Infervision Files for Hong Kong IPO After Over 300% Revenue Growth for Two Consecutive Years

Infervision

Artificial Intelligence Product Developer

On the evening of August 20, Infervision Medical Technology Co., Ltd. (hereinafter referred to as “Infervision”) filed its prospectus with the Main Board of the Hong Kong Stock Exchange, with Goldman Sachs, UBS, and CSC Financial International serving as joint sponsors.

Infervision, founded in 2016, was among the first startups to enter the field of AI-powered medical imaging. Since its inception, Infervision has consistently stayed ahead of its competitors; it was the first medical imaging company to reach Series C financing and obtained the first Class III medical device certificate for pulmonary nodule detection approved by the National Medical Products Administration (NMPA). Today, Infervision is once again taking the lead as it approaches the threshold of an initial public offering (IPO).

No longer just the “pulmonary nodule AI company” it once was, Infervision now boasts an AI portfolio comprising 15 products, and its annual report reveals revenue figures that place it among the industry’s top performers.

Looking back at the rise of medical AI to date, there have been no fewer than a hundred companies targeting pulmonary nodules. Why has Infervision managed to stand out from the crowd and bring AI into broader healthcare scenarios?

The head of Infervision does not have a medical background.

After graduating from high school, Chen Kuan remained at the University of Chicago to study economics and finance. He studied under James J. Heckman, a pioneer in microeconometrics who was awarded the Nobel Prize in Economics in 2000. Until that point, he had had little exposure to the healthcare sector.

According to the conventional script, he was destined to earn dual Ph.D. degrees in Economics and Finance at this world-class university and then secure a prestigious job in Silicon Valley. However, in 2014, while pursuing his doctoral studies, family-related circumstances suddenly made him realize that he had already spent two decades in academia—far too long. He aspired to leverage his expertise to create tangible social value, and he chose AI as his instrument.

By the end of that year, Chen Kuan, who had put his studies in Chicago on hold, borrowed money from relatives and rented a dilapidated small room outside a hospital in Sichuan. From then on, he devoted himself entirely to the research and development of AI for medical imaging. According to him, he would go to the hospital early every morning and once went four days without bathing.

The influence of Chen Kuan is evident in Infervision’s later-stage team. In 2018, the Center for Medical Device Evaluation had not yet clarified the approval procedures for medical AI, but Infervision’s AI products had already garnered praise from physicians at numerous hospitals. A radiologist from Shijiazhuang once told VCBeat, “The Infervision team is incredibly dedicated. They practically live, eat, and conduct their research at the hospital. We often provide feedback and suggestions regarding their AI solutions, and their response time is always the fastest.”

Establishing effective communication with physicians and hospitals is key to the commercialization of medical enterprise products. Under this service model, Infervision has achieved rapid deployment. From August 2018 to March 2021, its products were deployed in more than 400 hospitals worldwide.

Chen Kuan’s background in economics and management quickly became a significant asset as technology companies matured. In the field of molecular diagnostics, which is adjacent to AI-powered medical imaging, half of the CEOs of listed companies come from economics and management backgrounds. As one of the first entrepreneurs in China to enter the medical AI sector, Chen Kuan has grown alongside the industry. Beyond his strengths in economics and management, he possesses a profound understanding of AI technology itself.

Thus, from its inception to the filing of its prospectus, Infervision has indeed served as a bellwether among leading enterprises in many respects. For instance, it obtained the first Class III medical device certificate for AI-based pulmonary nodule detection in China, demonstrating the superior efficacy and non-inferiority of AI technology in clinical settings. Furthermore, its regulatory approvals in the United States, the European Union, and Japan have provided a viable roadmap for other AI companies seeking overseas expansion.

These various choices have shaped today’s Infervision. Returning to the prospectus, two data points stand out prominently.

First, revenue has grown more than threefold, with annual income expected to exceed RMB 100 million. According to the prospectus, Infervision’s operating revenues in 2019 and 2020 were RMB 6.62 million and RMB 27.7 million, respectively, representing a year-on-year growth of 318%. In the first quarter of 2021, the company achieved revenue of RMB 22.13 million, a 357% increase from RMB 4.84 million in the same period last year. Based on the proportion of Q1 2020 revenue to full-year revenue, it is roughly estimated that Infervision’s total revenue for 2021 is expected to reach RMB 125 million.

Second, operating losses continue to narrow, with a turnaround to profitability expected in the future. After excluding share-based compensation and changes in the fair value of preferred shares, Infervision’s adjusted losses for 2019, 2020, and the first quarter of 2021 were RMB 151.74 million, RMB 125.26 million, and RMB 12.69 million, respectively, demonstrating a consistent narrowing of operating losses. Sales and administrative expenses also decreased from two to three times sales revenue to approximately 60% of sales revenue. The data for 2021 is particularly notable, with the loss amount being less than half of that recorded during the same period in 2020.

These two data points offer a glimpse into Infervision’s development journey. In 2019, Infervision had not yet obtained any Class III AI medical device certifications, with annual revenue totaling only RMB 6.62 million. In other words, in 2019, while still in the R&D phase, Infervision’s revenue was virtually negligible. However, as Infervision’s product portfolio began to take shape in 2020, its revenue surged threefold that year.

As Infervision’s AI for pulmonary nodules and AI for pneumonia received Class III medical device approvals from the NMPA in November 2020 and March 2021, respectively, and given that Infervision generated nearly a full year’s worth of revenue within just three months, its operating income is expected to grow further following the March approval of its pneumonia AI solution, which boasts broader application scenarios.

Despite having achieved significant breakthroughs, Infervision cannot rely solely on a few products, such as those for pulmonary nodules and pneumonia, to go further.

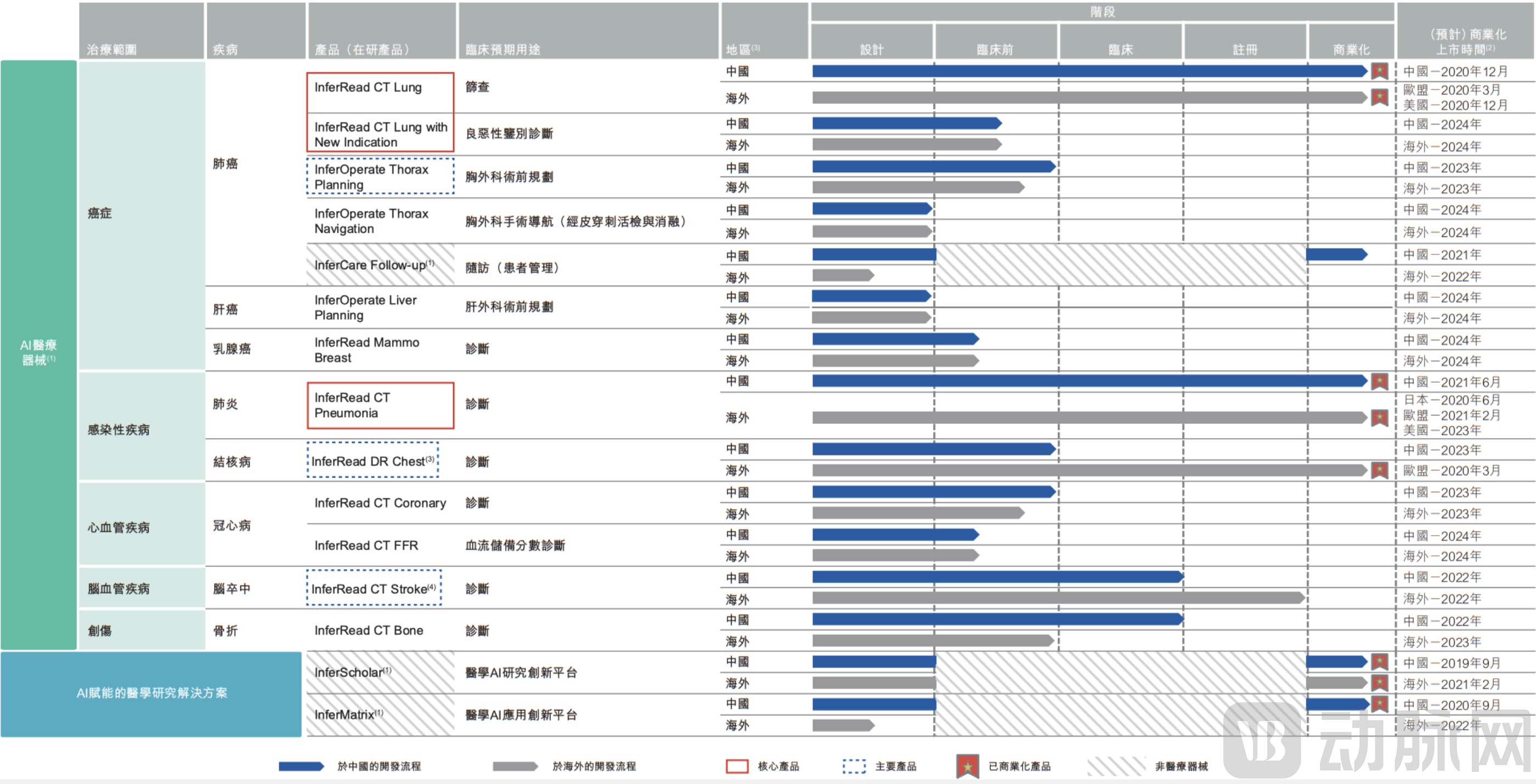

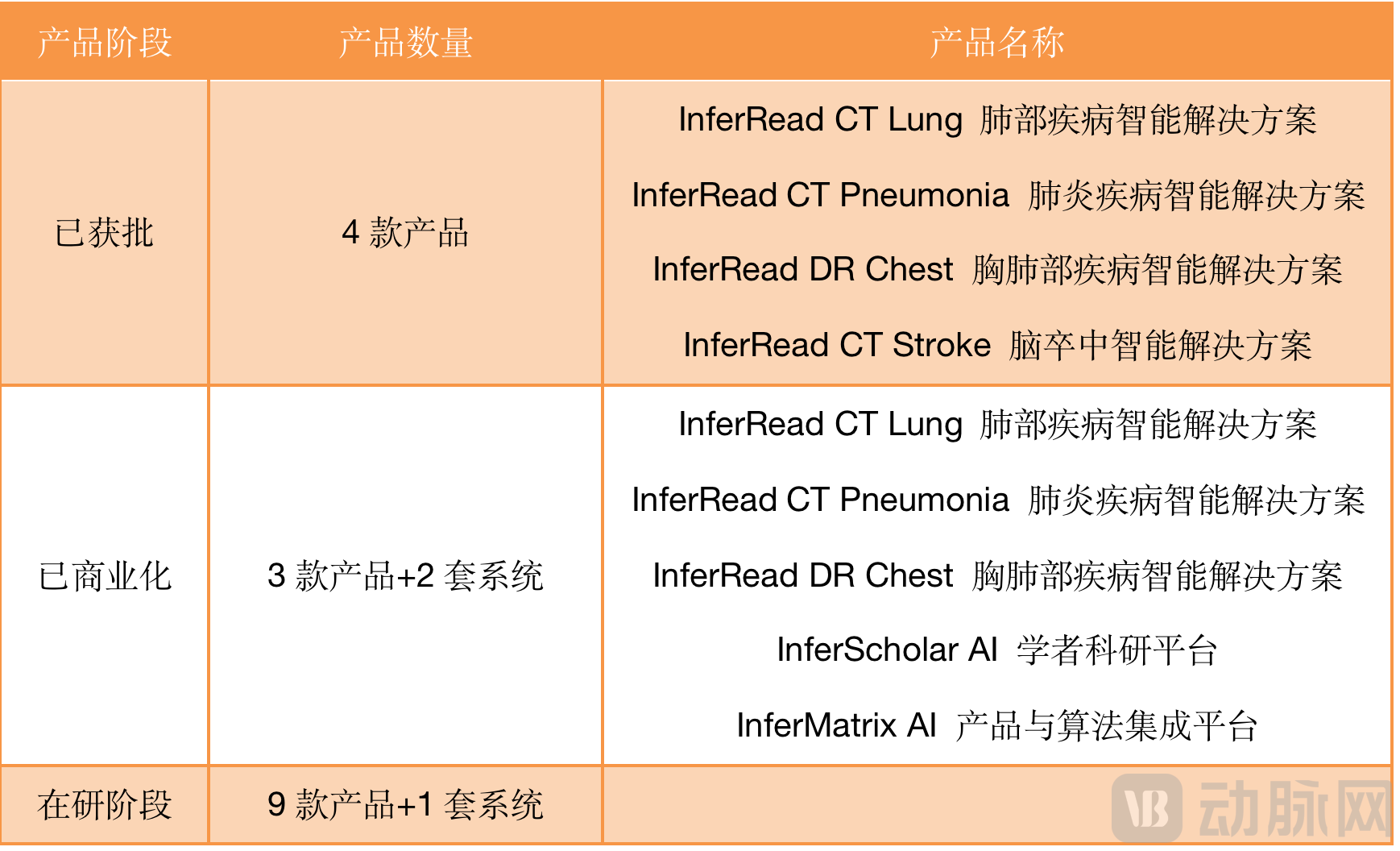

In fact, Infervision has established a portfolio of 15 medical AI products, among which four have received regulatory approval, three products and two systems have been commercialized, and nine products and one system are currently under development. All products are scheduled to achieve commercial deployment by 2025.

Infervision AI Product Matrix

From the perspective of the entire pipeline, Infervision’s product portfolio can be categorized into four strategic pathways. These four pathways broadly encompass the development models adopted by the vast majority of medical AI companies currently on the market:

First, we are continuously deepening the development of our flagship AI product for pulmonary nodules, evolving it from a simple nodule classification tool into a comprehensive CT-based auxiliary diagnostic system for the lungs. This system aims to rapidly identify and detect suspicious pneumonia lesions (including those caused by coronaviruses), analyze their volume and density, and compare changes in lung lesions depicted across CT images.

Second, building on the successful R&D experience in pulmonary AI, we will expand vertically to explore the application of AI in diseases with large patient populations and significant screening value, such as liver cancer, breast cancer, pneumonia, tuberculosis, and stroke.

Third, there is a shift from radiology departments to clinical specialties, with the development of AI-powered thoracic surgical navigation systems for percutaneous biopsy and ablation in thoracic surgery, and CT-derived fractional flow reserve (CT-FFR) applications in cardiology.

Fourth, it has built a medical AI research innovation platform and a healthcare AI application innovation platform for physicians to accelerate scientific research and its translation, thereby fostering the development of a sustainable AI ecosystem.

Infervision Product Status

Behind the strength of its pipeline lies a concentration of talent. To ensure the value and future sustainable development of medical AI, Infervision has assembled an R&D team of 110 members, all graduates of prestigious institutions such as the University of Chicago, Tsinghua University, and Peking University. Over 40% hold master’s or doctoral degrees, and approximately 20% have medical or biotechnology backgrounds in fields such as radiology, clinical medicine, biomedicine, and pharmacology.

This has been accompanied by substantial R&D investments and share-based compensation expenses. Data shows that for the years ended December 31, 2019 and 2020, and for the three months ended March 31, 2020 and 2021, Infervision’s administrative expenses were RMB 43.44 million, RMB 143.07 million, RMB 14.15 million, and RMB 14.47 million, respectively, accounting for 656.0%, 516.5%, 292.5%, and 65.4% of revenue during the corresponding periods. Specifically, while Infervision’s share-based compensation expenses did not increase in the latest year, their proportion of revenue declined significantly due to revenue growth.

R&D expenses were also substantial. For the years ended December 31, 2019 and 2020, and for the three months ended March 31, 2020 and 2021, Infervision’s R&D expenses amounted to RMB69.0 million, RMB66.8 million, RMB13.2 million, and RMB14.9 million, respectively, representing 1,042.7%, 241.3%, 272.3%, and 67.2% of its revenue for the corresponding periods. This indicates that its annual R&D expenditures fell within the range of RMB60 million to RMB70 million.

If the product-based ecosystem constitutes Infervision’s first competitive moat, then, drawing on the development logic of the healthcare informatics sector, medical enterprises seeking to maximize scale must embed their robust products within hospitals and establish strong institutional ties. In this light, if Infervision can leverage its first-mover advantage to capture as much market share as possible, does this imply a significant reduction in sales costs for subsequent product launches?

This hypothesis still requires further validation. However, for the medical device sector, which is heavily reliant on distribution channels, Infervision has already established its second barrier to entry—commercialization.

Looking back at the history of global technological development, humans have consistently excelled at automating highly repetitive tasks, replacing manual labor with machinery. Medical AI, however, aims to go beyond mere automation of repetitive work to address personalized medical challenges. From this perspective, medical AI uncovers latent needs for physicians through its inherent value. To make physicians aware of these needs and proactively articulate them, medical AI enterprises must demonstrate the value of AI.

From the current perspective, the value that medical artificial intelligence can bring can be roughly divided into two aspects: efficiency improvement and cost reduction.

Efficiency enhancement refers to the use of AI-based medical devices to assist physicians in streamlining workflows and supporting clinical decision-making, thereby improving the effectiveness of disease screening and diagnosis, disease intervention, and patient management. For example, clinical trials of Infervision’s InferRead CT Lung in China demonstrated that AI-assisted pulmonary nodule detection improved sensitivity by more than 40% compared to unassisted performance, while reducing image interpretation time by nearly 15%.

This feature addresses the issues of insufficient physician supply and suboptimal healthcare quality. According to a Frost & Sullivan report, China had 2,496.1 physicians per million population in 2020, which was 20.3% lower than the United States’ figure of 3,132.5 physicians per million population. Furthermore, although tertiary hospitals accounted for only 8% of all hospitals in China in 2020, they handled 54.2% of the nation’s total outpatient visits. Integrating AI into primary care settings can effectively improve the quality of grassroots healthcare, alleviate the burden on tertiary hospitals, and provide high-quality services to more patients.

Cost reduction refers to the early detection and intervention in disease progression to achieve better treatment outcomes and significantly lower overall medical expenses. For example, the cost of treating cancer is generally lower when it is first diagnosed at an earlier stage. In China, the estimated lifetime direct treatment cost for patients initially diagnosed with early-stage lung cancer is $9,200, whereas for those initially diagnosed with late-stage lung cancer, the lifetime direct treatment cost is nearly double ($17,800).

Due to the nonspecific early symptoms of lung cancer and the limited sensitivity of conventional chest radiographs in detecting it, a large number of patients in China are diagnosed at an advanced stage. In such cases, patients and hospitals incur substantial treatment costs, yet therapeutic outcomes remain poor. Therefore, if AI-enabled lung cancer screening could be decentralized to increase its penetration rate, a significant proportion of patients would have the possibility of curative treatment, thereby substantially reducing both medical insurance expenditures and out-of-pocket costs for individuals.

Thus, the emergence of medical AI represents a win-win scenario for four stakeholders: hospitals, health insurance providers, enterprises, and patients. Enterprises generate revenue by providing services; hospitals enhance operational efficiency and improve service quality; health insurance providers reduce expenditures; and patients benefit from access to richer medical resources thanks to the advent of AI.

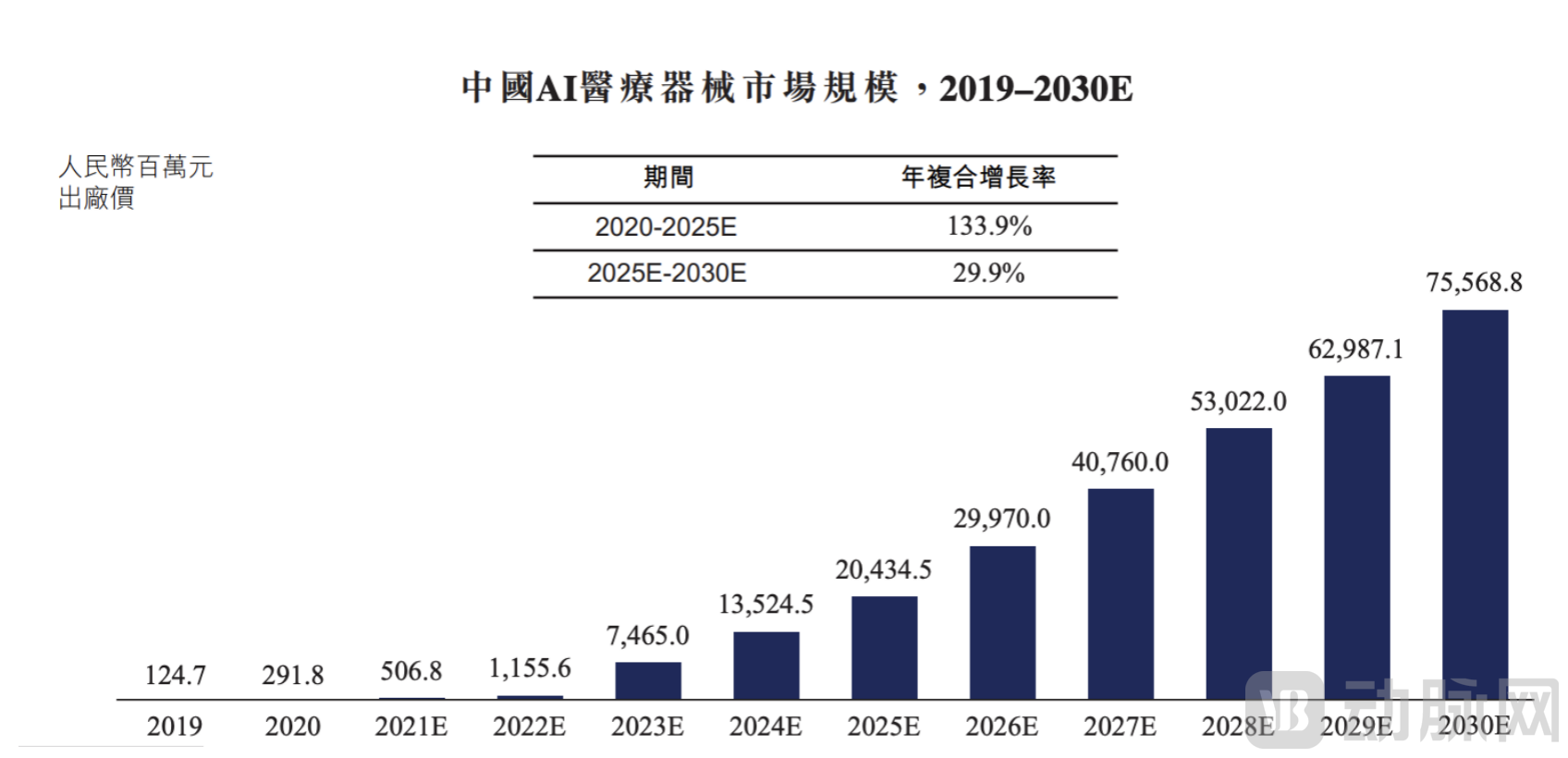

Driven by genuine demand, China’s AI medical device market has experienced rapid growth, with its market size surging from RMB 125 million in 2019 to RMB 291 million in 2020. The compound annual growth rate (CAGR) from 2020 to 2025 is projected to be 133.9%, reaching a market size of RMB 20.435 billion by 2025.

In the face of such a market, Infervision can further expand its addressable market size by accelerating physicians’ recognition of the value of artificial intelligence and increasing AI penetration. For markets where awareness mechanisms are already established, Infervision seeks to leverage its first-mover advantage in regulatory approvals to rapidly capture global market share.

The prospectus shows that Infervision’s number of distributors increased from 12 in 2019 to 47 in 2020, with an additional 15 added in the first three months of 2021, bringing the total to 62. As market penetration increases, this figure is expected to expand further.

Although Infervision has achieved sufficient maturity in its products and commercialization, this does not imply that it holds a strong competitive advantage. In fact, medical AI addresses a global market, and most existing AI companies have only taken the first step.

Moreover, developing AI products is a long-term investment process that requires rigorous oversight at every stage, from design and training to clinical validation and regulatory approval. Meanwhile, the independence of various medical scenarios means that success achieved in Scenario A cannot be effectively replicated in Scenario B; once a company suffers setbacks in clinical applications, the resulting losses are often irreparable.

Fortunately, recent trends indicate that the Center for Medical Device Evaluation is continuously improving the regulatory review and approval framework for medical AI, striving to assist AI companies in optimizing existing approval processes, which will to some extent mitigate risks for artificial intelligence enterprises.

Infervision’s IPO filing also sends a positive signal to the primary market, affirming the viability of commercializing medical artificial intelligence. With subsequent capital inflows, the R&D risks faced by AI companies may be further reduced.