Billion-Dollar Venous Intervention Market: Pipeline Completeness to Differentiate Domestic Players

With the volume-based procurement of coronary stents, the growth focus of vascular interventions has shifted from the coronary field to neurovascular and peripheral vascular areas. Peripheral interventions are divided into peripheral arterial interventions and peripheral venous interventions. Although venous interventions started later, they have developed rapidly. According to estimates by Industrial Securities, the Chinese market for venous intervention devices, primarily targeting common venous diseases such as varicose veins, deep vein thrombosis, and iliac vein compression syndrome, is valued at approximately RMB 19.46 billion.

In the fiercely competitive peripheral intervention market, which is projected to exceed RMB 10 billion, multinational giants such as BD, Medtronic, and Boston Scientific have established a strong presence, while domestic companies are rapidly emerging. Firms like LifeTech Scientific and JetMed Technology have built robust R&D pipelines in the venous sector.

Multinational giants entered the market early, leveraging innovative technologies, first-mover advantages, and substantial resource accumulation, while domestic enterprises have followed closely behind. How the Chinese venous intervention market will evolve, and which companies will emerge as leaders, remain uncertain. The only thing we are convinced of is that,Innovation Determines Survival。

Venous Disease: The Hidden Health Killer.

Venous diseases account for approximately 60% of peripheral vascular diseases and predominantly affect the lower extremities. In China, the prevalence of lower extremity venous diseases is 8.89%, corresponding to nearly 100 million patients. In terms of patient population size, there are 13 million stroke patients and 11.39 million patients with coronary heart disease in China; thus, the number of patients with venous diseases is several times that of these conditions.

Unlike arterial diseases such as stroke and coronary heart disease, venous diseases have an insidious onset and are rarely understood or prioritized. However, they are a “silent killer” that cannot be overlooked; they can progress rapidly and lead to severe complications. For instance, deep vein thrombosis (DVT) can trigger fatal pulmonary embolism. Statistics show that 100,000–300,000 people die from venous thromboembolism annually in the United States, while 500,000 die from it each year in Europe.

Peripheral venous disease is generally asymptomatic in its early stages, making it easy to overlook. This often leads to disease progression to advanced stages, which not only increases the difficulty of treatment but also imposes a heavy medical burden on patients. Therefore,Patient education on peripheral venous diseases conducted both in-hospital and out-of-hospital, development of diagnostic and therapeutic products better suited to Asian physiological characteristics, and improvement of diagnosis, treatment standards, and management protocols for venous diseases have become focal points of attention in the peripheral venous industry.。

Peripheral venous diseases mainly include three categories: varicose veins, deep vein thrombosis, and iliac vein compression syndrome, among which varicose veins are the most common venous disease.

Varicose veins are characterized by tortuosity and dilation of the lower extremity veins, resulting from factors such as blood stasis and weakened venous walls. This condition not only affects cosmetic appearance but may also lead to active ulceration and thrombus formation in advanced stages.

The "latent" nature of the early stages of varicose veins has resulted in a low treatment rate for this condition. In the United States, the prevalence of lower extremity varicose veins among adults is 23%. Among individuals aged 40 to 80 years, there are approximately 11 million male patients and 22 million female patients, yet only 1.9 million patients seek treatment.

High ligation and stripping of the great saphenous vein is a traditional surgical approach that remains commonly used, although it involves significant surgical trauma. Thermal ablation, foam sclerotherapy, and emerging techniques such as CHIVA and venous closure constitute minimally invasive treatments.

Radiofrequency ablation is the mainstream modality among thermal ablation therapies, delivering energy in the form of heat to the venous wall, thereby causing occlusion of the diseased vein. The Society for Vascular Surgery and the American Venous Forum recommend endovenous thermal ablation for the treatment of chronic venous insufficiency, with a higher strength of recommendation than open surgical procedures. With the market introduction of domestically produced radiofrequency ablation devices, endovenous thermal ablation is expected to become the mainstream therapeutic approach in China as well.

Beyond varicose veins, deep vein thrombosis is another major “roadblock” threatening cardiovascular health.

Blood clots “silently” in the deep veins, forming thrombi; only a minority of patients exhibit obvious symptoms, resulting in high rates of missed or misdiagnosis in the early stages. Deep vein thrombosis can lead to severe pulmonary embolism, which is the third leading cause of cardiovascular death after coronary heart disease and stroke.

For deep vein thrombosis, in addition to first-line anticoagulant therapy, there are four interventional treatments: catheter-directed thrombolysis (CDT), percutaneous mechanical thrombectomy (PMT), percutaneous transluminal angioplasty combined with stent implantation, and inferior vena cava filter placement. Catheter-directed thrombolysis involves delivering drugs directly to the thrombus via a catheter. Percutaneous mechanical thrombectomy, newly added in the third edition of the Guidelines for the Diagnosis and Treatment of Deep Vein Thrombosis, removes thrombi through mechanical methods such as maceration, fragmentation, extraction, dissolution, or liquefaction. Among these, thrombus aspiration catheters can apply negative pressure to directly aspirate the thrombus out of the vessel.

For patients who have developed deep vein thrombosis and are at high risk of embolus detachment, retrievable or temporary inferior vena cava filters are increasingly being used in clinical practice to prevent recurrent pulmonary embolism.

Iliac Vein Compression Syndrome is also a common venous disorder. It is a condition characterized by impaired venous return from the lower extremities and pelvis, caused by compression of the iliac vein by the adjacent iliac artery and spine, or by intraluminal abnormal adhesions.

With the continuous advancement of minimally invasive techniques, dedicated venous stents have become the first-line treatment for iliac vein compression syndrome.

According to Grand View Research, the global peripheral vascular medical device market is projected to reach $8.92 billion in 2020, with the United States remaining the largest market worldwide. In the global interventional market for venous diseases,BD, Cordis, Boston Scientific, and Medtronic are in the first tier.. Having entered the market early and achieved substantial scale, these companies have developed extensive product portfolios, with flagship products already launched in four key areas: inferior vena cava filters, thrombectomy devices, radiofrequency ablation catheters, and venous stents. The peripheral venous intervention sector has become a critical niche for innovation among multinational corporations in recent years, with venous intervention products emerging as their primary growth engine and even a major source of revenue.

Domestic medical companies have also taken note of the high-growth peripheral venous intervention sector. In terms of product R&D layout, these companies have adopted different strategic focuses, with some proactively building robust pipelines of investigational products in the venous intervention space. Based on available information, VCBeat has compiled an overview of the key players and their products in China’s venous intervention market.

Major Players in the Venous Interventional Device Market

Major Players in the Venous Interventional Device Market

Overall, most domestic venous intervention companies focus on single-product portfolios, with few enterprises offering a comprehensive product line in the venous intervention field.

Domestic companies primarily focus on three major disease areas: deep vein thrombosis, varicose veins, and iliac vein compression syndrome, developing their flagship products around inferior vena cava filters, thrombus aspiration catheters, radiofrequency ablation catheters, and iliac vein stents.

Although both domestic and international companies have established a presence in the venous disease sector with individual products, the performance of existing venous interventional devices still requires improvement. VCBeat has compiled a comprehensive overview of the market participants and R&D directions of emerging companies for major interventional products across the three primary areas of venous disease.

Radiofrequency Ablation

In the field of varicose veins, which has the highest patient prevalence, radiofrequency ablation is experiencing rapid adoption. According to Frost & Sullivan statistics, the number of varicose vein cases treated with radiofrequency ablation in China increased from 2,700 in 2015 to 26,300 in 2019, representing a compound annual growth rate (CAGR) of 76.9%. The rapid development of the radiofrequency ablation sector has attracted domestic companies such as Scientech, Hengrui Medicine, and Acotec, whose products have successively entered clinical trial phases.

Domestic Radiofrequency Ablation Catheter Products

Medtronic holds absolute dominance in the field of radiofrequency ablation, with its radiofrequency ablation catheter being the first product approved by the NMPA, thereby establishing a high technical barrier.

However, radiofrequency ablation faces challenges in precisely targeting treatment sites and controlling thermal energy. Chinese manufacturers have improved radiofrequency ablation products. The venous radiofrequency ablation catheter developed by Zenflow Medical utilizes a softer nylon material, offering excellent wire-free navigability through tortuous vessels and enabling segmented ablation. Furthermore, this catheter delivers radiofrequency energy to the heating element located in the distal treatment zone while transmitting temperature feedback to the radiofrequency generator, thereby achieving visualized monitoring of radiofrequency energy delivery.

Building upon traditional radiofrequency ablation systems, the implementation of visualization and intelligent temperature control to enhance the safety of radiofrequency ablation procedures will inevitably widen the technological gap between products and establish a competitive barrier for enterprises.

Vena Cava Filter

The treatment of deep vein thrombosis and the prevention and management of pulmonary embolism are also key areas in venous intervention.

China offers a comprehensive range of domestic vena cava filters, with a high rate of substitution by locally produced alternatives. Among numerous imported and domestic brands, LifeTech Scientific’s Aegisy filter has captured approximately 56% of the market share, emerging as a successful “breakout” product in the peripheral intervention field.

Vena cava filters can be classified into umbrella-shaped filters and fusiform filters.Umbrella-shaped filters have a prolonged retrieval window but are prone to tilting and perforation within the human body. For instance, BD’s Denali filter features an extended retrieval window, with an average retrieval time of approximately 201 days. In contrast, fusiform filters have a shorter retrieval window, typically around 14 days, but are less susceptible to tilting; LifeTech Scientific’s Aegisy filter is a fusiform device with a 14-day retrieval window. Clinically, inferior vena cava (IVC) filters are generally implanted for more than two months. From a development trend perspective, umbrella-shaped filters with longer retrieval windows hold greater market potential than traditional fusiform filters.

Working Principle of Umbrella-Shaped Filters Source: Zentech Medical

Furthermore, the types of inferior vena cava (IVC) filters are continuously expanding. B. Braun’s convertible IVC filter can be converted into an IVC stent when needed, while biodegradable IVC filters are currently undergoing animal studies.

Amid rapid advancements, the use of vena cava filters has remained controversial. Neither umbrella-shaped nor fusiform filters have achieved the dual goals of extended retrieval windows and resistance to migration. The 2019 Clinical Practice Guidelines for Vena Cava Filters recommend the use of retrievable filters. However, clinical practice continues to face challenges such as low retrieval rates and a high incidence of complications associated with long-term implantation.

Therefore, companies both domestically and internationally are committed to developing inferior vena cava (IVC) filters with more rational structures, longer retrieval windows, and easier implantation and retrieval, thereby providing a longer therapeutic window for thrombosis treatment. The retrievable IVC filter under development by Zhenjiang TransMed adopts a three-layer umbrella structure created through integrated laser cutting of nickel-titanium alloy. This design offers excellent stability, while its hollow tubular structure helps reduce the formation of secondary thrombi. Currently, clinical trial enrollment for this product has been completed.

Three Vena Cava Filter Products Under Development

It is evident that vena cava filter products are evolving toward longer retrieval windows and higher stability,Effective filter recovery will be a key focus for product improvement.。

Thrombectomy Catheter

Thrombectomy catheters are a “powerful tool” for treating deep vein thrombosis. Currently, nine thrombectomy catheters have been approved in China, all of which are imported products; among them, only the thrombectomy catheters from Straub Medical and Boston Scientific are indicated for use in peripheral veins.

Traditional aspiration catheters have a simple structure but low thrombus removal efficiency. In contrast, Straub Medical’s RotarexS device employs a high-speed rotating helical rotor to cut, fragment, and evacuate thrombi, thereby integrating three functions: aspiration, maceration, and thrombus transport. Meanwhile, Boston Scientific’s AngioJet generates negative pressure through high-velocity saline jets to aspirate thrombi and fragment them within the catheter; furthermore, thrombolytic agents such as urokinase are added to the saline, enabling dual functionalities of “hydrodynamic aspiration and thrombolysis.” However, these novel devices may cause hemolysis during thrombus aspiration, thereby increasing clinical risks. They also require specialized equipment and are costly, which hinders their adoption at primary healthcare facilities.

There remains substantial room for innovation among domestic brands in the thrombectomy catheter market. For instance, the venous thrombectomy catheter developed by Weiyu Medical, a subsidiary of Leo Med, transforms the surgical Fogarty embolectomy into a minimally invasive endovascular procedure, eliminating the need for specialized equipment or thrombolytic agents. Meanwhile, the thrombus removal device under development by Endovastec features an integrated three-in-one functionality of thrombolysis, thrombus fragmentation, and aspiration, making it more suitable for deployment at primary care institutions and meeting the demand for localized thrombosis treatment.

Novel thrombectomy devices integrate functions such as aspiration and thrombolysis, aiming to enhance the efficacy of thrombus treatment; however, improvements in safety and cost-effectiveness will be key determinants of their successful commercialization.

Venous Stent

Until 2019, China had no dedicated venous stents, and arterial stents were commonly used intraoperatively to treat iliac vein occlusive disease. HoweverSignificant Anatomical Differences Between Arteries and Veins, arteries have relatively small lumens, thick walls, and high elasticity, whereas veins have large lumens and low elasticity. Therefore, using arterial stents in veins may lead to complications such as thrombosis and vascular tear or perforation. Dedicated venous stents need to simultaneously provide adequate radial force and vascular compliance, making them a key focus of research and development for companies both in China and abroad.

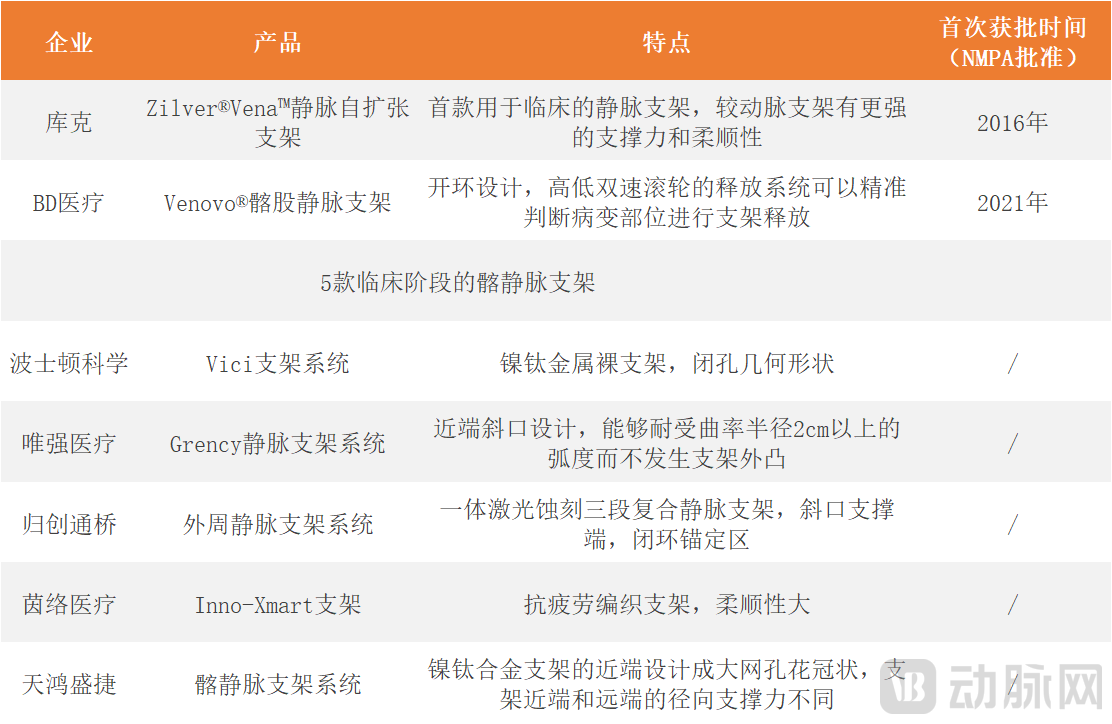

Currently, two products have been approved in China, both of which are imported and carry high price tags. Although several international products are available, including Venovo (BD), Zilver Vena (Cook Medical), Wallstent (Boston Scientific), and Abre (Medtronic), none has yet emerged with a clear dominant advantage. Meanwhile, Chinese companies such as JetMedical, BluePulse Medical, Tianhong Shengjie, and InnoCare Medical are actively engaged in R&D, suggesting that the market is poised for intense competition. Through independent innovation, domestic enterprises are well-positioned to achieve “overtaking on the bend” in the venous stent sector.

Domestic Venous Stent Products

Zynlastic, the venous stent from Genesis MedTech, is undergoing clinical trials led by the First Affiliated Hospital of Chongqing Medical University. This stent is a product of medical-engineering collaboration. The stent adoptsBeveled Tip Design, to fully cover the compressed segment of the vein, while the middle section of the stent is soft and can well conform to the natural curvature of the iliac vein. Moreover, this stentEquipped with a handle for precise deployment and repeatable positioning, capable of adjusting the position of the stent within the human body.

Zynlastic Venous Stent by GuiChuang TongQiao

Furthermore, Tianhong Shengjie’s venous stent has taken the lead in completing 12-month clinical follow-up, securing a first-mover advantage among domestic peers. In contrast, the Inno-Xmart stent developed by Innolife Medical is a braided stent with fatigue-resistant properties, differing from conventional laser-cut stents.

Overall, Chinese companies are capitalizing on the rapid growth of the venous intervention market by establishing a presence in key device segments, striving for independent innovation across product dimensions, and actively advancing product commercialization. The venous intervention market is characterized by intense competition, where those who strive take the lead; domestically produced products are gradually surpassing imported ones, ushering in the dawn of the “me-better” era.

Barring any unforeseen circumstances, the field of venous intervention is poised for a period of robust growth in the coming years. With over 100 million patients suffering from lower extremity venous diseases and a device market size exceeding RMB 10 billion, the sector is attracting an increasing number of enterprises. Beyond traditional therapies, new mechanisms, novel treatments, and innovative devices are continually emerging, ensuring that the venous intervention market never lacks capacity.

As China’s population ages and patients become more conscious of disease treatment, venous conditions previously deemed “non-disruptive” are now being prioritized for minimally invasive interventions. To meet the substantial patient demand, top-tier (Grade A tertiary) hospitals across China are progressively establishing vascular surgery departments and cultivating specialized professionals.

Currently, China’s venous intervention market remains in its early stages of development. Imported products are scarce and struggle to meet the growing domestic demand for disease treatment, leaving substantial market space for domestic brands. Furthermore, there is significant room for innovation in venous intervention products. Domestic companies possess inherent market advantages, as they have a deeper understanding of the current clinical landscape for Chinese patients and are well-versed in national medical insurance policies. This enables them to conduct research and development based on clinical needs through close collaboration between medical professionals and engineers. Products from companies such as LifeTech Scientific, JetMed, and Tianhong Shengjie are currently in clinical trials and are expected to receive approval in the coming years, positioning them to rapidly lead the market.

Taking Jointcare’s product portfolio as an example, let us examine the comprehensive development direction of its venous intervention product line. In both neurointerventional and peripheral interventional fields, Jointcare is committed to developing a complete suite of disease-specific solutions.Within its comprehensive venous intervention solutions, ZendoVasc’s key devices—including venous stents, retrievable inferior vena cava (IVC) filters, filter retrieval snare kits, and radiofrequency ablation closure catheters—have successively completed clinical trials or received market approval.Meanwhile, the company is also developing products such as thrombectomy devices, thrombolytic catheters, and venous capsules.Across the three major domains of venous intervention, ZC Medical is achieving organic integration and strategic prioritization of its core products. This may well be the key for domestic companies to rapidly break through in the field of venous intervention.