Can a New Giant Emerge in China's Clear Aligner Market Dominated by Invisalign and Angelalign?

Invisible orthodontics has become one of the hottest trends in the dental industry.

In mid-year, Angelalign (06699.HK), a provider of clear aligner orthodontic solutions, listed on the Hong Kong Stock Exchange, triggering frenzied buying from investors. Its shares surged 132% on the first day of trading, bringing its market capitalization to nearly HK$70 billion. Since filing its prospectus in January, Angelalign has attracted widespread attention from the capital markets, with oversubscription exceeding 2,000 times during the IPO phase.

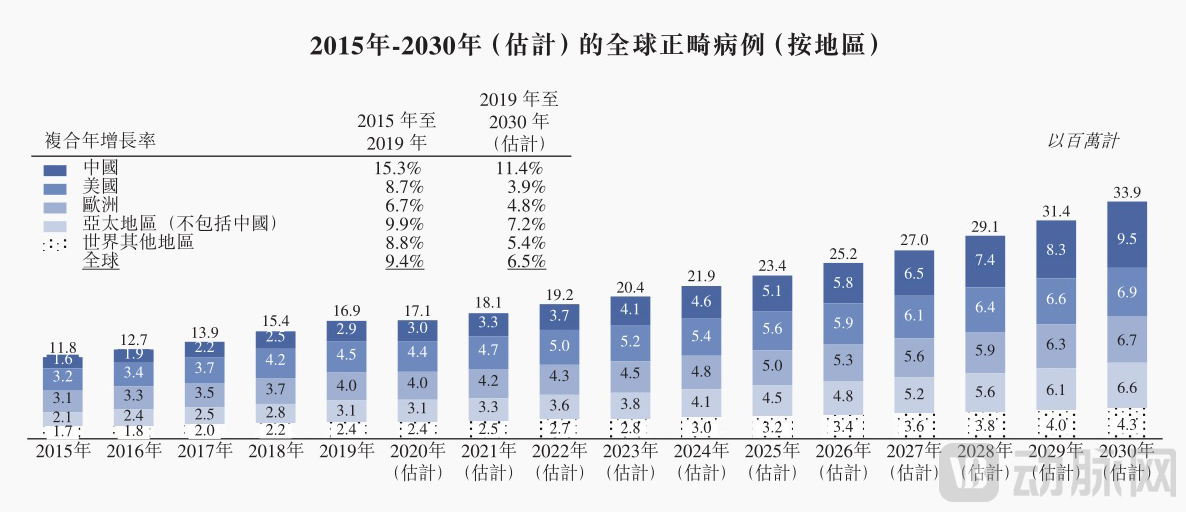

Behind investors’ frenzied bets on Angelalign lies their bullish outlook on the entire clear aligner orthodontics sector.According to statistics from Frost & Sullivan, the number of orthodontic cases addressed with clear aligners in China increased from 47,000 in 2015 to 335,500 in 2020, representing a compound annual growth rate (CAGR) of 47.7%. The figure is projected to reach 3.8 million by 2030, indicating substantial growth potential for the market.

(Source: Frost & Sullivan Report)

More importantly, the invisible orthodontics sector has been proven by the market to be capable of producing major high-performing stocks.: Over the past decade, the stock price of Invisalign, the industry leader, has surged more than 30-fold. Therefore, when a domestic clear aligner company with outstanding business performance emerges in the Chinese market, investors are undoubtedly enthusiastic, as scarcity is a significant factor influencing investment decisions.

A rapidly expanding market, coupled with the potential to produce major stock performers,The invisible orthodontics sector is attracting a growing influx of companies.Research by Zhongtai Securities shows that as of January 2021, there were 125 valid registration certificates for clear aligner orthodontic products in China, held by 104 companies. This means that more than 100 companies have obtained registration certificates for clear aligner orthodontic products.

Additionally,In the primary market, invisible orthodontics companies have also frequently secured financing, with individual funding rounds typically reaching the hundred-million-yuan level.

On the other hand,The vast majority of companies have yet to gain a firm foothold in the market.For example, among enterprises that have obtained product registration certificates, only 31 companies are currently providing clear aligner services. Most of these manufacturers offer only a single aligner product, and no more than five possess comprehensive clear aligner products and technologies.

Why Has Invisible Orthodontics Become a Major Market Opportunity? What Are the Industry’s Core Barriers? Amidst the “Duopoly” of Invisalign and Angelalign, Do Other Companies Have a Chance to Emerge? What Challenges Remain in This Sector? How Are Companies Pursuing Differentiated Strategies? To address these questions, VCBeat has interviewed seasoned industry institutions and enterprises to shed light on the answers.

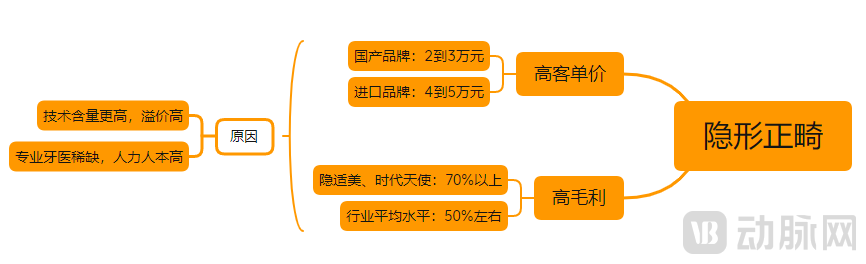

When it comes to clear aligner orthodontics, many people immediately think of “exorbitant profits.”

This is because information disclosed by the two industry leaders, Invisalign and Angelalign, indicates thatThe gross profit margins of both invisible orthodontic companies reached as high as 70%.The industry’s average gross profit margin also exceeds 50%. The exceptionally high gross profit margin has earned invisible orthodontics the nickname “the Moutai of dentistry.”

On the other hand,High unit prices have also become the industry standard for invisible orthodontics.A search of current market prices for mainstream orthodontic braces (aligners) reveals that traditional metal wire braces cost between RMB 10,000 and 20,000, while clear aligners are priced higher: domestic brands range from RMB 20,000 to 30,000, and imported brands cost RMB 40,000 to 50,000. As a result, clear aligner therapy has earned the nickname “the Hermès of dentistry.”

“Exorbitant Profits”: Behind the scenes, one factor stems from the differentiation of clear aligners in terms of technology and product experience.Compared with traditional braces, clear aligners offer advantages such as aesthetics and comfort, while significantly reducing patient pain. Furthermore, thanks to the rise of digital orthodontic technology, patients can visualize the treatment outcome at each step prior to therapy. This capability is underpinned by barriers formed through the integration of multidisciplinary technologies, thereby commanding a higher premium for clear aligner orthodontics.

(Differences between invisible orthodontics and traditional orthodontics; image source: Angelalign’s prospectus)

(Differences between invisible orthodontics and traditional orthodontics; image source: Angelalign’s prospectus)

Second, the scarcity of dentists has led to consultation fees accounting for the majority of the total treatment cost.“The procurement cost for leading-brand products ranges from RMB 8,000 to RMB 20,000, but the final price paid by patients is doubled. This markup primarily covers clinic operating expenses, with dentist compensation being the largest cost component,” the founder of a dental clinic in Chongqing told VCBeat. The underlying reason is that orthodontic treatment heavily relies on the individual skills and experience of dentists, while the industry faces a significant shortage of talent overall.

Data from Frost & Sullivan corroborates that in 2020, China had approximately 277,500 general dentists and 6,100 orthodontists, equivalent to 19.5 general dentists and 0.4 orthodontists per 100,000 people. In comparison, the United States had approximately 158,000 general dentists and 10,800 orthodontists, equivalent to 47.8 general dentists and 3.3 orthodontists per 100,000 people, indicating a significant shortage of dentists in China.

In summary, it can be seen thatInvisible orthodontics undoubtedly possesses the characteristics of a lucrative business: high unit price, high gross margin, and a relative scarcity of supply (dentists) in the short to medium term, which are key factors contributing to its emergence as a market hotspot.However, beyond this, capital’s strong enthusiasm also hinges on whether the industry can sustain rapid expansion, which is closely tied to users’ long-term demand.

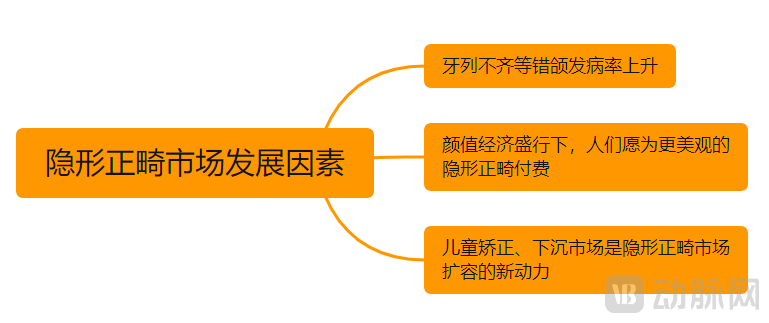

Thus, let us shift our focus back to the demand side. First, from the perspective of disease prevalence, due to factors such as the increasing refinement of modern diets,The incidence of malocclusion, such as dental misalignment, has risen significantly, and demand for orthodontic treatment remains strong.

Furthermore,The rise of the "beauty economy" has made people willing to pay for solutions to issues such as teeth that are not white or straight enough.The combination of the two makes clear aligner orthodontics a high-quality choice for users.

“Unless patients are particularly price-sensitive, they will generally opt for clear aligner orthodontics, as it is more aesthetically pleasing and comfortable,” stated the founder of the aforementioned dental clinic. The rapid growth in the number of clear aligner orthodontic cases supports this assertion. Research data from Zhongtai Securities shows that from 2015 to 2019, the number of such cases increased from 47,800 to 303,900, representing a compound annual growth rate (CAGR) of 58.8%.

Beyond overall demand, niche segments within the clear aligner orthodontics market are also expanding to offer greater possibilities.

For instance, the market potential for early orthodontic intervention in children is expanding. Data from Zhongtai Securities indicates that the prevalence of malocclusion among children in the mixed dentition stage has reached 71.2%. During this phase, the high plasticity of periodontal tissues and jawbones allows for more effective treatment outcomes with less effort. Given the current low market penetration rate, the long-term market size is projected to reach RMB 50–60 billion.

Another example is the untapped potential in lower-tier cities (third- and fourth-tier). According to data from Zhongtai Securities, first- and second-tier cities account for approximately 70% of the clear aligner market. From 2015 to 2019, the market growth rate in these cities was 53%, slower than the 66% observed in third-tier cities and below. As both dental care providers and clear aligner manufacturers expand their presence into lower-tier markets, the consumer potential in third-tier cities and below urgently needs to be unlocked.

Driven by sustained market growth potential and a favorable cost structure, the clear aligner industry has become a highly sought-after investment sector, giving rise to leading companies such as Invisalign, Angelalign, Smartee, and Zhenli, while attracting an increasing number of new entrants.

In the face of a trillion-dollar market for clear aligners, what exactly constitutes the core competitive barrier in this industry? Or, to put it another way, amid intense competition, which capabilities—such as technology, product, or distribution channels—are most critical for new entrants?

Before answering this question, we must first address what characterizes the clear aligner orthodontics industry.

First is technology-driven.As a multidisciplinary and multi-field technological integration, clear aligner orthodontics has been continuously optimized and developed through iterative technological advancements since its inception.

“Invisible orthodontics relies on technologies such as materials, software systems, and algorithms, with the core component being the design of treatment plans. This involves two key capabilities: one is modeling capability, and the other is digital development capability,” said the R&D Director of a leading invisible orthodontics company to VCBeat.

Taking Invisalign as an example, it features a proprietary force delivery system comprising SmartTrack material, SmartForce optimized attachments, and SmartStage precision algorithms. Among these, the SmartTrack aligner material is a core patent; it delivers gentle, continuous orthodontic forces and is characterized by high elasticity, stress relaxation, superior fit, and high durability. In terms of user experience, advanced technology ensures enhanced aesthetics and comfort.

It is reported that Align Technology spent eight years, invested millions of dollars, tested more than 260 materials, and leveraged extensive expertise in biomechanics and materials science to successfully develop the SmartTrack aligner material.

Building on the Invisalign treatment technology, Align Technology has also introduced the iTero intraoral scanner, creating a digital platform centered on the iTero intraoral scanner and Invisalign treatment technology. This has significantly enhanced Invisalign’s modeling capabilities and digital development capacity.

The seamless integration between the iTero intraoral scanner and the Invisalign system has enabled a fully digital workflow, spanning from intraoral scanning and model creation to patient record establishment, treatment plan design, and large-scale customized production, thereby continuously optimizing and refining the entire diagnostic and treatment process. Thanks to continuous technological breakthroughs, the number of global patients served by Align Technology had exceeded 10 million as of May this year.

(The Development History of Invisalign Products)

Furthermore, the scale effect is prominent.For clear aligner companies, competition is not one-dimensional; it requires enterprises to have relatively complete R&D, sales, and middle- and back-office service teams. This results in high upfront costs, so clear aligner companies need continuously growing scale to spread out expenses, i.e., covering these costs through the accumulation of orthodontic cases.

Additionally, economies of scale are also reflected in the precision of treatment plans, as a larger case library enables more accurate “model training” in the clear aligner industry.

Taking Invisalign as an example, it took 11 years from the launch of its first product in 1998 to surpass one million cases in 2009. However, the time required to achieve each subsequent million-case milestone has continued to shorten; between 2019 and 2020, it took only about one year for the case volume to increase from 7 million to 9 million. This trend is driven by improved accuracy and enhanced user experience as the number of cases grows, which in turn generates more positive market feedback.

Finally, there is patient acquisition capability, which is also the core competitive capability in the industry today.In the orthodontics industry, the use of braces must be prescribed by licensed orthodontists, underscoring their critical role. However, orthodontic treatment typically spans a prolonged period of one to two years, and achieving proficiency generally requires managing approximately 100 cases. Consequently, the training cycle for orthodontists usually lasts five to seven years. Compared with market demand, the supply of orthodontists remains significantly scarce.

As clear aligner companies have entered the specialized phase of treatment planning, they have established strong connections with orthodontists. Given the limited availability of dental professionals, the ability to attract and retain doctors has become a critical component for clear aligner companies in expanding their market presence.

“Invisible orthodontics is highly dependent on doctor-patient scenarios.” Chende Capital told VCBeat that there are three main challenges in recruiting doctors.

First, can it provide doctors with cutting-edge technology and high-quality products? The essence of clear aligner therapy lies in its medical nature. For physicians, product selection inevitably prioritizes actual clinical efficacy, particularly the underlying technologies incorporated into the product, which can even empower some primary-care dentists in China to manage complex malocclusion cases.

Second, whether sufficient service support and logistical backing can be provided to clinicians. Clear aligner therapy is not merely a diagnosis-to-treatment process; it also encompasses early-stage patient acquisition and consultation, mid-stage cephalometric analysis and treatment planning, as well as post-treatment services. If companies can offer clinicians a comprehensive suite of treatment support services, enabling them to focus primarily on clinical care, this will serve as a competitive advantage in attracting and retaining healthcare providers.

Finally, the question remains whether doctors’ legitimate rights and interests can be safeguarded. Currently, many companies in the market emphasize forming strong partnerships with physicians to conduct technological research and development. In this process, whether enterprises take doctors’ interests into consideration is also a point worthy of attention.

Take Smartee, a portfolio company of Chende Capital, as an example. Since 2019, Smartee has collaborated with the Shen Gang Orthodontic Team at Taikang Bybo Dental, with both parties providing mutual support in the R&D of multiple projects over the past two years. For instance, the joint project “Smartee Active Mandibular Position Retainer S17,” launched in January this year, represents a significant independently developed original technology in China’s clinical field. It is reported that the development of this retainer can effectively stabilize the mandibular position and the relationship between the maxilla and the dentition.

In summary, it is evident that technology, scale, and dentist acquisition are critical factors determining whether clear aligner companies can achieve substantial growth, and they are also key to building core competitive barriers.

Currently, Invisalign and Angelalign account for 82.3% of the market share in China’s clear aligner market, forming a “duopoly.” Given this market landscape, can the industry still produce new giants?

“Amid industry competition, companies that can break through homogeneous rivalry, integrate supply chain resources, or develop products with genuine technological barriers will still be favored by the market,” said an industry investor.For new entrants, the fastest way to achieve a breakthrough is to seek differentiation.

For example, securing two rounds of financing this year, with a total amounting to hundreds of millions of yuan,Weiyun AI: Its Differentiated Path Is to Build a Closed-Loop, Full-Industry Chain Centered on Artificial Intelligence and Robotics Technologies, with technological advantages spanning multiple complex disciplines, including artificial intelligence, graphics and image algorithms, robotics, motion control, materials science, and dentistry.

At the beginning of last year, Weiyun officially launched its AI-driven clear aligner brand, “Xiangbei,” in China. Leveraging its network of nearly 20,000 clinics, the brand has already delivered tens of thousands of cases. Born from a fully automated smart factory, Xiangbei utilizes cutting-edge technologies—including millions of user data points, intraoral point cloud scanning, AI simulation, AI tooth arrangement, and AI-enabled automated production—to simulate clinical orthodontic processes and the patterns and steps of tooth movement. It calculates and generates aligner models for the entire orthodontic treatment cycle, which are then manufactured and delivered with micron-level precision through its smart factory. This robust technological foundation provides dentists and patients with a more efficient and convenient delivery experience, as well as superior treatment outcomes.

Beyond orthodontics, WeiCloud provides a comprehensive suite of digital dental industry solutions through its unmanned smart factory, which integrates its independently developed cloud-based SaaS and MaaS platforms with a matrix of robotic terminals. With over 400 SKUs covering multiple oral healthcare sectors—including dental implants, orthodontics, medical aesthetics, and prosthodontics—the company has reduced single-product production time by 90% and achieved a yield rate as high as 98%. Furthermore, through strategic deployments targeting both B-end and C-end markets, WeiCloud strives to become the comprehensive “Invisalign” of China’s oral care market.

Another example is the one established in 2018,EasySmile has chosen a differentiated path by targeting consumers directly.。

The Qingsong Xiao model focuses on selecting cases with mild-to-moderate orthodontic indications, streamlining and standardizing service processes such as user diagnosis, treatment plan design, clinical procedures by dentists, and post-treatment monitoring of appliance wear. It enables full-lifecycle data tracking throughout the correction process and builds a large repository of mild-to-moderate cases to empower comprehensive digitalization via a middle-platform system. In the future, this digital middle platform will help dentists serve patients more efficiently, addressing industry-wide challenges such as the scarcity of skilled dentists and operational difficulties for private dental practices.

Specifically, after making an online appointment, users can undergo intraoral scanning at offline partner clinics of Qingsong Xiao. Once the data is acquired, digital modeling is performed, and AI-driven algorithms match it against a vast database of Asian oral anatomy. Treatment plans are then designed based on this analysis and subject to remote review by orthodontic specialists.

Throughout the entire orthodontic treatment process, apart from the comprehensive oral examination and intraoral scanning required at the clinic, all other steps can be completed online. This enables Qingsong Xiao to provide users with a more convenient and superior clear aligner therapy experience.

This year, it received investment from the Zhonghe Oupu Medical Health Fund, under the listed company Aier Eye Hospital (300595.SZ).Dijia Medical (Meilike)’s differentiated path is to focus on technology and materials.

In terms of product features, Meilike clear aligners boast four key highlights: first, they utilize imported German medical-grade resin films to ensure safety; second, with a thickness of only 0.75mm, they offer comfort and can be quickly removed and inserted by the user; third, they provide precision, moving each tooth by 0.2mm per step; and fourth, they are custom-made based on individual dental impressions and replaced every two weeks to align with personal treatment progress.

In terms of technological advantages, Dijia Medical is China’s first company to independently develop and manufacture 3D printing photosensitive resins specifically for dental applications, as well as a domestic producer of multi-layer dental films with independent production capabilities. The company has also established an automated intelligent manufacturing base in China.

As can be seen from the above, clear aligner companies still have promising opportunities through differentiated pathways.It is worth noting that the oral care industry possesses inherent medical characteristics, requiring every product and solution to undergo a period of maturation and rigorous testing from inception to market entry. This, in turn, demands sufficient patience and perseverance from those entering the field.

In recent years, the dental industry has emerged as a high-growth sector, with clear aligner orthodontics riding this wave of expansion.

ButFor every participant, it is not enough to simply leverage the momentum to take off; one must also identify the underlying logic driving the trend, in order to achieve steady development over an extended period.A review of the development trajectories of leading enterprises reveals five evolutionary paths worthy of reference.

The first is to prioritize synergistic support across the entire industry chain.The oral care industry is characterized by a high degree of vertical integration; mutual trust and collaboration across the upstream and downstream segments, particularly through ecosystem synergy, provide a stronger impetus for the growth of clear aligner companies.

Taking Angelalign as an example, its controlling shareholder, Shuangbai Investment, is an industrial investment and operation group specializing in the dental healthcare sector. Based on Shuangbai Investment’s historical strategic deployments, it has established an investment ecosystem spanning the entire industry chain—from upstream orthodontics, implants, prosthodontics, and hardware/software equipment, to midstream clinical management software and distribution, and downstream hospitals and clinics. Its investments and partnerships encompass more than 40 companies across Asia, Europe, and North America.

According to Angelalign’s prospectus, its industrial layout based on Shuangbai Investment has helped the company gain a deep understanding of the needs of customers in different segments and the technological drivers in various segments of the industry chain, which has also become the company's most unique advantage.

For example, as a key piece of equipment in digital dentistry, intraoral scanners are an indispensable component of the clear aligner industry. Shuangbai Investment has invested in companies such as Raycome, Medit, and Phitax in this field, thereby providing Angelalign with more options and a more open collaborative network through the synergies of these strategic resources.

The second is to attract high-quality capital.Invisible orthodontics is, at its core, an R&D-driven business; therefore, capital plays a particularly crucial role in corporate development.

For example, the collaboration between Chende Capital and Zhengya. Since beginning its strategic deployment in the dental sector in 2016, Chende Capital has covered multiple segments of the industry chain. It has currently invested in and incubated several companies in the dental field, including, in addition to Zhengya, Fisen Technology, a provider of digital dental equipment and solutions; Realint Technology, an enterprise engaged in the R&D of chairside 3D printing equipment and materials; and Aidite, a company focused on the R&D of new dental materials and equipment.

“We have devoted substantial energy to providing post-investment services to our portfolio companies, positioning ourselves as integral team members who share in the entrepreneurial journey. In this capacity, we assume multiple roles, including business development, sales, marketing, human resources, and even product management,” stated Chende Capital. “We maintain close communication with our portfolio companies, fostering mutual enhancement of industry insights through collaborative dialogue and strengthening industry synergies.”

It is evident that investors inject various core resources into their portfolio companies, further assisting them in market expansion and business synergy. Meanwhile, they provide strategic guidance on market operations and directional control, ensuring that the companies’ business development stays on the right track.

The third is to continue focusing on the digitalization and technological empowerment of core processes.For example, the penetration rate of intraoral scanners in China remains relatively low. High-precision optical impressions will effectively enhance the accuracy of subsequent aligner design and manufacturing. Furthermore, the development of true-color intraoral scanning technology contributes to improving the precision of tooth and gingiva segmentation, a critical step in clear aligner orthodontic data processing.

“Automated 2D lateral cephalometric analysis has emerged, freeing clinicians from manual tracing at their desks.” Industry insiders state that the widespread future application of CBCT in orthodontics will further enhance risk mitigation in clear aligner therapy (such as assessment of root and alveolar bone volume, evaluation of temporomandibular joint health, and detection of impacted teeth), while simultaneously reducing the rate of treatment deviations and restarts. For instance, Angelalign’s newly launched Implant-Root System (IRS), unveiled at this year’s A-TECH Conference, advances clear aligner therapy from simulating crown movement to concurrently considering both crown and root displacement.

In the realm of scaled manufacturing via 3D printing, achieving full automation and implementing flexible production to address strong seasonal demand cycles are key to further enhancing the delivery quality and turnaround time of aligners. Meanwhile, given that orthodontic treatment is a clinical process spanning two to three years, monitoring treatment progress through follow-up visits throughout the entire course of alignment is crucial. This area holds significant potential for digitalization. Industry experts predict that the wider adoption of intraoral imaging devices will enable digital follow-up consultations, thereby further improving dentists’ clinical efficiency. Moreover, remote consultations could help alleviate the current imbalance in the distribution of orthodontic treatment resources in China.

Maintaining results in the later stages of orthodontic treatment is also crucial. “The United States is a major country in orthodontics, and we have observed an increasing number of relapse cases. In China, we believe that post-treatment maintenance involves not only preserving dental alignment but also comprehensively maintaining the overall health of the teeth, periodontal soft tissues, and occlusal relationships, thereby reducing secondary caries, secondary periodontal tissue recession, and mucosal injuries. This approach presents opportunities for interdisciplinary collaboration,” said industry insiders.

The fourth is to be medicine-centric and provide localized solutions tailored to users in different regional markets.For instance, to address the critical pain points in China of insufficient physician supply and non-standardized clinical competencies, we can provide standardized services on one hand to lower the technical barriers for physicians, and on the other hand help improve their diagnostic and treatment efficiency. This is particularly aimed at bolstering the capabilities of general dentists operating at a larger scale, thereby fully empowering them.

Furthermore, China has a large population, with the majority of its citizens exhibiting convex facial profiles. The prevalence of complex malocclusions is higher than that in the United States, resulting in a greater number of complex cases. Therefore, personalized arrangements must be made based on the current characteristics of the Chinese population, spanning from medical treatment planning and the research and development of aligner materials and films to production and multi-batch distribution. This places higher demands on capabilities in medicine, R&D, and advanced manufacturing. Given that clear aligner orthodontics relies heavily on digital science and data analytics, a company’s medical expertise requires not only support from foundational technology R&D but also the accumulation of extensive databases and diverse case types.

In response to this challenge, many companies have actively made strategic moves. For instance, Angelalign has established one of the largest oral medicine databases for Asian populations and assembled the largest team of medical designers in China’s dental services sector, comprising over 400 members. Currently, Angelalign holds 93 registered patents in China and has independently developed its technology and data platforms. Leveraging the breadth and maturity of these technology and data platforms, Angelalign has built unique advantages in helping dentists address complex cases that are prevalent and specific to China.

The fifth trend is the emphasis on expanding clear aligner orthodontics into specialized niches.Early orthodontic treatment for children is emerging as a rapidly growing segment within the clear aligner market. A survey conducted by the Orthodontics Professional Committee of the Chinese Stomatological Association, involving more than 20,000 Chinese children and adolescents, revealed that in 2015, the prevalence of malocclusion was 51.84% in the primary dentition group, 71.21% in the mixed dentition group, and 73.97% in the permanent dentition group, with an overall prevalence rate of 67.82% across all three groups. This indicates a substantial demand for pediatric oral health care.

This area of demand is gradually gaining attention. Taking Topchoice Medical, a dental care service provider, as an example, its financial reports show that the compound annual growth rate (CAGR) of its pediatric business revenue from 2016 to 2020 was approximately 36%, indicating a period of rapid growth. Within this segment, orthodontic services have occupied a significant position.

From the perspective of the overall market landscape, companies such as Remu, MRC, and ETA are currently active in early childhood orthodontics. They primarily provide functional appliances for the early correction of malocclusion during the mixed dentition stage in children aged 5 to 12. Meanwhile, clear aligner providers like Invisalign and Angelalign have also expanded their product lines to include appliances for children in the mixed dentition stage and are actively strengthening their market presence. For instance, Angelalign Kids is a comprehensive clear aligner treatment solution designed for children aged 6 to 12, which includes clear aligners, lip and cheek shields, and a set of myofunctional exercises.

Since children’s functional appliances typically require only 3 to 9 months of wear to achieve muscular adjustment, followed by 6 to 12 months of retainer use, the overall treatment duration is shorter than that for adults, conferring certain advantages in product promotion.

In summary,For clear aligner companies that have already entered the market or are preparing to do so, prioritizing R&D, fostering industry collaboration, and adeptly identifying emerging trends are essential to seizing opportunities in the next phase of industry evolution.