Acotec Scientific, the Stealth Champion in Vascular Intervention, Files for Hong Kong IPO After Capturing Nearly 90% Market Share in Four Years

In 2021, the Hong Kong Stock Exchange witnessed a surge in initial public offerings (IPOs) by vascular intervention companies.

According to incomplete statistics from VCBeat, the vascular intervention sector has seen more than five companies go public in the past two years.

The architects behind this wave of IPOs share similar backgrounds. Most of the founders built China’s vascular intervention industry from the ground up. As pioneers in the field, they possess global management and operational experience and were instrumental in creating the initial prosperity of China’s vascular intervention sector.

However, the peak of China’s vascular intervention market is not limited to this. The large patient population and high mortality rate determine that this market can accommodate a new round of brilliance. Therefore, the second ventures of these pioneers have set off a new wave of IPOs in the vascular intervention industry.

Soon, the Hong Kong Stock Exchange will welcome another leading player in vascular intervention. Like other founders, this individual is also a pioneer and trailblazer in the development of China’s cardiovascular intervention sector.

The vascular intervention pioneer set to ring the bell this time is 49-year-old Ms. Li Jing. Ms. Li has 25 years of experience in the vascular interventional medical device industry. On August 12, Acotec, the leading peripheral intervention company under her leadership, began its subscription period., with an offering price of HK$22.2–23.8 per share. The subscription period is from August 12 to August 17, and the company is expected to list on the Hong Kong Stock Exchange on August 24. Morgan Stanley and CICC serve as joint sponsors.

The cornerstone investors include China Universal Asset Management, CPE Investment Wu, CICC, Valliance Fund, Perseverance Asset Management (Gaoyi), Daguan International, Athos Capital, Panjing Fund, Dymon Asia, Baoyin, PRIMEONE LUCK LIMITED (Jinglin), E Fund, and New Milestone Group, totaling 13 cornerstone investors who collectively subscribed for US$105 million (approximately HK$815 million).

Acandis is an interventional medical device company headquartered in Beijing, primarily focused on the endovascular treatment of vascular diseases. Acquired by Li Jing, the company saw him target the peripheral intervention sector—a niche market at the time—after the acquisition in 2011, building the drug-coated balloon (DCB) market for peripheral applications from the ground up. Acandis’s drug-coated balloons filled a gap in China’s peripheral market, ending the long-standing reliance on imported products for peripheral endovascular interventions in the domestic market.

Leveraging its dominant position in the field of peripheral interventions, Acotec received favor from CITIC Private Equity Funds in 2018, with CPE China Fund III becoming its controlling shareholder and holding a 64.81% stake through CA Medtech.

What Makes This Hidden Champion in the Interventional Space So Appealing That CITIC Has Taken a Majority Stake? Beyond Drug-Coated Balloons, What Other Competitive Products Does Acotec Have? As Acotec Opens Its IPO Subscription, VCBeat (WeChat ID: vcbeat) Provides an In-Depth Analysis.

The blood vessels within the human body are akin to the crisscrossing rivers on this planet, delivering nutrients to every corner of the body. Interventional treatments for vascular diseases are generally categorized into three major fields: coronary intervention, neurointervention, and peripheral intervention. Acotec’s primary focus is peripheral intervention, which mainly addresses vascular conditions outside the cardiac and cerebrovascular circulatory systems.

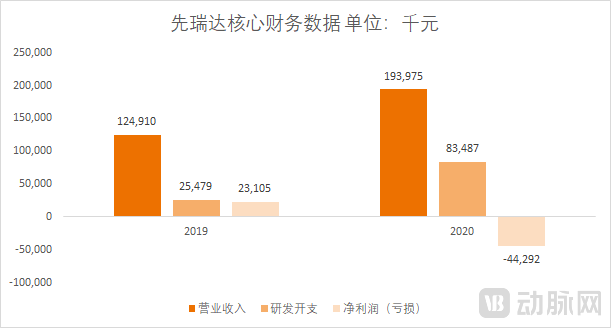

With its unique strategic vision, Acotec was the first to reap the benefits of the rapid growth in peripheral interventions. In 2019, Acotec generated revenue of RMB 120 million and a net profit of RMB 23.1 million; in 2020, revenue reached RMB 190 million, but the company incurred a loss of RMB 44.29 million due to increased R&D investment. R&D expenditures in 2019 and 2020 were RMB 25.47 million and RMB 83.48 million, respectively. Acotec’s gross profit margins for 2019 and 2020 were 84.8% and 84.4%, respectively.

At its inception in 2008, Acotec focused primarily on the research and development of cardiac radiofrequency ablation catheters. In 2011, Li Jing and Silvio Rudolf Schaffner acquired Beijing Acotec.

Prior to Acotec’s IPO, its founder, Li Jing, rarely made public appearances. Information disclosed in the prospectus shows thatLi Jing graduated from Jiangsu University in 1993 and worked in cardiovascular product sales for nearly a decade after graduation.From 2006 to 2008, Li Jing served as the Head of Greater China at Invatec, where she successfully led the company to achieve a leading position in the peripheral, coronary, and neurointerventional fields. In 2010, Invatec was acquired by Medtronic.

Another key figure at Acandis, Chief Operating Officer Silvio Rudolf Schaffner, is from Switzerland and brings over 28 years of experience in the medical device industry. He previously served as Chairman of the Management Board and legal representative of Invatec, and holds multiple patents in the fields of orthopedic implants and vascular interventions.

Ms. Li Jing and Schaffner’s experiences at Invatec had a profound influence on the founding of Acotec.Invatec commercialized the world’s first drug-coated balloon product as early as 2009, demonstrating profound expertise in the balloon catheter field.Invatec is also a strong player in the peripheral vascular field. What was Invatec’s market position in the peripheral segment back then?

There is such a story. In the early years, Invatec invited foreign professors to China to perform live surgical demonstrations, which helped promote standardized endovascular treatment of lower extremity arterial diseases in China. Meanwhile, a group of Chinese vascular surgeons also participated in short-term fellowship training at Leipzig through Invatec; the vast majority of them have now become key leaders in the field of vascular surgery in China.

Therefore, as the then Head of Greater China at Invatec, Ms. Li Jing not only recognized the opportunities in China’s peripheral intervention market at an early stage but also played a key role in vigorously driving the development of peripheral interventions in China.

The founder team at Acotec, combining a global perspective with local expertise, possesses extensive experience in managing and operating global businesses. Their unique strategic vision and global outlook enabled them to recognize the vast market potential of peripheral interventions at an early stage. Following the acquisition of Acotec, Li Jing and Schaffner chose to focus on the research and development of peripheral drug-coated balloons (DCB), a single product that integrates Invatec’s two core advantages.

In the past, the potential of the peripheral intervention market was often overlooked. In reality, with the vigorous development of vascular surgery in China, the entire peripheral intervention market has begun to take off rapidly in recent years. According to relevant research reports by Frost & Sullivan, the market size of peripheral vascular interventional medical devices in China was RMB 3.01 billion in 2017, and is projected to reach RMB 30 billion by 2030.

Table of ContentsCurrently, multinational corporations account for over 90% of the peripheral vascular intervention market in China.

Compared with coronary intervention, the peripheral intervention field has a large patient base, and its market growth potential cannot be underestimated. Compared with neurointervention, peripheral intervention involves diverse disease types and complex procedural techniques, resulting in higher entry barriers and more diversified growth drivers. With the advent of an aging society, improvements in living standards, and the emergence of new technologies, the peripheral intervention market has seen rising momentum in the past two years.

Acandis’ uniqueness lies in its early recognition, years ago, of the potential in the peripheral intervention sector, and its proactive positioning with a blockbuster product for the era of implant-free vascular interventions: the drug-coated balloon.

In the peripheral intervention market, traditional bare-metal stents and plain balloon angioplasty catheters remain the cornerstone products.

After acquiring Acandis, Li Jing did not follow the conventional path of mimicking products already launched in China. Instead, she took an unconventional approach by focusing on peripheral drug-coated balloons, a product category that had zero presence in the Chinese market at the time.

Why Drug-Coated Balloons? First, from a technical perspective, drug-coated balloon technology can breakthroughly address the limitations of existing devices. Second, in terms of commercialization potential, drug-coated balloons have three major indications—above-the-knee lesions, below-the-knee lesions, and hemodialysis access—as drivers for sustained growth.

First, in terms of technological advantages,For peripheral arterial stenotic lesions, both traditional bare-metal stents and plain balloon angioplasty still have limitations. In the field of peripheral arterial disease, the development trend of minimally invasive interventional devices is focused on better addressing the challenges of recanalizing lower-extremity vascular lesions and reducing the high rate of post-procedural restenosis.

Drug-coated balloons are a powerful tool for addressing restenosis. They combine conventional balloon angioplasty with drug-eluting technology by coating the balloon surface with antiproliferative agents. During inflation, these drugs are delivered to the local vessel wall at the lesion site, thereby inhibiting smooth muscle cell proliferation and preventing vascular restenosis.

Upon its market launch, the drug-coated balloon (DCB) significantly disrupted the dominance of bare-metal stents and plain old balloon angioplasty. Chinese physicians generally recognize the efficacy of DCBs, with substantial clinical evidence demonstrating that DCBs reduce restenosis rates post-treatment. It is projected that the penetration rate of DCBs among patients undergoing lower extremity endovascular interventions will reach 50% in the future.

Second, in terms of the potential for commercial monetization,Drug-coated balloons have a broad range of indications, with three major application scenarios: above-the-knee lesions, below-the-knee lesions, and hemodialysis access.

In the market for femoropopliteal lesions, Li Jing and Schaffner early on anticipated the trend that drug-coated balloons would capture share from the stent market. In 2011, when drug-coated balloon products were just emerging globally, Acotec had already initiated R&D of its PTA balloons and drug-coated balloons (DCBs).

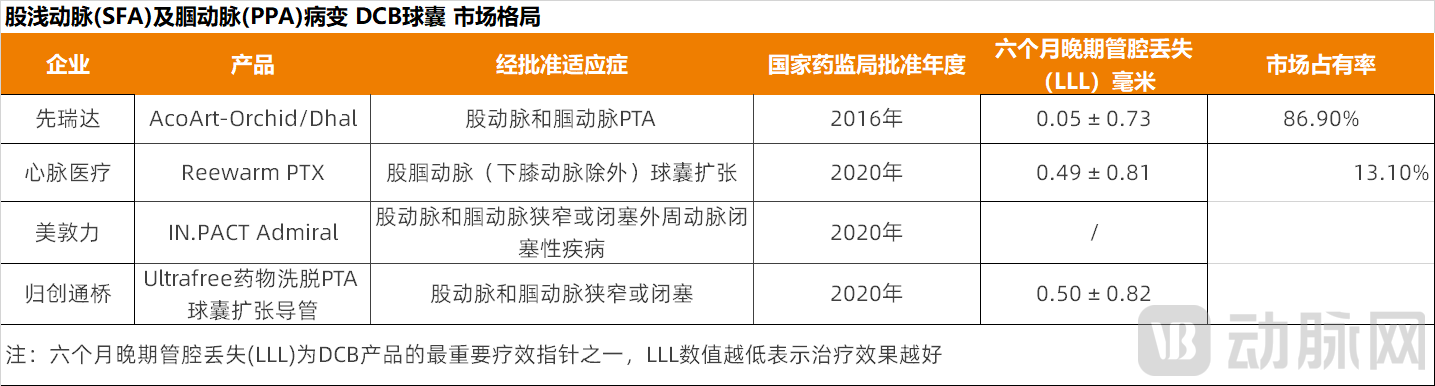

In 2016, Acotec’s core products, AcoArt Orchid® & Dhalia, were indicated for lesions of the superficial femoral artery (SFA) and popliteal artery (PPA).TMApproved, it became the first peripheral drug-coated balloon (DCB) product to receive market approval from the National Medical Products Administration (NMPA). For the following three years, Acotec’s above-the-knee DCB balloons remained the sole available product. It was not until 2020 that similar products from multiple domestic and international companies were successively approved for market launch.

Launched three years ahead of competing products, this early market entry allowed Acotec to establish a significant lead in distribution channels and provided ample time for product innovation and iteration. Although several similar products are now available on the market, Acotec’s product maintains a competitive edge based on clinical data for core endpoints of domestically approved peripheral drug-coated balloons (DCBs), such as late lumen loss (LLL) at six months.

Meanwhile, the markets for below-the-knee lesions and hemodialysis access are in their early stages, with enormous growth potential driven by a large patient population.

Infrapopliteal Artery Occlusion: A Persistent "Minefield" in Endovascular TherapyInfrapopliteal artery occlusion is common among patients with diabetes. However, due to the slender lumen of infrapopliteal vessels, it is difficult to overcome factors such as restenosis and elastic recoil, thereby precluding guaranteed long-term outcomes with current treatments. Consequently, infrapopliteal arterial disease remains a challenging “minefield” in endovascular therapy worldwide.

In the below-the-knee (BTK) lesion market, Acandis also holds a first-mover advantage.

Currently, AcoArt Tulip from Acotec is the only below-the-knee DCB product available in China.TM & Litos TMIt has been launched on the market. Moreover, this product has been granted Breakthrough Device Designation by the U.S. Food and Drug Administration (FDA). This marks the first time in history that an interventional medical device independently developed in China has received FDA Breakthrough Device Designation.

AcroMed has achieved a breakthrough in this field. The core of its innovation lies in the use of a different excipient (coating matrix), combining lipophilic magnesium stearate with lipophilic paclitaxel, which is loaded onto the balloon platform. This represents a third-generation coating technology that reduces drug loss and improves drug loading efficiency.

In the past two years, clinical trial results for drug-coated balloon (DCB) therapy in infrapopliteal lesions have preliminarily demonstrated favorable short- to medium-term efficacy and the potential for repeat endovascular interventions. Supported by the large population of patients with diabetic foot, the market for endovascular treatment of infrapopliteal lesions is projected to reach RMB 363 million by 2024.

The third major growth driver for drug-coated balloons (DCBs) lies in the hemodialysis access market. DCBs are used in interventional procedures to treat stenosis in arteriovenous fistulas (AVFs) created for hemodialysis (HD). In China, the number of interventional procedures for treating AVF stenosis in hemodialysis patients increased from 7,700 cases in 2015 to 39,100 cases in 2019, and is projected to reach 994,500 cases by 2030. It is anticipated that the overall hemodialysis access market will become a significant segment for DCBs in the future.

In the hemodialysis access market, Acotec, a well-established domestic balloon manufacturer in China, is expanding its portfolio with the AcoArt Orchid® & Dhalia peripheral drug-coated balloons.TMindications for the treatment of AVF stenosis in nephrology departments. The product is expected to be launched in 2023 and will become a key player in this market in the future.

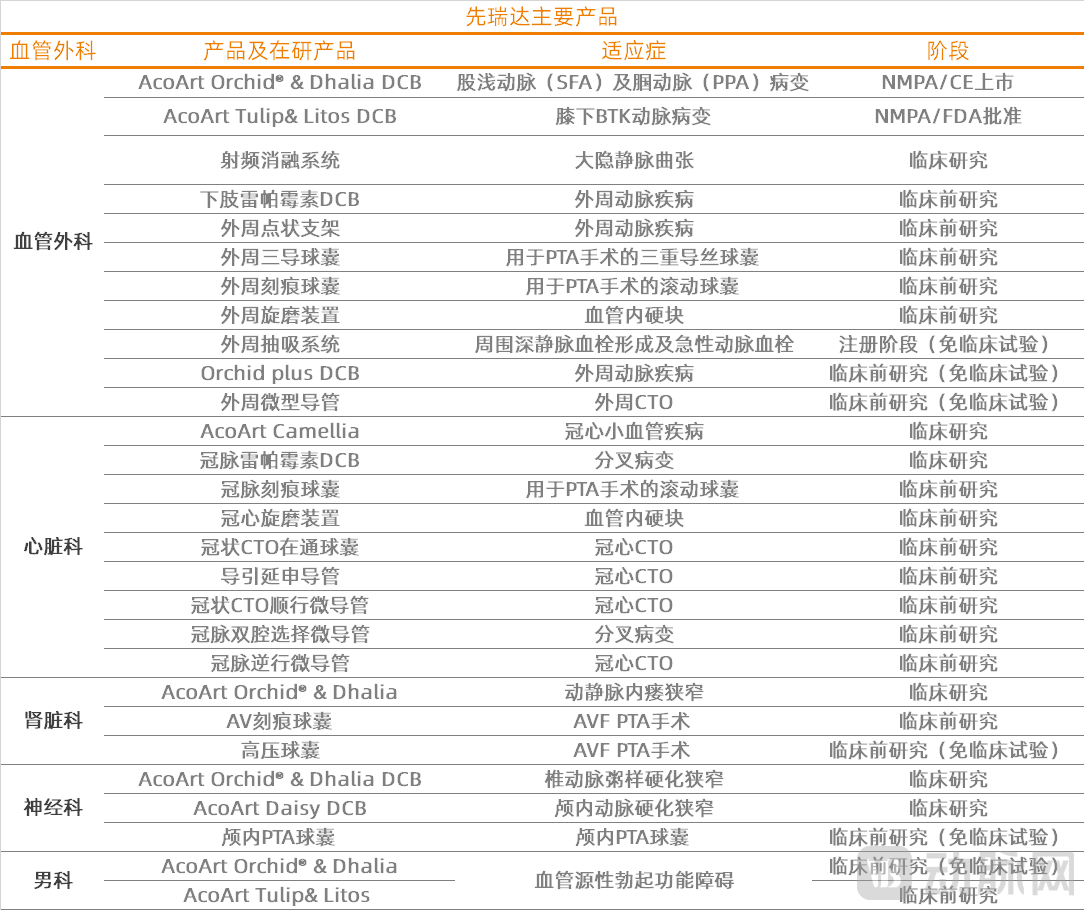

According to the product pipeline disclosed in Acotec’s prospectus, the company will continue to tap into the potential of balloons as a specialized vertical product. Its pipeline covers various types of balloons, including drug-coated, scoring, and high-pressure balloons, with indications spanning multiple specialties such as coronary intervention, neurointervention, urology/andrology, and neurology.

Amid growing attention on drug-coated balloons (DCBs), Acotec has secured a first-mover advantage in this field. However, as more DCBs gain regulatory approval and enter the market, competition has intensified significantly. Ultimately, the ability to dominate the DCB market will hinge on product R&D capabilities and commercialization prowess. Is Acotec well-prepared in these two critical areas?

In terms of R&D, AcandA is committed to building a world-leading R&D team capable of rapid iteration.

Acandis has partnered with Dr. Ulrich Speck, a globally recognized leading expert in the vascular interventional medical device industry, appointing him as Chief Technology Officer.Dr. Ulrich Speck, who developed the world’s first drug-coated balloon (DCB), is a globally recognized leading expert in the vascular interventional medical device industry. The coronary DCB he co-developed with B. Braun is the best-selling coronary drug-coated balloon worldwide.

A world-leading R&D team has enabled Acotec’s drug-coated balloons to demonstrate superior clinical outcomes in clinical trials, outperforming many other mainstream DCB products despite stringent patient enrollment criteria.

Another major highlight of Acotec’s drug-coated balloon is that Acotec has mastered upstream “chokehold” technologies and established a polymer materials platform, enabling rapid iterative innovation in product development.

Innovation in upstream materials directly constrains innovation in end products, affecting the stability of product performance and quality. However, the capacity for material innovation is lacking in most domestic enterprises. The majority of medical device companies in China cannot independently produce polymer materials; instead, they rely on imported raw materials for product research, development, and manufacturing.

To overcome this “chokepoint” technology, Acandis acquired Weitai Medical and established a Polymer Materials Center in Shenzhen to support innovation in its balloon catheter products. By building its own polymer materials R&D center, the company has broken its reliance on the traditional model of “imported raw materials + domestic manufacturing.” This enables faster product iteration.

In terms of commercialization capabilities, Acotec started from scratch to create and cultivate the peripheral drug-coated balloon (DCB) market in China, demonstrating strong marketing capabilities with its AcoArt Orchid® & DhaliaTMIn the second year after its market launch, the usage volume of peripheral drug-coated balloons (DCBs) reached 8,000 units, rising to 15,000 units in 2019, with a compound annual growth rate (CAGR) of 36.9% from 2017 to 2019. In terms of hospital coverage, Acotec’s DCB products have been adopted by more than 800 vascular intervention centers and over 90% of hospitals capable of performing peripheral vascular interventional procedures in China.

From this perspective, among the new generation of vascular interventional companies in China, Acotec is one of the few enterprises with mature commercialization capabilities, and it has also achieved a high penetration rate in leading hospitals across the country.

Acandis was fortunate to spot the emerging opportunity in drug-coated balloons ahead of the curve. In the complex peripheral intervention market, which other segments are poised to become the next hotspots?

Acotec has bet on the concept of “intervention without implantation,” strategically aligning its portfolio around this philosophy to provide physicians with a comprehensive suite of solutions for peripheral interventions without implants. This will serve as an additional growth driver for Acotec, beyond its drug-coated balloons.

Although drug-coated balloons are a key product in the "intervention without implantation" approach, they are insufficient for a comprehensive solution. Therefore, in addition to its drug-coated balloon technology platform, Acotec has established three additional technology platforms: aspiration technology, radiofrequency ablation technology, and polymer materials technology.

These three major technology platforms share several common characteristics: high barriers to entry, high growth potential, and import monopolies.

First, let’s examine radiofrequency ablation technology.In terms of application scenarios, radiofrequency ablation technology is widely used in interventional procedures for various clinical treatments. Beyond Acotec’s core strength in the peripheral vascular field, radiofrequency ablation is primarily employed for the treatment of varicose veins. Emerging radiofrequency ablation therapies are replacing traditional stripping surgery.

High growth is reflected in the “surge” in the volume of radiofrequency ablation procedures for varicose veins. In 2015, only 2,700 patients in China underwent radiofrequency ablation for varicose veins, a figure that reached 26,300 by 2019, representing a compound annual growth rate (CAGR) of 76.9%.

The high barriers to entry are reflected in the fact that few domestic companies are capable of manufacturing radiofrequency ablation (RFA) generators, with most enterprises possessing only the ability to develop RFA catheters. Consequently, all peripheral RFA products available in China are supplied by imported brands. Acotec’s RFA system includes an RFA generator. The market launch of this RFA system is expected to achieve rapid volume growth, thereby driving a swift increase in Acotec’s revenue.

Aspiration platforms are also a key focus of Acotec’s strategic layout. Aspiration catheters, akin to “vascular scavengers,” can extract thrombi.

The high growth of aspiration systems is reflected in the rapid expansion of aspiration catheters in peripheral interventional applications. Aspiration systems are primarily used in peripheral interventions to treat venous thromboembolism (VTE), which includes pulmonary thromboembolism (PTE) and deep vein thrombosis (DVT). Pulmonary embolism is the third leading cause of cardiovascular death, following coronary heart disease and stroke, and is characterized by high incidence, high disability rates, and high mortality, making it a severe and acute condition of the respiratory system. Pulmonary embolism is typically a consequence of deep vein thrombosis.

In 2019, the number of new deep vein thrombosis (DVT) cases in China rose to 1.5 million, while the number of thrombectomy procedures for DVT treatment reached 60,000. The compound annual growth rate (CAGR) from 2015 to 2019 was 19.9%. The procedure volume is projected to increase to 527,000 by 2030.

The high barriers to entry are evident in the Chinese market, where nine complete aspiration system products have been launched, all manufactured by multinational corporations. Moreover, few domestic companies are capable of producing both aspiration pumps and aspiration catheters. Acotec’s aspiration system is specifically developed for peripheral thrombus aspiration. In 2019, Acotec began establishing its peripheral aspiration platform, deploying a comprehensive solution ranging from aspiration pumps to aspiration catheters. Acotec’s peripheral aspiration system is expected to be the first domestically produced peripheral aspiration system approved by the National Medical Products Administration (NMPA).

Both the radiofrequency ablation platform and the aspiration product platform are expected to be in niche markets capable of achieving rapid volume growth following product launch.

The value of the polymer materials technology platform not only enables Acotec’s drug-coated balloons to iterate rapidly, but also extends its strategic layout into the market for basic catheters, guidewires, and other consumables in peripheral interventions. Access products such as catheters and guidewires serve as the foundation for every interventional procedure; although their unit price is low, their high usage volume makes them a significant component of the peripheral arterial intervention market.

Acandis currently possesses four major technology platforms: drug-coated balloons, radiofrequency ablation, thrombus aspiration, and polymer materials. Building on this foundation, the company is capable of developing multiple commercialized products, whereas most emerging domestic vascular intervention companies possess only a single commercialized product and technology platform.

Overall, Acotec is a rare high-quality investment target in the vascular intervention sector. In terms of market segmentation, peripheral intervention, which is Acotec’s core focus, is one of the three major segments of vascular intervention. In the long run, the neurointervention and peripheral intervention markets are expected to be comparable in size, with both projected to reach RMB 30 billion by 2030.

From a performance perspective, Acotec’s key commercialized product, the drug-coated balloon (DCB), is poised to significantly capture market share from stents, driven by the “intervention without implantation” philosophy, and has become a leading single product in the peripheral artery disease segment. Acotec’s DCB demonstrates excellent clinical data and boasts extensive market channel coverage. Meanwhile, two other major application areas for DCBs—arterial stenosis and hemodialysis access—are just beginning to see substantial volume growth. Both segments are supported by a large patient base, indicating promising future market size.

Based on the product pipeline, radiofrequency ablation and thrombus aspiration are core technology platforms in the field of endovascular therapy. Currently, these markets are predominantly monopolized by imported products; however, domestically produced alternatives are expected to achieve rapid volume growth upon market entry. As a domestic pioneer with established advantages in the peripheral vascular sector, Acandis is poised to become the market leader.

Reference: Acandis Prospectus

LINC Conference and China – New Generation in Vascular Medicine