Navigating the Next Chapter of Cancer Early Screening: Investment Frenzy Meets Strategic Breakthrough

In 2015, China’s early cancer screening industry began to take off. From 2015 to 2019, the industry experienced steady development, with technologies gradually maturing and several auxiliary diagnostic products entering the market. Starting in 2020, the sustained high growth of leading companies such as Exact Sciences highlighted the vast potential of China’s early cancer screening sector, sparking a surge in industry interest. Both the size and frequency of individual financing rounds far exceeded those of previous years, leading 2020 to be hailed as the “Year One” of early cancer screening.

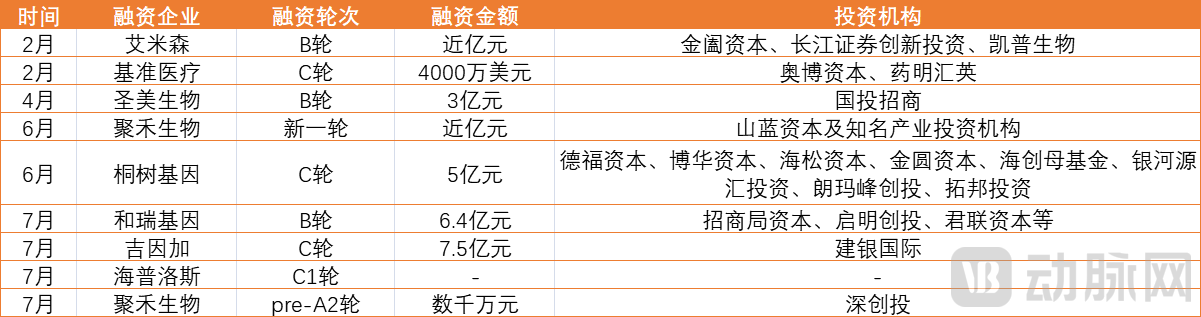

In 2021, the cancer early screening sector continued its rapid growth momentum from 2020. In the first half of the year, China saw its first publicly listed company whose core revenue source was cancer early screening services. Multiple new enterprises announced their entry into the cancer early screening market, while several prospective clinical studies achieved breakthroughs. The frequency and volume of financing remained at high levels, gradually clarifying the industry’s prospects.

Financing Status of Early Cancer Screening Companies from January 1 to July 31, 2021

However, it is also evident that competition in the early cancer screening sector is becoming increasingly fierce. Industry insiders have remarked, “2021 was a breakthrough year for early cancer screening.” In this context, building differentiated competitive advantages has become crucial. How can companies find a path to break through? How can they establish differentiated development strategies? And how can they accelerate growth with capital support? Addressing these questions, Zhang Lianglu, founder of Ameson, shared his insights in a recent exclusive interview with VCBeat.

With the large-scale commercialization of Cologuard and its diversified product development capabilities driven by a combination of in-house R&D and mergers and acquisitions, Exact Sciences has become one of the most successful companies globally in early cancer screening. In the uncharted territory of early cancer screening technology development, a company’s success hinges on a diversified product portfolio and the establishment of an early cancer screening platform, particularly its capability in identifying detection targets.

Currently, early cancer screening products are mainly divided into(1) Algorithmic interpretation of the target panel; (2) Detection of specific targets.Among these, assays for specific targets are increasingly becoming the mainstream testing modality for early cancer screening products.There are relatively few mature cancer early screening products available internationally, and China’s cancer spectrum differs significantly from that of Europe and the United States; therefore, a multi-product strategy heavily relies on a company’s own target discovery capabilities.

The “discriminatory power” of tumor biomarkers is the core competitiveness of companies specializing in early cancer screening. Zhang Lianglu stated that for cancers such as colorectal cancer, where mature early-screening products already exist both internationally and domestically, most companies opt to develop their products by referencing established biomarkers. However, for many other cancer types, both China and other countries are still in the early stages of development, with no mature reference products available. This is particularly true for cancers with high incidence rates among the Chinese population, such as esophageal cancer, liver cancer, and endometrial cancer, where the ability to identify and validate appropriate biomarkers becomes especially critical.“Without the capability to identify therapeutic targets, companies will be unable to make any headway when confronting cancer types for which there are no established reference targets internationally.”

Amyson has made significant strategic investments in the research and development of oncology target identification.Over the years, multiple targets closely associated with the onset and progression of esophageal cancer, liver cancer, gastric cancer, bladder cancer, pancreatic cancer, and other malignancies have been identified.To support the company’s diversified product portfolio and achieve multi-target precision diagnostics. To date, it has secured over 40 patents, many of which cover detection targets that are either first-in-class discoveries or first-to-market commercializations, with several applications filed under the Patent Cooperation Treaty (PCT).Exclusively licensable detection targets will serve as the foundation for multi-product portfolios in early cancer screening enterprises, and act as a moat for product internationalization and the establishment of competitive barriers.

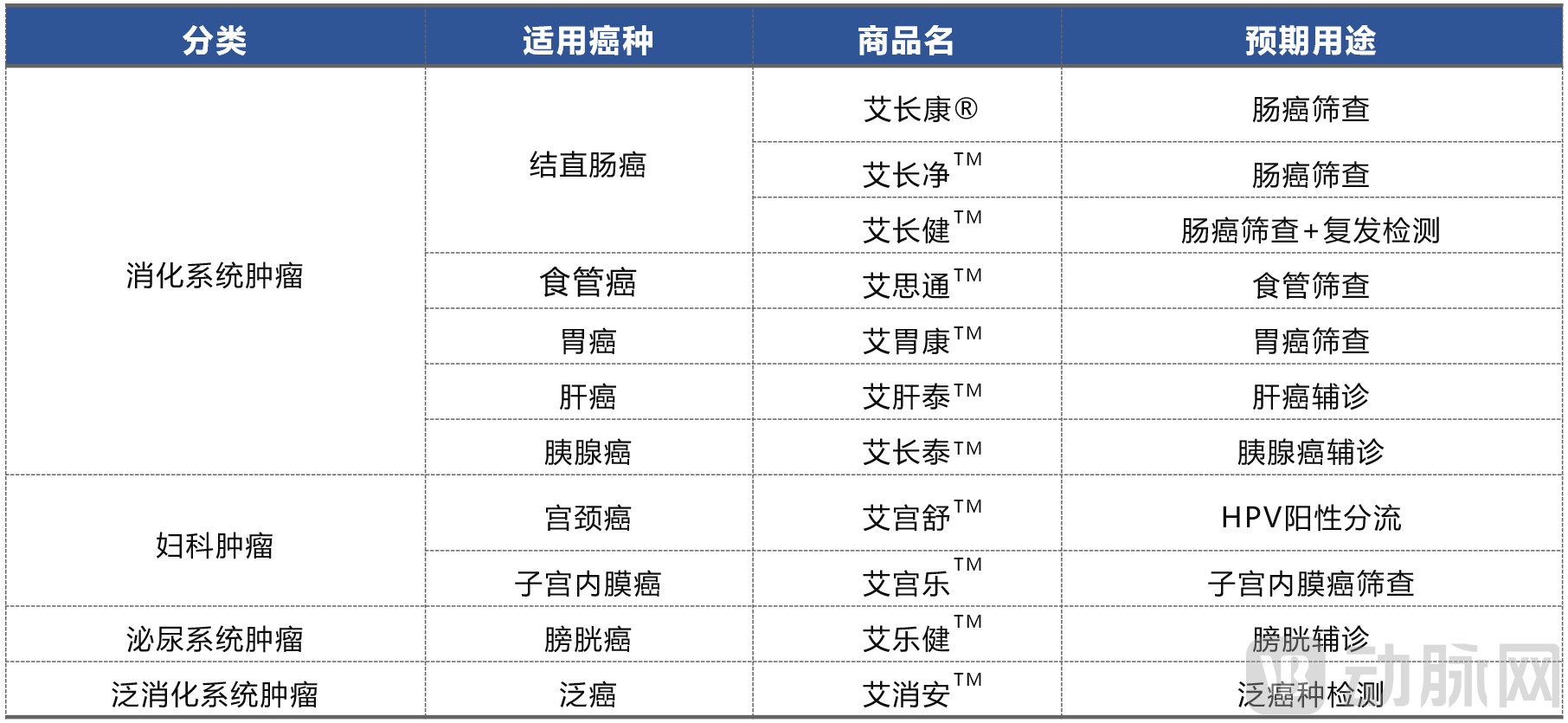

In terms of product portfolio, Amison has established a diversified lineup covering digestive system tumors, gynecological tumors, urological tumors, and pan-cancer early screening. Specifically, in the field of digestive system tumors, Amison has developed solutions for five major cancer types: colorectal cancer, esophageal cancer, liver cancer, gastric cancer, and pancreatic cancer. In gynecological tumors, it has focused on cervical cancer and endometrial cancer. The company has secured a leading advantage in the completeness and richness of its product pipeline.

Aimisen's Diversified Product Portfolio

In terms of precise target-based diagnostics, Ameson’s “Aichangkang” innovatively adoptsDual Methylation Target Detection Technology. The dual-target product exhibits a high Youden index. By employing a dual-target detection combination with strong complementarity, “Ai Changkang” achieves a sensitivity of up to 93.4% and a specificity of up to 94.6%, demonstrating high sensitivity for the detection of colorectal cancer and adenomas (precancerous lesions). Furthermore, the personnel efficiency ratio of “Ai Changkang” is more than 10 times that of Cologuard, making it suitable for large-scale population screening for colorectal cancer.

There are two revenue models for early cancer screening products: Laboratory Developed Tests (LDTs) and In Vitro Diagnostics (IVDs). LDTs refer to the provision of testing services, while IVDs refer to reagent products that can only be sold after obtaining approval from regulatory authorities such as the NMPA and the FDA. Currently, most early cancer screening companies adopt the LDT model. Compared with the IVD model, the LDT model reduces the time required for regulatory review and approval, enabling faster market entry and generation of sales revenue.

However, it must be clarified that LDTs can only serve a limited number of patients, which contradicts the original intention and philosophy of early cancer screening. Meanwhile, issues such as regulations, costs, and quality control determine thatLDTs are unlikely to remain the mainstream model in the long term.Based on the experience of previous domestic early cancer detection products, Helicobacter pylori testing, HPV testing, TCT testing, and tumor markers have all been promoted in the market as IVD (In Vitro Diagnostic) products. Developing IVD-based products is a strategic pathway for companies to achieve sustainable growth.Enterprises should achieve the transition from the LDT model to the IVD model as early as possible.

It is evident that some companies have recently prioritized the in vitro diagnostics (IVD) transformation. “Obtaining regulatory approval is merely the first step; whether a product meets actual clinical needs is the key to its successful implementation,” pointed out Zhang Lianglu. “We have learned that for broad and smooth clinical adoption, four essential characteristics must be present simultaneously, with none being dispensable: compliance, precision, accessibility, and convenience.”

The first is compliance,The product complies with China’s “Measures for the Administration of Registration of In Vitro Diagnostic Reagents” and has received Class III medical device marketing approval from the National Medical Products Administration (NMPA) through well-designed clinical studies. Currently, some products feature relatively advanced technologies, posing significant challenges in designing appropriate clinical trials or obtaining regulatory approval.

Second is precision,High-quality products not only demonstrate high detection accuracy but also enable precise positioning within clinical pathways. The superior the performance of a product in detecting early-stage cancer or precancerous lesions compared to other clinical alternatives, the more significant its clinical value and the easier its adoption in clinical practice. Furthermore, as a novel diagnostic tool, clearly defining its clinical role and providing complementary support to existing diagnostics to assist physicians in diagnosis and treatment constitutes a critical foundation for its clinical application.

Third is inclusiveness,Early cancer screening products primarily serve asymptomatic individuals or high-risk populations, representing a vast consumer base with high price sensitivity. Therefore, market pricing should remain affordable to ensure accessibility for the general public and enable broad population-level benefits. Companies that effectively control product costs will be better positioned to sustain a competitive advantage in the future red-ocean market.

Fourth is convenience.Most current tumor screening products utilize non-invasive or minimally invasive sampling methods, effectively improving patient compliance. However, it is equally critical to ensure operational convenience for the large volume of medical technologists performing frontline tasks on a daily basis. Currently, many tumor screening products fail to account for the real-world operational scenarios of frontline personnel; complex handling techniques and redundant testing processes deter medical technologists in healthcare institutions, severely hindering product adoption. Consequently, ease of operation has become one of the most important points of differentiated competition for companies in the early cancer screening industry.

Aimisen has always adhered to a service orientation toward medical institutions, guided by the philosophy of benefiting the public through early cancer screening. While meeting the needs of clinical diagnosis,Continuously enhance product testing throughput, reduce turnaround time, and increase the level of automation from sample pre-processing to result reporting, with the aim of transforming specialized early cancer screening tests into routine examinations in healthcare institutions.Meanwhile, achieveThe localization of reagent raw materials and the in-house production of supporting reagent products have effectively controlled product costs.The market for early cancer screening may not be broad in its “surface area,” but it is exceptionally “deep.” To carve out a share of this substantial market, companies need not only sharp “knives” but also craftsmanship and enduring resilience.

Capital is one of the key drivers behind the rapid development of the early cancer screening industry. In 2020, several mega-rounds of financing ushered in the sector’s first major boom. As of July 2021, total funding in the early cancer screening segment had surpassed RMB 10 billion.

As one of the early domestic companies to enter the field of early cancer screening, Amison has naturally attracted significant attention from investment institutions. In 2017, the company received investment from Hybribio, a leading enterprise in cervical cancer screening in China. In 2020, it completed its Series A financing round with investment from the CCB Medical Growth Fund. In 2021, it closed a Series B financing round of nearly RMB 100 million, with participation from Jinhe Capital (an affiliated fund of KingMed Diagnostics), Changjiang Securities Innovation Investment, and Hybribio.

Notably, both Hybribio and KingMed Diagnostics, two leading IVD companies, are investors in Aimsen. The criteria that industrial capital uses to select investment targets differ from those of financial capital in thatIndustrial capital places greater emphasis on the true value and clinical utility of products, using clinical utility as the core criterion for long-term investment.“At that time, both CapBio and KingMed Diagnostics conducted multiple rounds of testing on Ameson’s early screening products for colorectal cancer and cervical cancer. They ultimately recognized Ameson’s R&D capabilities, product performance, and clinical implementation capacity, leading to their decision to invest.”

Next,As early cancer screening enters the stage of commercial implementation, the supportive role of industrial capital in channels, marketing, and customer resources will gradually become more prominent.It is foreseeable that, with the support of industrial capital such as Hybribio, the clinical implementation of Ameson’s products will proceed more smoothly.

Capital interest in early cancer screening will not cool down in the short term and is expected to intensify further. Driven by capital influx and corporate initiatives, the industry will maintain rapid growth for a period of time. However, caution is warranted against overheating and blind investment; excessive hype increases the risk of a sharp market correction, which would be detrimental to the industry’s healthy and sustainable development.

Capital must first recognize that the future of early cancer screening will inevitably lie in in vitro diagnostics (IVD). Next,Investment institutions should move beyond the mindset of evaluating corporate value solely from the perspectives of technology and clinical trials, and instead place greater emphasis on verifying whether products align with actual clinical needs. Companies must also recognize that capital is merely a facilitator; the more frenzied the capital market becomes, the more calmly companies should respond, focusing on strengthening their core competencies and refining their products.As more products that meet clinical needs undergo IVD transformation, investment institutions will become increasingly rational, and the industry will enter a phase of healthy development.

Currently, Amisen has launched a new round of financing, which will be used to expand the market, conduct new product research and development, registration, and prospective clinical trials.