Mental Health B2B Services: A Billion-Dollar Early-Stage Sector Poised for Breakout Growth?

The recently concluded Tokyo Olympics not only sparked a nationwide surge in sports-related discussions but also laid the foundation for the development of numerous sectors and industries, with the field of mental health being one of the key beneficiaries.

As early as 2019, the International Olympic Committee released the “Consensus Statement on Mental Health in Elite Athletes,” which found through a 12-month follow-up study that the prevalence of mental health disorders among elite athletes ranged from 5% to 35%.

To address this issue, organizations such as the National Football League (NFL), the National Basketball Association (NBA), the Women’s National Basketball Association (WNBA), and the Association of Tennis Professionals (ATP) have begun to provide athletes with professional mental health services by developing mental health initiatives and partnering with specialized mental health service providers.

Behind this lies a market with immense growth potential—the B2B mental health market.

For a long time, in the public perception, the B2B market for mental health has been like an underwater iceberg compared to the B2C market: while it holds significant growth potential, it remains largely unseen.

In fact, the B2B market for mental health has been advancing rapidly. Just this year, LifeStance Health and Talkspace, two companies that have strategically prioritized the B2B segment, went public in succession. This not only reignited market interest in mental health but also drew greater attention to the B2B mental health sector as an emerging high-growth area. (In this article, we collectively refer to mental health services provided to governments, social organizations, schools, enterprises, and other entities as “B2B mental health business.”)

Ideally, B-end users are more stable than C-end users, and companies entering the market from the perspectives of corporate employers, health plans, and medical institutions are more likely to gain a competitive advantage. Specifically, why is there a need for B-end mental health services? What are the modes of service delivery? What are the drivers propelling market development? Is future market demand sustainable?

How Mental Health Services Can Address the Core Needs of B-End Clients

In November 2018, the National Health Commission and nine other ministries and commissions issued the Work Plan for Pilot Programs on the Construction of a Nationwide Social Psychological Service System. The plan required pilot regions to gradually establish a social psychological service system, build social service platforms, incorporate mental health services into the evaluation index system for Healthy Cities, and ultimately explore models and working mechanisms for social psychological services that could be promoted nationwide.

In January 2019, multiple departments jointly launched pilot programs for the construction of a social psychological service system. Based on the established objectives and the implementation status of the 2019 pilot tasks, in April 2020, the National Health Commission and nine other ministries and commissions jointly issued the "Notice on Printing and Distributing the Key Tasks for 2020 of the Pilot Program for the Construction of a National Social Psychological Service System and Adding New Pilot Sites," to further advance and guide the standardized implementation of the social psychological service system across various regions.

In accordance with the requirements, pilot regions must establish a comprehensive psychological service network accessible to all segments of the population. Meanwhile, government agencies, schools, enterprises, and public institutions are encouraged to provide mental health services to employees, students, and other groups by setting up psychological counseling offices or purchasing related services.

In the “Mental Health Promotion Action” of the Healthy China initiative, it is also stipulated that all entities and schools shall establish mental health service teams or provide mental health services to employees and students by purchasing such services. Meanwhile, grassroots social organizations, social workers, and volunteers are encouraged to provide mental health services to key populations, including the elderly, women, children, and persons with disabilities.

Furthermore, by acquiring and studying knowledge related to mental health, government personnel can better address public needs and provide more refined communication and support services. Consequently, there is a strong demand on the government side for procuring mental health services, leading most enterprises to currently prioritize the government sector as a key entry point into the B2B mental health market.

Among the mental health services offered to enterprises, the Employee Assistance Program (EAP) is arguably the most widely recognized service delivery model. Originating in the United States during the 1920s and 1930s, EAP aims to improve organizational environment and climate by providing professional diagnostics and recommendations to organizations, as well as offering expert counseling, education, guidance, and training to employees and their immediate family members. It addresses various psychological and behavioral issues faced by employees and their families, thereby developing and enhancing employees’ psychological capital, which in turn boosts their job performance and well-being.

EAP services in China were first introduced by large foreign-invested enterprises in the IT industry, such as Nokia and HP. As awareness of EAP concepts has grown, domestic companies like Lenovo and SAIC Volkswagen have also begun implementing EAP programs. Meanwhile, localized EAP service providers have emerged, including Beijing Yipusi Consulting Company, CIIC Occupational Mental Health Center, and the China EAP Service Center.

In recent years, China’s rapid socioeconomic development has been accompanied by increasing workplace pressure and a growing susceptibility to psychological imbalance among employees. Social incidents stemming from employee mental health issues have also been frequently reported in the media. In this context, an increasing number of enterprises are purchasing Employee Assistance Programs (EAPs) out of social responsibility and for talent management purposes. It is understood that companies such as Huawei, Tencent, and Baidu have implemented EAPs and related services for their employees.

Schools and institutions procure mental health-related products or services for a variety of reasons.

First, policy-driven initiatives. In December 2019, twelve ministries and commissions, including the National Health Commission, the Publicity Department of the Communist Party of China Central Committee, and the Ministry of Education, jointly issued the Healthy China Action—Action Plan for Mental Health of Children and Adolescents (2019–2022). The plan proposed that by the end of 2022, schools at all levels and across all types should establish mental health service platforms or leverage personnel such as school doctors to provide mental health services for students, while preschool education institutions and special education institutions should be staffed with full-time or part-time mental health education teachers.

Second, the demographic seeking psychological counseling is trending younger. According to data from the National Health Commission of China, there are 340 million children and adolescents under the age of 17 in the country, with approximately 30 million suffering significantly from mental disorders.

It can be said that, driven by both policy and demand, the school sector has also become a key battleground for companies seeking to establish a presence in the B2B mental health market.

Furthermore, hospitals can also serve as an entry point into the B2B market for mental health services. In the wake of digitalization, hospitals themselves have a certain willingness to adopt platforms and tools designed for mental health care.

The Government as the Primary Purchaser; The Market Is Still in Its Growth Phase

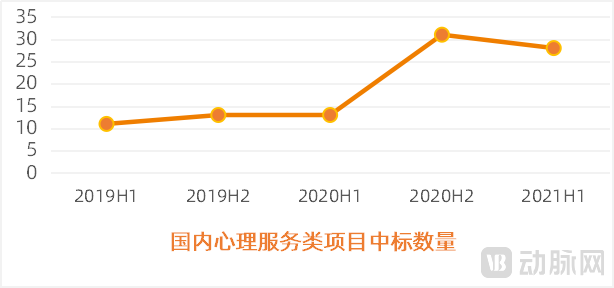

The most intuitive way to gauge market attention is to examine data on the market application of related products and services, as well as capital investment trends. To gain a preliminary understanding of the application landscape of China’s mental health services market, VCBeat compiled a summary of winning bid information for domestic mental health service projects from 2019 to the first half of 2021 (data source: China Government Procurement Network).

According to statistics, approximately 96 winning bid announcements for psychological service projects were disclosed on the China Government Procurement Network over the two-and-a-half-year period from 2019 to the first half of 2021 (excluding projects with low business relevance), showing an overall upward trend in volume.

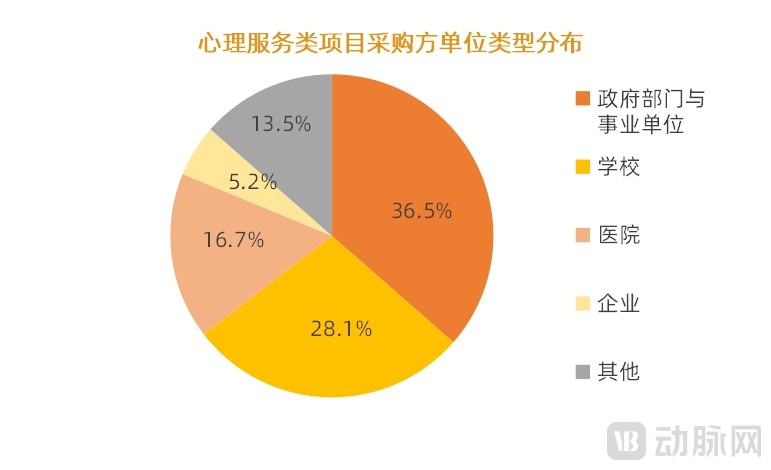

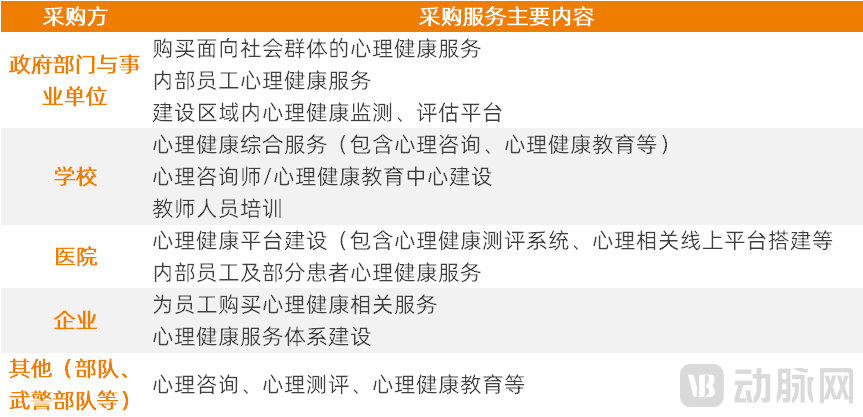

Based on the nature of the user entities in winning bid projects, we categorize purchasers into five major groups: government departments and public institutions, schools, hospitals, enterprises, and others (such as the military and armed police forces). Analysis of the winning bid information reveals that government entities are the primary purchasers, accounting for over 35% of the total. Their main procurements consist of mental health services targeted at various social groups, with a smaller portion dedicated to services provided directly to internal staff, thereby closely aligning with the objective of building a comprehensive social psychological service system.

Schools constitute the second-largest purchaser, accounting for 28.1% of the market, with their primary demand being the procurement of comprehensive mental health services. Additionally, there is a widespread need among schools to provide psychological knowledge training for teachers.

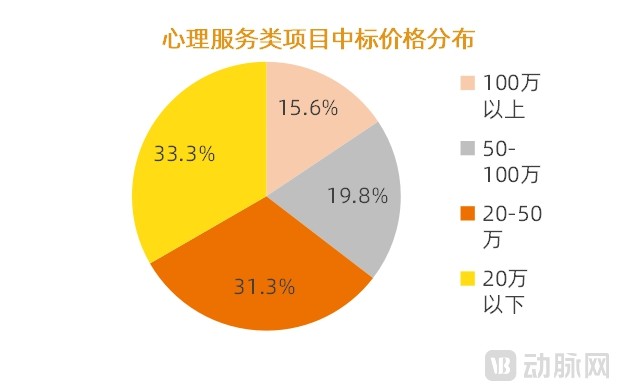

Regarding pricing, the winning bid prices for projects exhibit a wide range, with a maximum spread of up to five million yuan. As indicated by the distribution chart of winning bid prices, projects priced below 200,000 yuan constitute the majority, accounting for 33.3%, followed by those in the 200,000–500,000 yuan range, which account for 31.1%; the difference between these two categories is not particularly significant.

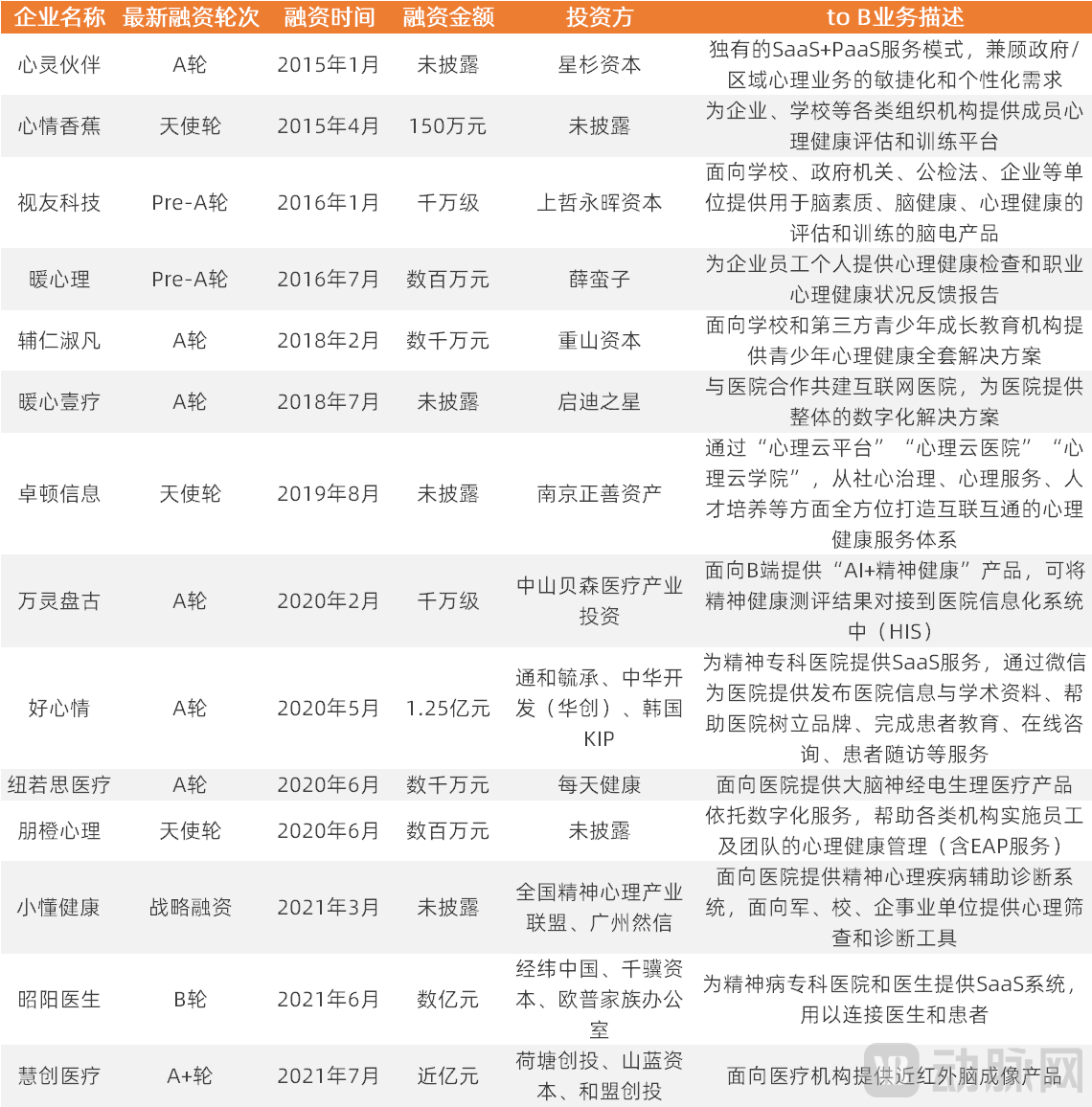

In terms of capital market performance, according to incomplete statistics from VCBeat, since 2015, approximately 14 domestic B2B mental health companies, as well as enterprises with B2B operations constituting a significant portion of their revenue, have secured financing.

Based on the information in the table above, we find that the latest round of financing for most companies is concentrated between the angel round and Series A. This phenomenon aligns with the current status of China’s mental health market, which remains in its early stages.

An analysis of the business operations of companies that have secured financing reveals that, for B-side clients, the primary service offerings include: providing hardware and software products; adopting a B2B2C model by establishing SaaS platforms for B-side clients; and delivering psychological counseling and assessment services directly applicable to psychological intervention.

Among these, the B2B2C model is also a primary approach for enterprises developing business-to-business (B-end) operations. Taking Haoxinqing and Zhaoyang Doctor as examples, both provide SaaS services to psychiatric specialty hospitals, assisting them with operational and patient management. This model not only facilitates expansion in the B-end market but also builds a bridge for enterprises to strengthen their presence in the consumer (C-end) market.

What are the replicable models for the B2B mental health market?

Although China’s B2B mental health market is currently in a phase of gradual development, the most extensive and successful industry applications remain in the United States. According to incomplete statistics from VCBeat, nearly 20 U.S.-based mental health service companies primarily focused on B2B business have secured financing this year alone, with the majority having reached Series B funding or later stages.

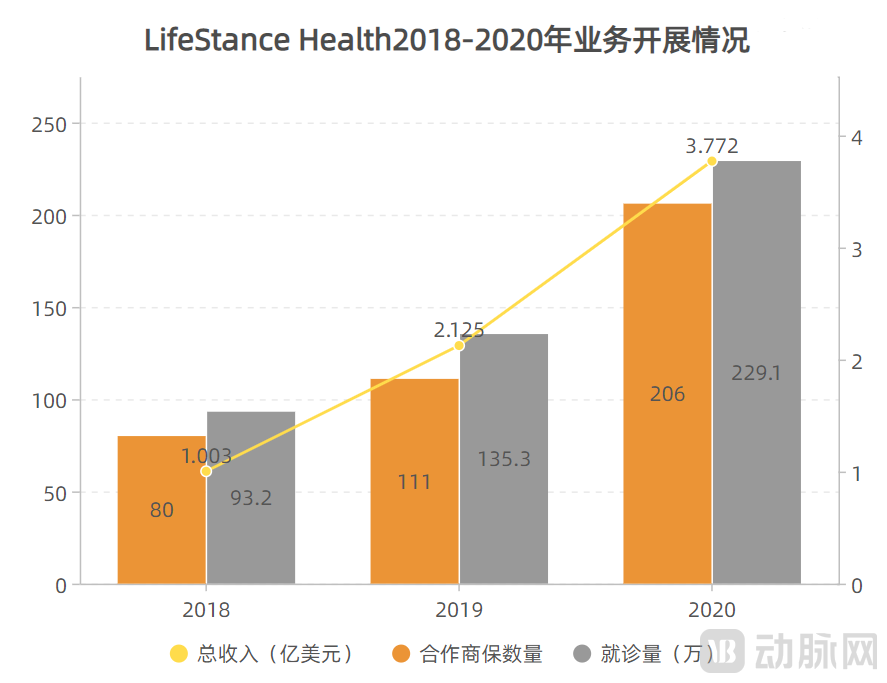

LifeStance Health, founded in 2017, primarily operates by selling mental health services to health insurance companies. Leveraging offline psychological clinics as its service delivery platform, the company provides integrated care that combines online and offline modalities, as well as collaborative treatment involving both psychiatrists and psychological counselors.

According to LifeStance Health’s financial data, 89% of the company’s revenue in 2020 came from commercial insurance, only 5% from government health insurance programs, 4% from out-of-pocket payments by patients, and 2% from non-patient services.

Relevant studies indicate that for every $1 spent on mental health care, $6.5 in medical costs can be saved. For commercial insurers and employers, adopting services provided by LifeStance Health can effectively reduce healthcare costs.

An analysis of LifeStance Health’s business operations and revenue from 2018 to 2020 reveals that the volume of its collaborations with commercial insurers has risen steadily over the past three years, nearly doubling by 2020. This growth has also driven a steady increase in patient visits and the company’s total revenue.

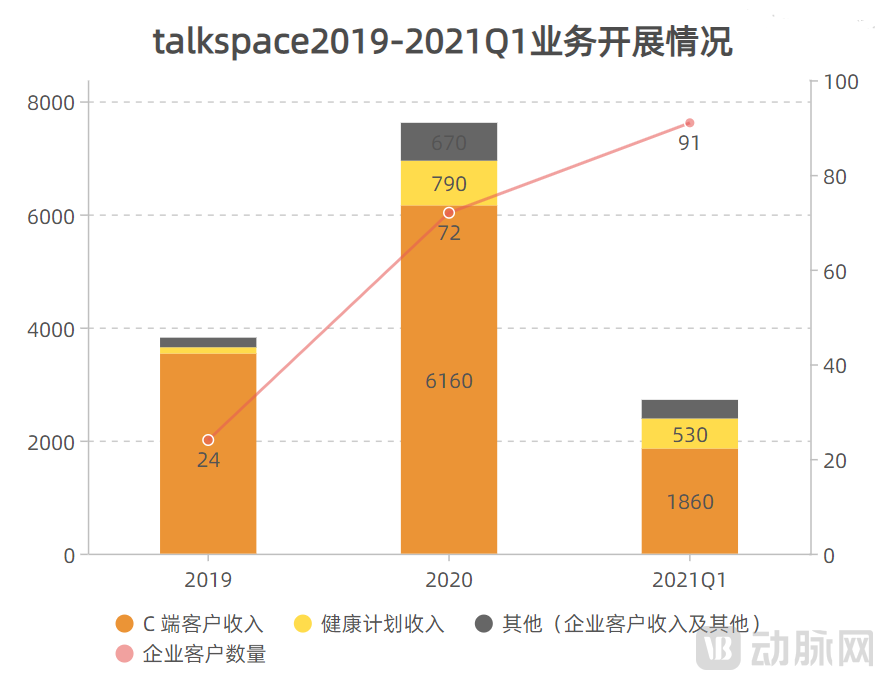

Talkspace, founded in 2012, entered the psychological counseling market with a business model centered on low-cost text-based therapy and video consultations, allowing users to communicate with therapists via unlimited messaging. Initially focused on providing online psychological counseling services to individual consumers (B2C), the company later expanded its offerings to businesses (B2B), delivering employee mental health services to corporate employers.

Leveraging its earlier accumulation of C-end users, Talkspace formally entered the B-end market in 2018; its B-end business subsequently scaled rapidly and gradually became a significant source of the company’s revenue.

As shown in the chart above, Talkspace’s B2B business has experienced rapid growth in recent years, while the proportion of revenue from individual consumers (C-end) has declined. In terms of the number of partner enterprises, Talkspace had 25 corporate clients as of March 31, 2020; this figure rose to 91 in 2021, representing a year-over-year increase of 264%.

Lyra Health, founded in 2015 and headquartered in Burlingame, California, has established a platform that leverages AI-driven matching technology to connect corporate employees with high-quality mental health therapists. Additionally, Lyra Health serves as a digital tool for self-guided therapy.

For employees, the safety and confidentiality of psychological counseling services are key factors considered when selecting a service. Therefore, Lyra Health has always prioritized security and privacy in its platform design, ensuring that employees can describe their symptoms, severity levels, and other mental health-related concerns in a private space. The platform then matches employees with appropriate therapists based on their needs.

What areas need improvement?

From the perspective of capital market performance, there is still a certain gap between China’s B2B mental health market and its foreign counterparts. So, what is the current status of each segment across the entire service chain? Which segments offer room for improvement?

Purchasers: Corporate Willingness to Pay Needs Strengthening

In recent years, driven by policy influences, both government and educational sectors have accelerated the development of mental health service systems, creating substantial market growth opportunities. Meanwhile, hospitals are also procuring mental health-related products to enhance patient management efficiency and the quality of diagnosis and treatment.

However, for enterprises, policies have primarily mandated state-owned enterprises (SOEs) and central SOEs to provide mental health-related services, while private enterprises demonstrate significantly lower willingness to purchase such services. According to VCBeat’s communications with industry insiders, on one hand, companies must consider factors such as budget and cost when purchasing mental health services; on the other hand, there is a shortage of qualified professionals in China’s mental health industry, making it difficult to ensure professional standards and quantify service outcomes. Therefore, although large enterprises continue to invest in this area, most small and medium-sized private enterprises do not prioritize mental health services as their first choice for employee benefits.

“This reflects a problem: the industry’s overall development remains disordered,” Zhang Ling, Dean of the Nanjing Lizhi Psychological Big Data Industry Research Institute, told VCBeat. “Whether through bidding processes or directed procurement, companies find it difficult to trace the entire service workflow and quantify service outcomes.” This has also led to issues regarding professional standards and after-sales support. Under these circumstances, some companies believe that delivering job-related training directly to employees can generate greater value.

Payers: Gradual Inclusion in Medical Insurance

Unlike China’s medical insurance system, the U.S. healthcare system features a significant share of commercial insurance, most of which is employer-sponsored health coverage provided by companies to their employees. Therefore, mental health companies can bundle mental health services into insurance products through partnerships with insurers, while employers themselves also have demand for purchasing mental health-related products for their staff.

In China, the medical insurance purchased by enterprises for their employees is generally social security-based medical insurance, which typically does not cover psychological counseling or psychotherapy.

However, earlier this year, the Guangdong Provincial Healthcare Security Administration, in conjunction with the Provincial Department of Human Resources and Social Security, issued the “Guangdong Province Basic Medical Insurance, Work-Related Injury Insurance, and Maternity Insurance Diagnosis and Treatment Items Catalog (2021)” and the “Guangdong Province Basic Medical Insurance, Work-Related Injury Insurance, and Maternity Insurance Medical Consumables Catalog (2021),” which will officially take effect on August 15. Notably, psychotherapy has been included in the scope of medical insurance reimbursement.

The launch of this policy will, on the one hand, open up a larger B2B market for psychological services and, on the other hand, further enhance public awareness of mental health and well-being.

Supply Side: Scarcity of Top Talent

The insufficiency of high-quality medical resources has long been a perennial issue in China, a phenomenon that is particularly pronounced in the mental health sector.

According to publicly available information, the Ministry of Human Resources and Social Security has issued over one million Level 3 or Level 2 Psychological Counselor qualification certificates since 2002. However, only 30,000 to 40,000 individuals are engaged in full-time or part-time work in the psychological counseling industry. With the current cancellation of the accreditation examination for psychological counselors, the shortage of qualified professionals is expected to continue widening.

Furthermore, there are significant differences between the training systems for psychological counselors in China and those abroad. Taking California, USA, as an example, individuals aspiring to become licensed psychological counselors must pursue a master’s degree in clinical psychology after completing their undergraduate studies, accumulate thousands of hours of supervised internship experience, and pass a licensing examination to obtain practice credentials. Even after licensure, they are required to undergo continuing education annually, which helps ensure the professional competence of licensed psychological counselors.

Compared with psychological counselors, psychotherapists are even scarcer; by the end of 2017, there were only about 6,000 psychotherapists in China.

To some extent, it can be said that the shortage of high-quality talent is the primary factor contributing to the slow development of China’s B2B mental health market.

Final Thoughts

Although China’s B2B mental health market still lags behind that of foreign countries overall, the industry has been on a steady upward trajectory in recent years under the influence of policy support. Amid this trend, some companies that originally provided mental health services to consumers (B2C) have begun to expand into the B2B sector.

The Depression Institute, which prioritizes community management for individuals with depression as a key service model, launched its corporate mental health services business this year and established the Ke Xinli Public Welfare Foundation to advance public education on mental and psychological health. Its core initiative is the “Life Guardian Center,” which employs an “AI + crisis psychology team” approach to intervene with depressed individuals at imminent risk of suicide.

In addition, companies such as YiXinLi and YiDianLing have also begun offering B2B digital mental health service products and SaaS-based psychological risk screening systems.

Although the B2B mental health market in China is still in its early stages of development, with no “unicorns” or publicly listed companies emerging compared to overseas markets, this has not dampened the resolve of numerous entrepreneurs to establish a presence in this sector.

However, for China’s B2B mental health market to achieve sustained growth, focusing solely on the service supply side is clearly insufficient. In light of the current overall development status of China’s mental health industry, policy remains the most critical driving force.

First, policy-driven initiatives can gradually improve the talent development system in the mental health industry and strengthen the service supply side.

Second, it is difficult to rapidly increase the willingness of B-side clients to pay by relying solely on service providers for market education; therefore, policy-driven initiatives are required.

From a market perspective, China’s B2B mental health sector is not expected to experience explosive growth in the short term. However, the current industry momentum gives us confidence that this “iceberg” of the B2B mental health market will eventually emerge into full view.