Who Will Lead China's Neurointervention Market? A Prospectus Analysis of Emerging Domestic Players

Amidst the sweeping transformation of China’s medical device industry, I have personally witnessed its rapid development in recent years. Against this backdrop, issues such as volume-based procurement, intensifying competition, foreign companies’ continued dominance of the domestic market share, and surging capital interest have emerged one after another over time.

The current neurointerventional landscape resembles the primordial chaos of creation—disordered and bewildering, with a mix of genuine innovators and opportunists. It is as tumultuous as “jagged cliffs piercing the sky, stormy waves crashing against the shore, churning up a thousand piles of snow,” and as fiercely competitive as “thousands of troops vying to cross a single-log bridge.” Yet, after the dust settles, the industry will inevitably return to a sustainable trajectory, ultimately prompting countless participants to reflect that “the great river flows eastward, washing away all the heroic figures of ages past.” Consequently, how to stand out has become a critical question requiring deep consideration from both startups and investment institutions.

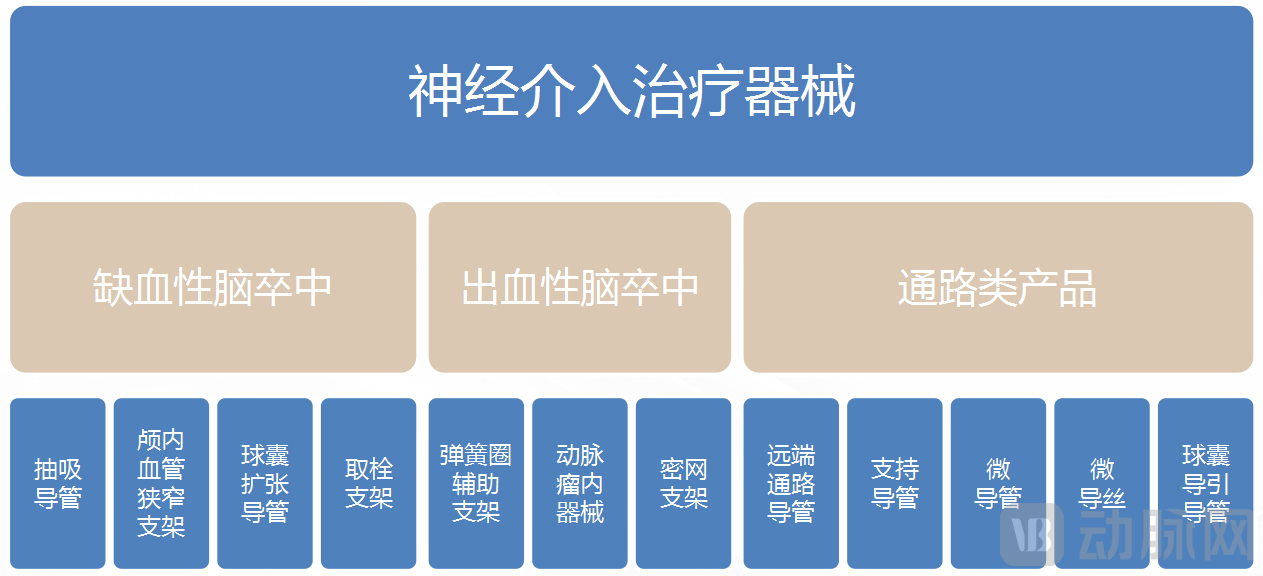

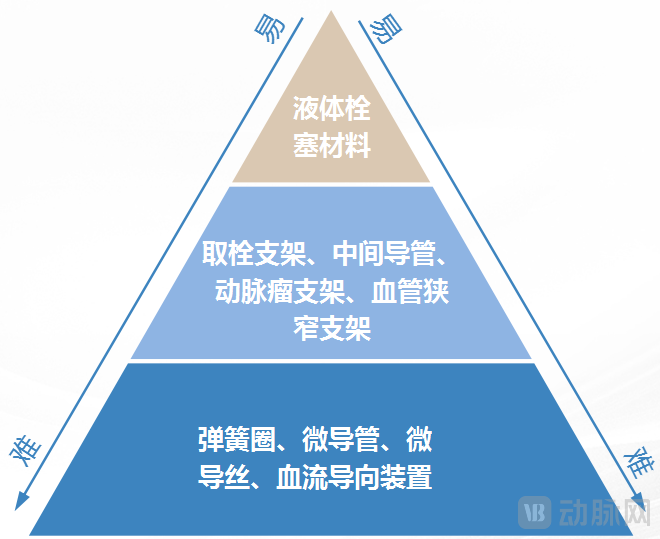

Neurointerventional devices are categorized into three major subfields: hemorrhagic, ischemic, and access. Hemorrhagic and ischemic devices are primarily therapeutic—such as stents, aspiration catheters, and coils—and currently all require clinical trials in China. According to the Catalogue of Medical Devices Exempt from Clinical Trials, access devices currently do not require clinical trials in China.

Currently, the population of stroke patients in China is steadily increasing, with high risk factors for mortality. In 2019, there were 14.8 million stroke patients in China, including 11.9 million with ischemic stroke. The incidence rate was 2.3 million cases, and it is projected to rise to 2.7 million cases by 2030. Additionally, statistics show that at least one out of every five deaths in China is due to stroke, accounting for approximately one-third of global cerebrovascular disease deaths, ranking third among causes of death.

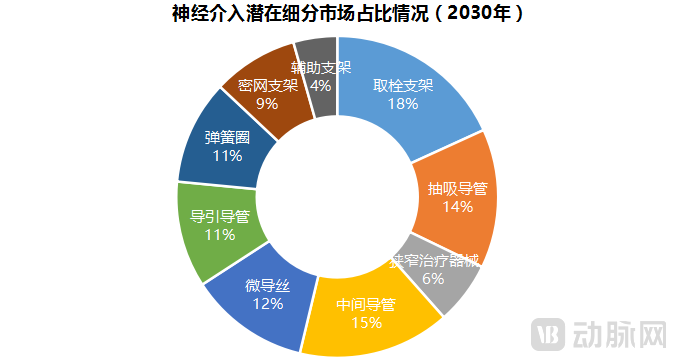

In terms of the market size of neurointervention in China, it increased from RMB 2.9 billion in 2015 to RMB 6.0 billion in 2019, with a compound annual growth rate (CAGR) of 20%. It is expected to reach RMB 48.9 billion by 2030, representing a CAGR of 21% from 2019 to 2030. From the perspective of sub-sectors, CICC expects that the market size of high-value consumables for neurointervention in China will reach tens of billions of yuan by 2030. However, in terms of the number of neurointerventional procedures, the penetration rate in China was extremely low in 2019, at only 2.3%, and is projected to reach 35.8% by 2030.China's Neurointerventional Market Holds Vast Potential. Furthermore, from the perspective of the neurointerventional sub-sector market, it possesses characteristics not found in other tracks—no single sub-segment dominates, nor does any individual product account for the vast majority, resulting in a relatively balanced distribution of market size. Consequently, there is no so-called single core product in the neurointerventional track.

Source: CICC Research Department

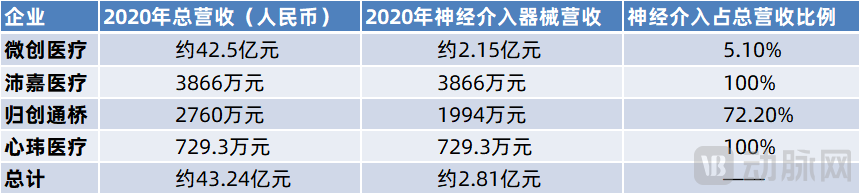

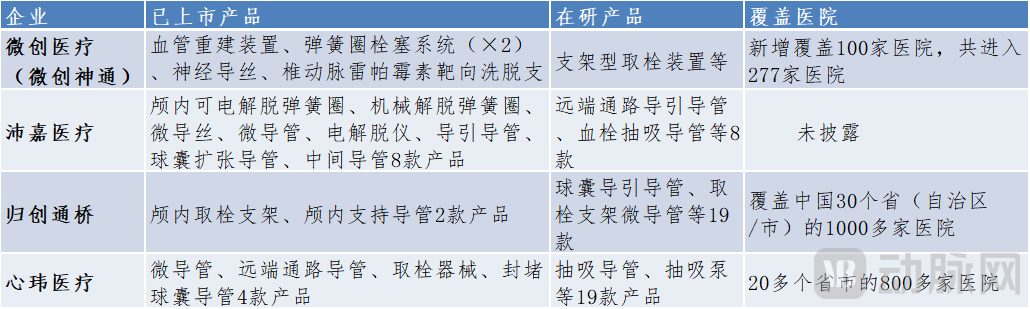

In terms of market participants, the number of competitors in China’s neurointerventional sector is steadily increasing, and competition is becoming increasingly intense. However, the reality is that in 2020, the combined market share of leading domestic neurointerventional companies—defined as “leading” solely from a capital market perspective, namely MicroPort Scientific, Peijia Medical, JetMed, and HeartCare Medical—was only 3.8% (according to HeartCare Medical’s prospectus, the estimated size of China’s neurointerventional market in 2020 was RMB 7.3 billion). The total market share of domestically produced products remained below 10%.For example, mechanical thrombectomy comprises two procedural approaches: stent retriever thrombectomy and aspiration thrombectomy. According to Hemu Biology’s prospectus, there are currently 14 approved stent retrievers in China, four of which are manufactured by domestic companies. In addition, three domestically developed stent retrievers are undergoing clinical trials. Competition in the stent retriever segment is fierce, dominated by foreign brands, with significant product homogenization and limited ability to address unmet clinical needs. There are four approved aspiration catheters, one of which is produced by a domestic company (approved in May 2021). Furthermore, four domestic enterprises have aspiration catheters in clinical trials, and one is under regulatory review. Currently, the domestic aspiration catheter market is essentially monopolized by Penumbra. According to relevant statistics, although numerous domestic neurointerventional companies are developing aspiration catheters, it is understood that domestically produced aspiration catheter systems still rely primarily on license-in arrangements. This was also the case for the first domestically launched aspiration catheter system, with truly self-developed products remaining scarce.

In addition, access-related products (consumables) used more frequently in neurointerventional procedures—microguidewires and microcatheters—are characterized by extremely high technical barriers, with foreign companies accounting for over 97% of the market share.Although a few domestic companies have held regulatory approvals for their related products for about a decade, their products are rarely seen in the Chinese market, and their brand influence remains extremely low.. In China, the neurointerventional market remains firmly dominated by imported brands, and domestic companies still face a long and arduous journey.

An analysis comparing the technical complexity of neurointerventional devices, combined with insights from physician interviews, reveals that products not requiring clinical trials are not necessarily less technically challenging than those that do. On the contrary, neurointerventional access devices—such as microcatheters and guidewires—pose significantly higher technical hurdles than therapeutic devices requiring clinical evaluation (e.g., thrombectomy stents, flow diverters, and coils). However, R&D investment in therapeutic devices is not substantially higher than that in access devices. “Neurointerventional companies capable of manufacturing high-quality microcatheters and microwires demonstrate considerable expertise; it follows naturally that their other product lines will also be of high quality. We are very willing to trial and procure their products,” stated a chief physician.

However, after the collision between numerous startups and capital, the vast majority have entered the neurointerventional market through stents, coils, or aspiration catheters. This may be because clinical products are more high-end and attractive; however, from a financial perspective, their return on investment is highly unfavorable. But this may also have led to many capitals hesitating to invest in the field of neurointervention, as they have yet to see a company that truly starts from the basics, is willing to begin with access-type products, strives to overcome the core technologies of neurointervention, and requires significantly less initial investment compared to clinical products.

From another perspective, the domestic substitution of medical devices is advancing vigorously in China, with a host of neurointerventional startups launching their businesses under the logic of import substitution. However, while the ideals and direction are promising, the reality is harsh. Many Chinese neurointerventional device companies are merely using domestic substitution as a pretext, having only shifted from “OEM 1.0” to “OEM 2.0.” The most typical example is catheters: semi-finished products are directly imported from abroad, then assembled, private-labeled, and certified domestically. The development strategy of these neurointerventional enterprises continues to prioritize rapid regulatory approval and quick market launch, resulting in a significant lack of foundational capabilities. This model largely restricts the rapid iteration of enterprise products, preventing them from embarking on a path of high-quality development. “Neurointerventional companies have collectively failed in the past because they prioritized launching more products and achieving short-term financial returns over breakthroughs in product quality.” The neglect of underlying technologies and product quality—a key factor severely constraining the rapid rise of China’s neurointerventional enterprises—is becoming increasingly evident.

As one investor noted, “Medical devices follow an iterative paradigm; it is rare for a single device to emerge as truly disruptive and completely replace its predecessors. Therefore, for innovative companies in the medical device sector, displacing established industry giants is significantly more challenging than it is for novel drug developers. Currently, surpassing market leaders such as Medtronic or Johnson & Johnson remains a formidable task across many high-value consumable segments, including neurology, cardiovascular disease, and orthopedics.” Consequently, we believe that, from a cost-efficiency perspective, entering the neurointerventional market with access-oriented products may represent the optimal strategy for startups. Ultimately, possessing foundational technological capabilities is the key to ensuring sustainable, long-term corporate growth.

Secondly, we anticipate that volume-based procurement (VBP) will eventually be implemented across the entire medical device sector in China. Once the neurointerventional field reaches a state of sufficient competition, it will inevitably become subject to VBP. Given the broader macroeconomic context—including China’s economic structural transformation and upgrading, the intensifying Sino-U.S. trade war, and the growing trend of Chinese enterprises expanding overseas—we believe that relevant companies should adopt three key strategies. First, accelerate product iteration cycles to stay ahead of centralized procurement initiatives. Second, increase investment in foundational innovation by venturing into uncharted territories and prioritizing the R&D of innovative medical devices. Third, strengthen capabilities for global expansion, accelerate entry into international markets, and proactively engage with a broader base of end users. By effectively implementing these measures, companies can mitigate the various adverse impacts associated with centralized procurement.

Finally, competition in China’s neurointerventional product market is only just beginning, with all players starting from the same baseline and product homogenization being quite pronounced. In this environment, we believe that only companies truly committed to focusing on long-term development will have the opportunity for ultimate success.

So, what characteristics should neurointerventional companies in the Chinese market possess? In summary, they should have a more internationalized team, a global strategic vision, robust international R&D capabilities, and an extensive global sales and marketing network. Crucially, they must firmly master core underlying technologies, diligently strengthen foundational infrastructure, and solidify the base for corporate development. Otherwise, they will be left to merely lament, “Life is but a dream; let me pour a libation to the river moon.”

Author: Kaicheng Capital

WinX Capital is a leading investment bank in China’s healthcare sector. Five members of its founding team hold Ph.D. degrees in Global Finance from the PBC School of Finance at Tsinghua University, while its frontline professionals boast an average of over 10 years of experience in management, investment, and M&A, with cumulative transaction values exceeding RMB 30 billion. Headquartered in Beijing and Shanghai, WinX Capital serves more than 3,000 active institutional investors and industrial conglomerates. In 2020, it was ranked among the “Top 5 Most Promising Emerging Investment Banks in China” by 36Kr’s WISE2020 awards, and named one of the “Top 4 Best Financial Advisory Firms in Healthcare” for 2020 by Qiming Technology & Xinsheng Chuangfu.