Another Health Insurance Unicorn Files for IPO: Nearly RMB 2.7 Billion in Annual Revenue, Backed by Tencent and IDG

After seven years in operation, SiPay Health Technology Co., Ltd. (hereinafter referred to as “SiPay Health”) has decided to pursue an initial public offering (IPO).

On the evening of August 6, Si Pai Health, a medical health management platform company, submitted its listing application to the Hong Kong Stock Exchange. Morgan Stanley, CICC, and Haitong International served as joint sponsors.

Since its establishment in 2014, Si Pai Health has been a “star enterprise,” favored by numerous investors.To date, Si Pai Health has completed seven rounds of financing, raising a total of over RMB 3 billion. The investor roster includes prominent companies and institutions such as Tencent, Ping An, IDG Capital, Sidao Capital, and F-Prime Capital. Among them, Tencent, Ping An, and IDG Capital have participated in multiple financing rounds of Si Pai Health.

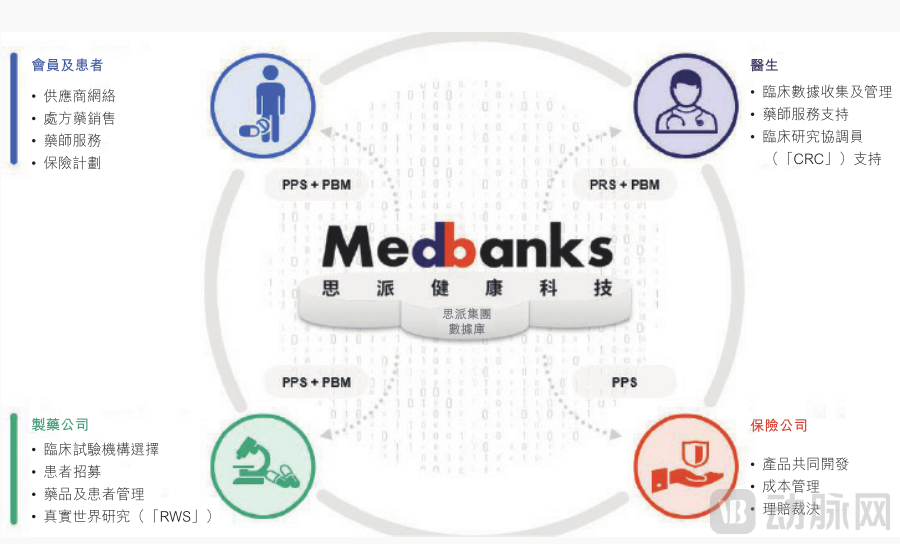

To date,Si Pai Health already has three business lines, including Physician Research Solutions (PRS), Pharmacy Benefit Management (PBM), and Provider and Payer Solutions (PPS)., the underlying logic lies in bridging the gaps among patients, pharmaceutical companies, healthcare institutions, and insurance payers, thereby establishing a closed loop of “pharmaceutical, medical, health insurance, and healthcare services.”

(Si Pai Health Revenue Data. Image Source: Prospectus)

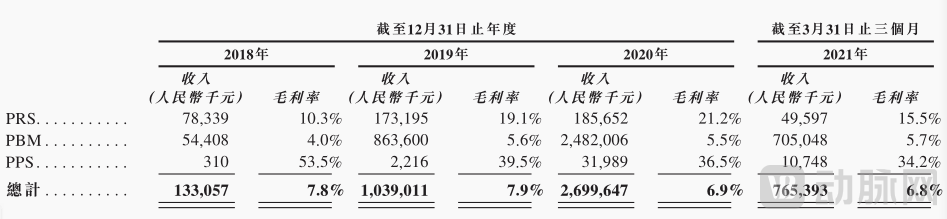

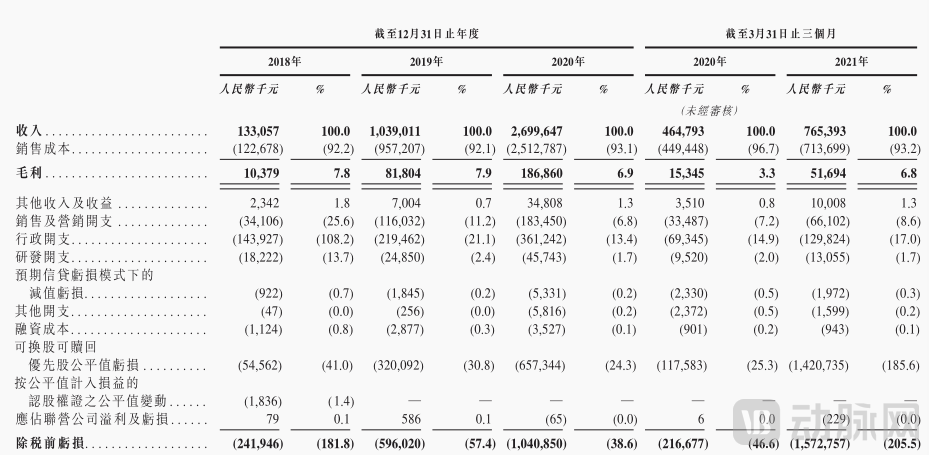

In terms of specific revenue, the prospectus shows that,Si pai Health's revenues in 2018, 2019, and 2020 were RMB 133 million, RMB 1.039 billion, and RMB 2.7 billion, respectively, reflecting very rapid growth.; In addition, Si Pai Health's revenue in the first quarter of 2021 was RMB 765 million, representing a year-on-year increase of 64% from RMB 465 million in the same period of the previous year.

Notably, according to a report by Frost & Sullivan, Si Pai Health’s oncology clinical trial site management organization (SMO) business—the core revenue contributor within its Provider Research Services (PRS) segment—ranked first in China’s oncology drug R&D sector based on full-year 2020 revenue. The scale of its Pharmacy Benefit Management (PBM) business is comparable to that of the largest private specialty pharmacy in China. Meanwhile, its Provider Payment Services (PPS) business has aggregated more than 1,100 Tier-3 Grade-A hospitals, 42,000 physicians, and 500 health examination institutions across over 100 major cities in China. It is evident that all three of Si Pai Health’s core business segments have achieved remarkable success.

(Business achievements of Si Pai Health Technology. Image source: Prospectus)

However, on the other hand, losses have been increasing year by year.The prospectus shows that Sipi Health’s losses in 2018, 2019, and 2020 were RMB 242 million, RMB 596 million, and RMB 1.042 billion, respectively; additionally, the loss for the first quarter of 2021 was RMB 1.573 billion, compared with a loss of RMB 217 million in the same period of the previous year.

On one hand, revenue is growing rapidly; on the other, losses are widening. What strategic intentions does this reflect for Sinopharm Health? What are the company’s core competitive moats? What challenges remain unresolved? In what direction will its future development evolve? To answer these questions, we may find clues by examining the founding team’s background, the company’s financial performance, and its business layout.

Since digital technologies, represented by mobile internet and AI, have gradually permeated the healthcare sector, the value of medical big data has rapidly gained prominence among industry players and investors.

ThusIn 2014, the venture capital boom in medical big data began to sweep across China, prompting entrepreneurs who sensed the opportunity to rush into this burgeoning sector., including Ma Xuguang, who formerly served as the National Head of Marketing and Sales for Bayer’s Oncology Specialty Pharmaceuticals Group. He co-founded Si Pai Health alongside Li Ji, who also worked at Bayer, and Li Dayong, who had prior experience at Pfizer and Boehringer Ingelheim. In that same year, benchmark enterprises in the medical big data sector, such as Yidu Tech and LinkDoc Technology, were also officially established.

The first step in starting a business is to set the direction.Guided by its original mission to “serve physicians” and leveraging the founding team’s background primarily in oncology pharmaceuticals, Si pai Health decided to initially focus its business on the oncology sector.

“We found that traditional data software severely constrained the clinical and research work of oncologists,” said Li Dayong, Chief Operating Officer of Si Pai Health. He stated that to enter the field of oncology big data, the first step is to improve the work efficiency of oncologists.

Based on this assessment, Si Pai Health has established customized data structure modules for each type of tumor, enabling each department to record tumor case data according to its specific needs and to query and share relevant data at any time for research, clinical practice, and case discussions.

At that time, many entrepreneurs also targeted the needs of oncologists and developed specialized products. For instance, some post-treatment follow-up tools for oncology patients also featured functionalities to assist physicians in patient management and data accumulation. HoweverThe key differentiator for Si Pai Health is its structuring of data to facilitate retrieval and statistical analysis, thereby enabling physicians to effectively apply such data in scientific research and clinical practice.

Moreover, Si Pai Health has adopted an approach of in-depth data mining for individual types of cancer. This is because, unlike chronic diseases such as diabetes and hypertension, single-disease data hold greater value in oncology. Therefore, when the platform accumulates substantial data on a specific type of cancer, it enables physicians to gain a comprehensive understanding of the disease’s clinical manifestations, thereby facilitating the provision of more effective treatment plans.

Thanks to its intense focus, Si Pai Health rapidly gained a competitive edge in the field of oncology big data within just over a year. By early 2016, the company had covered approximately 400 hospital departments, encompassed 20 types of cancer, and accumulated nearly 100,000 oncology case records.

Meanwhile, Sinopharm Health’s performance also attracted investor attention. In January 2016, the company secured a $10 million Series A financing round from F-Prime Capital Partners, Ping An Venture Capital, and Sida Capital. That June, it completed its Series B financing round, led by Tencent with participation from existing shareholders.

With capital support, Si Pai Health's business has also begun to rapidly iterate and upgrade.For example, the multi-center research-oriented database was upgraded into a management-oriented database encompassing all personnel, all data, and entire workflows, thereby facilitating the optimization and development of core medical, educational, and research activities in oncology from the most fundamental levels.

Starting from its patient clinical database and patient follow-up management system, Si Pai Health, with ample funding, is also expanding into additional business areas.By the end of 2017, Simcere Health had established business segments including SMO (Site Management Organization), RWE (Real-World Evidence), and PPO (Preferred Provider Organization for Oncology Experts), and began to expand its DTP (Direct-to-Patient) oncology pharmacy services.

It was from this point onward that SiPai Health gradually evolved beyond its singular focus on oncology big data, beginning to expand toward an ecosystem-driven model centered on a “pharmaceutical and healthcare closed loop.” This transformation drove SiPai Health’s valuation steadily upward, rapidly propelling it into the ranks of unicorns in the digital health sector.

In 2017, when Si pai Health was still widely perceived as a big data company specializing in oncology, it officially announced its entry into the DTP (Direct-to-Patient) pharmacy sector, with plans to cover 30 provinces across China and open more than 70 stores within the year. This move immediately drew significant attention from industry insiders.

It is worth noting that although DTP pharmacies had already been emerging in China for many years, the sector was crowded with players—including pharmaceutical distributors, retail pharmacy chains, and internet healthcare companies—and its business model was still undergoing market validation. Given such capital-intensive investments, Si Pai Health’s cross-industry expansion was indeed bold enough.

(Smart Health DTP Pharmacy Layout Map Source: Prospectus)

From the perspective of Mou Jian, General Manager of SiPharm Pharmacy under Sipei Health,SiPi Health’s business logic is built around aligning with the demand for oncology services, spanning from upstream pharmaceutical R&D services and midstream follow-up tools for oncologists to newly launched professional pharmacy and pharmaceutical care services targeted at patients.

“By establishing a tumor care network that spans the early, middle, and late stages of disease, we have acquired the most comprehensive and continuous oncology data, providing robust data support for cancer research and drug development,” Mou Jian stated in a previous exclusive interview with VCBeat. “Particularly in the realm of real-world studies, we have accumulated data covering the entire patient journey from diagnosis and treatment to subsequent medication adherence. This approach more accurately reflects the treatment realities of cancer patients, thereby facilitating research based on real-world data.”

In other words, as a link between in-hospital and out-of-hospital services for patients, DTP pharmacies can provide oncology medications and pharmaceutical care services, thereby capturing out-of-hospital patient data and breaking down the previous fragmentation of data between in-hospital and out-of-hospital settings.

Leveraging its integration of resources among physicians, medical institutions, and pharmaceutical companies, Si Pai Health has further streamlined commercial insurance payment channels.For example, Si Pai Health has implemented inclusive supplementary medical insurance in multiple regions and launched a new generation of corporate health and medical benefit solutions—Si Pai Health Bao. Through a model featuring proactive management by corporate physicians, Health Bao completes the commercial insurance closed loop of “risk occurrence–service–claims settlement” within Si Pai Health’s self-built healthcare ecosystem. It is rapidly expanding its reach across China, helping enterprises accelerate their development with high-quality and efficient medical services.

The addition of health insurance services has formally established Sipai Health’s closed-loop ecosystem of “pharmaceuticals, healthcare, and health insurance,” boosting its visibility in the capital markets and securing substantial financing.At the end of 2019 and 2020, Si Pai Health completed two rounds of financing, securing approximately RMB 1 billion in its Series D+ round and nearly RMB 2 billion in its Series E round.

(Specialized Health’s Business Structure. Image source: Prospectus)

How Has Sipei Health, Now Well-Equipped with Ample “Ammunition,” Performed in Building Its Closed-Loop “Pharmaceutical and Healthcare Insurance” Service Ecosystem? Next, VCBeat will analyze this from two dimensions using data disclosed in the prospectus.

Dimension 1: Nearly RMB 2.7 billion in revenue over the past two years—primarily sustained by “drug sales”?

According to the prospectus, SiMai Health’s total revenue surged by 680.9% from RMB 130 million in 2018 to RMB 1.039 billion in 2019, and further increased by 159.8% to RMB 2.699 billion in 2020, demonstrating strong growth momentum.

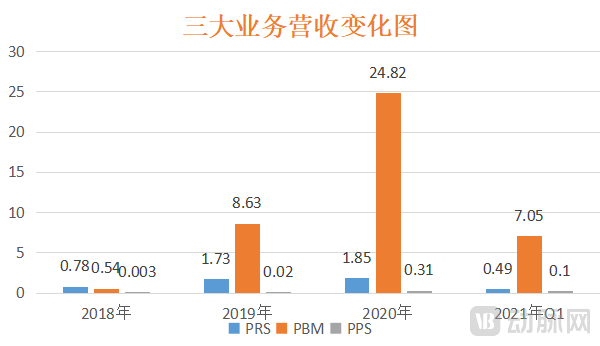

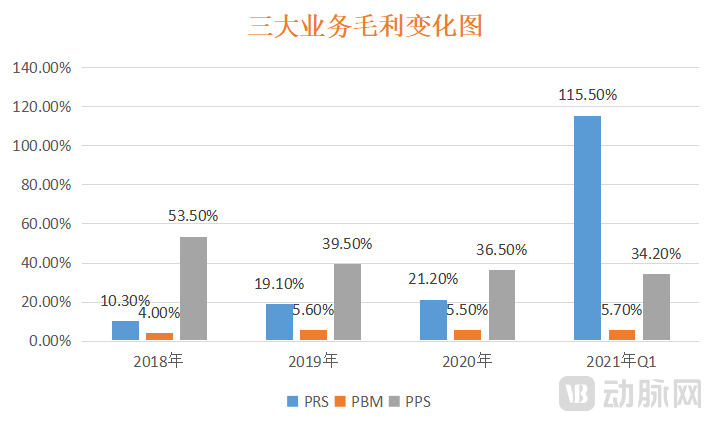

In terms of specific business operations, PRS generated RMB 185 million in revenue in 2020, with a gross margin of 21.2%; PBM generated RMB 2.482 billion in revenue, with a gross margin of 5.5%; and PPS generated RMB 32 million in revenue, with a gross margin of 36.5%. This indicates that PBM currently accounts for the majority of total revenue, while PRS and PPS make relatively limited contributions to overall revenue.From this perspective, SiPai Health Technology’s entire business model hinges on pharmacy-based “drug sales.”

ButFinancial observation is not static; rather, it should be conducted over an extended timeframe to monitor dynamic changes and identify trends.Examining SiMai Health’s three core business segments over the 39-month period from 2018 to March 2021 reveals that, in addition to the rapid growth of its PBM business, its PPS business also expanded quickly. The PPS segment’s revenue in 2020 surged more than 100-fold compared with RMB 310,000 in 2018, and its gross margin, exceeding 30%, offers greater commercial potential.

Therefore, from the perspective of business model construction, Si pai Health has already established a leading advantage in the SMO service sector within its PRS business. The company will focus on consolidating its market position in this area in the future. However, as the current scale of this business remains relatively small with average gross margins, it is considered an advantageous but not a dominant business line for Si pai Health.

Meanwhile, the PBM business currently underpins SiMai Health’s market presence due to its solid revenue-generating capability. However, given its low gross margin, the company will need to pursue further scale expansion, optimize its supply chain and logistics to reduce costs, and drive additional revenue growth in the future.

Finally, PPS serves as the core growth engine for Sinopharm Health’s long-term development. The prospectus states that Sinopharm Health Technology may unlock the commercial potential of its PPS platform through future expansion, thereby achieving scalable growth.

In summary, it is evident that Sipei Health will continue to consolidate its leading position in the PRS business, further unlock the market potential of its PBM business, and drive the rapid development of its PPS business over the medium to long term.

Dimension 2: Technology-Driven or Model-Driven?

Is Siping Health a technology-driven or business-model-driven enterprise?

Data from the prospectus shows that SiPai Health’s R&D expenditures have increased year by year, reaching RMB 18.2 million, RMB 24.8 million, and RMB 45.7 million in 2018, 2019, and 2020, respectively, indicating a consistent rise in technological investment.

(Si Pai Health Financial Data. Image source: Prospectus)

(Si Pai Health Financial Data. Image source: Prospectus)

But on the other hand,The proportion of R&D investment in revenue is showing a downward trend.In 2018, 2019, and 2020, R&D expenditures accounted for 13.7%, 2.4%, and 1.7% of revenue, respectively. Furthermore, in terms of absolute R&D investment, the figures were at an average level.

It is worth noting that although Si Pai Health’s sales and marketing expenses are on the rise, their proportion of revenue has decreased significantly. The prospectus shows that in 2018, 2019, and 2020, the sales and marketing expenses were RMB 34 million, RMB 116 million, and RMB 183 million, respectively, while the ratio of sales and marketing expenses to revenue was 25.6%, 11.2%, and 6.8%, respectively.This indicates that, driven by the maturity and scale of its three core business segments, Sipai Health has achieved a significant reduction in sales and marketing expenses.

Therefore,Overall, Si Pai Health is more of a model-driven enterprise and has gained significant advantages in building a “pharmaceutical and healthcare closed-loop.” The core focus moving forward remains on deepening and optimizing the entire service loop to reduce operating costs, achieve greater economies of scale, and serve a larger population with higher-quality services.

China's health management and health insurance industries are entering a phase of rapid development.

From a macro perspective, China’s new healthcare reform, centered on the “three-medical linkage” model, has gradually entered a critical phase after ten years of implementation. In February 2020, the State Council issued the Opinions on Deepening the Reform of the Healthcare Security System, further clarifying the need to accelerate the establishment of a multi-tiered healthcare security system and promote reforms in payment methods and supply-side structural reforms of pharmaceutical and medical services.

Driven by strong policy support,China’s healthcare delivery, medication use, and payment systems are accelerating their optimization, moving toward a multi-tiered medical security framework. Markets such as out-of-hospital prescriptions, online consultations, commercial health insurance, and health management are also entering a phase of rapid growth.

Manifested at the industry level, it appears as# Industry Sees Continuous Large-Scale Financing as Leading Companies Rush Toward IPOs. For instance, since last year, companies such as Yuanxin Technology and Magin Health have successively secured billions in financing, and Waterdrop Inc. successfully went public in the first half of this year.

On the other hand,Significant challenges remain for the industry to overcome in establishing a closed loop between “health management” and “health insurance.”For instance, challenges such as information asymmetry, low levels of specialization, high loss ratios, and weak profitability still stand in the way of all market entrants.

In contrast, the U.S. health insurance and health management market has already given rise to industry giants such as UnitedHealth Group. As a constituent of the S&P 500 Index, UnitedHealth Group has seen its stock price increase more than 15-fold over the past decade, with annual revenue now exceeding $240 billion.

Specifically, UnitedHealth Group’s integrated model primarily comprises two components: insurance coverage and health services, with numerous innovations in this field. For instance, in 1988, UnitedHealth pioneered the Pharmacy Benefit Management (PBM) business, linking benefit design with retail pharmacy networks and offering mail-order prescription services. The core rationale behind this innovative business model was to leverage economies of scale in price negotiations with pharmaceutical manufacturers and pharmacies, thereby helping consumers better control prescription drug costs.

(UnitedHealth Group Building; Image source: company website)

By 1995, UnitedHealth Group had acquired MetraHealth for $1.65 billion, a company formed by integrating the group health businesses of Travelers Insurance Company and Metropolitan Life Insurance Company. At this point, UnitedHealth Group possessed the nascent form of its “pharmaceutical and healthcare closed-loop” model.

In its subsequent development, UnitedHealth Group continuously expanded its business boundaries and deepened its services. For instance, in insurance product design, it added prescription drug coverage to its existing inpatient medical benefits, which helped unlock the senior market.

As can be seen, by acting as the payer, insurance has enabled the integration of “pharmaceuticals, healthcare, and health services,” helping UnitedHealth Group set its business model flywheel in motion.Driven by massive economies of scale, UnitedHealth Group has ultimately become a behemoth in the health insurance and healthcare management sectors, with a market capitalization exceeding RMB 2 trillion. According to the latest Fortune Global 500 list, UnitedHealth Group ranks eighth overall, making it the second-largest company in the healthcare sector.

Judging by UnitedHealth Group’s trajectory, the health ecosystem being built by Si Pai Health aligns closely with that of UnitedHealth, suggesting significant market potential for Si Pai Health from a strategic standpoint. However, it is important to note that medical and healthcare services represent the most complex and challenging segment of the broader health industry. Therefore, Si Pai Health must continue to deepen and refine its medical service offerings and withstand the test of time.

From this perspective, Si Pai Health’s latest push for an IPO does not signal that it is nearing the finish line; rather, it marks a new starting point. Only time will tell what the future holds.