Clinical Mass Spectrometry: A $1B+ Funding Surge in Six Months, Clinical Adoption Challenges Persist, but Market Maturity Expected Within 3–5 Years

If the clinical mass spectrometry industry was previously in a dormant state, then by 2021, it had already shown strong momentum for explosive growth.

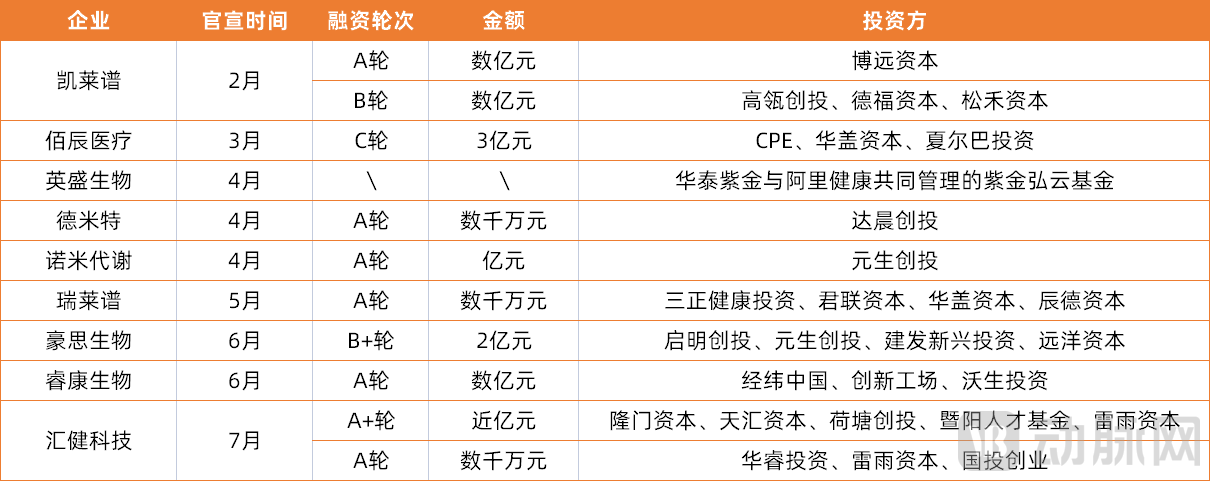

First, the signals from capital investment. According to statistics from VCBeat, from January 1 to August 31, 2021, a total of eight clinical mass spectrometry companies completed financing in the primary market. Among them, Baichen Medical secured RMB 300 million in Series C funding in March, led by CPE, marking the largest financing round in the clinical mass spectrometry industry to date.

Clinical Mass Spectrometry Companies’ Financing Activities from January to August 2021

In 2021, various companies also intensified their efforts in the field of clinical mass spectrometry, with significant moves being made continuously.

Yingsheng Biology has obtained approval for multiple reagents, becoming the company with the largest number of certifications in the clinical mass spectrometry field; Hexin Instruments was officially approved for listing on the STAR Market; Metabolon (MaiTe HuiPu) announced its formal entry into the clinical mass spectrometry sector; KingMed Diagnostics partnered with Thermo Fisher Scientific to establish a demonstration laboratory for clinical mass spectrometry applications, jointly advancing the informatization construction of clinical mass spectrometry laboratories; Rongzhi Biology launched the “QuanTOF Next-Generation Broad-Spectrum Quantitative Time-of-Flight Clinical Mass Spectrometry Platform”; Dipu Diagnostics released China’s first universal time-of-flight mass spectrometry detection system; In March, Meikang Biology collaborated with Thermo Fisher Scientific to promote the localized production of clinical mass spectrometers and related supporting equipment, accelerating the application and popularization of clinical mass spectrometry technology in China.

Various signs indicate that clinical mass spectrometry is emerging as the next golden track in the field of precision medicine.

Compared with traditional diagnostic techniques such as biochemistry and immunoassays, mass spectrometry offers unique advantages in sensitivity, specificity, and multiplexed detection. It serves not only as a complement but also as an extension to existing biochemical and immunological testing methods. Mass spectrometry can enhance the precision of current test items and detect analytes that are inaccessible to other technologies, thereby better guiding clinical diagnosis and providing more accurate test results for patients. Consequently, it is playing an increasingly important role in various clinical application scenarios.

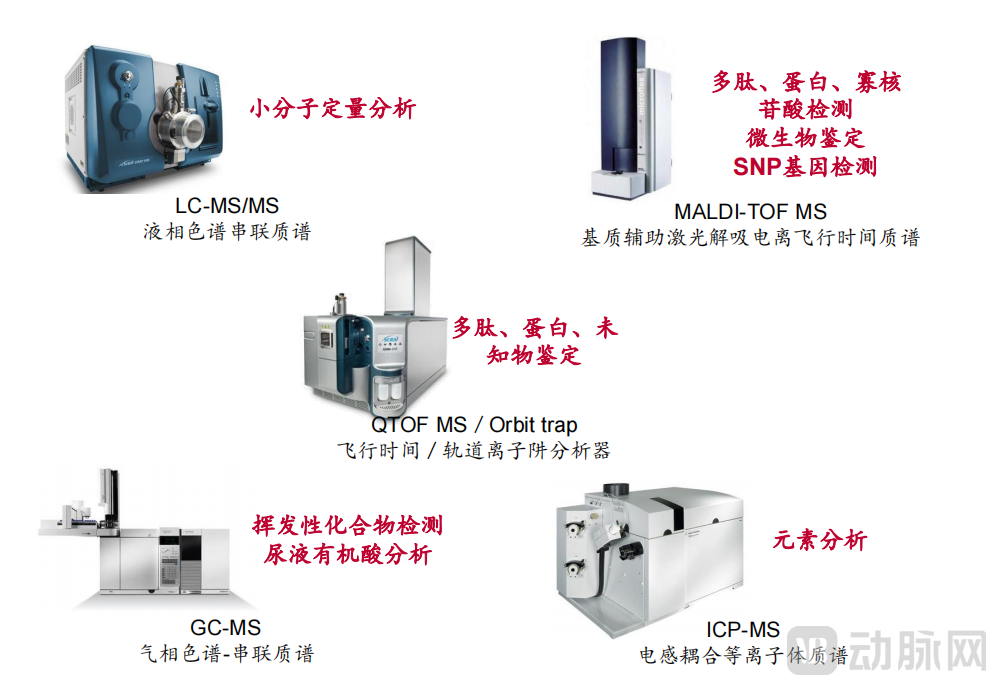

Mass spectrometers are categorized into various types, suitable for different clinical application scenarios.

(Source: Zhongtai Securities Research Institute)

Capital always has the keenest sense of market trends. In the clinical mass spectrometry sector, Hillhouse Capital has invested in Caliper and YingSheng Bio, CPE led the investment in Baichen Medical, and GTJA Investment backed Hezhen Diagnostics, the largest clinical chromatography/mass spectrometry testing technology platform. Frequent financing events and the entry of multiple investors may signal that clinical mass spectrometry is on the verge of an explosive growth period.

Wang Haijiao, Executive Partner at GTJA Investment Group, stated that the fundamental reason for the growing prominence of clinical mass spectrometry is the increasing recognition of its clinical application value. “Since 2018, the application of mass spectrometry in areas such as newborn screening and vitamin testing has expanded significantly, driving the growth of the clinical mass spectrometry market and attracting substantial interest from investors.”

According to statistics from VCBeat, there are currently 24 mass spectrometers and 48 clinical mass spectrometry kits approved in China. The application of mass spectrometry in scenarios such as vitamin testing and drug concentration monitoring has become relatively widespread.

As the first mass spectrometry company approved for listing in the IVD sector, Hexin Instrument’s prospectus also highlights the broad prospects of mass spectrometry technology. From 2018 to 2020, the company’s overall gross profit margin remained no lower than 64%, peaking at over 68%, with the unit price of its sold mass spectrometers reaching millions of yuan.

At the policy level, multiple policies and reform measures have been introduced to encourage the development of mass spectrometry technology. In early 2021, the Ministry of Industry and Information Technology solicited public comments on the “Development Plan for the Medical Equipment Industry (2021–2025).” In Part III, it outlined seven key areas for priority development in China’s medical device industry over the next five years, one of which is diagnostic and testing equipment, with mass spectrometry analyzers included among the prioritized diagnostic and testing equipment.

Furthermore, Liu Huafen, founder of Kaluopu, stated that the development of clinical mass spectrometry products currently lags behind clinical and technological advancements, with services in North America primarily delivered through Laboratory Developed Tests (LDTs). On June 1, 2021, the latest version of the Regulations on the Supervision and Administration of Medical Devices, issued by the State Council, officially came into effect. Article 53 of these Regulations stipulates that for in vitro diagnostic reagents for which no comparable products are yet marketed domestically, eligible medical institutions may, based on their clinical needs, independently develop such reagents and use them within their own facilities under the guidance of licensed physicians. The introduction of these Regulations is undoubtedly a significant benefit to the clinical mass spectrometry industry. In China, the regulatory compliance of the LDT model was previously a major factor constraining the development of clinical mass spectrometry; the gradual liberalization of LDT policies in China is now strongly promoting the application of mass spectrometry technology in clinical practice.

However, Wang Haijiao believes that although the number of financing events in 2021 was considerable, the proportion of investment institutions actually deploying capital in the clinical mass spectrometry sector remains very low. “China claims to have hundreds of capital firms investing in the healthcare sector, but according to our statistics, only about 50 have truly invested in the clinical mass spectrometry track.”

Clinical mass spectrometry is a systematic endeavor. Investment institutions primarily evaluate a company’s comprehensive capabilities, including clinical application development, upstream R&D, market expansion, and cost reduction. As the industry is still in its early stages, companies with such comprehensive strengths and investment value are exceedingly rare, which explains why most capital remains on the sidelines.

Mass spectrometry has a long history worldwide. The United States is the largest clinical mass spectrometry market globally, accounting for approximately 45% of the global market share. On the instrumentation side, among the top five global mass spectrometry manufacturers, four—Thermo Fisher Scientific, SCIEX, Agilent Technologies, and Waters Corporation—are headquartered in the United States, with only Shimadzu from Japan being the exception. This underscores the substantial strength of the United States in this market.

Liu Huafen stated, “Mass spectrometers are precision instruments designed for scientific research. They offer high levels of customization, flexibility, and scalability in both hardware and software; however, they lack standardized supporting applications and impose stringent requirements on operators. Consequently, in the early stages, third-party medical laboratories—with their abundant resources and substantial investments—became the preferred initial setting for clinical mass spectrometry. It is precisely due to the high proportion of third-party medical testing laboratories in the United States that the U.S. clinical mass spectrometry industry has experienced robust growth since 2000.”

Data shows that the share of clinical mass spectrometry testing has risen to 15% of the U.S. in vitro diagnostics market. In 2019, the U.S. clinical laboratory testing market was valued at approximately $80 billion, with the mass spectrometry testing segment accounting for about $12 billion.

In China, the clinical mass spectrometry industry started relatively late. Its application is limited to a small number of third-party medical testing laboratories and tertiary hospitals in major cities, with very limited scale. Both the depth and breadth of its adoption fall far short of those in developed countries such as the United States.

VCBeat has mapped out the current landscape of China’s clinical mass spectrometry industry across three dimensions: instruments, reagents, and testing services.

Device side: Very low domestic production rate; OEM certification is widespread.

China’s Mass Spectrometer Market Boasts Broad Prospects. Data from Essence Securities shows that China’s mass spectrometer market reached approximately RMB 14.22 billion in 2020, accounting for around 30% of the global market, with a compound annual growth rate (CAGR) of about 20% from 2015 to 2020. However, constrained by factors such as limited development levels, challenges in import substitution, and intellectual property protection issues, the localization rate of mass spectrometers in China remains extremely low.

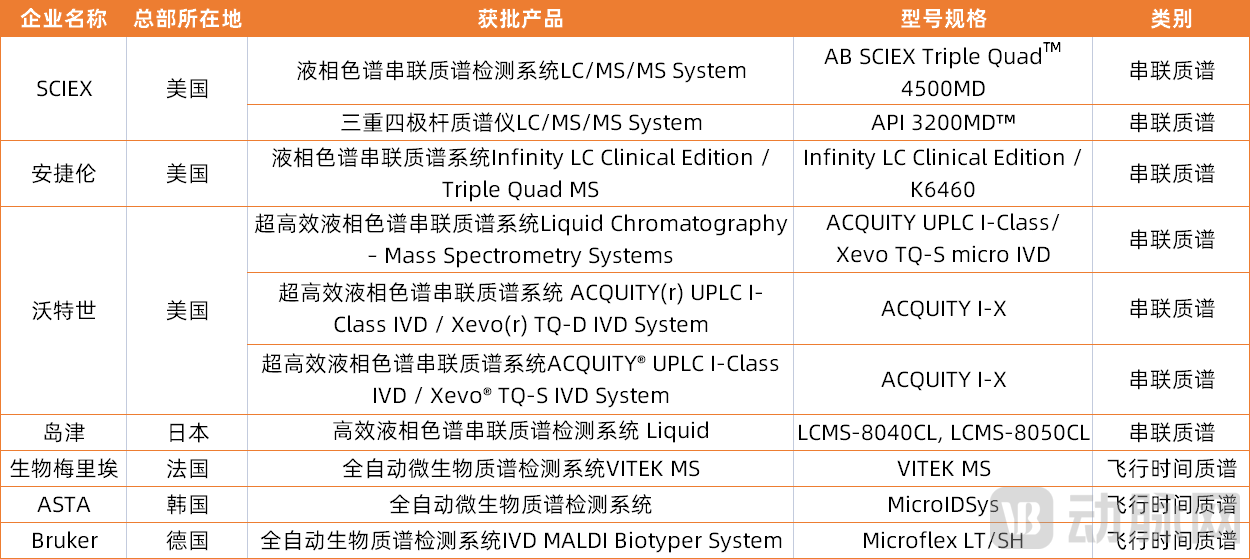

Imported Clinical Mass Spectrometry Instruments Approved by the NMPA

Currently, a total of 10 instruments have obtained import medical device registration approval, with manufacturers primarily consisting of major companies such as SCIEX, Agilent, Waters, and Shimadzu. Among these instruments, only three are time-of-flight mass spectrometers, while the remaining seven are tandem mass spectrometers.

In addition to registering imported medical devices independently, foreign companies commonly adopt OEM partnerships with domestic enterprises for registration purposes.

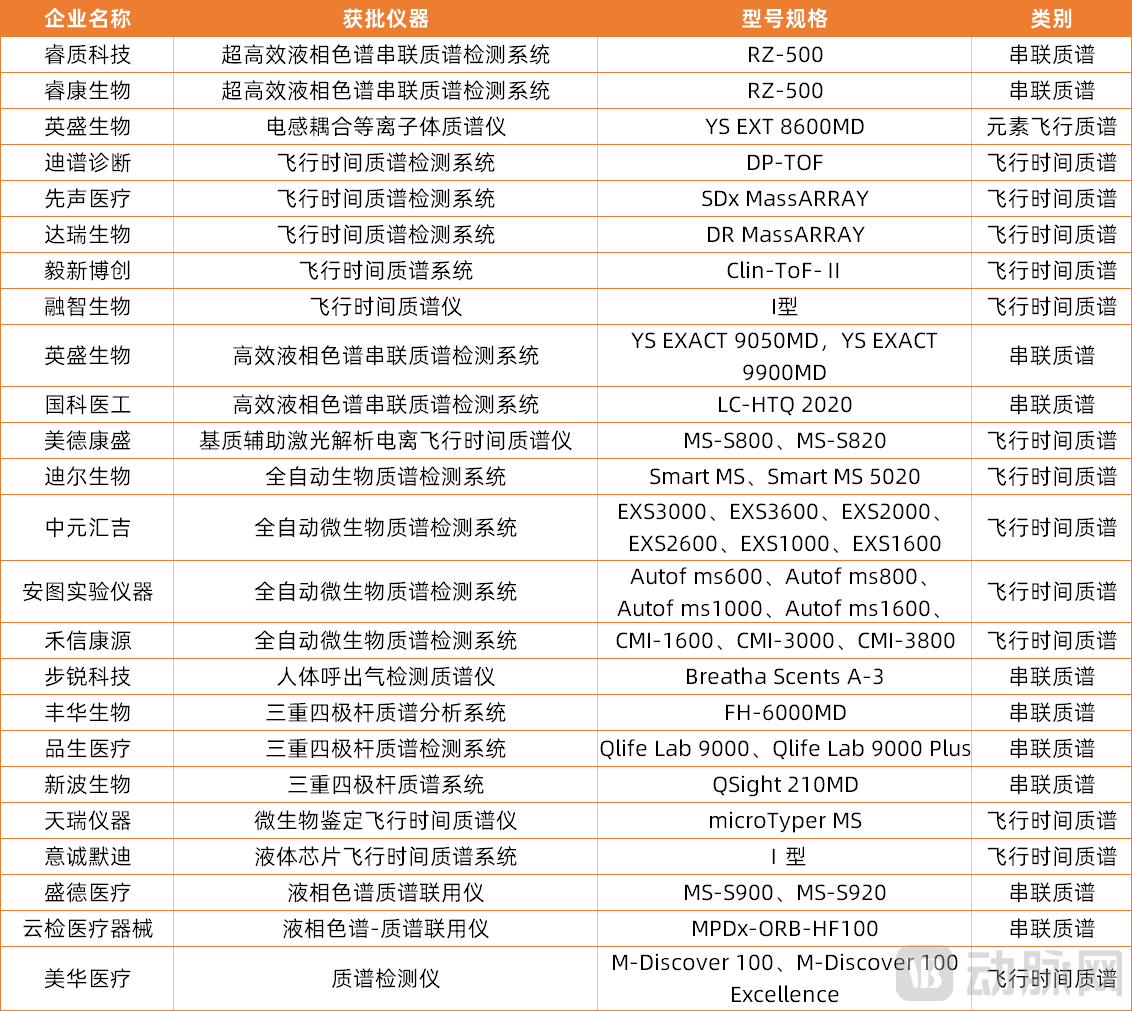

Domestic Clinical Mass Spectrometry Instruments Approved by the NMPA

A total of 24 domestically produced clinical mass spectrometry instruments have obtained registration certificates in China, significantly outnumbering imported clinical mass spectrometry instruments. However, it is understood that most of these instruments are actually imported devices rebranded for registration purposes. For instance, Thermo Fisher Scientific did not choose to register its imported medical devices independently in China; instead, it adopted a collaborative OEM approach, partnering with companies such as Yingsheng Biology, Ruikang Biology, Fenghua Biology, and Meikang Desheng. Only a few domestic enterprises, such as Hexin Instruments and FPI (Focused Photonics Inc.), possess independent intellectual property rights.

Liu Huafen stated, “Currently, mass spectrometers truly deployed in clinical settings, particularly liquid chromatography-mass spectrometry (LC-MS) systems, are predominantly imported or imported under original equipment manufacturer (OEM) arrangements. Although domestic manufacturers have invested years in developing China-produced LC-MS instruments, these domestically made devices are currently utilized more extensively in the food and environmental monitoring sectors, which involve larger sample volumes, while their share in the clinical market remains very small.”

Overall, there remains a certain gap between China’s high-end mass spectrometers and international standards. In the future, China will need to engage in long-term accumulation in the iterative upgrading of mass spectrometry technology and the development of its industrial chain.

Reagent Segment: Severe Homogenization in Vitamin Testing and Newborn Screening Calls for Accelerated Innovation

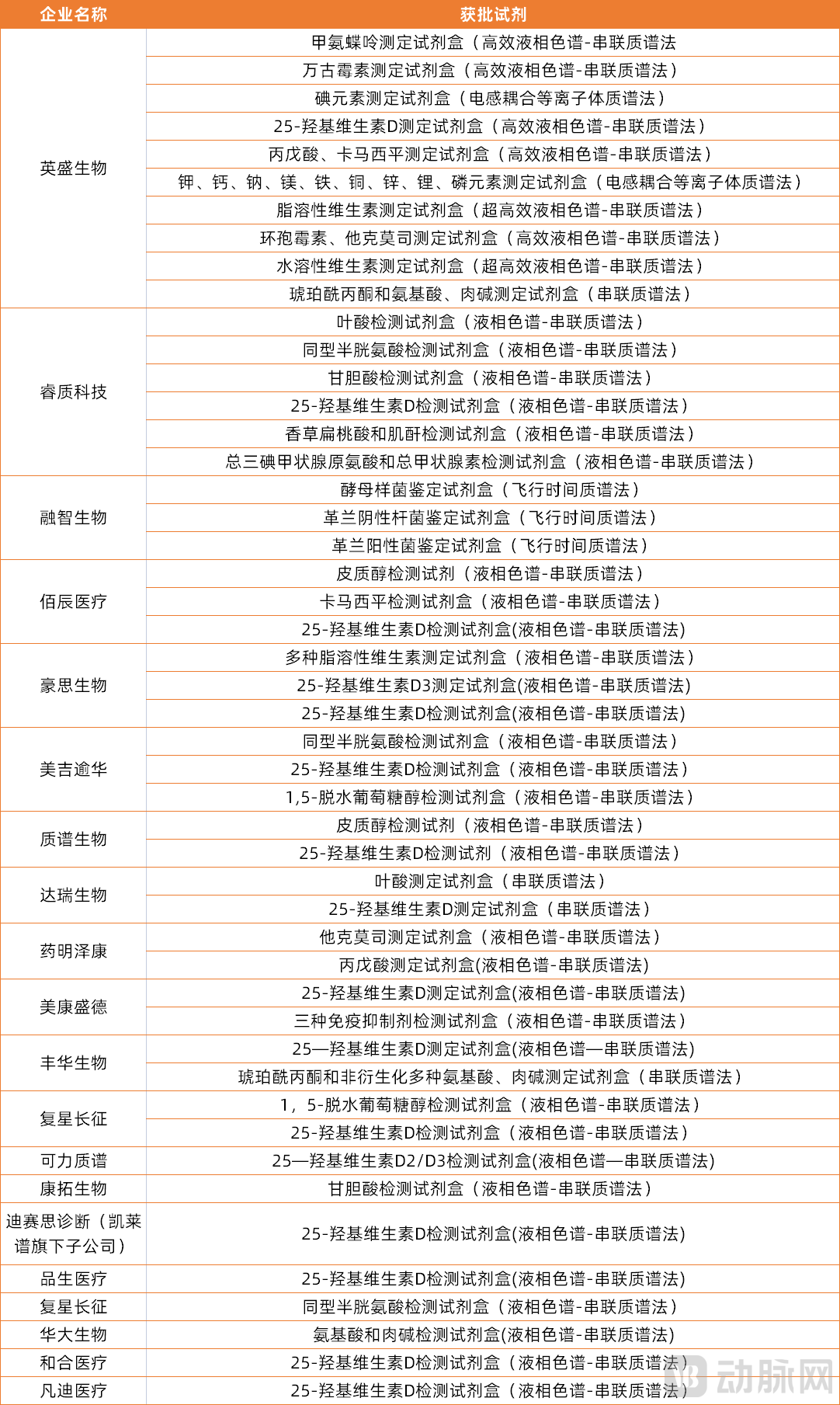

NMPA-Approved Domestic Clinical Mass Spectrometry Reagents

Foreign companies such as Agilent and Waters have not deployed reagent products in China, creating opportunities for domestic enterprises.

A total of 48 clinical mass spectrometry reagent products have been approved in China. In terms of quantity, Yingsheng Biology has the highest number with 10 approved reagent products. By category, there are as many as 43 tandem mass spectrometry kits, while only three time-of-flight mass spectrometry kits are available, indicating a greater preference for small-molecule analysis. Regarding application scenarios, vitamin testing and newborn screening are the key niche areas where companies are primarily focusing their efforts, and both applications are more mature in clinical practice.

High homogenization of reagents is an issue that cannot be overlooked in the clinical mass spectrometry sector. Most tandem mass spectrometry companies focus on vitamin testing, newborn screening, and therapeutic drug monitoring. As shown in the table, there are 14 different 25-hydroxyvitamin D test kits alone.

Developing proprietary projects and innovating mass spectrometry reagents will be the core of a company’s strategy to build a differentiated competitive advantage.

VCBeat has noted that Hepu Testing is developing innovative mass spectrometry reagents for the detection of Alzheimer’s disease, hyperhomocysteinemia, prostate cancer, and lysosomal storage disorders. Meanwhile, it is upgrading its existing product portfolio to achieve comprehensive vitamin profiling and broad coverage of medications across all clinical departments. Pinsheng Medical has bypassed the highly competitive markets for vitamin testing and newborn disease screening, instead targeting untapped clinical applications of mass spectrometry. It is developing diagnostic products for major diseases, including alternatives to traditional tests and cardiovascular conditions.

Enterprises should first seek breakthroughs on the service side and gradually achieve domestic substitution of products.

Testing services are the primary revenue source for the vast majority of clinical mass spectrometry companies today. However, there remains a significant gap between China and developed countries in terms of test menu breadth. Quest Diagnostics and LabCorp, the largest clinical mass spectrometry testing service providers in the United States, offer more than 400 mass spectrometry-based tests. In China, Hehe Diagnostics, currently the largest clinical “chromatography/mass spectrometry testing platform,” offers only slightly over 100 mass spectrometry tests.

In addition to the limited range of test items, there are few enterprises in China capable of providing mass spectrometry testing services. The market is primarily dominated by large third-party medical laboratories such as Hehe Diagnostics, KingMed Diagnostics, Dian Diagnostics, and Kangsheng Global, as well as specialized mass spectrometry service providers like Baichen Medical.

Among these, Hehe Diagnostics offers precise serum vitamin measurements, quantitative testing for amino acids and organic acids, as well as over 100 mass spectrometry-based assays including bioequivalence and pharmacokinetic studies. The KingMed Clinical Mass Spectrometry Center is the first clinical mass spectrometry laboratory in China to achieve dual accreditation from CAP and ISO 15189.

Wang Haijiao believes that, in the short term, companies specializing in clinical mass spectrometry testing services have greater growth opportunities. The timing for domestic substitution of clinical mass spectrometry products has not yet arrived; Chinese enterprises should first achieve breakthroughs on the service side. Once clinical education matures and the market opens up, they can then develop domestically produced mass spectrometry products to realize import substitution.

Is a One-Stop Solution the Right Development Path for China’s Clinical Mass Spectrometry Industry?

VCBeat has noted that overseas companies have a clear division within the industry chain, with Agilent and Thermo Fisher Scientific focusing on the product side, while Quest Diagnostics and LabCorp focus on testing services. In China, however, many companies claim to be developing one-stop solutions for clinical mass spectrometry. Is this one-stop solution approach a development path suited to China’s unique characteristics?

As the name suggests, a one-stop solution refers to an integrated approach that spans the upstream and downstream segments of the industrial chain, providing a comprehensive package including pre-analytical processing equipment, mass spectrometry instruments, reagents, and testing services. Multiple companies, such as Calibra Biosciences, YingSheng Biotech, Baichen Medical, Raycan Technology, Haosi Biotechnology, Medconn Biotechnology, Pinsheng Medicine, and Yixin Bochuang, have all announced their strategic initiatives to develop complete clinical mass spectrometry solutions.

It is reported that Calipso pioneered the concept of a “one-stop clinical mass spectrometry solution” in 2017. Liu Huafen, founder of Calipso, stated that so-called one-stop solutions are rare in Europe and the United States. The primary reason for their emergence in China lies in the small proportion of independent medical laboratories; clinical resources in China are predominantly held by hospitals, and not every hospital possesses sufficient technical expertise to independently carry out clinical mass spectrometry testing. Given the substantial differences between mass spectrometry instruments and conventional biochemical analyzers, and considering clinicians’ limited familiarity and experience with this emerging technology, hospitals are often unable to conduct mass spectrometry tests independently. Therefore, beyond product sales, companies must also provide comprehensive support services, including professional laboratory renovation, selection of ancillary equipment, establishment of methodologies and quality management systems, training, as well as ongoing instrument maintenance and assay upgrades.

“In China, independent medical laboratories account for a small share of the market, hospitals control clinical resources, and mass spectrometers cannot achieve the same high level of automation as biochemical and immunological analyzers. Under these circumstances, one-stop solutions will remain a unique business model in China for a certain period,” said Liu Huafen.

Wang Haijiao stated, “The prevalence of one-stop solutions is merely a temporary phenomenon. We believe that as technology advances and clinical education matures, companies will inevitably have to choose between focusing on products or services.”

The fundamental issue hindering the clinical implementation of mass spectrometry is that its inherent technical approach is not sufficiently adapted for clinical use.

Wang Feng, founder of Demeter, once pointed out to VCBeat that currently, Chinese mass spectrometry and chromatography companies mainly operate under two models: one is the “rebranding registration” model, which involves importing foreign mass spectrometry equipment, rebranding it for regulatory registration, and then selling it; the other is a third-party testing service model that establishes hospital-based outlets to “stake out territory,” generating profits through regional sample collection and analysis.

Neither of these two models has addressed the core pain points hindering the clinical adoption of mass spectrometry. To pave the way for its integration into clinical practice, substantial technological upgrades to existing mass spectrometry systems are imperative.

Wang Haijiao noted that biochemical and immunological assays, which are widely used in clinical practice, have generally achieved a high degree of automation with user-friendly, “foolproof” operation. In contrast, mass spectrometers resemble computers, requiring users to establish their own methodologies and decide which programs to run and what functions to perform. This results in complex instrument operation, stringent requirements for operators, and prolonged testing times. In terms of both performance and usability, mass spectrometry does not well align with the technical requirements and operational environment of modern laboratory medicine, remaining largely at the level of a scientific research instrument.

It can be noted that some companies are already upgrading their mass spectrometry systems.

Demeter has achieved breakthroughs in chromatography automation and mass spectrometry stabilization technologies, pioneering the development of the MS-MATE highly stable clinical-grade mass spectrometry system and the MLC/FLC fully automated two-dimensional liquid chromatography system designed for clinical laboratory use. The MS-MATE 9500/9600 clinical-grade mass spectrometry system incorporates a suite of advanced features, including isotope-free calibration, alternating count measurement, automated solvent management, and RTJ (Raw Tube to Injection) sample preparation. These innovations significantly enhance the accessibility of mass spectrometry by reducing its reliance on specialized expertise.

To better align mass spectrometry systems with the practical demands of clinical applications, Kalu Pu has established a closed-loop ecosystem encompassing automated front-end sample processing, high-throughput testing, mass spectrometry instruments, standardized consumables, traceability of measurement values, reagent products, methodological optimization, quality system management, and customer training. This integrated approach enables rapid establishment of mass spectrometry platforms for clients, ensuring high-quality and efficient fulfillment of clinical testing needs. Hepu Testing has entered into an exclusive partnership with Tecan to jointly develop an automated pre-treatment platform for mass spectrometry. InnoCare Bio has launched two automated mass spectrometry pre-treatment devices—the fully automated pre-treatment platform MSLET™ 2000 and the fully automated multi-functional sample pre-treatment system YS-600—thereby building a comprehensive, one-stop, fully automated clinical mass spectrometry platform based on mass spectrometry application technologies. Baichen Medical has developed an automated immunomass spectrometry pre-treatment platform.

Meanwhile, the high cost of mass spectrometers, limited test menus, and insufficient clinical awareness are major obstacles hindering the clinical adoption of mass spectrometry. It is believed that these issues will be resolved one by one as clinical education matures, testing speed increases, and testing volume grows.

In summary, the clinical mass spectrometry sector offers a long runway and is currently in an expansion phase, requiring considerable time for clinical education and the establishment of core competitive advantages. Once these advantages are solidified, the snowball effect will gradually become apparent. Wang Haijiao predicts that mass spectrometry technology is poised for large-scale clinical adoption within the next three to five years. Liu Huafen stated, “In the future, product quality and innovative multi-omics biomarkers will be the two key drivers of enterprises’ long-term development.”