through which key indicators can the specialized services and corresponding capabilities of each CDMO be demonstrated?

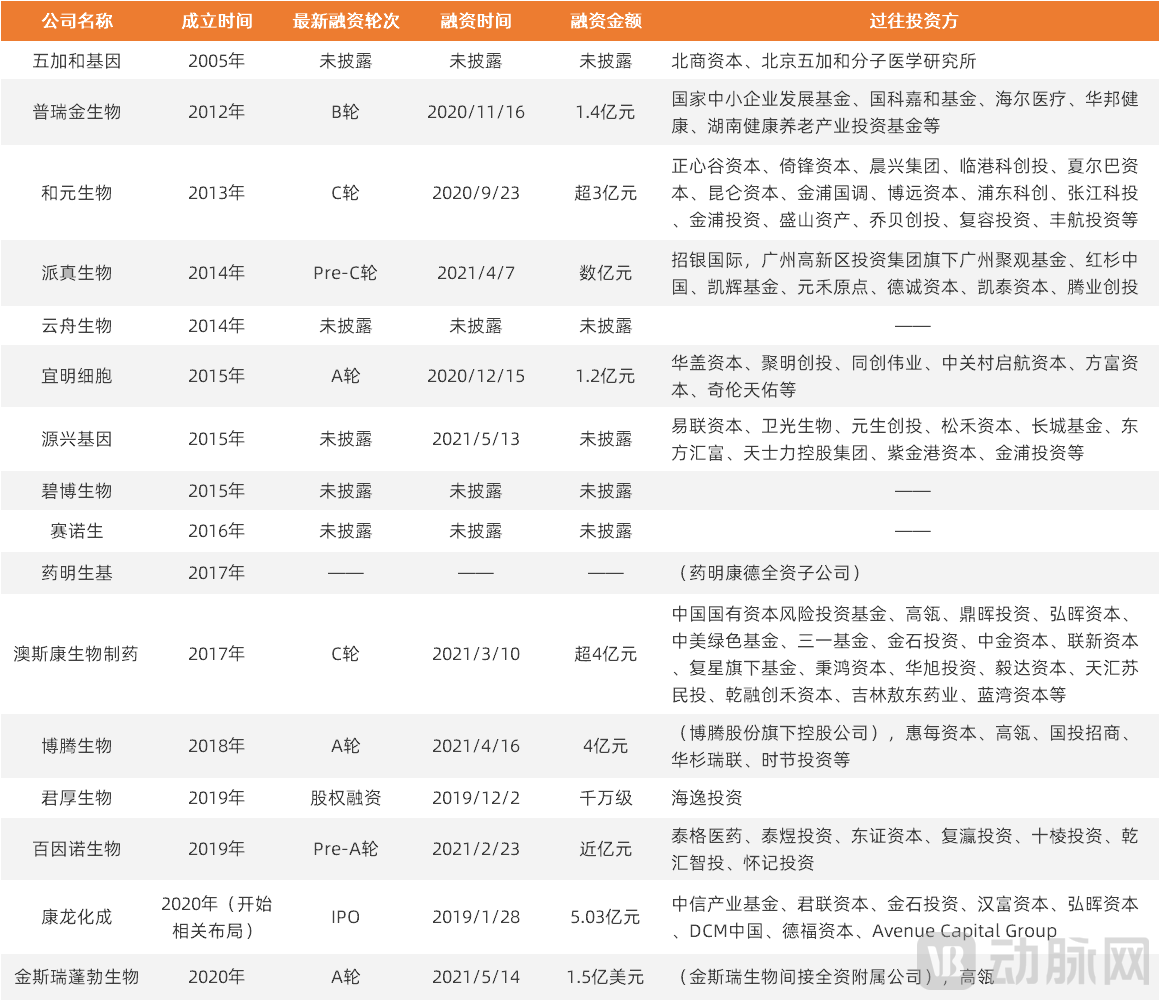

According to incomplete statistics from VCBeat, there are currently 16 companies in China’s CGT sector primarily engaged in CDMO services. To gain insight into the latest performance of these CGT CDMOs in the capital market, VCBeat has compiled and analyzed their most recent financing activities, as detailed below:

Overview of the Latest Financing Rounds for CGT CDMOs in China

(The above are listed in order of company establishment date; sources: VCBeat, Tianyancha, Qichacha)

Based on the information in the table above, we found that,Among companies that have publicly disclosed their financing information, the majority of CGT CDMOs secured their latest round of funding at the level of hundreds of millions of yuan.This partly explains the booming CGT CDMO market and investors' optimism about this sector.

GenScript ProBio secured the largest financing amount, totaling $150 million (equivalent to RMB 970 million). Other significant financing rounds include those of Auscan Biopharma (over RMB 400 million), Porton Biologics (RMB 400 million), GenScript BioServices (over RMB 300 million), Puruijin Biotech (RMB 140 million), IMMUNE CELL (RMB 120 million), PackGene Biotech (tens of millions of RMB), and Baizinuo Biotech (nearly RMB 100 million).

From the perspective of the latest financing rounds of various companies,Currently, the largest number of companies are in Series A financing.Including IMMUNE CELL, Porton Biologics, Baizhinuo Biotech, and GenScript ProBio. Obio Technology, PackGene Biotech, and Auscan Biopharma are currently in the Series C financing stage.

From the perspective of past investors in various CGT CDMOs, we can observe that,A wide variety of institutions have invested in the CGT CDMO sector, but few have adopted a multi-company investment strategy within this space.This may be because the CGT CDMO sector is still in a relatively early stage of development. In the absence of established standards and metrics to assess the strength and future prospects of individual companies, investment institutions employ varying criteria to evaluate the CGT CDMO enterprises they favor. Nevertheless, it is evident that the capital market demonstrates high overall participation and strong enthusiasm for investing in the CGT CDMO sector.

Why Do CGT “Gold Diggers” and “Water Sellers” Have Overlapping Businesses?

Where Will Entrepreneurs Still “Hesitating” at the Crossroads Ultimately Head?

At the beginning of this article, we mentioned that there is a phenomenon in the current CGT CDMO industry:Some companies are simultaneously developing CGT-related products and undertaking CDMO services.Many readers are likely puzzled by this phenomenon, and CGT companies, as the service recipients, also harbor certain concerns about the current situation. What lies behind the overlap between the businesses of the “gold diggers” and the “water sellers”?

By analyzing the growth trajectories and development histories of the current cohort of CDMO enterprises in China, we may uncover partial answers to this question. Currently, CDMOs in China’s CGT sector primarily originate from three categories.

Traditional CXOs’ Cross-Border Expansion into the CGT CDMO Sector

Such enterprises oftenWith substantial capital, an international resource team, and relatively comprehensive hardware platforms and service systems, it primarily enters the CGT CDMO sector through mergers, acquisitions, and investments, while simultaneously strengthening its capabilities by enhancing international cooperation and recruiting top-tier global talent.Representative companies in this category mainly include WuXi AppTec, Pharmaron, and Porton Pharma.

1. WuXi Advanced Therapies

In 2017, WuXi Advanced Therapies was established as a wholly-owned subsidiary of WuXi AppTec, the CXO giant, dedicated to developing its CGT CTDMO business. To further enhance the subsidiary’s capabilities, WuXi AppTec provided comprehensive support in technology, talent, and capacity building through various strategies, including investments, mergers and acquisitions, and equity stakes in CGT companies.

March 2, 2021,WuXi AppTec Announces Completion of Acquisition of UK Gene Therapy Technology Company OXGENE,Further expand WuXi AppTec’s footprint in the CGT CDMO business; OXGENE will retain its original name and become WuXi Advanced Therapies’ first R&D and production base in Europe. In addition, WuXi AppTec has acquired stakes in or invested in several CGT companies in recent years, including JW Cayman, Lyell, and VIGeneron, which are expected to help drive client referrals to WuXi Advanced Therapies in the future.

As can be seen, WuXi AppTec achieved strong performance in the CGT CDMO sector in 2020. According to its annual report, WuXi AppTec assisted multiple clients in China with CGT CTDMO services in 2020, supporting two Phase II/III clinical trial projects. In its U.S. laboratory services segment (primarily comprising CGT CTDMO services and medical device testing services), the company generated revenue exceeding RMB 1.5 billion and provided CTDMO services for a total of 36 clinical-stage CGT projects. Although WuXi Advanced Therapies boasts substantial backing, unquestionable professional expertise, and a solid industry reputation, the presence of JW Therapeutics may still raise some concerns among certain CGT clients.

2. Pharmaron

In 2020, Pharmaron began to lay out its CGT CDMO business, mainly through acquisitions. Currently, it has not yet completed the construction of its related production facilities in China.

On November 9, 2020, Pharmaron announced the acquisition of the U.S. company Absorption Systems for $137.5 million., Absorption’s business primarily focuses on providing non-clinical in vitro and in vivo laboratory analyses, biological testing, and animal testing services for the CGT industry.On March 1 this year, Pharmaron announced another new move:Acquisition of Allergan Biologics Limited, an AbbVie subsidiary based in Liverpool, UK, with plans to transition Allergan from its role as an internal R&D center within the AbbVie Group to a provider of CGT CDMO services for third-party clients through a period of business integration. The significant acquisition of Absorption and Allergan has yielded pronounced synergies, enabling Pharmaron to achieve a comprehensive layout across the entire preclinical research and CDMO value chain in the CGT sector following the integration.

Can Pharmaron Successfully Achieve a “Come-from-Behind” Victory by Rapidly Expanding Its CGT CDMO Portfolio Through an Aggressive M&A Strategy to Acquire Advanced Technologies from Established Foreign Companies?

3. Porton Biologics Ltd.

Suzhou Porton Biologics, established in 2018, is a subsidiary of Porton Pharma Solutions, a leading domestic CXO company, and focuses on CGT CDMO services. Similar to the aforementioned two companies, Porton Biologics has a relatively short history; however, by leveraging the advanced experience of its listed parent company, Porton Pharma Solutions, it has achieved rapid growth. In 2020, Porton Biologics secured gene therapy CDMO orders worth approximately RMB 56 million.

To further enhance its operational capabilities, Porton Biologics Ltd. introduced in December 2020Sander van Deventer, Co-founder and Chief Scientific Officer of UniQure.Sander is the lead developer of the world’s first FDA-approved TNF-targeting chimeric monoclonal antibody and Glybera, the first approved gene therapy drug. In public interviews, Sander stated that in addition to developing new gene therapies, he was personally involved in building uniQure’s internal gene therapy manufacturing facilities. This hands-on experience can provide strong support for Porton Biologics’ CDMO business.

The Transformation/Business Layout of the Earliest Batch of CGT Companies into CDMOs

Currently,The CGT industry is developing at a rapid pace, but inevitable issues such as crowded therapeutic areas and clustered target research have emerged. While the innovative drug R&D sector offers high returns, it also faces high risks and substantial investment requirements.Therefore,Some of the earliest CGT companies have begun to leverage their experience and process platform expertise in early-stage R&D and manufacturing of CGT products to strategically transition into CDMO services.

This category of enterprises primarily includes GenScript ProBio, Puruijin Biologics, Sainoson, and Wujiahe Gene, among others. These companies are typical representatives within the industry that engage in both CDMO services and independent R&D activities. This section will take GenScript ProBio as an example for detailed introduction.

GenScript ProBio, a subsidiary of GenScript Biotech, originated from GenScript’s Biologics Development Business Unit (BDBU), which was established in January 2019. In 2020, GenScript officially launched the independent GenScript ProBio brand to enter the CDMO sector. In the field of gene and cell therapy, ProBio provides comprehensive solutions covering plasmid and viral vector production across all stages, including non-registration clinical trials, process development, registration-enabling clinical trials, and commercial manufacturing.

With Nanjing Legend Biotech as its “living” showcase, GenScript’s capabilities in CGT CMC processes are naturally compelling. The impressive performance of cilta-cel directly reflects GenScript Biologics’ proficiency in CGT CMC manufacturing. Should cilta-cel receive regulatory approval in the future, its commercial-scale production will most likely be undertaken by GenScript ProBio.

Furthermore, we can directly assess GenScript Biotech’s capabilities in the CGT CDMO business through the performance of its subsidiary, ProBio. In 2020, ProBio generated $6.2 million in CGT CDMO revenue, adding a total of 29 preclinical projects, 14 CMC (Chemical Manufacturing and Control) projects, and 14 clinical-stage projects. These included projects from multiple mRNA vaccine developers, with its client base covering nearly all mRNA vaccine R&D companies in China.

Mature production experience and process platforms, backed by robust resource empowerment, constitute the competitive advantages of this category of CGT CDMOs. Capital markets have shown strong enthusiasm for such enterprises. Notably, the largest financing round in the CGT CDMO sector to date ($150 million) was secured by GenScript ProBio.

Among other companies of this type not discussed in detail, it is also possible that some CGT enterprises have no intention of undergoing transformation.These companies engage in CDMO services solely to make effective use of their heavily invested industrial-scale R&D and manufacturing platforms, while generating a certain level of cash flow to support the development of their cell and gene therapy (CGT) products.

A Startup CGT CDMO Independently Established by Domestic and Overseas Talents

This type of CGT CDMO mainly originates fromA CDMO company built by a large cohort of academic and industry professionals, both homegrown in China and returned from overseas studies, leveraging their technology, resources, and teams.Representative companies include Obio Technology, PackGene, Vigene Biosciences, IMMUNE CELL, Yuanxing Gene, BOC Sciences, OSC Biopharmaceuticals, Junhou Biotechnology, and Baiyinuo Biotechnology.

Leveraging their years of accumulated research achievements in the field of cell and gene therapy (CGT) and extensive experience in industrial-scale manufacturing, these companies have established themselves as independent entities, riding the early wave of CGT contract development and manufacturing organization (CDMO) development in China with remarkable momentum. Although they may not have the strong “capital backing” enjoyed by companies such as WuXi Advanced Therapies, Pharmaron, and Porton Biologics, they have attracted significant attention and investment from numerous domestic and international venture capital firms. Indeed, the majority of investment activities in the CGT CDMO sector have been concentrated among these enterprises. Notably, Obio Technology, a leading domestic producer of oncolytic viruses, is preparing to go public on the secondary market. According to publicly available information,On June 8, 2021, the review status of Obio Technology’s application for listing on the STAR Market was updated to “Accepted.”

Founded in 2013, Obio Technology specializes in providing integrated CRO/CDMO services for gene therapy, encompassing lead research and drug development for products such as recombinant viral vectors, oncolytic viruses, and CAR-T therapies. Its business scope covers gene therapy vector construction, target identification and efficacy studies, process development and testing, IND-enabling CMC pharmaceutical studies, GMP manufacturing for Phase I–III clinical trials, and commercial production. In terms of performance (as of the date of signing the prospectus), Obio Technology has accumulated over 90 CDMO projects, with more than 50 currently in execution, covering both pre-IND and post-IND stages. Its key clients include Shenzhen ImmuneOnco, Shanghai Funuo Jiankang, Kanghua Biological, and Jima Biotechnology.

In addition to companies like Obio Technology, which expanded from providing research-oriented services into the CDMO sector, a small number of firms in this category also operate under a model that combines in-house development of CGT products with CDMO services.The reasons for this situation include these companies’ desire to effectively leverage their heavily invested industrialized R&D and manufacturing platforms, while generating certain cash flows to fund the development of their own cell and gene therapy (CGT) products; or, alternatively, their uncertainty regarding long-term strategic positioning, leading them to temporarily “waver” between the two business models of CGT-focused biotech firms and CGT contract development and manufacturing organizations (CDMOs), thus remaining in an early stage of “exploration.”

However, we can also see that some companies have moved beyond the early-stage overlap between CGT R&D and CDMO businesses,Focus on excelling in CDMO services. Established in 2015, IMMUNE CELL boasts an expert team composed of academicians or researchers from internationally renowned institutions such as the National Cancer Institute of the U.S. National Institutes of Health, Harvard University, and Johns Hopkins University, with over a decade of industry experience in cell therapy and gene therapy.

It is understood that when IMMUNE CELL was founded in early 2015, it developed certain cell and gene therapy (CGT) products as internal projects to rapidly implement advanced platform processes in the absence of domestic orders. As demand for contract development and manufacturing organization (CDMO) services surged in China’s CGT industry, IMMUNE CELL recognized its team’s superior technical expertise and deeper accumulation in CDMO operations, further solidifying its positioning as a CGT CDMO provider. Subsequently, to alleviate customer concerns, the company completely divested its proprietary CGT product pipeline to focus exclusively on CDMO services. Recently, the company announced positive news: on June 22, IMMUNE CELL successfully completed the delivery of multiple batches under a 200L serum-free suspension production order for GMP-grade adeno-associated virus (AAV), achieving the localized implementation of large-scale GMP manufacturing processes for AAV in China.

In summary, we can observe thatThe primary reason for the business overlap between domestic CGT “gold diggers” and “water sellers” is that China’s CGT CDMO industry is currently in its early stages of development, with some companies yet to firmly establish their strategic positioning.As the sector gradually matures, drawing on the development status of the CGT CDMO field abroad, we can conclude that the current overlap between “gold diggers” and “water sellers” in China’s CGT/CDMO landscape will eventually disappear. The transitional period during which CGT R&D enterprises transform into CDMOs will come to an end, and young entrepreneurs who are currently “torn” and “confused” at this crossroads will ultimately determine their definitive business paths.

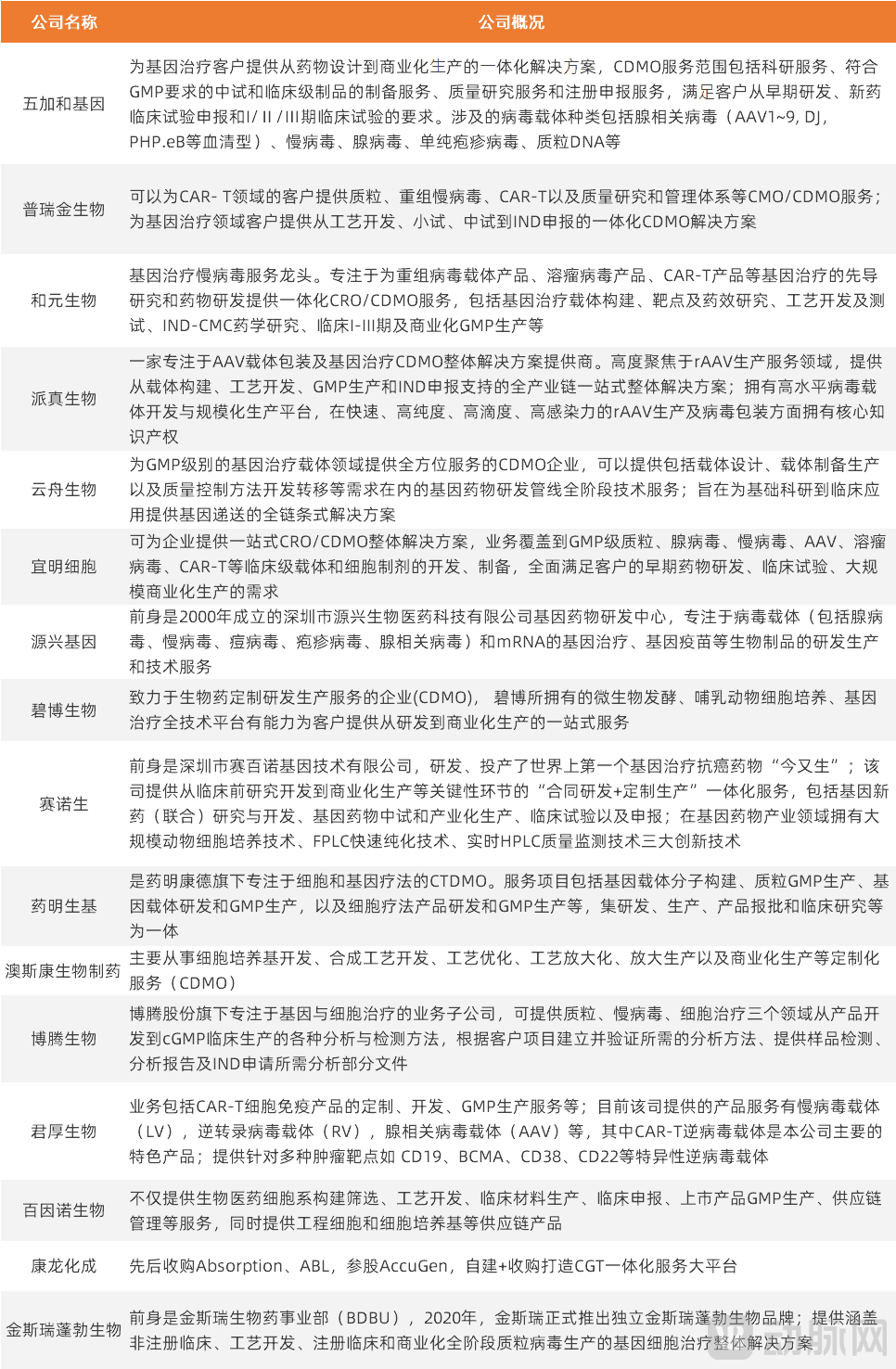

To further organize and compare the current primary business operations of domestic CGT CDMOs, VCBeat has summarized the businesses of 16 CGT CDMOs:

Major CGT CDMO Companies in China

(The above ranking is ordered by the establishment date of each company; information sources: official websites and publicly disclosed information, for reference only)

By examining the business profiles of the companies listed in the table above, we can observe thatMost CGT CDMOs offer services that tend to be “homogenized,” making it difficult to distinguish the unique specialties of individual companies on an overall basis.The phrase “one-stop service” appears with considerable frequency. Even industry leaders in niche segments such as oncolytic viruses, like Obio Technology, describe their business operations in integrated and generalized terms, such as “providing integrated CRO/CDMO services for the exploratory research and drug development of gene therapies, including recombinant viral vector products, oncolytic virus products, and CAR-T products.”

However, the reality is that even though each CDMO company offers one-stop services covering the entire industry chain—from vector construction and process development to GMP manufacturing and IND application support—business acquisition is invariably based on the team’s technical strengths. Taking IMMUNE CELL as an example, the company describes its offerings as “providing enterprises with one-stop CRO/CDMO integrated solutions, with services spanning the development and preparation of clinical-grade vectors and cell products, including GMP-grade plasmids, adenoviruses, lentiviruses, AAVs, oncolytic viruses, and CAR-T cells, fully meeting customer needs for early-stage drug R&D, clinical trials, and large-scale commercial production.” However, it is understood that the company’s most competitive businesses are the large-scale production of AAV viral vectors and the large-scale, low-cost manufacturing of plasmids.

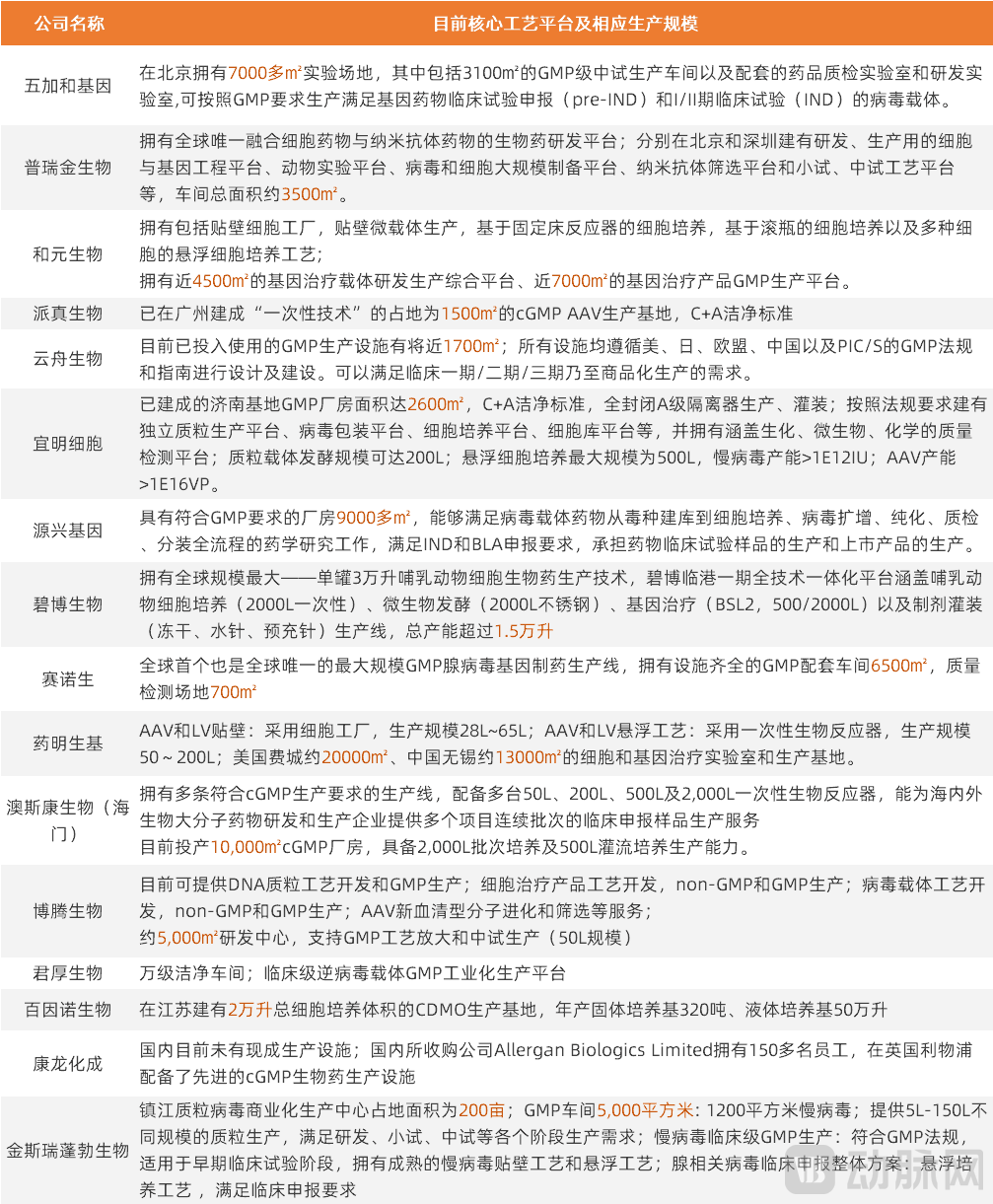

In the previous article, we mentioned thatA major bottleneck in the development of the cell and gene therapy (CGT) industry lies in the limited production capacity of viral vectors; therefore, the construction and technological advancement of manufacturing facilities by various contract development and manufacturing organizations (CDMOs) are particularly critical.VCBeat has compiled information on the core process platforms and corresponding production scales of 16 CGT CDMOs in China:

Core Technology Platforms and Corresponding Production Capacities of Major CGT CDMO Companies in China

(Note: The above companies are listed in chronological order of their establishment; sources: respective official websites and publicly disclosed information, for reference only.)

The CGT industry features complex manufacturing processes and high technical barriers. CGT CDMOs have adopted varying or similar process pathways for the production of related CGT auxiliary materials, such as plasmids, cells, and viral vectors. However, based on their descriptions of R&D focus and platform scale, it remains difficult to discern the specific competitive advantages of each CDMO. This ambiguity makes it challenging for some early-stage CGT developers to quickly identify and select suitable CDMO outsourcing partners.

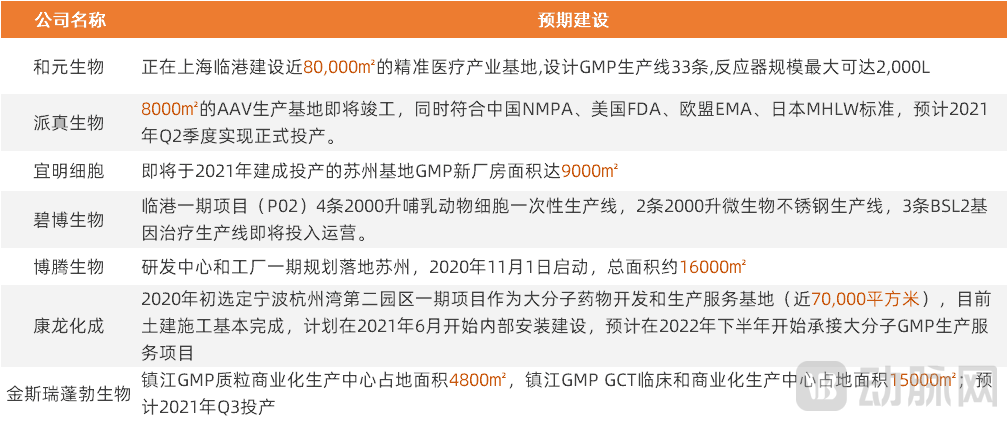

Additionally, VCBeat has compiled publicly disclosed information on planned capacity expansions by various CGT CDMOs.

Current Expansion Plans of Domestic CGT CDMO Companies

(Source: Official websites and publicly disclosed information; for reference only)

It can be seen that,“Capacity Expansion” is the current main theme driving the CGT CDMO industry.Nearly half of CGT CDMOs are currently undertaking significant capacity expansions based on their existing infrastructure. This also represents the primary use of funds from recent financing rounds for most companies.

In summary, it appears that the business offerings of various CGT CDMO companies are becoming increasingly “homogenized,” making it difficult to differentiate their capabilities in terms of process platforms and production capacity. Surprisingly, their future development plans also seem remarkably consistent: expanding production capacity. To help readers better understand the distinctive services and specific strengths of each CDMO, VCBeat has summarized three key evaluation criteria for reference only.

First, the CDMO's past service cases.The business types with the highest volume are often the flagship offerings of a given CDMO; past service cases can also serve to validate, to some extent, the CDMO’s comprehensive service capabilities. Currently, China’s cell and gene therapy (CGT) industry is in its early stages of development, and the progress of service cases handled by various CDMOs is not yet distinct enough to allow for clear assessment. As the CGT sector continues to mature and more CGT products across different therapeutic areas enter clinical trials, the capabilities of high-quality CDMOs will become increasingly prominent.

Second, the team behind the CDMO.The professional backgrounds of team members also reflect, to some extent, the capabilities of a CDMO. In addition to technical expertise, the team’s ability to communicate with regulatory authorities is critically important, as it helps companies assess the feasibility of their operations and avoid unnecessary detours for both the CDMO and its clients.

Third, the hardware facilities and specific production capacity of CDMOs.CGT clients should not focus solely on a CDMO’s capacity and facility infrastructure. Specifically, using fermentation as an example, prioritizing volumetric productivity (yield per liter) over total fermentation volume is a more effective strategy for identifying truly superior CDMOs. Furthermore, if a company offers suspension culture systems, a key criterion for evaluating high-quality CGT CDMOs is whether they possess proprietary cell lines that have been independently adapted to serum-free suspension culture.

The Parenteral Drug Association (PDA) and the journal *Journal of Stem Cell Research & Therapy* have proposed evaluation recommendations for contract manufacturing organizations (CMOs) and contract development and manufacturing organizations (CDMOs) in the field of cell therapy. At a 2016 conference, Amnon Eylath, Vice President of the New England Chapter of the Parenteral Drug Association, delivered a presentation titled “Evaluating Biotechnology and Cell and Gene Therapies,” in which he provided the following recommendations for assessing cell therapy CMOs/CDMOs: establish standardized evaluation processes based on risk management principles; conduct quality assessments by evaluating the CMO/CDMO’s performance in terms of facilities, technology, and staff operational proficiency; and determine the CMO/CDMO’s technological standing within the industry through horizontal benchmarking.

The assessment includes the following detailed evaluation criteria:Whether cell therapy product manufacturing has been initiated, whether there are precedents of successful technology transfer for cell therapies, whether environmental monitoring is compliant, whether robust measures are in place to control biological contamination associated with cell therapies, and how to ensure that staff possess the requisite technical proficiency in cell therapy.

Although the current CGT CDMO market is still in its early stages of development, with various CGT CDMOs experiencing “hesitation” and “uncertainty,” we perceive a more dominant trend of their rapid growth.

The booming CGT industry has given rise to countless emerging CGT companies, which are eagerly seeking support from developing CGT CDMOs to fuel their rapid growth and success. Meanwhile, large, mature CGT enterprises, facing increasing opportunity costs for their time and resources, are looking to outsource certain critical reagents and non-core excipients. This allows them to concentrate more heavily on drug development and clinical trials.

Among the pioneers navigating the blue ocean of CGT CDMO, all are brave, young, and driven “navigators.” So, who will lead their team to “clear the fog on the sea surface” and uncover the “great treasure” hidden in the deepest depths, claiming the largest market share? VCBeat will continue to closely monitor developments in the CGT CDMO sector.