Flagship Pioneering Files IPO Prospectus: The Architect Behind Moderna’s Trillion-Dollar mRNA Revolution

Flagship Pioneering

Venture Capital Firms

Flagship Pioneering (hereinafter referred to as “Flagship”) is a unique entity in the U.S. investment community.

Unlike traditional venture capital firms, Flagship creates and incubates startups based on internally developed scientific intellectual property; external venture capital investments—those in companies founded by independent entrepreneurs or third parties—constitute only a small fraction of Flagship’s business.

In the words of founder Noubar Afeyan, Flagship is“A Fully Integrated Life Sciences Innovation Enterprise”, dedicated to continuous innovation in unique, “unoccupied” domains. Its innovation does not merely iterate or update existing technologies, but rather provides entirely new solutions for potential future problems and scenarios.

Since its founding in 1999, Flagship has launched and nurtured 109 life sciences companies, with a total value exceeding $90 billion.(Information sourced from official website news updates; however, the promotional pages on the official website have not been updated and still display $30 billion.) These enterprises include dozens of well-known innovative companies, with prominent names such as Moderna Therapeutics, Denali Therapeutics, Rubius Therapeutics, Sana Biotechnology, Seres Therapeutics, Syros Pharmaceuticals, and Quanterix featured on the list.

Among the 109 companies incubated and established by Flagship (since 2003), 24 have successfully completed initial public offerings (IPOs), while more than 30 others have continued to grow their businesses through acquisitions or mergers and acquisitions.According to Flagship, its portfolio companies currently have 53 clinical projects and 150 preclinical projects underway.

Undoubtedly, Flagship has pioneered a distinctive approach to venture capital, leveraging this unique strategy to solidify its position as a top-tier investment firm in the industry. Compared to all venture capital funds closed in the same vintage years, Flagship’s funds have ranked among the best performers and frequently topped the list of the 100 leading venture capital firms in the U.S. biotechnology sector.

So, what kind of organization is Flagship exactly? How has it achieved such remarkable success? What development model has it built? What are the key factors behind its success? What implications and insights does Flagship’s unique “approach” offer for China’s industry-incubated innovation and entrepreneurship?

VCBeat will help you address the above questions.

Noubar Afeyan, Founder of Flagship Pioneering

(Image source: Flagship Pioneering website)

In numerous public speeches, Noubar Afeyan, founder of Flagship Pioneering, has described himself as a “parallel entrepreneur” (simultaneously founding multiple companies). After nearly a decade of consecutive entrepreneurial endeavors, Afeyan realized that adopting the role of co-founder would offer greater scalability—providing him with more personal time and broader opportunities for growth. Consequently, he began to explore the feasibility of “parallel entrepreneurship,” abandoning the traditional mindset and development path of “serial entrepreneurship,” and embarked on an adventurous journey.

In 1999, Afeyan founded NewcoGen, an acronym for “New Company Generator,” to realize his vision of “institutionalized entrepreneurship.” Although Afeyan never intended to establish a venture capital firm—viewing capital merely as one input among others for startups—he recognized that investment was the only “systematic process” in the entrepreneurial world, whereby investment institutions channel funds into successive cohorts of nascent enterprises based on their own evaluation criteria. To reflect this “systematic” approach, the company was renamed Flagship Ventures in 2002.

14 years later (in 2016), to more accurately reflect its positioning and vision, Flagship Ventures was renamed Flagship Pioneering.In Afeyan’s view, “Ventures” still merely represents a capital input, fueling an internal engine for innovation and entrepreneurship aimed at systematizing the life sciences sector. What Flagship seeks to achieve is a pioneering process of “institutional entrepreneurship.” Clearly, “Pioneering” better reflects the company’s positioning and vision.

So, how exactly does Flagship carry out “institutional entrepreneurship”?

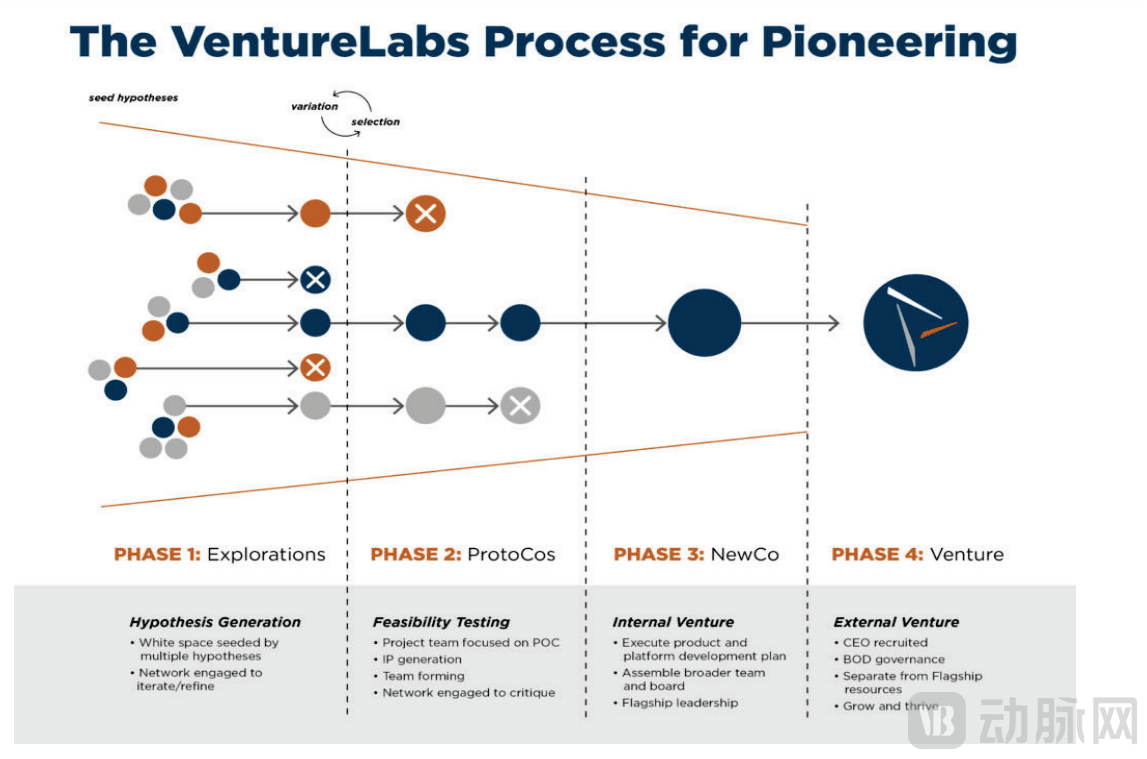

Image source: Flagship Pioneering official website

The process by which Flagship creates and incubates companies can be divided into four stages: Explorations → ProtoCos → NewCo → External Venture.

1. Hypothesis Exploration (Explorations)

During the hypothesis exploration phase, multiple senior executives from Flagship—typically two to three colleagues overseen by a partner, most of whom hold Ph.D.s in relevant fields—often engage in brainstorming sessions on internal innovation opportunities.They will propose various types of “risk hypotheses”—“what if?” scenarios—regarding whether cutting-edge technologies could offer solutions to problems and situations that may arise in the future. According to Afeyan, these “risk hypotheses” are purely products of imagination and are not constrained by the availability of existing scientific evidence or data.

After formulating hypotheses, Flagship relies on its extensive network of external collaborators—experts and industry professionals from academia and industry—to help select and refine the company’s ideas.When Flagship presents these imaginative, speculative ideas to external experts and industry professionals, it receives a mix of supportive and negative responses. Next,Flagship will take these supporting and opposing views into account, collaborate with external experts, and continuously iterate and refine its hypotheses.Test the weaknesses and strengths of new hypotheses, and propose increasingly refined ones until they identify some breakthrough technologies worth pursuing.

Flagship undertakes this process of proposing imaginative hypotheses and continuously iterating and optimizing them 80 to 100 times per year.

2. Scientific Validation (ProtoCos)

After three to six months, once the iteratively refined and optimized risk hypotheses have gained widespread recognition from the external collaborator network, they will enter the second phase—ProtoCos (ProtoCompanies). At this stage,ProtoCos is not a fully operational company; rather, it resembles a research project exploring the feasibility of certain hypotheses. At this stage, it is necessary to assess whether the project has the potential to evolve into a corporate entity.Therefore, the most important objective of this phase is trial and error.

“Generally, we aim to achieve scientific proof of concept within no more than one year and with an investment of no more than $1 million,” said Afeyan. At this stage,Each ProtoCo will be assigned a corresponding project number: “FL1,” “FL2,” “FL3,” …, and will undergo experiments designed to potentially expose its fatal flaws—known as “killer experiments”—to conduct scientific proof-of-concept validation for each project.These experiments are conducted at an experimental factory named “VentureLabs,” operated by Flagship. Projects that pass scientific validation will advance to the next stage—NewCo (New Company).

Flagship typically creates 8–10 ProtoCos each year. During the ProtoCo phase, Flagship begins to assemble a team of talent with relevant scientific and operational backgrounds for each project, while also engaging external scientific advisors. This phase is also when the company generates a substantial number of patents.

3. Establishment of NewCo

When the initial hypothesis exploration—the “what if?” question—yields a “here’s what happens” answer after scientific validation, ProtoCo, having passed the “test” of the research verification phase, advances to become NewCo, a true startup. NewCo will have its own official name and receive significant internal capital, but at this stage it remains affiliated with Flagship.

At this stage, Flagship’s most critical task is to formulate business strategies and product plans for NewCo, as well as to build a larger team.Each NewCo focuses on developing a proprietary platform to lay the groundwork for the continuous research, development, and production of new products in the future. Meanwhile, Flagship assembles a larger team of 20–30 people for each NewCo, along with a corresponding board of directors. In most cases, an internal partner from Flagship serves as the interim CEO. Flagship creates six to eight such NewCos annually.

4. External Venture Capital (External Venture)

In the final stage of Flagship’s incubation and creation of enterprises—the external venture capital stage—NewCo advances to the next level, evolving into GrowthCo (Growth Company), a growth-stage startup with independent operational capabilities. At this point,Flagship typically recruits a capable CEO from outside to formally operate the startup as a fully spun-out entity, while attracting substantial capital and partnerships from external sources to drive the company’s growth.

At this stage, some Flagship insiders who were involved in the company’s early development may choose to remain with that company or rotate to other NewCos to guide their growth. Although this phase attracts additional external capital, Flagship retains majority ownership and decision-making authority over the company.

According to Afeyan, a large number of risk hypotheses generated during the exploration phase are filtered out, while a small subset that undergoes iterative optimization advances to the ProtoCo stage. More than 50% of ProtoCos successfully evolve into NewCos. As NewCos mature into GrowthCos, substantial external venture capital begins to flow in, gradually giving rise to a cohort of companies with broad influence in their respective fields, such as Moderna, Denali, Rubius, Sana, and Quanterix.

Leveraging its unique system for creating and incubating startups, Flagship has carved out a successful and difficult-to-replicate development path, effectively “institutionalizing” entrepreneurship. Meanwhile, by consistently pursuing breakthrough innovations, Flagship enjoys a significant and enduring advantage over competitors in establishing dominance in new fields.

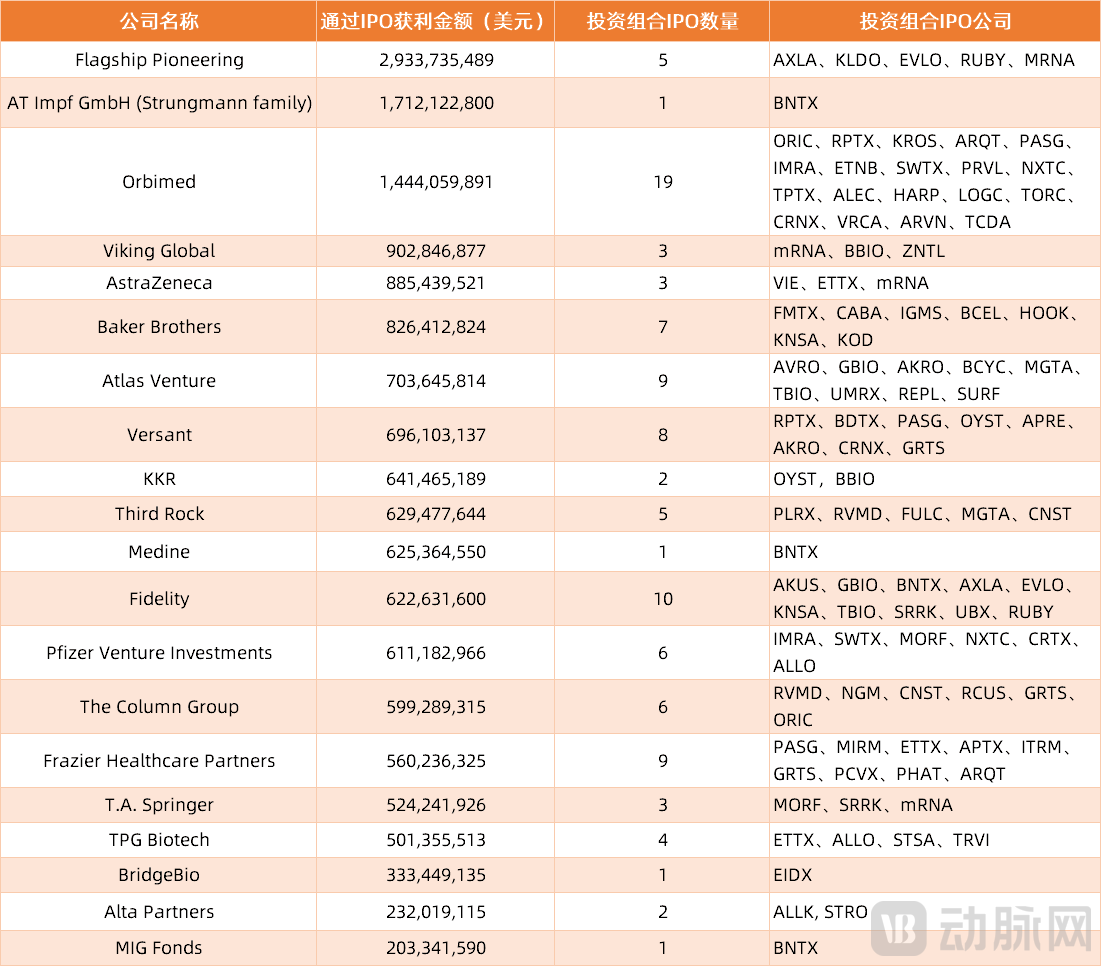

Compared to all venture capital funds that closed in the same year, Flagship’s funds are among the best performers.In 2020, in the ranking of the top biotech venture capital funds conducted by Bay Bridge Bio (based on investment return performance from 2018 to the first half of 2020), Flagship Pioneering topped the list of “venture capital firms with the highest IPO exit returns,” achieving an investment return of $2,933,735,489.

Ranking of Venture Capital Firms with the Highest Profits from IPO Exits in the First Half of 2018–2020

(Source: Public information, table compiled by VCBeat)

Flagship frequently tops the list of the top 100 venture capital firms in the U.S. biotechnology sector.

Based on the aforementioned development model for incubating enterprises established by Flagship, we can clearly discern its unique industry “playbook.” But how does this distinctive operational model deliver high returns? What are the key factors behind its remarkable success? VCBeat has summarized the following three points for readers’ reference.

First, because Flagship typically participates directly in the creation and incubation of its portfolio companies, it often assumes the dual role of founder and angel investor. Consequently, Flagship holds a significantly larger equity stake in these companies compared to typical venture capital funds.

A typical early-stage venture capital fund generally holds 20–30% equity in its portfolio companies, ultimately retaining 10–20% at the time of their IPO. In contrast, Flagship typically holds 60–100% equity in its portfolio companies, ultimately retaining 40–60% at the time of their IPO. This unique ownership position has made an exceptional contribution to Flagship’s returns.

We will provide a brief illustration using two typical cases incubated by Flagship Investment.

Rubius Therapeutics

Rubius Therapeutics, Inc. (Nasdaq: RUBY) is a clinical-stage biopharmaceutical company specializing in the genetic engineering of red blood cells. The company has created a novel class of cell-based medicines known as Red Cell Therapeutics™, introducing the concept of “red blood cell therapy.” Leveraging its proprietary RED PLATFORM, Rubius engineers therapeutic red blood cell products capable of producing drug proteins to treat various diseases, without causing side effects such as cytokine storms.

In 2013, Flagship participated in the incubation and creation of Rubius Therapeutics, bringing the discoveries of Professors Harvey Lodish and Hidde Ploegh from the Whitehead Institute for Biomedical Research at MIT to Flagship’s VentureLabs for scientific proof-of-concept. One year later, Flagship officially led the founding of Rubius. In 2017, Rubius was named one of the global “Fierce 15” biotech startups of the year by FierceBiotech. On July 18, 2018, Rubius went public on the Nasdaq with an IPO price of $23 per share, raising $241 million in its initial public offering and achieving an initial market capitalization of $1.8 billion.

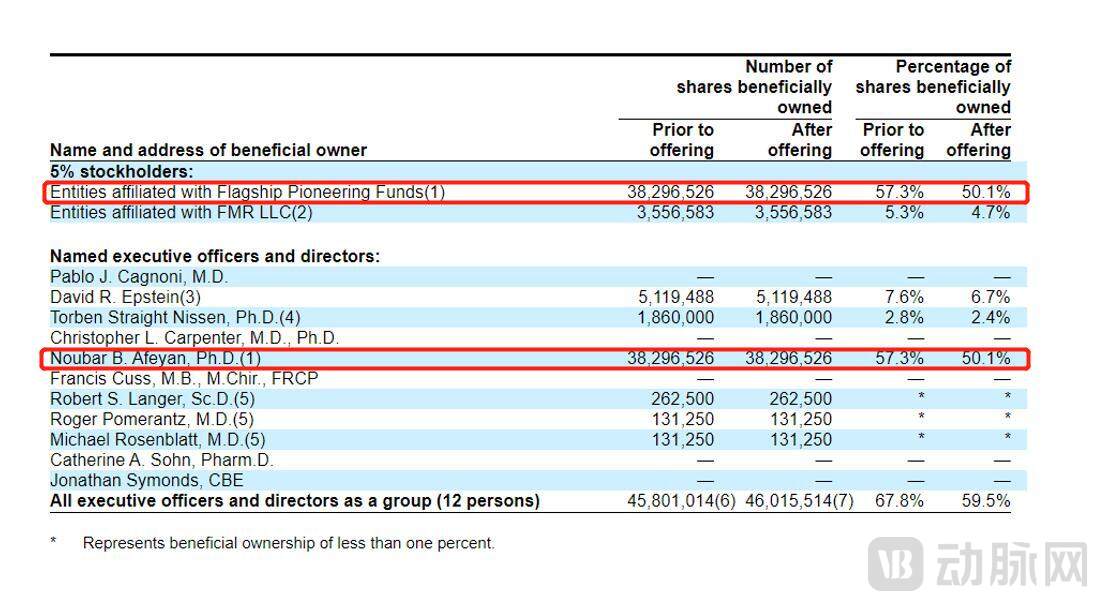

Rubius Therapeutics Prospectus

According to Rubius’ prospectus, Flagship held a 57.3% stake in the company prior to its initial public offering (IPO); following the IPO, Flagship’s ownership decreased to 50.1%. Based on Rubius’ initial market capitalization at listing, Flagship’s shareholding was valued at approximately $918 million (equivalent to RMB 5.94 billion) at that time.

Moderna Therapeutics

Moderna, the mRNA company that rose to prominence and became a household name during the COVID-19 pandemic, was internally incubated by Flagship under an “stealth mode” from 2010 to 2012. In January 2015, Moderna secured $450 million in private financing, marking the largest such round in the history of the biotechnology sector at the time. On December 6, 2018, the company made its debut on the Nasdaq, raising $604 million in its initial public offering (IPO) and setting a new record for the biotechnology industry.

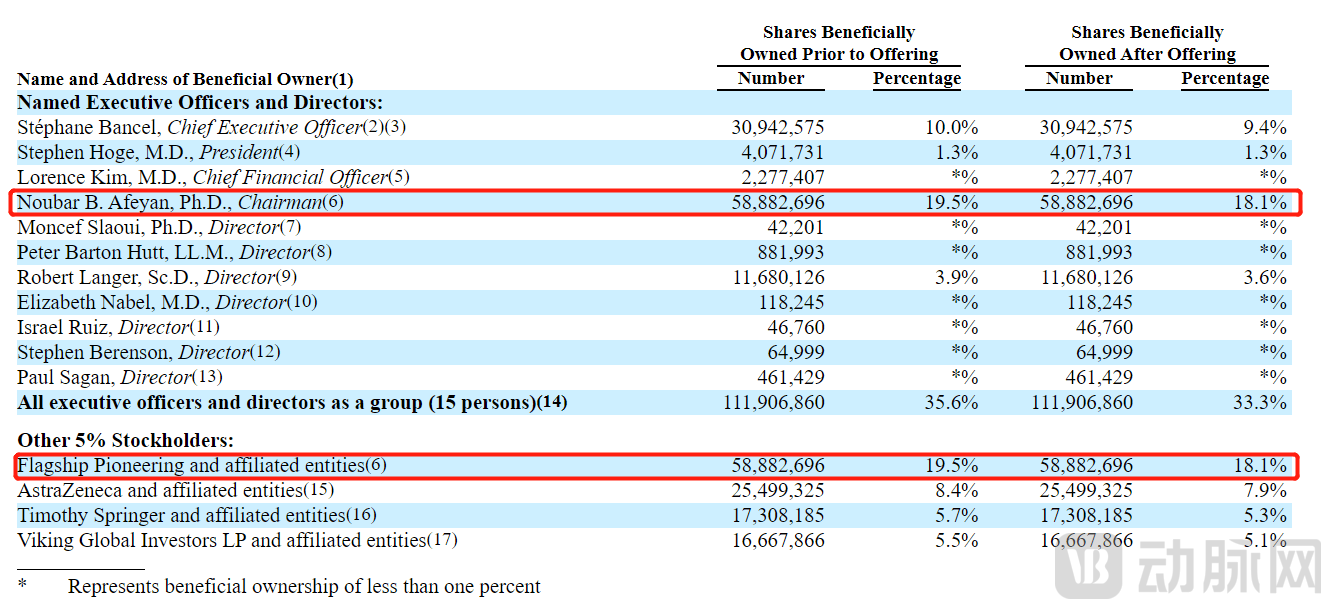

Moderna Therapeutics Prospectus

Prior to Moderna’s initial public offering (IPO), Flagship held a 19.5% equity stake in the company. Following the IPO, Flagship’s ownership was diluted to 18.1%, representing a total of 58,882,696 shares. Based on Moderna’s initial market capitalization at listing, Flagship’s holdings were valued at approximately $1.38 billion (roughly RMB 8.93 billion).

In 2020, Moderna shone brightly in the secondary market, with its stock price soaring directly to new heights due to its outstanding contributions to COVID-19 vaccine development. According to relevant data, Flagship has significantly reduced its holdings of Moderna shares since last year, cashing out a substantial portion and lowering its total shareholding to 24.3669 million shares, thereby achieving enormous investment returns.

Regarding the fascinating story between Moderna and Flagship, VCBeat previously reported in《How Did Moderna, the mRNA Industry Catalyst, Achieve a $400 Billion Market Cap in 10 Years?》A fairly detailed introduction has already been provided in the article; interested readers may choose to read it on their own.

Second, compared with pharmaceutical giants boasting a “cloud of patents,” Flagship’s performance in patent licensing is by no means inferior.

Flagship’s extensive portfolio of companies represents a vast source of inventions, enabling it to secure a large number of patent licenses with significantly lower investment compared to pharmaceutical giants that commit substantial resources.

According to statistics from the Derwent Innovation WIPO patent database, between 2015 and 2017, Flagship averaged 114 PCT patent publications per $100 million in R&D expenditure. In 2017, several large and mid-sized biopharmaceutical companies, such as Regeneron, BMS, Biogen, Pfizer, Gilead, and Vertex, averaged 26, 20, 16, 11, 10, and 10 PCT patent publications, respectively, per $100 million in R&D expenditure.

In 2017, Flagship’s total R&D expenditure was $1.2 billion, significantly lower than that of a representative biopharmaceutical company, yet its patent productivity surpassed that of these large and mid-sized companies in the biopharmaceutical industry. Over the past 20 years, Flagship has licensed more than 2,500 patents worldwide, filing over 300 patent applications in 2020 alone.

Third, Flagship boasts an exceptionally high success rate among its portfolio companies, measured by IPO outcomes.

To date, among the more than 100 life sciences companies incubated and nurtured by Flagship (since 2003), 24 have successfully completed initial public offerings (IPOs), while more than 30 others have continued to grow through acquisitions or mergers.

Flagship’s substantial equity stake enables it to secure significant capital returns whenever any of its incubated portfolio companies goes public.

A rich portfolio of patents serves as a “living spring,” enabling Flagship to continuously spawn new ventures based on its proprietary technologies and safeguard its exclusive technological rights.

The exceptionally high success rate of its incubated and invested companies directly leverages the aforementioned two advantages, propelling Flagship to the pinnacle as a star venture capital firm in the U.S. biotechnology sector.

According to statistics, Flagship has invested over $2.4 billion in the founding and development of its portfolio startups. However, we have found that the returns generated from Flagship’s investment in and incubation of Moderna alone have far exceeded the total capital invested in the more than 100 startups in Flagship’s history. Even after reducing its stake by nearly half, Flagship’s current holdings in Moderna are still valued at close to $10 billion. Of course, not every company in Flagship’s portfolio has performed as spectacularly as Moderna, but the outcome remains astonishing.

Flagship’s exceptional investment performance has made it highly successful in fundraising.In mid-June this year, Flagship announced that it had raised $3.4 billion for its latest fund (Fund VII).Following the completion of Fund VII’s fundraising, Flagship’s total operational capital pool stands at $6.7 billion, with $14.1 billion in assets under management.

Following Flagship’s completion of fundraising for Fund VII, Afeyan noted that the firm had launched “more than a dozen new internal projects” over the past year.“Over the next two and a half to three years, within the lifecycle of this capital pool (Fund VII), we may create approximately 20–25 new companies,” said Afeyan.

Flagship has pioneered a novel venture capital model, breaking with traditional investment conventions in the field and transforming entrepreneurship into an “institutionalized” process. Flagship’s internal staff hold multiple roles, serving simultaneously as industry practitioners, scientists, corporate executives, and investors.

“The definition of ‘venture capital firm’ clearly no longer aligns with Flagship’s positioning; it is merely its shell, not its soul. As Afeyan stated, Flagship is a ‘fully integrated life sciences innovation enterprise.’ However, we must also recognize that”The emergence of Flagship was inseparable from the close ties among the U.S. biomedical venture capital, industry, and research communities. It is precisely the high-frequency interactions within this tightly knit network that have enabled the formation of a “trinity” among academia, industry, and capital in the United States, thereby maximizing the efficiency of resources across all parties.

Currently, with the implementation of a series of supportive policies in China, the biopharmaceutical industry has developed rapidly, and a large number of new enterprises have sprung up. In some frontier fields, such as mRNA, domestic companies' ability to follow up with related product research and development is not inferior, and there is little gap compared with foreign levels.

However, we must also acknowledge that the rapid development of China’s biopharmaceutical industry has largely depended on returning entrepreneurs who are industry and technical talents with years of experience at large pharmaceutical companies (“Big Pharma”) and biotech firms abroad.Due to the late start of China’s biopharmaceutical industry and its relatively weak foundation in basic research, teams incubated for innovation and entrepreneurship from domestic universities remain a small minority.

Few institutions like Flagship bridge academia, industry, and capital to facilitate industrial incubation.Most early-stage angel investment firms in China typically invest by directly identifying expert teams with entrepreneurial intentions, yet they still lack the capabilities and resources to independently build and incubate teams based on specific research findings.

Although large-scale capital in China also participates in incubating and creating enterprises, compared to the high proportion of professionals with strong scientific backgrounds in Flagship teams, domestic team configurations are still dominated by industry practitioners, lacking participation from the scientific research system. In terms of hypothesis screening and scientific validation for certain projects, there is a lack of systematic processes and supporting collaborative resource networks.

With continuous development in recent years, some leading investment firms in the industry have accumulated strong industry resources and substantial financial reserves. They have begun to collaborate closely with governments and multinational large-scale pharmaceutical/medical device companies to establish healthcare industry incubators aimed at boosting the growth and development of startups.This also aligns with the current international trend in development models.

It will undoubtedly take time for China to achieve the highly efficient, tripartite collaboration among industry, academia, and capital seen in the United States. Nevertheless, star incubators such as Flagship Pioneering provide excellent case studies for us to learn from. It is the mission of the current generation of Chinese professionals in industry, academia, and investment to draw lessons from these successful models and forge a path for industrial incubation that aligns with China’s national conditions. We look forward to and believe that they will deliver an outstanding response to the call of our times.