How an MIT PhD Built a $30B+ Biotech Powerhouse by Mastering Cell Culture: Sinobiological's Record-Breaking IPO

On August 16, Sino Biological Inc. finally made its debut on the ChiNext board of the A-share market, becoming the first listed company in China to specialize in core reagent raw materials.

In the two weeks prior, Sino Biological Inc. made a splash in the capital markets with its record-breaking IPO pricing on the A-share market, becoming a star stock even before its official listing. Despite its relatively low profile, Sino Biological has earned a strong reputation in the industry for its independently developed recombinant proteins, which rival those of established international upstream raw material companies. Through its IPO, Sino Biological issued 17 million new shares, raising RMB 4.979 billion. On the day of the IPO, its share price surged by as much as 104.79%, closing at RMB 493.32, with a total market capitalization exceeding RMB 33.55 billion—equivalent to the combined market cap of at least two mid-sized IVD companies.

2021 can be hailed as the breakout year for upstream core raw material enterprises. In addition to Sino Biological Inc., companies such as Fapon Biotech, which specializes in antibody development; Vazyme Biotech, which focuses on molecular enzyme development; and Yeasen Biotechnology have all secured substantial financing and are poised to enter the capital markets. These hidden champions dominating the upstream sector have clearly become the hottest new trend in the pharmaceutical industry.

Sino Biological Inc. specializes in providing raw materials such as recombinant proteins, antibodies, genes, and culture media, along with related bioanalytical testing services, for the research, development, and manufacturing of biologics. The company originated from the reagent business that Sino Cell Therapy Ltd. began operating in 2007. Prior to its complete spin-off in 2016, this reagent business served as the “cash cow” that supported Sino Cell Therapy Ltd.’s development of biopharmaceuticals.

Following its independent operation, the self-sufficient, fast-paced model has propelled Sino Biological Inc. into a cycle of robust growth. Meanwhile, its products and team, as well as sales and profitability, have remained relatively stable.Sino Biological conducted only two rounds of external financing prior to its IPO, bringing in institutional investors such as Qiming Venture Partners and Qingsong Capital, making it a startup with highly concentrated equity ownership.With its high-priced IPO, Sino Biological Inc. has also delivered investment returns of more than 10-fold to several institutional investors.

Sino Biological IPO Site: Xie Liangzhi and Tang Yanmin

On the day of its IPO, Tang Yanmin, Investment Partner at Qiming Venture Partners, attended Sino Biological’s listing bell-ringing ceremony as the sole representative from the investment community. She told VCBeat that as early as 2006, Sino Biological’s antibody transient transfection expression levels were already among the highest globally.

When discussing the initial investment decision in Sino Biological, Tang Yanmin analyzed that with the booming development of China's biopharmaceutical industry, a large number of high-quality biotech companies have emerged, leading to an explosive demand for scientific research reagents closely related to new drug R&D. Previously, the vast majority of biological reagents relied on imports, but imported products were often expensive and had long lead times. Sino Biological has basically achieved ready-to-ship supply at low prices, greatly improving enterprises' R&D efficiency, while also possessing profound technical expertise and a rich product portfolio. “Such companies are rare in China,” said Tang Yanmin. “Therefore, when Sino Biological conducted its first external financing round in 2017, we invested without hesitation.”

So, once the cycle of the COVID-19 pandemic subsides, can this suddenly popular “chokepoint” sector continue to thrive? We attempt to find the answer by examining Sino Biological Inc.

Sino Biological was founded by Dr. Xie Liangzhi, a Ph.D. graduate of the Massachusetts Institute of Technology, who is arguably the world’s foremost expert in cell culture.

In 1991, Xie Liangzhi entered the Massachusetts Institute of Technology (MIT) in the United States to pursue his doctoral degree under the supervision of Professor Y. I. Wang, known as the father of industrial biotechnology. During his doctoral studies, Xie pioneered the use of stoichiometric models to control high-density fed-batch culture of animal cells, increasing monoclonal antibody yields to 2,400 mg/L—more than tenfold higher than the highest levels reported in the literature at that time. After completing his Ph.D., Xie joined Merck & Co. in the United States, specializing in viral vaccine research and development. Under his leadership, Merck established a globally leading manufacturing process for adenovirus-vector-based HIV vaccines, achieving cGMP production at a 2,000-liter scale. This process remains the largest-scale cell culture and viral manufacturing process for live human viral vaccines worldwide to date.

After leaving Merck, Xie Liangzhi returned to China, hoping to leverage the most advanced large-scale animal cell culture technology he had brought back to help the domestic pharmaceutical industry overcome bottlenecks in the industrial production of large-molecule drugs. However, to his disappointment, there were no biologic drug products in China at that time requiring large-scale manufacturing. Left with little choice, Xie decided to address the issue of product pipeline independently by establishing Sinocelltech and Nuoning Biopharma, which focus on the development of biologics and vaccines, respectively.

New drug development is an extremely capital-intensive endeavor. Initially, the cash flow generated by the concurrently operating reagent business barely sufficed to meet the substantial funding requirements. However, as Xie Liangzhi gradually realized that new drug development and the reagent business followed vastly different growth logics, the envisioned synergy between the two had become a mutual burden. By the end of 2016, the reagent business was spun off to operate independently under the name Sino Biological, a tribute to Professor Wang Yiqiao, Xie Liangzhi’s mentor.

For domestic biological reagent manufacturers that started nearly 30 years later than their international counterparts, the only way to diminish the market influence of imported brands is by offering a more diverse product portfolio, faster response times, and better cost-performance ratios. Therefore, at the outset of launching his reagent business, Xie Liangzhi held his team to the high standards set by global industry leaders such as R&D Systems and PeproTech, aiming to rapidly develop recombinant proteins and antibodies of sufficient quality to meet the rapidly evolving demands of scientific research and clinical applications. Acquaintances of Xie Liangzhi have noted that he eats only two meals a day, works an extended 12 to 16 hours daily, and rarely takes a complete vacation throughout the year, demonstrating an extraordinary obsession with optimizing cell culture conditions.

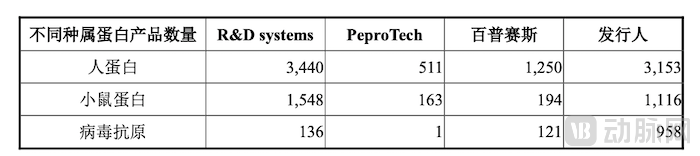

This is because, even in the domestic market, high-end biological reagents such as recombinant proteins and antibodies have long been monopolized by imported brands. However, Sino Biological Inc. has made rapid progress. According to its prospectus, as early as 2019, before the outbreak of the COVID-19 pandemic, Sino Biological had already broken through in the domestic recombinant protein market, becoming the third-largest brand with a 4.9% market share, trailing only R&D Systems and PeproTech. As of March 2021, the number of recombinant protein products offered by Sino Biological had surpassed those of R&D Systems and PeproTech. Furthermore, the company possesses significant technical advantages in mammalian cell expression systems, which produce proteins with structures and properties closest to natural human proteins but are characterized by difficult cultivation processes, higher production costs, and relatively lower yields. While it took R&D Systems 45 years and PeproTech 33 years to reach their current scale, Sino Biological achieved this in just four years.

Number of Protein Products from Sino Biological and Major Manufacturers

“Over the past four years of accompanying Sino Biological on its journey, the company has impressively achieved high growth in both revenue and profit each year, consistently meeting the budgets set at the beginning of the year,” said Tang Yanmin, Investment Partner at Qiming Venture Partners.

In early 2020, just 12 days after the nucleic acid sequence of the novel coronavirus was released, Sino Biological Inc. successfully expressed the S-RBD protein, a key target antigen of the virus, and subsequently supplied it to more than 200 biotechnology companies worldwide for the development of diagnostic and therapeutic products against COVID-19.

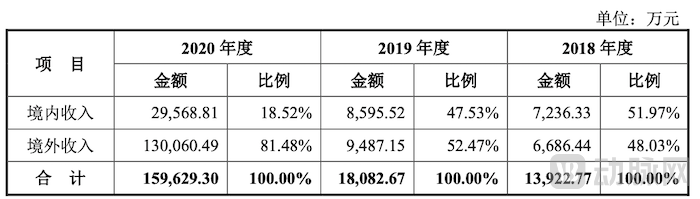

This agile response has brought substantial commercial returns to Sino Biological Inc. In 2020, the company achieved revenue of RMB 1.59 billion, representing a year-on-year increase of 782.78%, nearly equivalent to the sum of its revenues in all prior years. Furthermore, by meeting the surging demand for COVID-19-related products in severely affected regions such as the United States and Europe, Sino Biological’s overseas sales revenue surged from around 50% historically to 81.48%. Given that most of the pandemic-driven demand stemmed from direct orders placed by downstream manufacturers, these overseas orders undoubtedly helped Sino Biological expand its global market network.

Sino Biological’s Revenue Excluding the Impact of COVID-19, 2018–2020

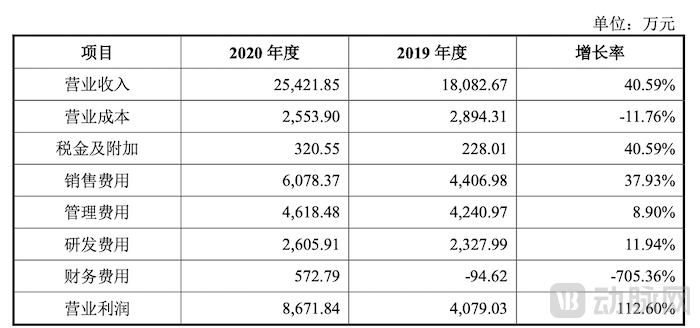

It would be incorrect to assume that Sino Biological’s performance growth was driven solely by the COVID-19 cycle. In its prospectus, Sino Biological specifically presented operational data excluding the impact of the pandemic. Even without the COVID-19 episode, the company achieved a 40.59% revenue growth in 2020, significantly surpassing the 29.87% recorded in the previous year, and realized a decrease in operating costs thanks to positive economies of scale.

Sino Biological’s Operating Data Excluding the Impact of the COVID-19 Pandemic, 2018–2020

In fact, a similar trend in performance growth can also be observed in the prospectuses of Fapon Biotech and Vazyme. Specifically, Fapon Biotech’s compound annual growth rate (CAGR) for revenue from 2018 to 2020, excluding the impact of the COVID-19 pandemic, was 28.99%. Vazyme did not provide its 2020 revenue data adjusted for the impact of the pandemic; however, its growth rate from 2018 to 2019 reached as high as 57.12%.

Comparison of Revenue for Sino Biological, Fapon Biotech, and Vazyme from 2018 to 2020, Excluding the Impact of COVID-19

Behind the rapid rise of upstream core raw material enterprises is the booming development of global and domestic scientific research, which has driven a surge in demand for biological reagents. In recent years, countries around the world have increased their investment in life sciences research. From 2015 to 2019, global scientific research funding grew from $116.6 billion to $151.4 billion. During this period, China's R&D expenditure also increased from RMB 43.4 billion to RMB 86.6 billion, with a compound annual growth rate (CAGR) of 18.8%, thereby driving the rapid expansion of the biological reagent market. From 2015 to 2019, the size of China's biological reagent market grew from RMB 720 million to RMB 13.6 billion, with a CAGR of 17.1%, significantly higher than the global average of 8.1% during the same period. During this time, domestic biological reagent brands, benefiting from enhanced scientific research capabilities, improved product quality, and advanced business operations of local enterprises, have gradually achieved import substitution. High-quality domestic brands that have emerged in this process include Sino Biological Inc., Fapon Biotech, Vazyme, ACROBiosystems, and Yeasen Biotechnology.

In addition to the highly favorable macroeconomic environment, Sino Biological Inc.’s rapid and efficient capabilities in recombinant protein and antibody R&D and production have been key to its ability to stand out amidst intense competition from numerous domestic and international brands. For Chinese biological reagent manufacturers that no longer enjoy first-mover advantages, the only viable strategy to capture market share from imported brands is to respond immediately to customers’ evolving needs, prioritizing speed above all else.

The manufacturing process for recombinant proteins typically includes steps such as acquisition of the target gene, plasmid construction and amplification, cell transfection, cell culture, protein purification, and lyophilization of the final product. Among these, high-efficiency transient protein expression systems, appropriate host species for expression, and high-precision genetic engineering technologies constitute key technical barriers that manufacturers leverage to build core competitive advantages. Sino Biological’s mammalian cell recombinant expression system features independently optimized expression vectors that support high-level transient protein expression. By utilizing fusion protein vectors with high-intensity fluorescent tags, the system enables protein expression tracing and monitoring, facilitates highly efficient cell transfection, and achieves cost reduction and efficiency enhancement, demonstrating significant advantages over comparable systems globally.

In fact, the COVID-19 pandemic was not the first time Sino Biological Inc. gained prominence for its efficient development of recombinant proteins. In 2009, when the H1N1 influenza outbreak erupted in Mexico, Xie Liangzhi led the company to develop the hemagglutinin protein essential for the H1N1 vaccine in just 30 days, drawing worldwide attention. In 2013, amid a sudden domestic outbreak of H7N9 avian influenza, Sino Biological mobilized over 100 personnel for emergency drug research and development, completing the production of H7N9 hemagglutinin protein in merely 12 days and pioneering the global development of a specific antibody drug for treating severe H7N9 infections.

Regarding Sino Biological’s recent IPO, there has been considerable skepticism from external observers. In summary, concerns primarily focus on two aspects: first, the risk that Sino Biological could be adversely affected due to its personnel, technology, and asset ties with Shenzhou Cell; second, doubts about the sustainability of its rapid revenue growth.

The first type of skepticism has long existed. In its latest prospectus, Sino Biological Inc. devoted considerable space to detailing the history of its separation from Sinocelltech, as well as the delineation of key elements such as personnel, patents, and assets, in an attempt to demonstrate the independence of its operations and finances. In reality, however, these descriptions based on historical information are insufficient to prove Sino Biological’s potential for independent growth in the future.

However, two points should not be overlooked when considering this issue. First, Sino Biological Inc. and Sinocelltech have markedly different corporate visions. The former aims to become a global one-stop provider of biological reagents, while the latter is committed to providing innovative solutions for major diseases to patients in China. The differences in target customers and business models may steer the two companies in divergent directions. Second, as both companies continue to deepen their development, they face entirely different challenges. Sino Biological Inc. must address how to efficiently produce high-quality proteins, antibodies, genes, and other biological reagents, whereas Sinocelltech must meet the challenge of delivering innovative drugs with guaranteed safety and efficacy under regulatory compliance. In this sense, the resources that Sino Biological Inc. and Sinocelltech need to focus on integrating in the future are fundamentally different. As for financial independence, it will test the strategic resolve of the founding teams—a matter to be discussed later.

Regarding the second challenge, this article has already provided a partial explanation in the previous section; here, we add two further points.

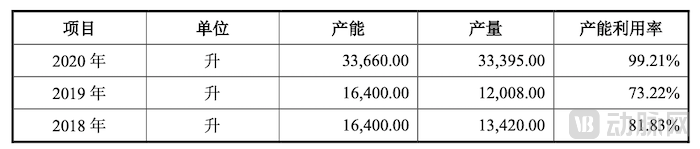

On one hand, Sino Biological Inc.’s production capacity and sales network have doubled over the past two years. As early as 2019, to accommodate its expanded production scale, Sino Biological introduced new production equipment, which commenced operations in early 2020. In the second and third quarters of 2020, the company further expanded its production capacity, enabling it to handle orders at least twice the previous volume. Meanwhile, the number of sales personnel increased from 43 in 2018 to 77 in 2020, while R&D staff grew from 95 to 102. Average compensation levels rose by approximately 50%. This expansion of the talent pool has undoubtedly provided a solid foundation for the growth of operational performance.

2018–2020: Sino Biological’s Production Capacity and Utilization

On the other hand, even with the highest IPO pricing in the A-share market, Sino Biological Inc. remains undervalued in the capital markets. Based on its 2020 earnings per share, the company’s current price-to-earnings (P/E) ratio is less than 20, significantly lower than the P/E ratio of at least 40 for companies with similar market capitalizations, and far below the industry average P/E ratio of over 100 for the research and experimental development sector. In other words, even if Sino Biological’s net profit were to decline by 50% in 2021, it would still be able to largely maintain investor confidence. Moreover, considering the company’s plan to invest RMB 450 million from its IPO proceeds into biological reagent R&D and RMB 200 million into building a global marketing network, its future prospects are promising.

However, for Sino Biological Inc., going public is merely a new beginning, with significant uncertainties lying ahead.

Can a sufficiently extensive product portfolio be established to meet the diverse needs of a multifaceted customer base in a one-stop manner? Can the company accurately position itself at the forefront of emerging hotspots in basic life sciences and pharmaceutical discourse to enable rapid response? Can customized products and services be delivered to customers quickly and cost-effectively? Can professional and timely technical support be provided during product use? Can sufficient market influence be built through horizontal and vertical collaborations amid rising market concentration? All these challenges test the determination and wisdom of the founding team and are critical to ensuring a smooth post-IPO trajectory for Sino Biological Inc.

Writing Reference:

Sino Biological’s R&D Expenses of RMB 26.06 Million Amount to Less Than 30% of Sales Expenses; Holds Nearly RMB 1.1 Billion in Bank Wealth Management Products; IPO Oversubscribed by RMB 4.08 Billion

From Zero to 18 Billion: Xie Liangzhi and His “Recombinant Protein Drug Empire”

Xie Liangzhi: The Chinese Bullet That Kills the Ebola Virus

Prospectuses of Sino Biological, Fapon Biotech, and Vazyme