Stryker's High-Stakes Game and the Turbulent Orthopedic Market

Stryker

Medical Device R&D, Production, and Sales Company

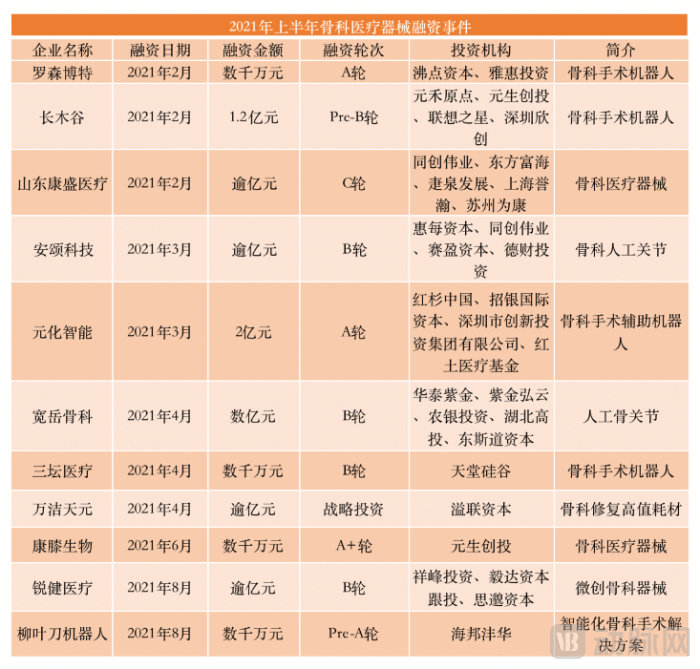

The orthopedic market remains hot.

According to statistics from VCBeat (WeChat ID: vcbeat), there were 11 financing deals in China’s orthopedics sector in the first half of this year alone, with most amounts exceeding RMB 100 million.

Data source: Artery Orange Database

“Import substitution” and the market environment in which leading orthopedic companies are expanding overseas are driving the orthopedic industry forward. Both the capital markets and the industry as a whole are eager to find answers for the development of China’s domestic orthopedic sector in this process.

A review of the development of relevant domestic enterprises in recent years reveals that only a small minority possess international competitiveness. How to expand into broader markets and forge their own growth trajectories has become a pressing challenge for many companies.

In this turbulent market, orthopedic giant Stryker has created its own miracle, achieving 40 consecutive years of sales growth. How did Stryker successfully break through and lead the industry for years? VCBeat provides an analysis.

The story of Stryker begins with its founder, Homer Stryker.

In fact, Homer Stryker was not originally a professional medical device developer, but an orthopedic surgeon. During his medical practice, he discovered that certain medical products failed to meet patient needs. This insight prompted him to take the first step into medical device research and development.

From 1936 to 1939, Homer Stryker formally embarked on his exploration of medical devices. During this period, he developed his first products: a turning bed frame and walking heels. Subsequently, Homer Stryker commenced his medical practice in Kalamazoo, Michigan, establishing an office at Borgess Hospital and utilizing the basement for product research and development.

As R&D progressed, its products were launched one after another and gained widespread popularity. In 1941, Homer Stryker founded The Orthopedic Frame Company to mass-produce these products.

One year later, the company began manufacturing the Wedge Turning Frame to assist caregivers in repositioning patients with severe back injuries.

Wedge Turning Frame

In 1946, Homer Stryker merged with The Orthopedic Frame Company, and in 1947, he invented the oscillating saw and patented it, laying the foundation for subsequent product lines such as surgical instruments.

After more than a decade of development, in 1958, Homer Stryker and his team successfully developed the Circ-O-Lectric bed by integrating features of the frame, achieving $1 million in sales.

Circ-O-Lectric Bed

1964 was a historic year for Stryker. It was the year Homer Stryker announced his retirement, and also the year the company was officially renamed Stryker Corporation in his honor.

Looking back on this history, it is easy to see how Homer Stryker’s personal journey and the more than two decades he spent growing alongside the company have continuously influenced Stryker. His original aspiration to develop devices that meet patient needs has become an intrinsic part of Stryker’s corporate DNA: “Advancing healthcare together with patients.”

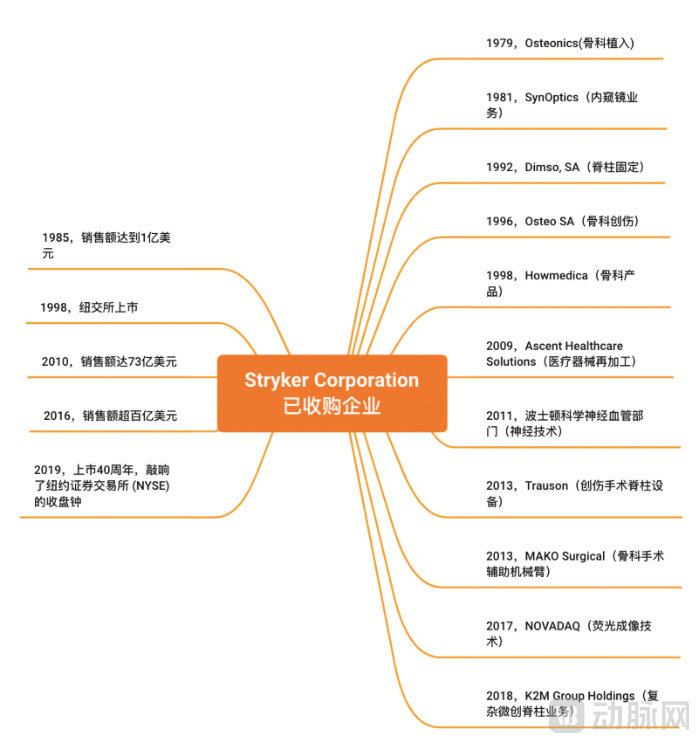

In 1976, Stryker's sales had grown to $17.3 million.Three years later, Stryker went public on the NASDAQ and acquired Osteonics in the same year, making a significant entry into the orthopedic implant market.

From 1981 to 1996, Stryker’s sales revenue nearly sextupled compared to five years earlier, surpassing $100 million.During this period, Stryker successively expanded its business lines in endoscopy, spinal fixation, and orthopedic trauma through acquisitions.

After 18 years on the Nasdaq, Stryker listed on the New York Stock Exchange in 1997. In 1998, Stryker acquired Howmedica, a major global player in the orthopedic market, and doubled its size the following year.

In 2009, Stryker acquired Ascent Healthcare Solutions, a U.S. provider of medical device reprocessing and remanufacturing services.In 2010, Stryker's sales revenue had grown to $7.3 billion.

In 2011, Stryker acquired Boston Scientific’s neurovascular division to expand its neurotechnology business. In 2013, Stryker made further moves by acquiring Trauson and MAKO Surgical, thereby expanding its trauma and spine product portfolio and advancing robotic-assisted orthopedic surgical systems. By 2016, Stryker’s sales had exceeded $10 billion.

Between 2017 and 2018, Stryker successively acquired NOVADAQ and K2M Group Holdings to expand its business in fluorescence imaging technology and complex minimally invasive spine surgery. In 2019, to celebrate the 40th anniversary of its public listing, Stryker’s leadership rang the closing bell at the New York Stock Exchange (NYSE).

Stryker’s Acquired Companies (Compiled from Official Website Information)

Leveraging the power of M&A, Stryker has advanced rapidly.

No M&A, No Giants.Since its IPO, Stryker has completed 11 major acquisitions, driving a rapid surge in its sales revenue.Rapid growth through mergers and acquisitions appears to have become a key strategy for Stryker.

Stryker has continuously expanded its product portfolio by integrating external resources, entering multiple fields, thereby enhancing its corporate competitiveness and enabling the company to achieve leapfrog growth.

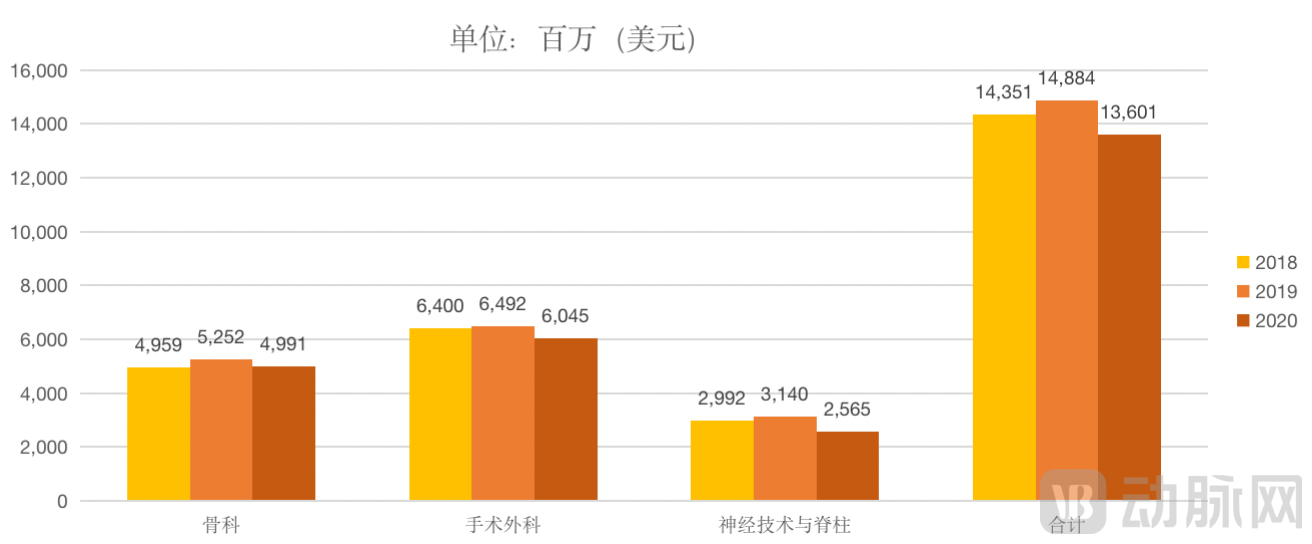

Net Product Sales

An analysis of Stryker’s net product sales data offers a glimpse into its market strategy.From 2018 to 2020, the sales contributions of Stryker’s three major segments—Orthopaedics, MedSurg (Medical and Surgical), and Neurotechnology & Spine—were nearly equal. However, while all segments experienced growth in 2019, they saw a decline in 2020.

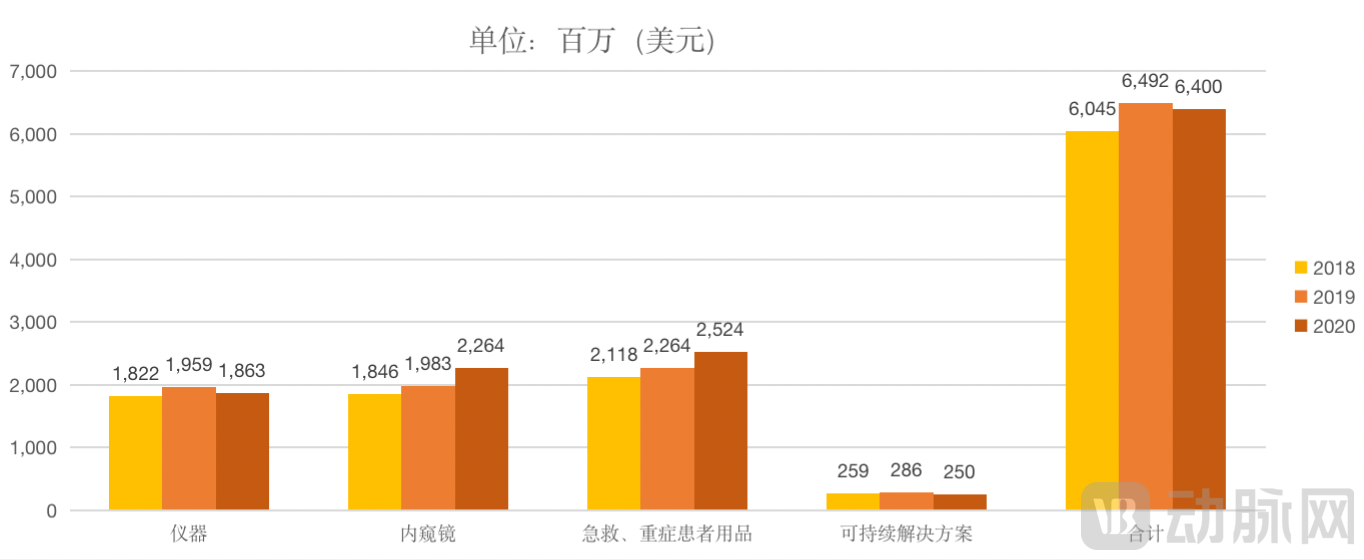

Breaking it down, the surgical segment accounts for the largest share of sales, representing approximately 45% of the total in 2020. Within this segment, instruments, endoscopes, emergency and critical care products, and sustainability solutions accounted for 39%, 29%, 28%, and 4% of the segment's sales, respectively.

Proportion of Sales in the Surgical Segment

Its surgical product portfolio spans nearly the entire medical care continuum, featuring an exceptionally robust pipeline.Including emergency and resuscitation products, surgical equipment, navigation systems (instruments), endoscopy and communication systems (endoscopes), patient handling, emergency medical equipment and critical care disposable products (supplies for emergency and critically ill patients), reprocessed and remanufactured medical devices (sustainability solutions), as well as other medical device products for various medical specialties.More importantly, some of Stryker’s specialized product segments comprise not just a single product category but multiple solutions.Its hospital bed product series includes as many as 11 solutions.

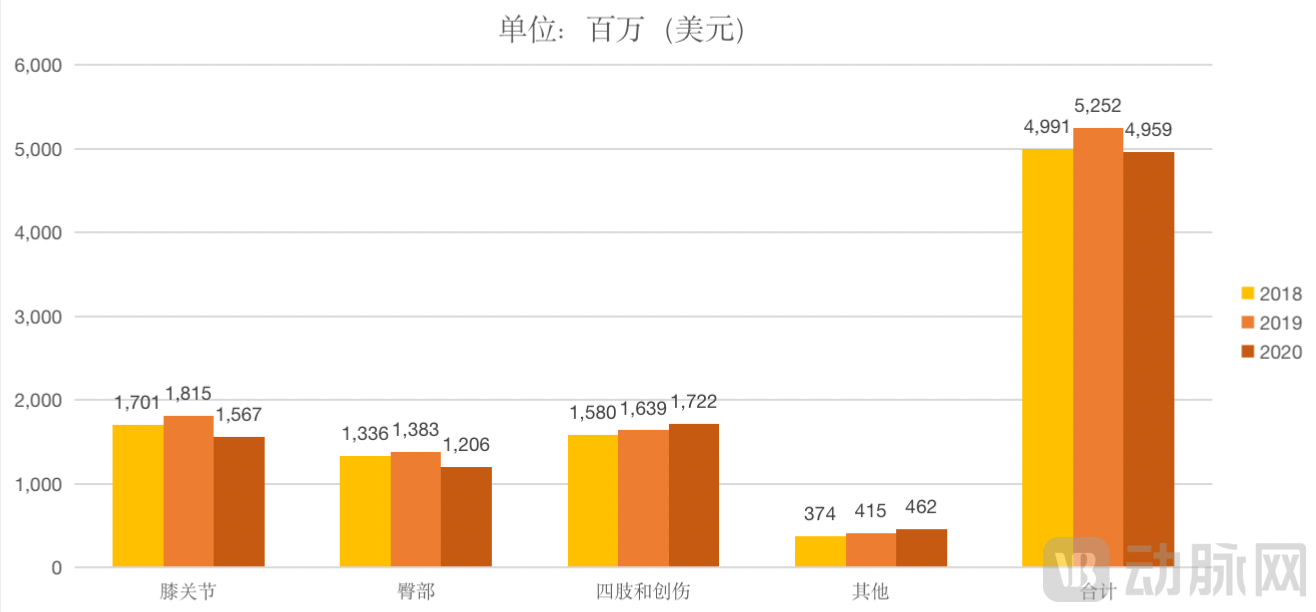

Stryker’s orthopedic business primarily covers solutions related to craniomaxillofacial, foot and ankle, joint reconstruction, spine, trauma and extremities, upper extremities, sports medicine, and digital systems. Ranking second in sales volume, Stryker accounted for 34% of total sales in 2020. Within its orthopedics segment, knees, hips, trauma and extremities, and other categories contributed 32%, 24%, 35%, and 9% of sales, respectively.

From the perspective of sales data, Stryker did not make significant adjustments to its strategic layout for hip-related products during the period from 2018 to 2019, remaining basically stable.However, in 2020, the knee segment, which was the primary revenue source for the orthopedics business, was overtaken by the trauma and extremities business in terms of revenue.

Orthopedics Sales Revenue Share

The change in revenue stems from strategic adjustments made by Stryker.In 2020, Stryker completed the acquisition of Wright Medical Group NV for a substantial sum of $4.1 billion.

Wright Medical is a long-established company founded in 1950, specializing in extremities products. Its offerings include surgical solutions for the upper limbs—such as the shoulder, elbow, wrist, and hand—as well as solutions for the lower limbs, including the foot and ankle.

Although Stryker and Wright Medical have some degree of business overlap, their respective areas of expertise are not entirely identical.This acquisition can be described as an innovative supplement to Stryker, filling the gap in its less competitive extremities business. Stryker aims to leverage this foundation to launch a strategic combination of initiatives, with the goal of rapidly capturing the trauma and extremities market.

Stryker CEO Kevin Lobo has stated on this matter“Wright Medical’s lower extremity products will address the limitations of Stryker’s related offerings. This acquisition further strengthens the company’s global market position in trauma and extremities, providing significant opportunities to drive innovation, improve patient care, and reach more patients.”

AxSOS3

After the acquisition of Light Medical,Last year, Stryker launched the AXSOS 3 Ankle Fusion System.By analyzing data from over 25,000 skeletal CT images across diverse populations, the system identifies products suitable for the majority of patients, thereby reducing the need for customization and further lowering healthcare costs.

"Industry giants are not built in a day; Stryker’s strategy in the orthopedics sector extends far beyond this."

In response to issues such as high revision rates for joint replacement surgeries and soft tissue damage caused by insufficient surgical precision, Stryker invested $1.7 billion in 2013Acquiring MAKO Surgical and securing its “ace” card—the MAKO joint replacement robot—successfully enabled entry into the orthopedic surgical robotics sector.

Mako Joint Replacement Robot

This robotic system enables 3D intelligent modeling of patients’ bony anatomy based on CT scans for preoperative planning, identifying the surgical trajectory that minimizes tissue trauma and reduces patient injury.Mako’s haptic technology continuously assesses the balance between soft tissues and joints throughout the surgical procedure, addressing issues such as implant alignment, soft tissue balance, and flexion contracture. By providing surgeons and the surgical team with continuous real-time data, it helps mitigate potential surgical risks and protects patients from bone injury.

Multiple studies conducted by Stryker have shown that,Compared with traditional treatment models, this technology (robotic-arm-assisted total knee arthroplasty) offers higher accuracy and precision. Patients experience significant postoperative pain relief, with reduced total morphine consumption and shortened hospital stays.

Addressing the long-standing industry pain point of insufficient precision in orthopedic surgeries, Stryker’s move has undoubtedly pinpointed the crux of the issue, once again positioning the company at the forefront of the industry.

The Mako robotic joint replacement system has not only helped Stryker enter the surgical robotics market and drive rapid growth in its orthopedics business, but has also become the only joint surgery robot approved for marketing in China, successfully opening the door to the Chinese market.

However, Stryker has not ceased its exploration of market demands.To enhance hospital adoption of the Mako system, Stryker has integrated the Mako robotic-arm assisted surgery platform with its existing joint implant portfolio, creating a comprehensive solution to facilitate clinical use. Furthermore, Stryker has developed two dedicated surgical protocols centered around the Mako robotic system: one for hip arthroplasty and another for knee arthroplasty. As one of the “Big Three” in orthopedics, Stryker has implemented a well-rounded product strategy.

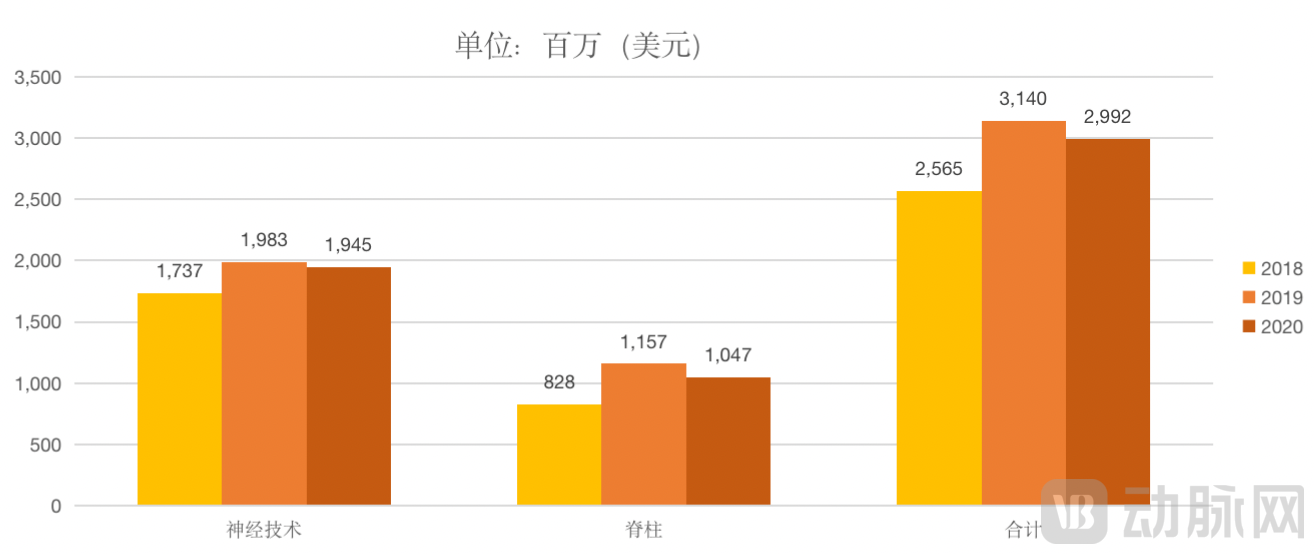

Looking at Stryker’s Neurotechnology and Spine segment, which accounts for 21% of total sales, the company’s financial report shows that in 2019, net sales in Neurotechnology and Spine grew by 19.2%. Compared with Orthopaedics (net sales growth of 5.2%) and MedSurg (net sales growth of 8.8%), the Neurotechnology and Spine business had the highest revenue contribution.

Meanwhile, sales revenue in this business segment has fluctuated over the past three years.In 2019, sales in Stryker’s Neurotechnology and Spine segments rose significantly, followed by a slight decline in 2020.

Neurology and Spine Sales Revenue Share

In fact, Stryker's Neurotechnology and Spine business segments have long faced bottlenecks.From 2013 to 2017, Stryker’s Spine division saw modest revenue growth with a slowing pace. According to its financial statements, the spine business continued to decline in 2018 before experiencing a significant rebound in 2019.

Faced with this dilemma, Stryker continues to breathe new life into its spine business through mergers and acquisitions.

In 2018,Stryker Takes Another Step to Revitalize Its Struggling Spine Business by Acquiring K2M, a Manufacturer of Minimally Invasive Spinal Products

Compared with giants such as Johnson & Johnson and Stryker, K2M appears relatively young in the orthopedic field, having entered the spine sector only in 2004. Nevertheless, its growth has been remarkably rapid. Leveraging its leadership in 3D printing technology, K2M not only boasts a robust product portfolio spanning complex spinal implants, minimally invasive surgical solutions, and products for degenerative spinal conditions, but also launches 10 to 12 new products annually. Prior to its acquisition by Stryker, the company had secured FDA approval for 10 of its products.

Stryker Scores Another Win, Revitalizing Its Underperforming Spine Business Through the Acquisition of K2M.

Stryker has demonstrated remarkable strategic clarity in the orthopedics sector. Although its orthopedic product portfolio is already comprehensive and competitive, the company remains acutely aware of its weaknesses. It has consistently leveraged mergers and acquisitions to integrate resources, thereby consolidating its industry leadership while mitigating competitive pressures.

Based on its performance and relevant financial data,, M&A appears to have become a lifeline for Stryker’s development, whereas its organic growth has appeared rather weak in recent years.Perhaps for Stryker, mergers and acquisitions are not just about expansion, but survival.

Stryker’s Rise to Orthopedic Giant Is No Accident. Although the orthopedics sector has grown increasingly competitive, with innovative enterprises continuously entering the market, and its business growth has slowed amid the impact of the pandemic, none of this has shaken Stryker’s dominant position.How Did Stryker Successfully Break Through in the Face of Adversity and Lead the Industry for Years? Its Market Strategy Deserves In-Depth Analysis.

First, Stryker entered the market early, and its core products, such as the Circ-O-Lectric bed, held a near-monopoly in the early market.The competitive advantages of this technology have enabled the company to rapidly capture market share, driving continuous growth in sales. Meanwhile, the accumulation of technological expertise and resources has laid a solid foundation for Stryker’s future development.

Second, after a period of steady expansion, Stryker launched its initial public offering (IPO) plan.Following its IPO, Stryker began to absorb external resources through acquisitions, rapidly expanding its business scope.It was in 1979 that Stryker’s acquisition of Osteonics helped it enter the orthopedic implant market.Subsequently, Stryker has gradually deepened its presence in niche markets through corporate acquisitions.Its product portfolio continues to expand,Sales revenue also doubled in line with this strategy.

Third, after establishing its corporate product framework, Stryker continues to closely monitor emerging trends in the industry.Along with the development of technologies such as 3D printing, surgical robots, and artificial intelligence,Stryker bolsters its business portfolio through strategic acquisitions to maintain corporate competitiveness. Meanwhile, the company integrates its proprietary technologies with innovative solutions to offer comprehensive packages, thereby creating greater market opportunities.。

Fourth, although Stryker’s orthopedics business is widely recognized as its “flagship” offering in the industry, the company’s strategic portfolio extends well beyond this segment.As evident from its product data, Stryker’s business scope also encompasses medical surgical, neurotechnology, and spine segments.Stryker’s extensive business lines have provided greater opportunities for trial-and-error innovation and expansion, while also enhancing its competitiveness within the industry.

Finally, in terms of market expansion, Stryker has not limited itself to the U.S. market but has also entered overseas markets such as China, Japan, and Latin America.

Through a systematic review and analysis, it is evident that Stryker possessed inherent advantages from its initial entry into the medical field. In its early stages, Homer Stryker’s profound insight into market pain points, combined with technological leadership, enabled the company to successfully capture the market through its innovations and rapidly accumulate resources, laying a solid foundation for subsequent growth.

Following its successful IPO, mergers and acquisitions (M&A) became Stryker’s primary strategy. Through M&A, Stryker expanded into various niche segments, thereby enriching its product portfolio. The extensive business lines across its three major divisions—Medical, Orthopaedics, and Neurotechnology & Spine—mutually reinforce one another, providing Stryker with diversified revenue streams, enhanced competitiveness, and greater growth opportunities, while also offering additional buffer space for its development.

However, Stryker’s ascent to the throne of industry giant is not solely attributable to this strategic success. The company possesses unique insight and strategy when it comes to acquisitions, where accurately gauging market trends and thoroughly understanding the target companies are paramount.

For Stryker, mergers and acquisitions (M&A) are not only a matter of survival but also key to maintaining corporate competitiveness. The types and sizes of companies it acquires closely align with emerging industry trends. Furthermore, post-acquisition, Stryker integrates the acquired entities with its own operations to create unique value propositions and rapidly capture market share.

Stryker’s rise to become an orthopedic giant stems from its inherent strengths and strategic advantages, offering valuable insights for other companies in the orthopedic market.

For “giants,” mergers and acquisitions may be an inevitable path.Achieving rapid growth and strategic pivots through acquisitions to overcome internal challenges is a viable approach. However, it is crucial to identify the right inflection points, avoid M&A pitfalls, integrate proprietary technologies with innovative solutions, and cultivate endogenous growth capabilities. Meanwhile, staying attuned to emerging market trends, enriching the product pipeline, and expanding into overseas markets are also indispensable.

For “new entrants”,InCorporate growth requires in-depth thinking and strategic planning.First, it is essential to identify a company’s core competitive advantages, leveraging innovation to differentiate from homogeneous competitors, thereby enabling rapid market penetration and resource accumulation. Second, cultivating market acumen by conducting in-depth market assessments aligned with the company’s developmental trajectory to formulate clear strategies is also key to facilitating rapid growth.

As population aging intensifies and policies such as the “Notice on the Standards for Establishing National Orthopedic Medical Centers and National Regional Orthopedic Medical Centers” are released, the orthopedics industry is leading a cohort of enterprises into a “golden age.”According to relevant data, in 2018, the market shares of domestic companies such as Double Medical, Kinetic Medical, and Zhengtian reached 2.86%, 1.83%, and 1.53%, respectively.

Among them, Double Medical specializes in orthopedics, neurosurgery, minimally invasive surgery, and spinal implants, having successively obtained professional certifications including FDA clearance, CE marking, ISO 13485, and GMP compliance. KaiLiTai has established a multi-segment product portfolio of high-value orthopedic consumables centered on spine, trauma, and joint minimally invasive products, and has sequentially secured EU CE certification, US FDA 510(k) clearance, and approval from Japan’s Ministry of Health, Labour and Welfare (MHLW). Zhengtian is primarily engaged in the R&D, manufacturing, distribution, and servicing of orthopedic medical devices, with substantial business operations in the fields of joints, spine, and trauma.

Although Chinese domestic companies in the orthopedics industry have become increasingly competitive as technology continues to advance, how they can break through their current growth trajectory and achieve import substitution remains a question worthy of consideration.