Neurointerventional Sector Booms in Capital Markets Amid Three Major Challenges

Zylox-Tonbridge

Innovative R&D, Production, and Sales of Medical Devices in the Vascular Intervention Field

2020Since [Year], the concept of neurointervention has surged in popularity in the capital market。

Leading neurointerventional companies Peijia Medical, Zylox-Tonbridge, and HeartCare Medical went public in May 2020, July 2021, and August 2021, respectively. Smooth exit channels and a visibly large market size have made primary market financing and investment in the neurointerventional sector extremely active.

According to incomplete statistics from VCBeat, as of now, at least 25 innovative companies and 60 investment firms have invested in the neurointerventional field in China. Since 2020, there have been more than 17 financing events in the neurointerventional sector, with a total cumulative funding amount exceeding RMB 1.5 billion.

As can be seen, the influx of numerous domestic companies into the neurointerventional sector will lead to intense market competition. Companies with first-mover advantages, such as Zylox-Tonbridge, are currently at the forefront. The future market landscape will depend on how each company responds to market changes. Historical trends in the coronary intervention industry suggest that companies that reach the IPO stage earlier possess greater competitive potential, while many others will gradually disappear amid market competition.

On the other hand, the entry of more than 25 companies into the field will lead to homogenization of neurointerventional products, making it highly likely that they will be included in centralized volume-based procurement (VBP) in the future. In response to VBP, the countermeasures adopted by different companies will have varying impacts.

From the current market landscape, although many domestic companies have entered the field, the neurointerventional market is still mainly dominated by multinational giants such as Medtronic. How to seize market share from these multinational giants and increase the localization rate has become a crucial issue that domestic neurointerventional companies must consider.

From a marketing perspective, diseases such as stroke have a rapid onset and high mortality rate, with strict therapeutic time windows. Consequently, the majority of stroke patients, constrained by these time limits and geographical distance, are better suited for treatment at primary care hospitals. Therefore, the rapid promotion of neurointerventional procedures in primary care settings significantly impacts the penetration rate of these procedures, the overall market size, as well as corporate revenue and market share.

Overall, domestic neurointerventional companies are facing three major challenges: market competition, risks associated with centralized procurement, and the popularization of surgical procedures. How will leading domestic neurointerventional enterprises respond to these common challenges?

Neurointervention is primarily associated with stroke. According to the prospectus of Zylox-Tonbridge, the number of stroke patients in China has reached 13 million, with approximately 2 million new cases annually. Driven by this substantial patient demand, the neurointervention market is experiencing continuous growth. In 2019, the market size amounted to RMB 4.9 billion and is projected to reach RMB 37.1 billion by 2030, representing a compound annual growth rate (CAGR) of 20.2% from 2019 to 2030.

Clinically, stroke is classified into ischemic and hemorrhagic types. Ischemic stroke accounts for 90% of all stroke cases. Data released by the National Center for Cardiovascular Diseases shows that the number of patients with ischemic stroke in China increased from 2.8 million in 2015 to 3.4 million in 2019, and is projected to reach 5.8 million by 2030.

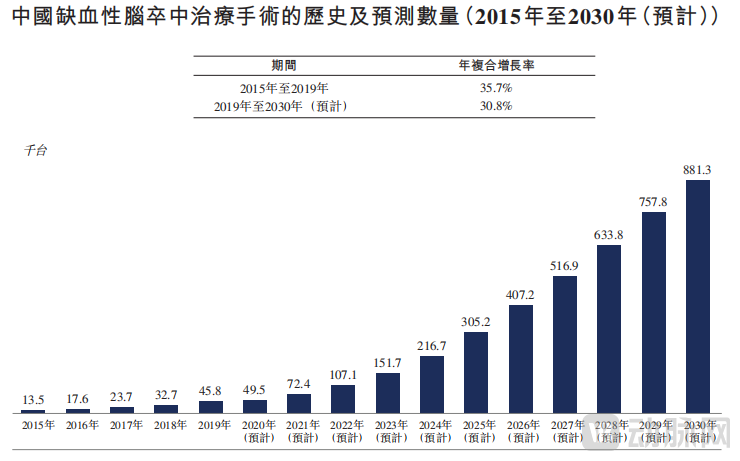

Data shows that the number of surgical procedures for ischemic stroke in China increased from 13,500 in 2015 to 45,800 in 2019, and is projected to reach 881,300 by 2030. Along with the rapid growth in procedural volume, the market for related medical devices will continue to expand.

For ischemic stroke, mechanical thrombectomy is gradually becoming the mainstream therapy due to its extended time window and broader indications. Mechanical thrombectomy primarily includes stent retriever thrombectomy and aspiration thrombectomy. The core devices used in stent retriever thrombectomy are the stent retriever and balloon catheter, while those used in aspiration thrombectomy are the aspiration catheter and aspiration pump.

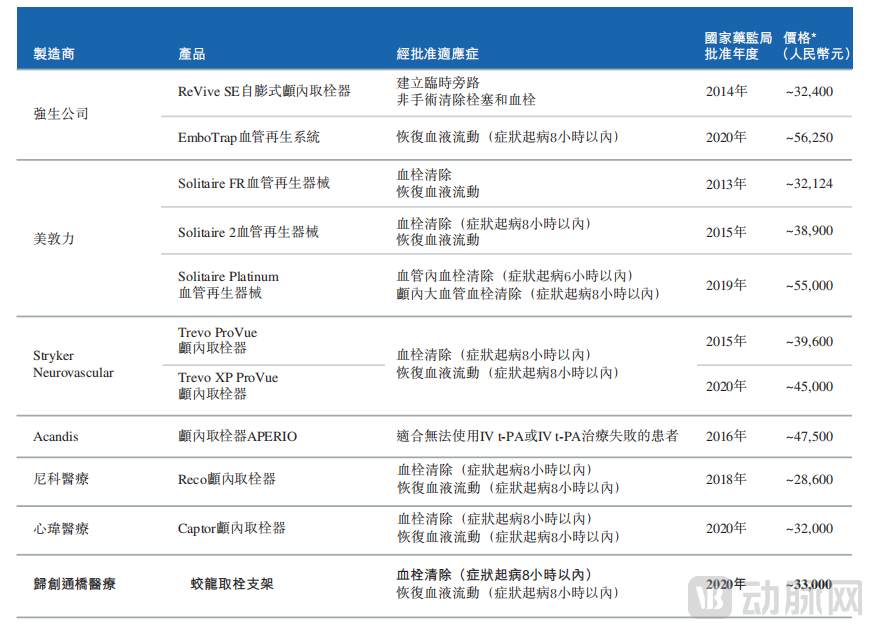

Currently, multiple core products for mechanical thrombectomy, such as stent retrievers, have been launched in the Chinese market. Taking stent retrievers as an example, 11 models have currently received approval in China, primarily manufactured by companies including Johnson & Johnson, Medtronic, Zylox-Tonbridge, NeuroQ Medical, and Xingwei Medical.

As shown in the figure above, seven companies have launched 11 thrombectomy stents, and with the advancement of other innovative enterprises, more thrombectomy stents are expected to enter the market in the future.

Similar to the ischemic stroke market, the hemorrhagic stroke market is also characterized by significant potential and intense competition.

The primary cause of hemorrhagic stroke is intracranial aneurysm. Statistics show that the number of patients with unruptured intracranial aneurysms in China was 51.1 million in 2019, and it is expected to increase to 57.9 million by 2030. In terms of harm, the mortality rate of intracranial aneurysms is as high as 50%, and the possibility of causing neurological diseases is 30%-50%.

Data shows that the number of endovascular procedures for intracranial aneurysms in China increased from 30,600 in 2015 to 60,000 in 2019, and is projected to reach 443,700 by 2030.

On the other hand, neurointerventional products for the treatment of intracranial aneurysms mainly include coils and flow diverters. Taking coils for intracranial aneurysm embolization as an example, 21 products have been launched in China, primarily manufactured by Medtronic, Boston Scientific, Johnson & Johnson, Peijia Medical, Weixin Medical, and MicroPort. Meanwhile, six additional coils for intracranial aneurysm embolization are in clinical trials or registration stages, produced by companies such as Zylox-Tonbridge, Vobi Medical, and Johnson & Johnson.

As can be seen, although the ischemic stroke market offers substantial growth potential, it has already entered a phase of intense competition, requiring companies to carefully strategize on how to gain a competitive edge.

At present, the domestic neurointerventional market is mainly dominated by multinational corporations such as Medtronic and Stryker, with Chinese manufacturers holding a relatively small share.

However, with technological innovations and product approvals by domestic companies, China’s neurointerventional market is poised for significant transformation. Compared with imported products, domestically produced neurointerventional devices inherently enjoy home-field advantages.

From a policy perspective, the state is promoting the substitution of imports with domestically produced goods and encouraging hospitals to procure domestic products. In terms of pricing, domestically produced neurointerventional products are generally priced 15%–40% lower than their imported counterparts, offering a significant price advantage. Regarding product quality, domestic enterprises have leveraged technological innovation to achieve substantial improvements in product performance; products from leading domestic companies are now comparable to imported ones, and even surpass them in certain metrics.

Taking Zylox-Tonbridge’s flow diverter stent as an example, this product is indicated for the treatment of intracranial aneurysms. Clinical trial results from 2021 demonstrated that the device is suitable for treating various types of intracranial aneurysms, including small unruptured aneurysms and giant unruptured intracranial aneurysms. According to Zylox-Tonbridge, its flow diverter stent features full-body radiopacity, a closed distal end, a flared (bell-mouth) design, moderate radial force, and strong wall apposition. Furthermore, the distal segment of the stent employs a closed-cell configuration using braided ring technology, which helps reduce vascular irritation and injury following deployment.

A professor at Changhai Hospital evaluated the product following the first clinical implantation of Zylox-Tonbridge’s flow diverter stent, stating: “The device demonstrated excellent performance. The delivery process was very smooth. Post-deployment apposition was satisfactory. Radiopacity was distinct. Contrast stasis within the aneurysm was observed, and the parent artery remained patent.”

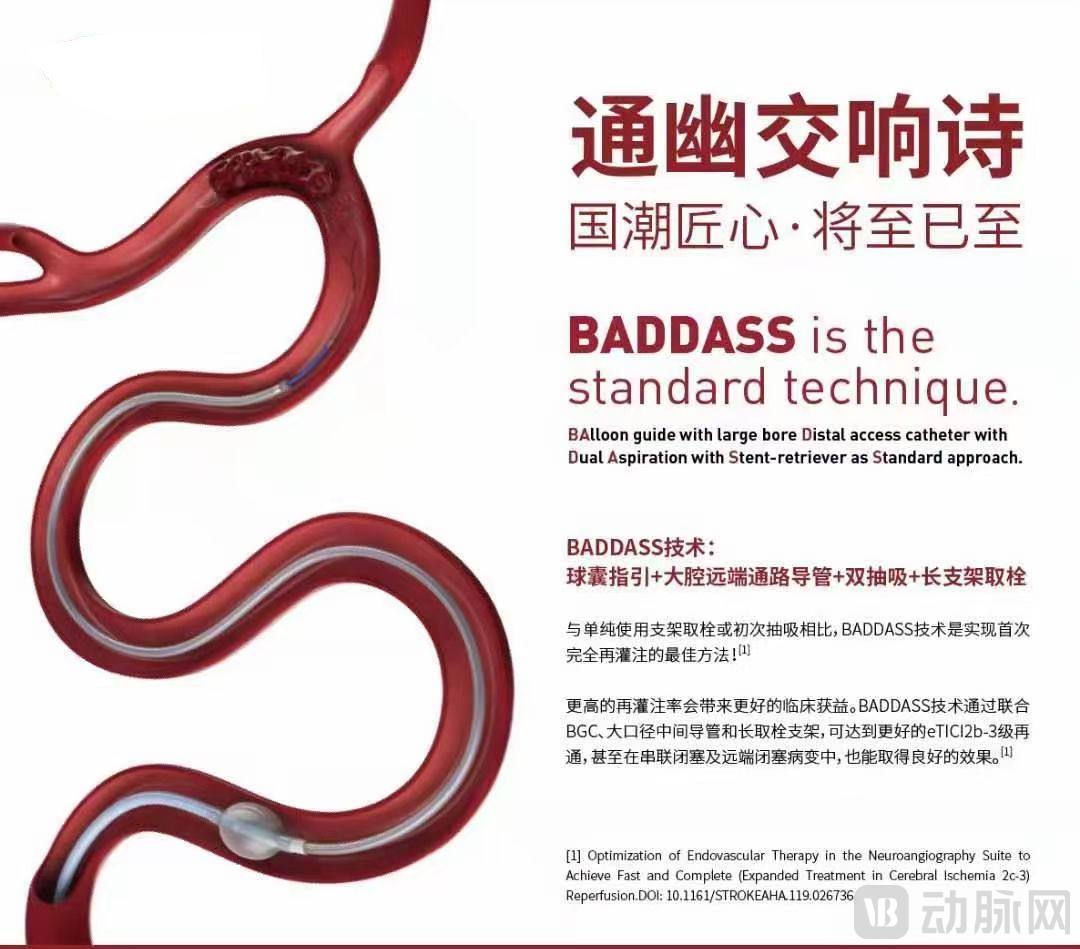

In addition, Zylox-Tonbridge pioneered the promotion of the BADDASS technique in China, a standardized neurointerventional surgical protocol for ischemic stroke that encompasses nearly all current thrombectomy devices, techniques, and concepts. Specifically, the BADDASS technique provides standardized operative procedures for patients with ischemic stroke using complementary neurointerventional devices such as stent retrievers, intracranial support catheters, and balloon guide catheters.

Current clinical studies show that,Currently, allofThrombectomy Techniques: BADDASSTechnologythe highest primary patency rate wasIschemic StrokeThrombectomyTreatmentOptimal Combination。

To facilitate the widespread adoption of the BADDASS technique, Zylox-Tonbridge has launched the “BADDASS Technique Trio,” comprising the Jiaolong® Stent Retriever, YinShe® Intracranial Support Catheter, and Dayu™ Balloon Guide Catheter, leveraging its extensive product portfolio and high product compatibility.

Overall, leveraging advantages in policy support, pricing, and product performance, domestic neurointerventional companies such as Zylox-Tonbridge will accelerate the substitution of imported products with domestically produced alternatives in the neurointerventional market. In this process, leading domestic neurointerventional enterprises will gain a greater competitive edge based on their product strengths and rapid execution.

In addition to the immense pressure from market competition, domestic neurointerventional companies also face risks associated with centralized procurement and challenges in promoting their products at the primary care level.

However, it is worth noting that volume-based procurement (VBP) for high-value medical consumables is becoming more rationalized. Price is no longer the sole consideration; instead, multiple indicators such as product performance and market share are evaluated simultaneously. Furthermore, supported by VBP, certain high-value consumables are accelerating import substitution with domestically produced alternatives, thereby boosting corporate revenues.

For instance, due to high entry barriers and fewer competitors, the overall price reduction for intraocular lenses (IOLs) has been relatively moderate. Amid this gradual price decline, the substitution of imported products with domestically produced ones has accelerated, leading to increased product penetration and a rapid rise in the market share of Chinese-made IOLs. Consequently, domestic companies have achieved substantial revenue growth, far exceeding their pre-volume-based procurement levels.

In 2019, the average price reduction for intraocular lenses (IOLs) in Anhui Province’s volume-based procurement program was 20.5%. Aibor Medical, the winning bidder, doubled its number of accounts in public hospitals in Anhui Province and increased sales volume of the awarded products by 1.65 times. Although sales declined in 2020 due to the impact of the pandemic, Aibor Medical’s average monthly sales revenue remained higher than the pre-procurement level.

Therefore, given the prevailing trend toward centralized procurement, it is highly likely that neurointerventional products in China will be included in volume-based procurement (VBP) programs once the market matures. Inclusion in VBP is expected to safeguard a portion of corporate profits while increasing the market share of domestic manufacturers and enhancing the penetration rate of neurointerventional procedures, thereby expanding the overall market size and benefiting the winning bidders.

Regarding the challenges of promoting these technologies at the primary care level, various technical approaches are currently available to facilitate their adoption. For instance, surgical robots leveraging robotic technology and surgical navigation systems powered by artificial intelligence can significantly reduce procedural complexity, assisting physicians in performing neurointerventional procedures more rapidly and effectively.However, the high procurement costs of surgical robots and surgical navigation systems are prohibitive for primary-care hospitals, and the market still requires education and physician training.

Beyond robotics and navigation systems, the widespread adoption of neurointerventional procedures relies on manufacturers’ support in professional education, enabling primary-care physicians to master thrombectomy techniques more rapidly and with higher quality.In this regard, Zylox-Tonbridge pioneered the BADDASS technique in China, which can help improve the first-pass recanalization rate of thrombectomy, enhance patient prognosis, and achieve better outcomes for mechanical thrombectomy. Meanwhile,Zylox-Tonbridge LaunchesJiaolong® Thrombectomy Stent, Yinshe® Intracranial Support Catheter, Dayu™ Balloon Guide Catheter“BADDASS“Three-Piece Technology Suite,” and with Zylox-Tonbridge’s online and offline professional education and promotional efforts, gradually promoting the popularization and application of these technologies, extending their reach to primary-care hospitals.

In summary, faced with the three major challenges of competition, centralized procurement, and grassroots promotion, neurointerventional companies are actively seeking diverse solutions. Leveraging its first-mover advantage, product strengths, and rapid execution capabilities, Zylox-Tonbridge, a leading domestic neurointerventional enterprise, is rapidly expanding its market presence and increasing the localization rate of the neurointerventional market in China.