Gene Testing Sector Attracts Over $1.1 Billion in H1, Driven by Four Major Shifts

MGI

Gene Sequencing Instruments and Related Reagent & Consumables R&D Manufacturer

Few medical sectors can match the sustained vitality of genetic testing, which remains vibrant even after years of continuous hype.

In the first half of the year, genetic testing projects in the primary market secured over RMB 7 billion in financing, while the secondary market welcomed three newly listed genetic testing companies, creating a combined market capitalization of nearly RMB 58 billion. Investors, practitioners, and consumers in the genetic testing sector are all becoming more mature. In light of the revision to the Regulations on the Supervision and Administration of Medical Devices, intensified competition among upstream technology platforms, and the rise of computational power and algorithms for front-end omics data, what transformations are underway in the R&D paradigm for genetic testing products?

In the first half of the year, early cancer screening remained the hottest trend in the genetic testing industry. However, as commercialization efforts continue to advance, many early cancer screening companies have begun to show signs of diverging paths. After years of intense competition in the red ocean of tumor NGS (Next-Generation Sequencing), will emerging and more specialized scenarios such as new drug development and MRD (Minimal Residual Disease) create new blue oceans?

With capital and policy in one hand, and technology and application scenarios in the other, what risks and opportunities lie beneath the surging popularity of genetic testing?

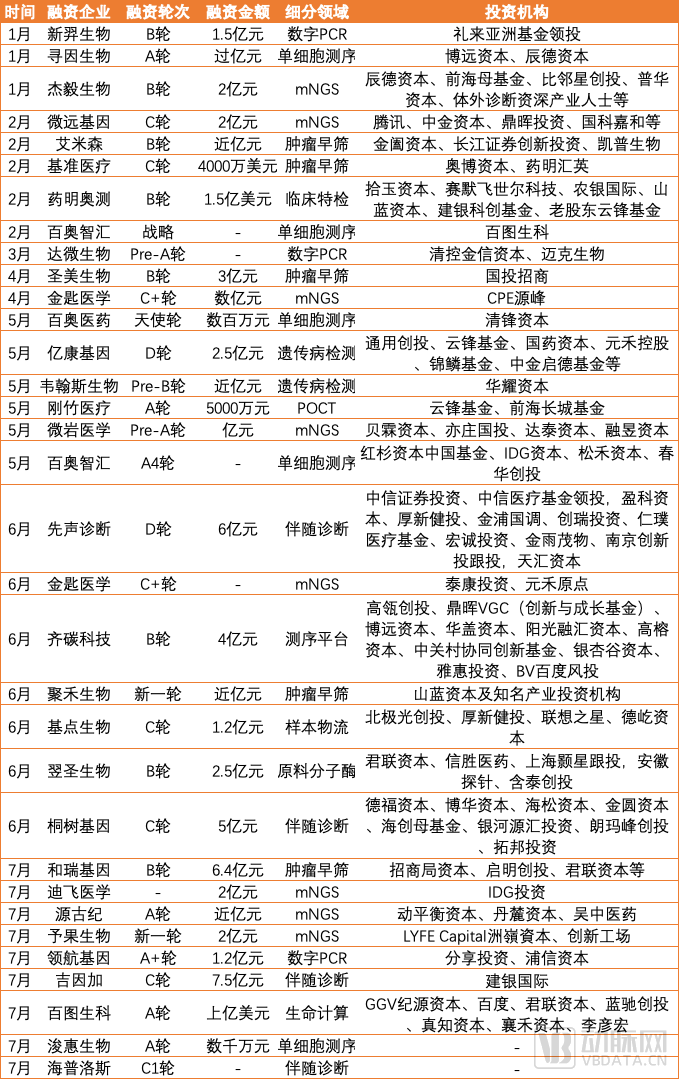

According to statistics from VCBeat, in the first half of 2021, a total of 30 companies in the genetic testing sector completed 32 rounds of primary market financing, with a cumulative amount exceeding RMB 7 billion. Among these, metagenomic next-generation sequencing (mNGS), early cancer screening, single-cell sequencing, and companion diagnostics remained investment hotspots in the genetic testing sector, attracting more than 65% of all funds invested in this sector during the first half of the year.

As of press time, financing in China’s genetic testing sector in 2021

For genetic testing financing in the first half of the year, maturity of the industry chain is an unavoidable keyword. This maturity is reflected in aspects such as funding rounds, product progress in funded sectors, and the position of funded companies within the industry chain.

First, let’s look at the funding rounds. In the first half of the year, apart from sporadic angel, Pre-A, and Series A financing events, all other deals were mid-to-late stage financings (Series B and beyond), with transaction amounts rising primarily from the millions or tens of millions to the hundreds of millions. Taking the mNGS sector as an example, star projects that have remained active over the past two years—such as Jieyi Biology, Weiyuan Genomics, Jinshi Medicine, and Yuguobiology—have successively closed new rounds of financing. GenoDx, a leading company in companion diagnostics, also recently disclosed financing for its mNGS business, successfully bringing IDG Capital on board as an investor.

mNGS financing has entered later-stage rounds, with transaction amounts consistently surpassing the RMB 200 million threshold. This trend is driven partly by the escalating costs of mNGS product development as clinical research advances, and partly by the capital market’s continued optimism about this sector. Notably, in the aforementioned mNGS financing deals, most early-stage investors have chosen to follow on in later rounds. For instance, Proxima Ventures increased its stake in Jieyi Biology during Series B after investing in its Pre-A round, while CAS Star invested in Weiyuan Genomics across Series A, B, and C rounds.

Next, let us examine product progress. Financing interest in early cancer screening and single-cell sequencing began to rise in the second half of last year and has continued through the first half of this year. In early July, Berry Genomics announced that its subsidiary, Huirui Gene, had completed a RMB 640 million Series B1 financing round, marking the largest financing deal for an early cancer screening company in the first half of the year. Since its inception, Huirui Gene has raised nearly RMB 2 billion in total, setting a new record for primary market financing by domestic early cancer screening companies.

Bolstered by capital investment, the maturity of early cancer screening products has further improved, with frequent developments in large-scale prospective cohort studies, commercial implementation, and product registrations. For instance, Imagen’s colorectal cancer early screening product, Ai Changkang, and its cervical cancer early screening product, Ai Gongshu, obtained EU CE certification in the first half of the year, while Burning Rock Biotech’s bladder cancer early screening product received the U.S. FDA’s Breakthrough Device Designation.

By examining the positions of funded companies within the industrial chain, an upward trend in the gene testing sector becomes evident. In the first half of the year, Qitan Technology, Basepoint Biology, and Yeasen Biotechnology completed Series B, Series C, and Series B financing rounds, respectively, raising a total of nearly RMB 800 million. Their primary focus areas—single-molecule sequencing platforms, biological cryopreservation systems, and molecular enzymes—all belong to the upstream segment of the gene testing service industry. Furthermore, Fibio and Vazyme, both suppliers of upstream raw materials for gene testing, are poised for initial public offerings. This indicates that capital market recognition of the gene testing sector has extended beyond the midstream and downstream service segments.

In terms of IPOs, the first half of the year continued and amplified the momentum from the previous year’s concentrated listings of two genetic testing companies, Burning Rock Biotech and Genetron Health. New Horizon Health, Rayagene, and Novogene all made their debuts in the capital markets. This marks another wave of IPOs in the genetic testing sector, following the listings of BGI Genomics and Berry Genomics in 2017 three years prior. Unlike the previous IPO boom, when genetic testing entered the secondary market as a novel technology, the capital market now has a more mature understanding of the technology itself. Companies must now convince the market through a combination of technology, products, and application scenarios.

Among them, New Horizon Health and Novogene claimed the titles of “China’s First Stock in Early Cancer Screening” and “China’s First Stock in NGS Research Services,” respectively, while Ruisen Genes, specializing in molecular diagnostics for hematologic diseases, joined the ranks of listed IVD companies. As of press time, Novogene’s share price had doubled from its initial offering price.

With CapBiotech investing in Amsino, Thermo Fisher Scientific investing in WuXi Diagnostics, and IVD industry veterans investing in Jieyi Biotechnology, it is becoming evident that the logic of industrial M&A is extending into the genetic testing sector. Such consolidation serves as a key indicator of the industry’s vigorous growth. Spillover effects from the transformation of the IVD industry driven by COVID-19 testing have led some insiders to predict that China’s genetic testing field will enter a period of explosive growth within the next two to three years. At that time, horizontal integration across channels and products, as well as between diagnostics and therapeutics, will reshape the competitive landscape of the entire market.

In the first half of the year, two and a half major events occurred in the upstream sector of genetic testing.

The first major development is the clarification of regulatory rules brought about by the revision of the Regulations on the Supervision and Administration of Medical Devices. Previously, most clinical genetic testing projects had not obtained product registration certificates and were classified as in vitro diagnostic (IVD) tests developed, validated, and used exclusively within laboratories, known as the Laboratory Developed Tests (LDT) model. Although this model is common abroad, and the flexibility of LDTs in terms of technical platforms and reagent selection is better suited for the implementation of cutting-edge technologies such as genetic testing.

However, regulatory risks have always been inherent to the Laboratory Developed Tests (LDT) model. On March 18, the State Council promulgated the revised Regulations on the Supervision and Administration of Medical Devices, which came into effect on June 1. Article 53 of these regulations has significantly boosted confidence within the genetic testing industry. Article 53 stipulates that for in vitro diagnostic reagents for which no equivalent products are yet marketed domestically, eligible medical institutions may, based on their clinical needs, independently develop such reagents and use them within their own facilities under the guidance of licensed physicians. Specific administrative measures shall be formulated by the drug regulatory department of the State Council in conjunction with the health administrative department of the State Council. Since the requirements for “independent development” and “use within the institution” closely align with the LDT model, industry participants view this as a trend toward the legalization of the LDT model.

More importantly, the legalization of the Laboratory Developed Tests (LDT) model may give rise to a parallel registration pathway for LDT reagents alongside In Vitro Diagnostics (IVD). This development is undoubtedly a significant boon for LDT companies that are at the forefront of clinical needs and whose relevant products lack equivalent alternatives on the market. Although in practice, LDT companies have sought to legitimize their operations through external quality assessment programs or by having specific test items endorsed on their PCR laboratory accreditation certificates, this indirect form of certification offers limited protection for LDT enterprises amid market disruptions and regulatory pressures.

Subsequently, the National Medical Products Administration (NMPA) and the Standardization Administration of China issued the “Opinions on Further Promoting High-Quality Development of Medical Device Standardization,” which proposed advancing the development and revision of standards in areas such as novel molecular diagnostic technologies including high-throughput sequencing, clinical mass spectrometry, companion diagnostic reagents, point-of-care testing, and traceability and reference measurement systems. On May 28, the NMPA approved the Center for Medical Device Standardization Management to formally establish the centralized technical unit for medical high-throughput sequencing standardization. This demonstrates that, despite the uncertainties brought by innovation, regulatory support for the clinical application of genetic testing is clear.

The second major development is the announcement by Illumina, the global leader in gene sequencing and chip solutions, and Sequoia Capital China Fund, a leading investment institution, of their joint establishment of an Intelligent Medical Genomics Incubator dedicated to supporting life sciences startups. It is not unprecedented for multinational corporations to set up innovation incubation centers in China; AstraZeneca, Merck & Co., and Microsoft are among those that have done so. However, what makes Illumina’s move particularly noteworthy is the shift in attitude demonstrated by this giant, whose technical platform commands nearly 90% of China’s gene sequencing market, toward the domestic clinical market. This also hints at the complex changes underway in the competitive landscape of the upstream gene testing sector.

Illumina’s Monopoly in the Upstream Gene Sequencing Market Appears to Be CrumblingOn July 20 local time, PacBio and Omniome signed a definitive merger agreement, under which PacBio will acquire Omniome for $800 million. PacBio has a longer history than Illumina in the development and commercialization of gene sequencers and holds an absolute advantage in high-quality long-read sequencing platform technology. Omniome’s core product is a high-quality short-read sequencing platform, and its SBB (Single Base Binding) sequencing technology closely mirrors Illumina’s proprietary SBS (Sequencing by Synthesis) approach. The combination of PacBio and Omniome will unite long-read and short-read sequencing capabilities, creating a synergistic force that is poised to challenge Illumina’s long-standing monopoly in the short-read sequencing market.

Challenges also arise domestically. In China, during the first half of the year, major and minor players such as BGI Genomics, Annoroad Gene Technology, Denovo Genomics, and Yuewei Genomics have entered the upstream market or clinical application scenarios with their independently developed gene sequencers.

At the 2nd Innovation Forum on Diagnostic Technologies for Infectious Diseases (IDD), MGI unveiled the DNBSEQ-E5 gene sequencer for the first time. Comparable in size to a laptop, this sequencer can generate SE50 output data in as little as 4.5 hours, enabling rapid response to urgent sequencing needs for special samples and facilitating quick detection of unknown pathogenic microorganisms.

Furthermore, in the first half of the year, Deno Jieyi and Yuewei Genomics each obtained product registration certificates for their independently developed gene sequencers. Both of these gene sequencers are based on first-generation sequencing technology, namely Sanger sequencing. Among them, Yuewei Genomics’ Zhiyue Gene Analyzer GenReader 7010 is specifically designed for clinical use. It is a four-channel gene analysis system that supports both Sanger sequencing and fragment analysis on the same reaction plate, and is compatible with 8-tube strips and 96-well plates. Its open detection platform enables simultaneous testing for multiple projects. Meanwhile, Anxuyuan entered the European market through Russia’s Generis Biotech.

The final half-item is biological computing, which gained significant traction in the first half of the year. As it remains in its nascent stages, its impact on China’s genetic testing market during this period can only be considered a partial major development. Nevertheless, advancements in biological computing power and algorithms will undoubtedly transform genetic testing practices. Biological computing companies, represented by BioMap, have begun establishing collaborative ecosystems with numerous genetic testing firms. By integrating sample throughput with omics data, biological computing—characterized by “big data + computing power”—provides a new foundation for the development of tumor genetic testing products.

For instance, from a technical perspective, transitioning from “supervised learning” to “unsupervised learning”; and from a product perspective, integrating IoT home products, consumer internet data, and online family doctor services to continuously collect and consolidate personal data, thereby enabling genetic testing for specific regions, populations, and scenarios, and even adopting a “C2B” R&D model.

In the first half of the year, Professor Wang Xiaowo’s team from the Department of Automation at Tsinghua University published DISMIR, a deep learning-based algorithm, in *Briefings in Bioinformatics*. This algorithm enables high-precision cancer detection using whole-genome bisulfite sequencing (WGBS) data of plasma cell-free DNA (cfDNA). Even after downsampling the test data to 1% of the original depth (sequencing depth of 0.01×–0.1×), DISMIR maintained an area under the curve (AUC) of approximately 0.9. Together with cfDNApipe, an integrated analysis software package for cfDNA sequencing data previously released by Professor Wang’s team, DISMIR forms a comprehensive end-to-end solution for cfDNA liquid biopsy data interpretation. Meanwhile, AlphaFold2, a newly designed neural network-based version of AlphaFold demonstrated by the DeepMind team, has achieved atomic-level accuracy in protein structure prediction, thereby providing more options for biomarker selection in genetic testing.

Therefore, in the first half of the year, changes in regulation, the industry chain, and digital infrastructure have transformed the R&D paradigm for genetic testing. While compliance and technical costs have decreased, the overall entry barrier has significantly increased.

After years of intense competition and fluctuating fortunes in clinical applications, tumor NGS companies have become more deeply intertwined with pharmaceutical companies’ new drug R&D. Beyond serving as companion diagnostic reagents to screen patients for marketed drugs, they have also entered new drug clinical trials, providing services to optimize outcomes for pharmaceutical companies.

In fact, tumor NGS companies have long provided precision medicine services to pharmaceutical companies. Some tumor NGS companies originally originated from pharmaceutical companies, such as Yuheng Pharmaceutical and Rendong Medicine, Simcere Pharmaceutical and Simcere Diagnostics, Belta Pharma and Ruipu Gene, etc. In the first half of the year, Burning Rock Biotech, AmoyDx, Quest Medical, Rendong Medicine, Genetron Health, and others successively announced progress in their pharmaceutical company service businesses. Judging from the timeline of cooperation, they have all been involved, to varying degrees, in clinical trials conducted by pharmaceutical companies.

For example, in March, CStone Pharmaceuticals’ pralsetinib capsules received conditional marketing approval in China through the priority review pathway under the brand name Gavruto. As the first RET inhibitor approved in China, it is indicated for adult patients with locally advanced or metastatic non-small cell lung cancer (NSCLC) who are positive for rearranged during transfection (RET) gene fusions and have previously received platinum-based chemotherapy. In June of the previous year, Burning Rock Biotech partnered with CStone Pharmaceuticals to develop a companion diagnostic for pralsetinib, planning to launch the OncoScreen Mate (DNA+RNA) fusion detection product.

Furthermore, in July, the Tajhwa companion diagnostic kit—Human PDGFRA Gene D842V Mutation Detection Kit (PCR-Fluorescent Probe Method)—jointly developed by Genetron Health and CStone Pharmaceuticals, received priority review from the National Medical Products Administration (NMPA), marking a pioneering attempt at the co-development model with new drugs.

In the past, pharmaceutical services provided by tumor NGS companies exhibited significant customization, with no standardization in functional positioning or service scope. This situation has improved in the first half of this year. In early June, the Center for Drug Evaluation (CDE) of the National Medical Products Administration released the "Technical Guidelines for the Application of Biomarkers in the Clinical Development of Anti-tumor Drugs (Draft for Comments)" (hereinafter referred to as the "Guidelines").

“The Guiding Principles,” on the one hand, clarify from the perspective of drug regulators that biomarkers have gradually become an essential tool in the development of anti-tumor drugs, and for the first time affirm their role in precisely identifying potential beneficiary populations, improving the success rate of clinical trials, and avoiding exposing patients with a low likelihood of benefit to unnecessary risks. On the other hand, they specify certain technical details; according to the “Guidance Opinion,” biomarkers include gene mutations, abnormal protein receptor expression, and changes in blood components. The “Guidance Opinion” also clarifies the roles of different types of biomarkers in subject stratification, population enrichment, dose selection guidance, and surrogate endpoint development in new drug clinical trials.

2021 was regarded by the industry as the first year of commercialization for early cancer screening.

Cancer Early Screening, with Its Vast Potential, Appears Poised for a True Explosion. In early June (local time), GRAIL presented prospective clinical trial data at the 2021 ASCO Annual Meeting, validating the clinical value of Galleri, which is now available by prescription in the United States. This news has significantly boosted confidence in China’s cancer early screening market. During the Two Sessions, Yu Jinming, a deputy to the National People’s Congress, an academician of the Chinese Academy of Engineering, and president of Shandong Cancer Hospital, recommended incorporating cancer screening into the national medical insurance system.

In the first half of the year, DNA methylation, as a mainstream technical approach for early cancer screening, was widely adopted in the development of more products. However, the iteration of technical approaches has never ceased, such as the application of mass spectrometry technology to early lung cancer screening. Nevertheless, what may be most noteworthy is the updated understanding among various companies regarding the underlying logic of early cancer screening itself, which has given rise to two distinctly different commercialization paths: one focused on serving public welfare and the other on cross-industry integration.

In a sense, participation in government-led public welfare initiatives is not purely commercial. At the current stage, the more significant value of such initiatives for early cancer screening enterprises lies in acquiring big data at a high cost. Through this process, the superior positive predictive capability of early cancer screening products compared to traditional screening tools is validated and optimized, ultimately quantifying their health economic benefits. In the first half of the year, companies such as Genron Bio, BGI Genomics, Geneseeq Technology, and Tellgen Corporation participated in numerous government public welfare projects.

Overall, government livelihood projects are characterized by their large scale and long duration. For instance, in June, the Jiangsu Government Procurement Network announced that the Health Bureau of Taizhou Medical High-Tech Zone and the Health Commission of Gaogang District, Taizhou City, planned to procure Helicobacter pylori nucleic acid testing based on stool samples and early colorectal cancer screening technology from Dingjianwei Medicine with a budget of RMB 50 million. The latter is an affiliate of Canhelp Genomics, a company with higher industry recognition.

Similarly, the Jinling Cohort, a large-scale public welfare project for early cancer screening launched in June, announced the completion of its pilot phase at the first site, where 262 residents underwent early cancer screening within 12 days. Supported by the Health Commission and Civil Affairs Bureau of Nanjing Jiangbei New Area, and spearheaded by Academician Shen Hongbing of the Chinese Academy of Engineering, the Jinling Cohort brings together professional teams from Nanjing Medical University and Geneseeq to provide 100,000 free early cancer screening tests to Nanjing residents. It is reported that Phase I of the Jinling Cohort will benefit approximately 15,000 eligible residents aged 45–75 in the Jiangbei New Area, focusing on screening for lung cancer, colorectal cancer, and liver cancer, with a five-year follow-up period.

Another approach is cross-sector collaboration. This path typically engages users directly, leverages product qualifications as a foundation, and emphasizes the negative predictive value for tumors, with the aim of increasing market penetration and scaling up product volume.

For instance, collaborating with commercial insurance. Currently, there are two primary models for the collaboration between early cancer screening and commercial insurance: front-end and back-end. In the front-end model, users receive health insurance coverage benefits when purchasing early cancer screening products, representing a relatively traditional "product + insurance" model. The back-end model targets individuals with pre-existing conditions by integrating early cancer screening products into insurance policy terms, thereby driving customer acquisition through commercial insurance channels. This model is predominantly seen on internet insurance platforms, such as the partnership between Huirui Gene and Ali Health, which provides coverage for hepatitis B patients.

Furthermore, by collaborating with the medical marketing departments of large pharmaceutical companies, these firms leverage the latter’s healthcare resources to penetrate hospital settings. For instance, Genetron Health and Chia Tai Tianqing signed an exclusive strategic cooperation agreement in China for HCC Screen, a liver cancer early screening product based on liquid biopsy technology. New Horizon Health also announced a three-year collaboration plan with AstraZeneca China at the beginning of the year.

Furthermore, New Horizon Health, which secured China’s first approval for cancer early screening, has adopted a more diversified approach to cross-industry collaboration. In addition to partnering with internet healthcare platforms such as JD Health and Ali Health for promotion, the company has extended its consumer-facing channels for tumor early screening into professional medical live-streaming, leveraging the substantial traffic from short-video platforms like Douyin and Kuaishou. Among the commercialization pathways currently observed for tumor early screening, the direct-to-consumer (DTC) model represents the most significant disruption to the traditional distributor-based business model of the in vitro diagnostics (IVD) industry and may also enable the most rapid scale-up. The key question moving forward is how New Horizon Health will achieve true market penetration.

In practice, whether serving public livelihood needs or facilitating cross-sector linkages, despite differing underlying logics, the significance for the early cancer screening industry remains consistent: namely, to expand market coverage at scale. Both approaches also face challenges in areas such as product integration and resource alignment. The performance during the inaugural year of commercialization for the early cancer screening sector still requires more data for thorough evaluation.

New Hotspot: It Will Take Another 5 Years to Validate the Clinical Value of MRD

Monitoring of Minimal Residual Disease (MRD) was an absolute hotspot among new scenarios for genetic testing in the first half of the year. Vendors providing in-house genetic testing services have either already developed MRD products or are in the process of preparing to develop such products.

According to incomplete statistics from VCBeat, since 2021, companies such as Tree Genetics, Huidu Medical, Genetron Health, and ZhiBen Medical have successively launched their own MRD monitoring products. Notably, FanYin Medicine’s blood cancer MRD detection product has obtained CE certification from the European Union, marking its entry into overseas markets. Furthermore, the results of the first domestic multicenter prospective study on colorectal cancer MRD, jointly conducted by Geneseeq Technology and research institutions including Sun Yat-sen University and Fudan University, were officially published in the Journal of Hematology & Oncology. HeRui Gene also plans to expand into the MRD sector in the second half of the year.

Meanwhile, the clinical community has also shown strong recognition of the application of MRD. For instance, at the 18th China Lung Cancer Summit Forum, the first Chinese “Consensus on Detection and Clinical Application of MRD in Lung Cancer” was released. The consensus clearly defines lung cancer MRD as cancer-derived molecular abnormalities that are undetectable by conventional imaging (including PET/CT) or laboratory methods after treatment, but can be identified through liquid biopsy. Examples include the stable detection of ctDNA with an abundance ≥0.02% in peripheral blood, encompassing lung cancer driver genes or other Class I/II gene variants, which indicates the persistent presence of lung cancer and the potential for clinical progression.

It is not difficult to observe that identifying new high-demand application scenarios—from non-invasive prenatal testing (NIPT) and tumor next-generation sequencing (NGS) to metagenomic next-generation sequencing (mNGS) and early cancer screening—has consistently been a viable strategy for both newcomers and veterans in the genetic testing industry. However, it may be premature to consider minimal residual disease (MRD) detection as a panacea for the saturated tumor NGS market. At the 2021 Fudan Zhongshan Liquid Biopsy Clinical Application Summit held in July, Professor Wu Yilong stated in his keynote address that it would take approximately five more years to fully validate the clinical value of MRD.

Indeed, the implementation of any genetic testing product is accompanied by the standardization of technical details and repeated validation of its clinical value, and this holds true for MRD as well. Once the application of MRD is widely adopted, it will undoubtedly create a niche market in genetic testing that is even larger in scale than the companion diagnostics segment.

Concerns about the genetic testing sector being prematurely accelerated by capital have been persistent. However, it is an indisputable fact that R&D investment ratios at genetic testing companies are significantly higher than those in the traditional IVD industry. After years of development, genetic testing has acted as a trailblazer, resolving many complex challenges in the diagnosis of genetic disorders, tumors, and infectious diseases, thereby amplifying the clinical prominence of relatively high-end specialized tests.

In the future, the consolidation of routine clinical laboratory tests and the specialization of specialized testing will undoubtedly be the development trend in medical diagnostics. For genetic testing companies, technological barriers constitute an inherent advantage; however, aligning with genuine clinical needs, and even broader health and wellness demands, remains a critical challenge to address as they advance rapidly.