Oral Healthcare Chains Enter Critical Acceleration Phase: $450M Invested in Six Months with Backing from SoftBank, Temasek, and New Hope

Since the beginning of 2021, the long-dormant dental services sector has once again become highly active.

How Hot Is the Industry? In Just Over the Past Six Months,A total of nine financing rounds occurred in the dental chain sector, with the total amount raised nearing RMB 3 billion.Among these, Arrail Dental’s nearly $200 million Series E financing and Meiwu Dental’s over RMB 1 billion Series B financing both rank among the top deals in the dental industry in recent years.

Notably, this year’s heavy investors include internationally backed capital firms such as SoftBank China, Temasek, and OrbiMed; well-known domestic institutions and enterprises such as Shubai Investment, Fortune Capital, and New Hope Group; as well as industrial capital entities like Yizhuang State-owned Capital Investment and Hubei Zhongyuan Jiupai.

The frenzied influx of capital has once again placed the dental chain healthcare industry in the spotlight:In the consumer healthcare segment of dentistry, industry players are searching for the next Topchoice Medical, leveraging scalable chain-operation models.(since 2007, the stock price has surged 47-fold), as well as Heartland Dental, the leading U.S. dental chain with over a thousand clinics.

(Stock price trend of Topchoice Medical after its IPO. Image source: Tiger Brokers)

A review of the development trajectory of domestic dental chain enterprises reveals that the industry experienced a surge in capital investment in 2018. However, due to challenges such as the scarcity of dentists, high labor costs, fragmented clinic operations, and elevated customer acquisition costs, this enthusiasm cooled rapidly after 2019. Compounded by the impact of the COVID-19 pandemic last year, the growth of the dental chain sector was once considered to have hit a bottleneck.

So, what are the underlying reasons for the renewed attention and investment from capital in the oral healthcare service sector? Does this signal that the entire industry has entered a critical acceleration phase? What challenges and dilemmas still exist within the industry at present? To address these questions, VCBeat conducted interviews and research with relevant investors and companies in the industry to gain insights into potential answers.

Reports and articles describing the oral care industry as a “golden track” have long been ubiquitous, with core arguments primarily centered on three aspects.

First, from the perspective of demand, China's prevalence of oral diseases has remained high for a long time. Coupled with population growth and an accelerating aging demographic, the demand for oral health continues to rise.

Second, from the perspective of business model construction, the consumer-oriented nature of dental care inherently endows dental medical services with high customer stickiness;

Third, with the rise of the appearance economy, the oral care industry holds even greater commercial potential in the future.

It is precisely for these reasons that the dental industry has attracted significant capital inflow in recent years. “In 2017, we co-invested in a dental chain clinic amid the prevailing market enthusiasm, and its valuation doubled by 2018,” an investor who requested anonymity told VCBeat. “The sudden surge in industry hype was indeed somewhat unexpected.”

But soon, dental chain clinics faced a “rude awakening.”Due to the overall weak economic environment and the gradual adoption of Diagnosis-Related Groups (DRGs), a significant number of patients in first- and second-tier cities have returned to public hospitals over the past two years, thereby increasing operational pressures on dental clinics that rely on high-cost customer acquisition strategies such as advertising and prime locations.

“Although there are macroeconomic reasons,The core issue lies in the numerous challenges dental chain institutions face in achieving profitability.“The aforementioned investors stated, ‘When breaking down the financial model of a dental service provider, net profit margins stand at approximately 15% under compliant operations, which is far from the exorbitant profits rumored in public discourse. As more players enter the market, maintaining a net profit margin of 10% would be considered respectable.’”

This is because, as oral healthcare service providers scale up, they face challenges related to talent, technology, market, and management, all of which dilute profitability. The specific issues are mainly as follows:

First, the barrier to entry is relatively low, and clinics are characterized by a fragmented landscape.The startup costs for dental practices are not high compared to other medical service sectors. In some regions, an initial investment of only RMB 1–2 million is sufficient to open a clinic. This has led to a proliferation of independent clinics across various locations, resulting in a relatively fragmented distribution. In certain high-demand areas, the growth rate of clinics has outpaced both the size of the addressable resident population and the number of available dentists.

Second, high labor costs.Dentists are the core productive force of dental institutions and the primary providers of patient care. Clinic services rely on dentists' clinical expertise; however, dentists are a relatively scarce resource in China. The lengthy training period for dentists contributes to labor costs being the largest expense in scaling dental chains, with personnel costs accounting for approximately 40% of total clinic revenue.

Third, customer acquisition costs are high.As a highly marketized sector, dentistry has prompted dental institutions to invest not only in offline advertising but also in online marketing. Coupled with patients’ increasingly high expectations for service experience, customer acquisition costs have remained persistently high, with some clinics incurring costs of even RMB 3,000–4,000 per patient.

Thus, when the “black swan” event of the COVID-19 pandemic emerged last year, numerous dental healthcare service providers faced operational shutdowns, with frequent media reports highlighting their inability to sustain operations due to insufficient cash flow. According to a questionnaire survey released in March last year by Guangzhou Ai Li Bi, a third-party hospital management consulting firm, nearly 60% of private hospitals had less than two months of cash runway at that time.

“Our portfolio companies were also forced to cut their outpatient services by half to generate cash flow during the pandemic,” said the aforementioned investor. In the wake of the outbreak, the fund he is affiliated with has begun to shift its focus. “We have recently started looking at upstream dental materials, but have not yet made any investments. We are definitely not considering downstream chain clinics for the time being, because”“Small and medium-sized dental chains have weak risk resistance, while top-tier chain institutions are too expensive.”

Among the multiple investment institutions interviewed by VCBeat, many investors stated that although dental chain clinics appear promising, it is extremely difficult to identify high-quality targets. This is because operating a dental chain is a capital-intensive business; each new clinic expansion requires substantial funding. The expected investment horizon may range from five to ten years, or even longer. Consequently, short-term losses are inevitable, while long-term risks remain difficult to manage.

As a result, oral healthcare service providers are hesitant to expand aggressively, making it difficult for them to rapidly extend their service coverage radius. BecauseOnce cross-regional expansion occurs, it becomes difficult to ensure the quality of medical care across various institutions; any medical malpractice incidents or negative publicity would adversely impact the entire brand.

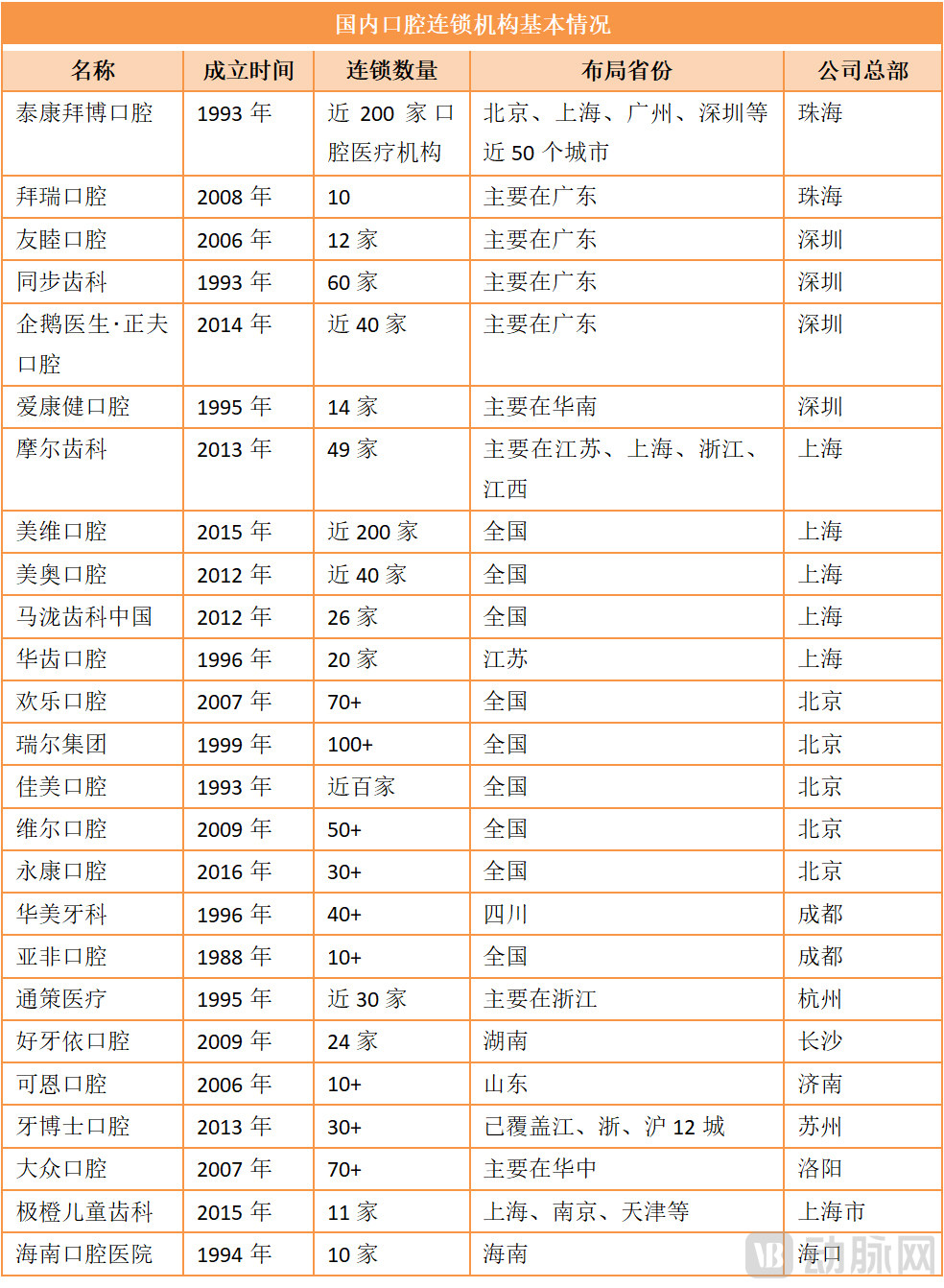

Based on the aforementioned logic, it is not difficult to identify an interesting phenomenon in the dental chain industry: currently, leading enterprises are all regionally concentrated.For instance, Topchoice Medical is primarily concentrated within Zhejiang Province, Dazhong Dental focuses on Wuhan and other central provinces and cities, while Little White Rabbit Dental concentrates on the northwest market, centered in Xi’an.As can be seen, various market entrants are maintaining a cautious stance toward expansion beyond their home provinces and nationwide growth across China.

As is well known, the greatest value of chain organizations lies in achieving overall cost reduction and efficiency improvement through scale and standardization, thereby continuously widening the corporate moat and enhancing profitability. However, the dental chain industry currently faces challenges that hinder rapid scaling. How, then, can it break through this impasse?

How to Address the Challenges Faced by Dental Chains During Scaling? Opportunities May Be Found in the Similarities and Differences Between the Chinese and U.S. Markets.

An Overview of the U.S. Dental Care Services MarketRelevant data indicate that the U.S. dental market is valued at approximately $120 billion, with a compound annual growth rate (CAGR) of around 3%. Within this substantial market, the primary service providers are dental clinics, with clinics and hospitals accounting for roughly 90% and 10% of the share, respectively.

It is important to note that the vast majority of dental clinic founders are dentists themselves. While they possess extensive clinical experience and strong professional competencies, they often lack expertise in non-clinical areas such as clinic management, operations, legal affairs, and accounting. In this regard, the United States market shares significant similarities with the Chinese domestic market:In the private sector, small-scale, independent dental clinics are the mainstream.

In response to this phenomenon, a large number of Dental Service Organizations (DSOs) have emerged in the United States. Specifically,DSO organizations are a collective term for operational management companies that provide non-clinical business support services to dentists and dental clinics. Their core function is to offer clinics the necessary support in management, operations, finance, legal affairs, training, and other non-clinical areas, enabling dentists to devote more energy to enhancing their clinical skills and treating patients.

According to statistics from the American Dental Association, as of 2019, there were more than 200,000 dental clinics in the United States, with 11.3% affiliated with Dental Support Organizations (DSOs), up from just 7.4% in 2015. Following this trend, a large number of DSO-model companies have emerged in the U.S., such as Heartland Dental, Aspen Dental, and Pacific Dental Services.

Of course, there is no specific size range for Dental Support Organizations (DSOs); a DSO may consist of as few as two clinics or aggregate hundreds or even thousands of clinics. Furthermore, DSO models vary across companies: some excel in helping dental practices achieve regulatory compliance, others are dedicated to enhancing the digitalization of clinic operations, and still others focus on supply chain management.

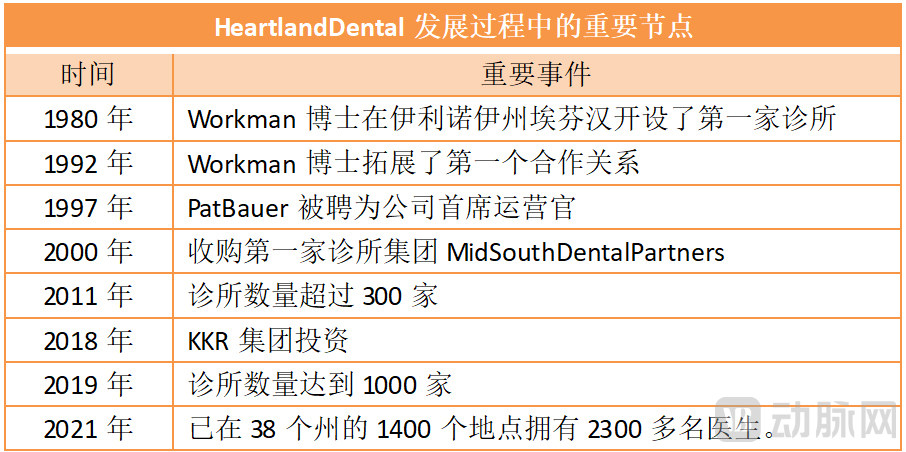

Taking Heartland Dental as an example, its acquisition journey began in 2000 with the purchase of its first clinic group, MidSouth Dental Partners. By 2011, Heartland Dental had grown to 3,000 employees and acquired Neibauer Dental Care, which operated 26 clinics, during the same period.

As the pace of mergers and acquisitions accelerated, Heartland Dental expanded its network to over 800 clinics in 2017 and brought in the globally renowned private equity firm KKR. With ample “dry powder,” Heartland Dental grew its total number of dental practices to more than 1,000 by 2019, becoming one of the leading dental service organizations in the United States.

An analysis of the reasons behind Heartland Dental’s rapid expansion reveals that, beyond the consolidation effects brought by the DSO model, the more critical factor lies in the underlying logic of this model: after securing investment from KKR, Heartland Dental made significant strides in digitalization and dentist empowerment.

Specifically, in terms of digitalization, Heartland Dental initiated the largest internal rollout of intraoral scanners, providing thousands of units to its supported practices. Additionally, Heartland Dental maintains the largest network of Invisalign providers, having completed more than 50,000 collaborative cases to date.

In terms of empowering dentists, Heartland Dental has launched the “A Company of More” campaign to understand and address the support dentists need in their daily practice. By partnering with leading dental product and technology companies, it enables dentists to adopt new technologies and equipment more quickly and conveniently. Furthermore, Heartland Dental offers a well-established continuing education curriculum to help dentists enhance their clinical skills.

It is precisely due to its continuous in-depth development in these two areas that Heartland Dental has been able to achieve constant breakthroughs during its scaling process. Relevant surveys show that 82% of dentists supported by Heartland Dental expressed satisfaction with the support provided, 85% indicated they would recommend their peers to join Heartland Dental, and 15% of clinics achieved revenue growth within the first year alone.

In summary, to overcome the many challenges in the chain expansion of dental clinics, the core strategy is to leverage digital tools to improve labor efficiency and reduce operating costs, while implementing a series of measures to retain dentists and secure talent.

Returning to the domestic market,The dental chain market is currently on the eve of consolidation.This is because leading dental chain enterprises are accelerating their fundraising efforts: in addition to the companies with large-scale financing mentioned above, numerous dental chains have also been striving for initial public offerings (IPOs) over the past year.

Last September, Smile Dental Group initiated preparations for its initial public offering (IPO). By the end of the year, Henglun Medical, a dental chain enterprise, submitted an IPO application to the ChiNext board (which was later withdrawn). In early 2021, Little White Rabbit Dental submitted an IPO application to the ChiNext board. In June, Jiahong Dental resumed its IPO review process. In July, Arrail Group Limited, the parent company of Arrail Dental, filed an IPO application with the Main Board of the Hong Kong Stock Exchange.

What deserves greater attention is that leading enterprises have gradually developed differentiated paths and directions, yet their underlying core logic aligns with international market experience: empowering dentists and driving digitalization.

“The primary pain points in the dental field are the supply of dentists and continuing education for professionals,” emphasized Shuangbai Investment, which has invested in regionally leading dental care chains such as Sync Dental Care and Moore Dental Care, on multiple occasions. In response, when developing downstream medical service industries, Shuangbai Investment adopted the vision and philosophy of “integrated development of medical practice, education, and research to enhance regional dental care standards.”

Specifically,In addition to chain institutions, Songbo Investment has also actively laid out large-scale dental hospitals with integrated development of medical treatment, education, and research., for example, it successively acquired controlling stakes in Huizhou Stomatological Hospital and Heyuan Hengxin Stomatological Hospital, two leading dental institutions in South China, in 2019 and 2020, respectively. In recent years, it has invested in and supported Shantou Stomatological Hospital, a teaching-oriented specialized dental hospital in Shantou; Henglun Dental, the largest dental hospital chain in Shanxi Province; and Hainan Stomatological Hospital, the first tertiary-level dental hospital in Hainan Province.

Next, let’s look at Meiwei Dental, which recently secured over RMB 1 billion in financing., it adopts a distinctive “DSO” model to bring together dental entrepreneurs and medical institutions, and continuously provides these organizations with comprehensive empowerment spanning strategic investment, standardization, clinical technology enhancement, brand management, and digital transformation, thereby helping them achieve rapid, personalized development.

Moreover, Meiwei Dental places significant emphasis on cultivating top-tier dental talent. “From its inception, we established the strategic goal of forming an ‘Industry-Academia-Research Innovation Alliance,’ partnering with numerous prestigious dental institutions both domestically and internationally. We engage in deep collaboration across academic forums, clinical teaching, scientific research innovation, and medical technologies, thereby building a research and innovation system and a physician group to enhance the clinical skills, service philosophies, and overall service levels of professionals within dental institutions,” Meiwei Dental told VCBeat. Leveraging resources from renowned medical experts at home and abroad, Meiwei Dental has gradually established a diversified, international talent development platform that includes the “2017 Meiwei Implant Forum,” the “Meiwei Dental Medical Case Competition,” the “China MaxiCourse® Implant Training Program,” and overseas study and fellowship opportunities.

To date, Meoway Dental has established nearly 200 dental clinics and hospitals across core urban clusters in China, along with a high-quality network of business partners. With positive operating cash flow and profits over the past two years, this demonstrates that Meoway’s distinctive “DSO” model has been successfully validated and has gained significant market recognition.

Under Meiwei Dental’s partnership model, dentist-owners become the managers of new clinics. Empowered by Meiwei’s distinctive “DSO” model, this approach not only helps dental institutions address operational challenges but also supports their expansion and growth, enabling them to emerge as regional leaders.

For Ma Long Dental, from its establishment in 2013 to this year, it has consistently adhered to a strategy that does not prioritize store count or expansion speed, but instead focuses on strategic deployment in key cities, achieving explosive regional growth on a solid foundation, and building a closed-loop integrated industry chain.

“We have gradually transformed from a traditional medical institution centered on planting technology. Currently, we are making significant strides in multiple areas, including facial management for adolescents, sleep and breathing management, and full-face aesthetics guided by the stomatognathic system. We continue to develop new medical service products to meet the evolving needs of our customers,” Malo Clinic told VCBeat.

In addition, Ma Long Dental is actively leveraging various digital tools and fostering collaboration within its operations team to reduce the chair time occupied by core dentists. This allows doctors to dedicate more time to research and innovation. By harnessing the platform’s resource advantages, Ma Long Dental helps inventors develop comprehensive, end-to-end solutions and facilitates their commercial implementation and promotion, thereby creating new value for both the inventors and the group.

“Digital capabilities will become a key benchmark for evaluating enterprises and individual dentists in the future. Competition in basic dental care services will intensify, leading to price declines, and businesses must establish differentiated core competencies to ensure their survival,” stated Malo Clinic.

Happy Dentistry has also prioritized strengthening its internal capabilities.In recent years, Happy Oral Care has slowed its blind cross-regional expansion while continuing to solidify its position as the No. 1 player in the Beijing market; meanwhile, it has promoted the productization of clinical services, the digitization of consultation plans, and the standardization of business processes.

For example, Happy Oral Care has refined its training for medical staff and Patient Management Managers (PMMs) into scenario-based modules and fully launched them online. The company is vigorously promoting digital diagnostic and treatment methods such as intraoral scanning and clear aligner orthodontics, independently developed the IDSO clinic business growth SaaS system (“Jiezhenbao”), further improved standards for clinic design and renovation construction, and streamlined and integrated procurement channels for high-value consumables and equipment.

Notably, Happy Dentistry has developed the IDSO Clinic Business Growth System, the first platform in China to empower dental practices not merely through the integration of commercial distribution channels such as supply chains, but by enhancing core operational aspects including treatment planning, clinic management, and patient CRM. Currently, more than 300 dental clinics across China have joined the IDSO Dental Alliance as member units, operating under the philosophy of “light marketing, heavy emphasis on building doctor-patient trust.” Happy Dentistry stated, “IDSO is poised to become the largest alliance platform empowering dental clinics nationwide and will serve as Happy Dentistry’s most core differentiated competitive advantage.”

During the pandemic, Happy Dentistry IDSO deepened its digital initiatives by leveraging its self-developed and launched IDSO Clinic Management System. Based on the entire patient reception and service workflow, it created an integrated online service platform combining front-end clinical care with internal clinic management. Its “Central Consultation Center” module enables expert teams to conduct online case consultations and analyses for thousands of cases daily. On the laboratory side, the application of digital chairside equipment was significantly expanded. “These multiple measures have improved diagnostic and treatment efficiency for patients and reduced the frequency of in-person consultations, thereby playing a positive role in epidemic prevention and control.”

As can be seen, although leading companies follow different paths, they share the same goal: striving to enhance their digital capabilities and making substantial efforts in the training and empowerment of dentists.

It is worth noting that China’s dental care services market comprises nearly 70,000 dental clinics, ranking among the largest in the world. This provides a fertile ground for industry consolidation and mergers and acquisitions, thereby supporting the growth of dental chain enterprises. Therefore, those who can continuously address the various complex challenges associated with scaling up while strengthening their core competencies will be poised to emerge as leaders.