The Next Stop: Universal Mental Health? An Innovation and Investment Outlook on the Mental Health Markets in China and the U.S.

Authors: Yu Xiangyu and Xiong Xiaojia from Shangyi Investment. Republished with permission by VCBeat.

Observations on Innovative Investment in the Mental Health Markets of China and the United States

The White Paper on Mental Health of Urban Residents in China, released in 2018, reveals that 73.6% of urban residents in China are in a state of suboptimal psychological health, while 16.1% exhibit varying degrees of psychological issues. In 2019, the total market size of the U.S. mental health industry exceeded $19 billion, whereas China’s stood at less than RMB 40 billion during the same period. Does this disparity indicate that mental and psychological disorders are less severe in China than in the United States, or that such issues remain largely undetected? In this analysis, we share our reflections on these questions, aiming to spark further discussion among entrepreneurs and investors in China’s mental health sector, as well as individuals affected by mental and psychological disorders. We hope to benefit a broader audience, recognizing that many of us may ourselves be on the verge of needing such support.

Public and Personal Stigma

The United States developed an understanding of mental and psychological disorders earlier than China; however, this does not imply universal recognition of these conditions as common diseases. Public, media, and individual ideological stigma toward mental and psychological disorders can be gradually alleviated through education and humanistic approaches, but ultimately, resolution depends on the establishment of a comprehensive system for diagnosis, treatment, and rehabilitative care.

Mental and psychological disorders are widely accepted in most Western cultures, with the public and individuals alike recognizing them as common medical conditions. However, certain regions in Western countries characterized by intense economic competition also witness movements that stigmatize mental and psychological disorders. Compassion for the vulnerable and a general sense of humanism serve as overarching drivers toward destigmatization. Nevertheless, protecting the vulnerable and those who are stigmatized may fulfill other social objectives: by demonstrating benevolence, societies reaffirm their social authority and commit to safeguarding individuals with potential vulnerabilities, thereby enhancing feelings of security and social cohesion.

In Eastern cultures, research on the stigma surrounding mental and psychological disorders is rarely discussed; this does not mean it is absent, and indeed, the situation may be even worse. We conducted a survey within a selected circle of acquaintances (sample size: 50): 85% of respondents stated that they did not have any mental illness, yet 53% reported experiencing persistent low mood, insomnia, or alcohol abuse lasting more than two weeks over the past three years; 76% expressed unwillingness to associate with individuals suffering from mental and psychological disorders, while only 13% indicated they would accept such relationships even if aware of the other party’s mental health condition; meanwhile, 93% of respondents believed that institutions for the diagnosis and treatment of mental and psychological disorders are psychiatric hospitals.

Discrimination against mental and psychological disorders persists in contemporary society. First, some individuals, constrained by prejudice, view patients as morally tainted. Second, inadequate social support systems and a lack of a caring atmosphere make it difficult for most patients with mental and psychological disorders to truly integrate into society. Medicine, particularly social medicine, has clearly demonstrated that individuals with mental and psychological disorders are no more dangerous than healthy individuals. Their unusual behaviors stem from abnormalities in thinking, emotions, and conduct, which result from dysfunctions in brain activity. These conditions are fundamentally no different from pathological changes in other organs and are both treatable and curable. Social discrimination not only exacerbates the psychological burden on these patients but also accelerates the “short-board” effect, undermining the development of societal moral standards.

Mental Health Market

The incidence rate and economic burden of mental and psychological disorders in China are no lower than those in the U.S. market. However, significant gaps exist between China and the United States in policy guidance, basic research, infrastructure development, diagnosis, treatment, and rehabilitative care for mental and psychological disorders, particularly in technological innovation and investment. The frequent occurrence of severe incidents involving behavioral disturbances in recent years indicates that China is at a critical tipping point in mental health management.

According to 2019 statistics from the National Alliance on Mental Illness (NAMI), 20.6% of U.S. adults (51.5 million people) had a mental illness; 5.2% of U.S. adults (13.1 million people) had a serious mental illness; and 3.8% of U.S. adults (9.5 million people) had both a substance use disorder and a mental illness. In 2019, 43.8% of U.S. adults with mental illness received treatment, while 65.5% of those with serious mental illness received treatment. One in every eight emergency department visits by U.S. adults involved mental illness or substance use disorders (an estimated 12 million visits). Mood disorders were the leading cause of hospitalization among all individuals under age 45 in the United States (excluding hospitalizations related to pregnancy and childbirth). Across the U.S. economy, serious mental illness results in annual losses of $193.2 billion.

Of the RMB 5 trillion output value of China’s big health industry (2017 data), mental health accounted for only over RMB 40 billion. By the end of 2015, there were 2,936 mental health service institutions nationwide, with 433,000 psychiatric beds available, representing a substantial increase from 2010 (1,650 institutions and 228,000 beds). Across China, there were 27,733 licensed (and assistant) psychiatrists, 57,591 psychiatric nurses, and more than 5,000 psychotherapists. Over 900,000 individuals obtained professional qualification certificates as psychological counselors. According to the White Paper on Mental Health of Urban Residents in China released in 2018, 73.6% of urban residents were currently in a state of suboptimal mental health, and 16.1% experienced varying degrees of psychological problems. Mental health is closely correlated with physical health; among patients with chronic diseases, 50.1% exhibited tendencies toward psychological issues of varying severity.

Technological Innovation Pathway

An analysis of the business directions of 1,000 startups in the U.S. mental health sector reveals that these companies aim to address challenges such as the diagnosis and treatment of mental disorders, the shortage of qualified professionals, and the need for market education. From a venture capital perspective, investors are more inclined to fund innovative products and business models that prioritize diagnostic and therapeutic services while integrating artificial intelligence and digital therapeutics. As an interdisciplinary field, mental healthcare relies on clinicians who prefer to evaluate the reliability of these new technological innovations based on efficacy and data.

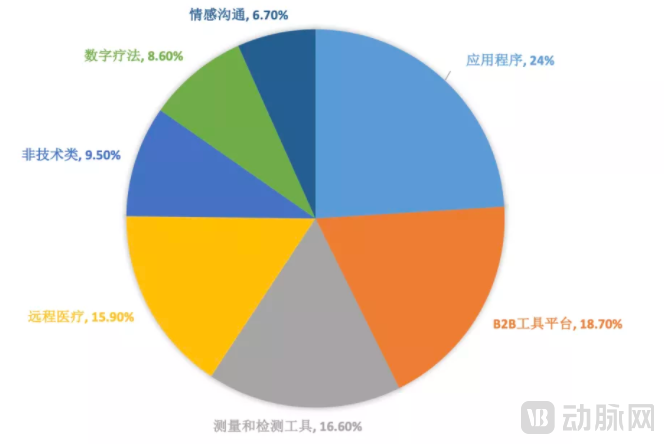

Of the 1,000 mental health startups surveyed, more than 80% were founded after 2010. Startups focusing on tools and gamified applications for sleep management, meditation and mindfulness, breathing regulation, and online mental health education accounted for the largest share at 24%. B2B tools that integrate mental health industry resources to provide search and resource allocation services for enterprises or healthcare providers represented 18.7%. Ranking third were startups offering measurement and testing tools capable of actively or passively tracking and assessing patients’ emotional and psychological activities, accounting for 16.6%. Startups facilitating remote consultations between patients and psychiatrists or psychological counselors made up 15.9%. Non-tech startups, including physical healthcare institutions and pharmaceutical companies, accounted for 9.5%. Digital therapeutics combined with pharmacological and behavioral interventions represented 8.6%. At the bottom were tools providing community-based emotional communication support, accounting for 6.7%, as shown in the figure below.

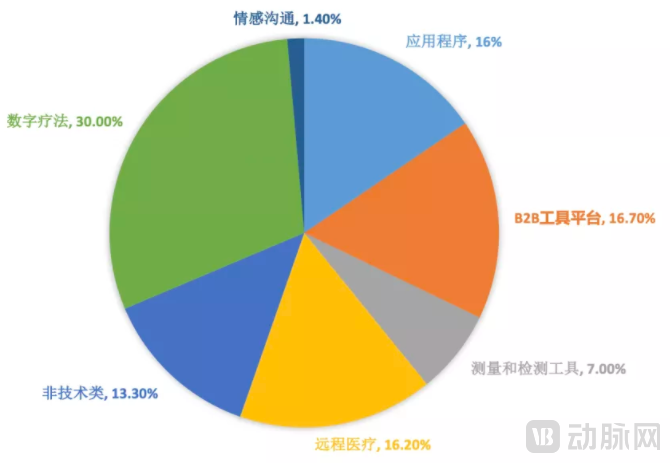

However, there is a stark contrast between investor interest and the areas where startups are concentrated. Applications account for the majority of startups in this field. To date, digital therapeutics (DTx) have secured the largest share of funding, at 30%. This trend is partly driven by the capital-intensive nature of obtaining FDA approval rather than merely building applications. Although tools designed to measure and track patients’ psychological activities are generally believed to gradually address the high labor costs and low efficiency in the mental health sector, they have attracted minimal funding, accounting for only 7%. As shown in the figure below:

The new medical model (i.e., the biopsychosocial medical model) emphasizes that the object of medical care is the whole person—an individual living within a specific social environment and possessing complex psychological activities—rather than merely a “physiological machine.” Dr. Murali Doraiswamy, Professor of Psychiatry and Behavioral Sciences at Duke University and Director of the Neurocognitive Disorders Program, notes that while there is a severe shortage of psychiatrists and therapists in some remote areas of the United States, he remains cautious about whether artificial intelligence can fill this gap. Dr. Alex Leow, Associate Professor of Psychiatry and Bioengineering at the University of Illinois College of Medicine, stated, “When neuroimaging first emerged, we hoped that by combining the power of genomics with this new technology, we would be able to identify specific patterns of brain activity that could tell us whether a person was depressed or manic.” More than 200 studies have used machine learning algorithms to distinguish brain differences between individuals with specific disorders (such as Alzheimer’s disease, schizophrenia, and depression) and healthy controls. However, these findings have not yet led to a leap forward in clinical care. “When you are focused on treating a specific individual, these patterns do not necessarily translate into clinical use,” said Dr. Leow. Dr. John Torus, Director of the Center for Digital Psychiatry at Harvard Medical School, believes that current innovations in mental health have not yet become national standards or tools in widespread use.

Investment and M&A

In stark contrast to the booming U.S. mental health investment market, China’s capital markets have remained notably lukewarm toward mental health initiatives, often conflating mental health with psychological counseling in public perception. It is essential to distinguish stigmatized psychiatric and psychological disorders from the colloquial and derogatory term “shenjingbing” (literally “nerve disease,” commonly used as an insult meaning “crazy”) and to eliminate associated discrimination. As of early 2020, the U.S. mental health sector had spawned 1,290 tech-enabled startups, whereas more than 400 comparable companies had emerged in China. The U.S. market boasted seven unicorns valued at over $1 billion, while only three Chinese counterparts had reached Series C financing. Given the highly fragmented nature of the mental health market, mergers and acquisitions are expected to become increasingly frequent in the future.

As part of the digital health investment boom, investors began venturing into the mental health sector in recent years, with venture capitalists pouring a record $1.5 billion into mental health-related startups by the end of 2020. Driven by digital health IPOs, SPAC transactions, and M&A activity, the United States now has seven mental health unicorns, up from just two a year earlier. According to CB Insights data, funding for mental health startups in 2020 was 5.5 times the $275 million invested four years prior. There were 124 deals last year, compared with 69 in 2016. Genoa Health, a telepsychiatry and specialty pharmacy company, became the first unicorn in the U.S. mental health space when it was acquired by UnitedHealth Group for $2.5 billion in 2018. Bob Kocher, a partner at Venrock, bet on Lyra Health, which he co-founded in 2015 with former Facebook CFO David Ebersman. Valued at $2.3 billion in a January financing round, Lyra Health focuses primarily on large employers, counting Morgan Stanley and eBay among its clients. The online mindfulness and meditation platform Calm has also reached a valuation of $2 billion. Against the backdrop of the pandemic, BetterUp (valued at $1.9 billion), Talkspace (valued at $1.4 billion), Modern Health (valued at $1.2 billion), and Ginger (valued at $1.1 billion) joined the club in 2021.

The global digital mental health sector has seen vigorous development over the past five years, with a number of early-established companies achieving mature business models. Meanwhile, emerging startups and innovative business models continue to proliferate. In China, the digital mental health landscape remains a blue ocean, characterized by relatively few participants and most enterprises still in their early stages of development. In 2020, Dami Xiaomi, a company specializing in rehabilitation and treatment for children with autism, completed its Series C financing. In 2021, Zhaoyang Doctor, a digital diagnosis and treatment platform for psychiatric and psychological conditions, announced the completion of its Series B financing, amounting to hundreds of millions of yuan. This round was co-led by Matrix Partners China and Qianji Capital, with participation from Opu Family Office. Haoxinqing, founded in 2016, focuses on the central nervous system domain, leveraging intelligent diagnostic and treatment systems along with internet hospital service networks to provide smart rehabilitation management and online medical services for users with psychiatric and psychological disorders. Within less than a year of its establishment, Haoxinqing secured RMB 50 million in angel-round funding led by Enhua Pharmaceutical. In 2018, Haoxinqing obtained tens of millions of yuan in Pre-A round investment from Zhongzi Capital and Korea’s KIP, bringing its cumulative financing to over RMB 125 million.

From a global perspective, the mental health market is highly fragmented, which means that mergers and acquisitions (M&A) will provide entrepreneurs and investors in this sector with more opportunities for growth and exit. Traditional giants such as UHS and ACADIA have achieved continuous scale expansion through M&A integration in the US and European markets. In the coming years, we believe that insurance companies, traditional healthcare providers, and even buyers from non-medical sectors will continue to focus on M&A opportunities in this field. For example, Anthem Inc. acquired Beacon Health Options in 2019, and the unicorns Talkspace and Ginger completed their merger in 2021.

Conclusion

1. Mental health issues affect everyone on the planet. Most individuals in need of assistance fail to receive adequate care, due to concerns regarding social stigma, high out-of-pocket costs, and barriers to accessing high-quality diagnostic and therapeutic services. At the national level, educational efforts to combat the stigmatization of mental health conditions are gaining momentum, and public awareness is awakening. Meanwhile, the government is beginning to prioritize the mental health sector in terms of infrastructure development and medical insurance policies. Consequently, we project that the market size of China’s mental health industry will exceed RMB 100 billion within the next five years.

2. As of the end of 2020, based on incomplete statistical data, there were approximately 97,000 enterprises in China’s mental health sector, with around 45,000 active companies. Only slightly more than 400 of these were technology-driven firms. The vast majority operated as psychological counseling studios, while institutions holding medical qualifications were exceedingly few. The development of products and services centered on technological innovation will be a key focus for future growth.

3. Basic research on mental health, the industrial service system, and two-way talent cultivation are key shortcomings that need to be addressed at the national level.

4. We do not believe that large funds dedicated to investing in the mental health sector will emerge in the current capital market, which constitutes the biggest obstacle to the prosperity of the mental health industry. However, we believe that investments and mergers and acquisitions within the healthcare industry will serve as a catalyst for the development of China’s mental health sector.

Author

Shangyi Investment

Yu Xiangyu

Founder of Shangyi Investment

Chairman of Yitou Medical

Shangyi Investment

Xiong XiaojiaDoctor

Partner, Shangyi Investment

Vice President of Yitou Medical

Chief Medical Officer