Carlyle and Sequoia Heavily Back Ambio Pharmaceuticals, the World’s Fourth-Largest Peptide CDMO, as It Files for Hong Kong IPO

In late June, Onbo Pharma quietly filed its IPO application with the Hong Kong Stock Exchange. Although this company has maintained a relatively low profile in the Asia-Pacific market, it ranks as the fourth-largest peptide CDMO globally. It has provided integrated peptide products and services, ranging from active pharmaceutical ingredients (APIs) to finished formulations, to more than 100 biopharmaceutical and biotechnology companies, including over half of the top 20 global pharmaceutical firms. Its proprietary hybrid liquid-phase/solid-phase chemical synthesis process for long and complex peptides reduces production costs while increasing yield and enhancing process flexibility, offering significant advantages over traditional recombinant technologies.

Despite having secured a strong competitive position in the North American market, Ambow Pharma has maintained a relatively low profile in Asia and Europe. Nevertheless, Sequoia Capital took notice of the company in 2020. In August 2020, during Ambow Pharma’s Series B financing round, Sequoia Capital invested $60 million in the company, acquiring a 9.2% equity stake—a rare move that signaled a significant bet on this understated CDMO firm.

In recent years, both peptide drugs and peptide CDMOs have entered a phase of rapid growth. The successive launches of blockbuster drugs such as liraglutide and semaglutide have significantly improved the medication experience for patients with type 2 diabetes, while generating billions of dollars in single-product sales. Consequently, peptides have become the second-fastest-growing drug category globally. Meanwhile, CROs, API manufacturers, and small-molecule CDMOs are actively expanding into peptide CDMO services, serving as a powerful driver of the global growth trend in peptide therapeutics.

Peptides are unique pharmaceutical compounds that extensively participate in and regulate the functional activities of various systems, organs, tissues, and cells within the body, including roles in hormones, neurotransmitters, and inflammatory responses. Typically, peptides consist of 2 to 99 amino acids linked by peptide bonds, with molecular weights intermediate between those of small molecules and proteins. They originate from both natural and synthetic sources. To date, tens of thousands of polypeptides have been identified in living organisms.

Comparison of Selected Indicators Across Different Drug Classes

(Data source: Amber Pharmaceuticals' prospectus)

Peptide drugs have long been a hotly contested arena for global biotechnology and biopharmaceutical companies.

This is because, on one hand, peptide drugs have a relatively complex composition, share certain similarities with protein biologics in terms of performance, and exhibit short half-lives, leading to rapid clearance from the human body, which results in low-dose administration and low toxicity. On the other hand, compared with protein biologics, peptide drugs typically entail lower production costs and higher yields.

Meanwhile, technologies for peptide drug molecular design and peptide delivery are continuously innovating. Key issues that previously limited the clinical efficacy of peptide drugs—such as inability to be administered orally, short half-life, and poor cell membrane permeability—have been successively overcome, placing peptide drug development on a rapid upward trajectory.

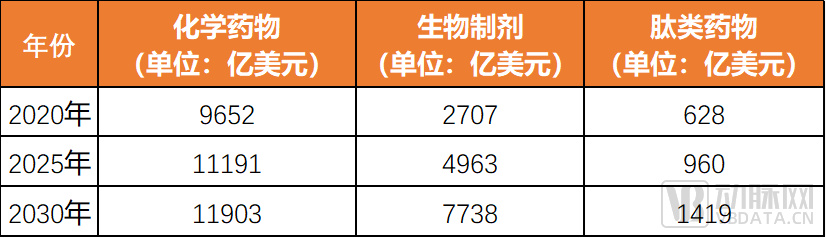

By the end of 2020, peptide drugs had become the second fastest-growing drug category globally. Statistics show that in addition to the 80 peptide drugs already on the market, approximately 440 peptide drugs are currently in clinical trials, and 400–600 are undergoing preclinical research. Among the three drug categories—chemical drugs, biologics, and peptide drugs—the global market growth rate of peptide drugs exceeds that of chemical drugs but remains lower than that of biologics. From 2016 to 2020, the global market size for peptide drugs grew at a rate of 2.6%, and this figure is projected to rise to 8.8% over the next five years.

Current and Projected Market Sizes for Three Drug Categories

(Data source: Anbo Pharmaceutical's prospectus)

Currently, multiple peptide drugs have received FDA approval for market launch worldwide, including star glucagon-like peptide-1 (GLP-1) receptor agonists such as liraglutide and semaglutide. Statistics show that in 2020, global sales of liraglutide-based drugs Victoza and Saxenda, indicated for the treatment of type 2 diabetes and obesity, reached $3.73 billion, while those of semaglutide-based drugs Ozempic and Rybelsus amounted to $3.54 billion.

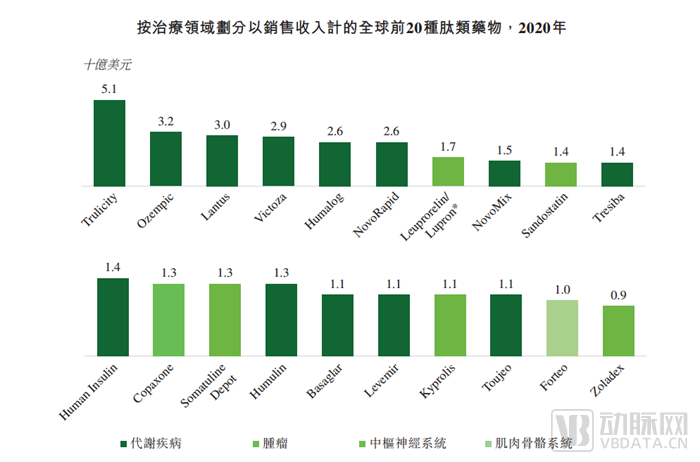

Currently, peptide drugs are primarily used to treat diabetes and other metabolic disorders, with a small number of peptide therapies approved for musculoskeletal diseases, tumors, and other indications. Statistics show that in 2020, 13 of the top 20 best-selling peptide drugs worldwide were indicated for metabolic diseases. Among these, the market size for insulin-related peptide drugs reached $27.2 billion, and is projected to grow at an annual rate of 3.5%–4.5% over the next decade.

(Data source: OncoTherapeutics' prospectus)

Notably, peptide drugs have demonstrated outstanding performance in the fields of rare diseases and chronic conditions, with a continuous emergence of blockbuster drugs such as glatiramer, liraglutide, semaglutide, dulaglutide, teriparatide, linaclotide, leuprorelin, and plecanatide.

Due to the unique nature of peptide drug research and development (R&D) and manufacturing, most therapeutic peptides are long-chain molecules composed of more than 30 amino acids, characterized by multiple disulfide bonds, macromolecular modifications, fatty acid conjugations, and hydrophobicity. Among companies engaged in peptide therapeutics, the majority of leading manufacturers choose to collaborate with contract development and manufacturing organizations (CDMOs) or contract research organizations (CROs) during the early stages of R&D. Consequently, the rapid advancement in peptide drug development has directly driven the growth of the peptide CDMO sector.

First, considerations from a cost perspective.The manufacturing process for peptide drugs is highly specialized, making it impossible to directly repurpose R&D and production equipment designed for small-molecule drugs or biologics. Since most new drug development companies typically maintain only one or two peptide drug pipelines, investing in an entirely new set of hardware facilities for peptide drug R&D and manufacturing is not cost-effective.

Next, considerations of efficiency and success rate.Peptide drugs differ significantly from small-molecule chemical drugs and biologics in pharmaceutical research, including process development, impurity profiling, analytical method development, and structural characterization. Due to the high professional barriers involved, collaborating with peptide CDMOs can help mitigate the risks associated with new peptide drug development and accelerate market entry.

Finally, there are compliance considerations.The unique compliance requirements for peptide drugs necessitate a dedicated talent pool specialized in this niche, along with responsive R&D and production management processes, to mitigate risks during development and manufacturing. Similarly, such a configuration is rarely sustainable as an independent entity within many pharmaceutical R&D companies that have already established or are preparing to establish peptide drug pipelines.

In fact, the clientele of peptide CDMOs includes both large pharmaceutical companies and biotechnology firms. Given that patents for several blockbuster peptide drugs worldwide have expired in recent years, unleashing substantial clinical demand, it becomes easier to understand the underlying rationale behind major pharmaceutical companies’ accelerated expansion of their peptide drug pipelines.

According to statistics, the global peptide CDMO market grew from $1.2 billion in 2016 to $2.0 billion in 2020, representing a compound annual growth rate (CAGR) of 13.3%. It is projected to increase from $2.0 billion in 2020 to $4.4 billion in 2025, at a CAGR of 17.7% from 2020 to 2025, and further rise to $7.9 billion by 2030. Currently, the United States holds the largest peptide CDMO market globally, followed by the five major European Union countries; together, these two regions account for approximately one-third of the global market share. Meanwhile, the Asian market is experiencing rapid growth, driven by biotechnology companies.

Currently, there are only four major peptide CDMOs in the market, with Ambow being one of them. It is generally challenging for conventional CROs, API manufacturers, and small-molecule CDMOs to enter the mainstream peptide CDMO sector.

First, peptide CDMOs that have transitioned from peptide CROs. This type of peptide CRO primarily serves research institutions, universities, and new drug R&D teams in enterprises. Peptide CROs often accumulate industry experience and resources over time. As their clients’ R&D efforts gradually move into the commercialization phase, these companies extend their service chain to the more stable commercialization stage. However, this transition requires many years of talent accumulation and the establishment of a GMP management system.

Second, peptide CDMOs transitioning from peptide active pharmaceutical ingredient (API) manufacturing. In recent years, a number of companies in China started with generic peptide drugs. Some of these enterprises achieved initial capital accumulation through generic peptide drugs and APIs, and thus chose to directly lay out new products, novel formulation technologies, innovative drugs, and internationalization to pursue leapfrog development. Others, which had accumulated certain industry experience and resources in software and hardware, R&D, and production but whose initial capital accumulation was insufficient for heavy-asset investments, opted to rapidly monetize by engaging in CDMO services. However, such companies require years of reputation building within the CDMO industry.

Third, small-molecule CDMOs are expanding into peptide CDMO services. As peptide therapeutics have become a hot and rapidly growing segment of the overall pharmaceutical market, an increasing number of leading, well-established CDMO companies are extending their businesses into peptide CDMO. Peptide manufacturing requires specialized equipment and technologies that differ from those used for small molecules; not every company possesses the capabilities to successfully expand into peptide CDMO, and there have been numerous historical cases of failure.

OnPharm, which is applying for an IPO, has been in operation for 14 years. The company was founded by Bai Juncai, former CEO of a U.S.-based peptide company. Its management team comprises many professionals with over two decades of experience in peptide manufacturing, including Chief Operating Officer Tim Nieters and Chief Scientist Mike Pennington.

Such peptide CDMOs typically uphold high quality standards. Their core teams possess a deep understanding of the needs of innovative drug developers, enabling them to rapidly respond to clients’ latest requirements and provide end-to-end services and deeply collaborative support for peptide drugs, spanning from early-stage R&D to commercialization. According to prospectus data, based on 2020 revenue, the top four peptide CDMO companies accounted for approximately 40.1% of the global peptide CDMO market. Ambio Pharmaceutical ranked fourth in the global peptide CDMO market with a 3.2% market share, slightly below the third-place holder’s 5.2%. Higher-ranked players include PolyPeptide and Bachem, known as the “European Duo.”

CDMO services typically encompass research, commercial manufacturing, and process development to support preclinical and clinical studies. Since commencing operations in 2007, Ambow Pharmaceutical has specialized in peptide CDMO services. Four years later, it established a subsidiary dedicated to peptide drug development. To date, the company has evolved into a full-service peptide specialist with vertically integrated capabilities in peptide drug development and manufacturing. These capabilities include R&D services, non-GMP intermediates, GMP starting materials, active pharmaceutical ingredients (APIs) ranging from preclinical to commercial scale, drug formulations, and analytical development and validation (excluding clinical trial services).

Peptide CDMO: Processes and Service Offerings

(Data source: Ambrx Biopharma’s prospectus)

To date, Ambow Pharma operates 16 peptide production lines across China and the United States, equipped with 1,000 L solid-phase reactors and 5,000 L liquid-phase reactors. With an annual output of over 300 kg of peptide active pharmaceutical ingredients (APIs), the company holds significant advantages in its technology platform, business model, and innovation capabilities.

Technical Platform:Ambow Pharmaceuticals boasts over 500 peptide experts, chemists, and industry professionals specializing in drug development and manufacturing, efficiently advancing fetal research, drug development, and drug production. The company possesses advanced technical capabilities in designing and optimizing commercial peptide manufacturing processes. By replacing recombinant processes with chemical synthesis, it reduces peptide production costs. Ambow has developed proprietary technologies employing combined liquid-phase and solid-phase synthesis methods to produce peptide fragments, which are then linked in solution to synthesize full-length peptides, thereby enabling the high-yield production of longer and more complex peptides.

Anbo Pharmaceuticals applies its proprietary technologies to the development and production of long-chain peptides with high purity, such as tirzepatide, liraglutide, and semaglutide. The company has developed a proprietary method for the selective introduction of multiple disulfide bonds into peptides. It is the first company globally to develop a scalable process for insulin analogs via chemical synthesis and has also specialized in the development of sustained-release peptide drugs.

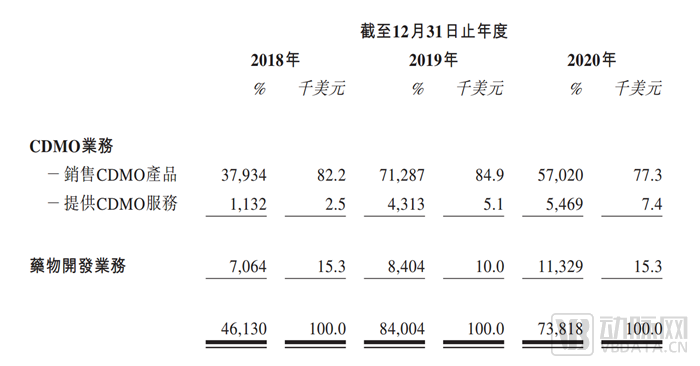

Business Model:Anbo Pharmaceuticals’ CDMO business comprises two segments: the sale of CDMO products and the provision of CDMO services. CDMO products refer to customized and non-customized peptide active pharmaceutical ingredients (APIs), while CDMO services encompass API process development and optimization, testing, regulatory filing, and storage services.

Typically, Ambow Pharmaceuticals establishes collaborative relationships with clients through early-stage services for novel molecule development and gradually progresses to late-stage commercial-scale manufacturing. Ambow Pharmaceuticals has stated that it will continue to enhance its coverage capabilities for high-value projects and aims to transcend the limitations of the clinical stage to enter commercial-scale supply, having already established peptide production service relationships with large pharmaceutical companies. The prospectus indicates that Ambow Pharmaceuticals’ revenue is primarily derived from providing peptide CDMO services to clients. Between 2018 and 2020, peptide CDMO revenue accounted for 84.7%, 90.0%, and 84.7% of total revenue, respectively. Prior to filing the prospectus, Ambow Pharmaceuticals was serving over 100 clients engaged in the development of new peptide drugs at the preclinical, Phase I, Phase II, and Phase III stages. These clients are primarily located in North America (62.5%), Asia (26.2%), and Europe (10.3%), with a top-customer retention rate as high as 80%.

Composition of Anbo Pharmaceutical's Operating Revenue, 2018–2020

(Source: OncoTherapeutics' IPO Prospectus)

Composition of CDMO Operating Revenue of Angbo Pharmaceutical from 2018 to 2020

(Data source: Ambo Pharmaceutical's prospectus)

On the other hand, Ambow Pharmaceutical’s peptide drug development business maintained rapid growth between 2018 and 2020. This was primarily due to the increasing number of milestone payments received by Ambow Pharmaceutical as time progressed and drug R&D advanced. This trend also led to a growing proportion of revenue derived from comprehensive long-term service contracts signed with pharmaceutical companies. For example, in July 2015, Ambow Pharmaceutical entered into a 20-year development, supply, and distribution agreement with Apotex, a global leader in biosimilars. In addition, Ambow Pharmaceutical is a major supplier of the active pharmaceutical ingredient (API) for plecanatide.

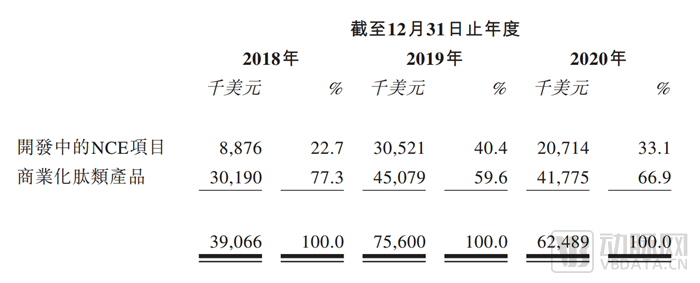

Innovation capability is primarily reflected in the peptide drug development business:From 2018 to 2020, the peptide drug development business generated revenues of $7.1 million, $8.4 million, and $11.3 million, respectively, representing a compound annual growth rate (CAGR) of 26.2%. During this period, the peptide drug development business, comprising upfront payments and milestone payments, accounted for an increasingly larger proportion of Ambow Pharma’s total revenue.

In reality, as an increasing number of biotechnology and biopharmaceutical companies establish peptide drug pipelines, innovation capability has become a key differentiator for peptide CDMOs. In 2020, the teriparatide drug co-developed by Ambow Pharmaceutical and Apotex completed bioequivalence validation against the originator product (Forteo) and received marketing approval in Canada. This achievement positions Ambow Pharmaceutical as a relatively successful case among peer peptide CDMOs in expanding into new drug development services. Over the past three years, Ambow Pharmaceutical entered into 10, 13, and 21 peptide drug development agreements with major global pharmaceutical companies, respectively, concurrently developing 9, 11, and 12 investigational peptide drugs. With its continuously enhancing R&D capabilities, Ambow Pharmaceutical has gained greater flexibility in pricing peptide drug development contracts, resulting in a year-on-year increase in contract values and strengthening its competitiveness within the industry.

However, just as the global peptide drug and peptide CDMO industries are in a state of constant flux, this IPO represents not only a milestone for Ambow Pharma but also the beginning of its direct confrontation with new challenges. VCBeat will continue to closely monitor Ambow Pharma’s subsequent development and market performance.