Unaffordable Mice and Unavailable Monkeys: How Long Will This Red-Hot Sector Stay Hot?

The traditional industry, which has long served as a behind-the-scenes enabler for CROs, has finally found itself at the center of capital market attention.

In less than two years, several well-known suppliers of model mice in the industry—Namocell, GemPharmatech, and Biocytogen—have successively entered the capital markets. When including Joinn Laboratories, a CRO characterized by its provision of experimental large animals that had already gone public earlier, model animals have undoubtedly become a significant force in the capital markets. Top-tier investment firms such as Hillhouse Capital, Sequoia Capital, CDH Investments, CPE Source, and OrbiMed have precisely capitalized on this wave of opportunities. Interestingly, the model animal sector is equally hot in the primary market. Model animal companies that started slightly later, such as Cyagen Biosciences, Zhonghong Boyuan, and Sinogene, have sequentially announced substantial financing rounds amounting to hundreds of millions of yuan, leaving many investors regretting their failure to secure a stake in time.

Behind this lies an explosive surge in market demand that can no longer be described merely as inflationary. According to a marketing professional in Beijing specializing in the sales of model animals, during the most intense early months of COVID-19 vaccine research and development, qualified off-the-shelf mice were unavailable even in China, forcing numerous studies to halt while awaiting mouse breeding. Recently, the R&D dilemma characterized by unit prices nearing 100,000 yuan yet extreme scarcity of monkeys has sparked heated discussion on social media platforms such as WeChat Moments. “An increasing number of research institutions are beginning to build their own animal facilities; however, equipment adaptation, environmental commissioning, and animal breeding all require time. Therefore, the supply-demand imbalance is likely to persist for some time.”

As innovative drugs such as novel antibody therapies, gene therapies, and cell therapies are intensively advanced into late-stage development, the unit prices of large model animals, including experimental monkeys and dogs, have multiplied several-fold since 2020. At the recently concluded Chongqing Smart China Expo, the Model Animal Center was highlighted as a major project and signed for establishment in Banan District, underscoring the surging momentum in the model animal industry.

Model organisms may appear simple, but ensuring their high-quality and consistent supply is by no means an easy task.

Model animals refer to artificially bred animals that have been genetically engineered, physically or chemically induced, or spontaneously exhibit certain diseases, genetic traits, or biological characteristics, and are used to elucidate disease pathogenesis, identify potential therapeutic targets, or validate the safety and efficacy of new drugs and novel treatment regimens. From a definitional perspective, technological modification and artificial breeding are the key elements in the development of model animals.

In addition to the animals' own breeding cycles, limited technical capabilities and the complexity of training animals also contribute to the current shortage of supply for model animals.

On the one hand, implementing technological modifications in animals is a complex systems engineering endeavor. This requires starting with the two iterations of model animal technology. The earliest approach was transgenic technology, which emerged in the 1970s and involves using DNA recombination to combine DNA from different genomes or introduce exogenous DNA into the recipient genome. However, transgenic technology cannot precisely control the insertion site and copy number, leading to the emergence of ES cell targeting technology more than a decade later. Nevertheless, ES cell targeting is time-consuming, inefficient, and costly. It requires first screening for positive ES cells, injecting them into mouse blastocysts, preliminarily assessing chimerism based on coat color, and then breeding with wild-type mice to obtain black-coated offspring.

If the entire process proceeds smoothly, it takes approximately 10 months; however, if any intermediate step yields unsatisfactory results, the cultivation period must be extended by 2–3 months. Subsequently, new site-specific gene editing technologies emerged, such as zinc-finger nuclease (ZFN) technology and transcription activator-like effector nuclease (TALEN) technology, but their widespread application remains limited due to issues such as cumbersome operational procedures.

Emerging in 2012, CRISPR technology represents the third generation of techniques for generating model animals. It is characterized by ease of operation, lower costs, and the capability for high-throughput, precise genome editing. Genetically edited animals produced via CRISPR can meet the complex requirements of various experimental studies. Previously complex methodologies, such as the Cre-loxP system, Tet-On/Off system, and site-directed mutagenesis, have become widely applicable, thereby propelling the model animal industry into a phase of rapid development.

Currently, CRISPR, embryonic stem (ES) cell targeting, and microinjection are the most prevalent technologies, accounting for the generation of nearly 70% of model animals. Major domestic suppliers of small model animals, including Vital River, GemPharmatech, Shanghai Model Organisms, Cyagen Biosciences, and Biocytogen, primarily rely on these technologies to provide model mice. Meanwhile, as bottlenecks in the production of model monkeys remain difficult to overcome in the short term, large animals such as dogs and pigs genetically engineered via CRISPR technology are increasingly coming into researchers’ focus.

On the other hand, the artificial breeding of model animals is subject to stringent quality control standards. Given the critical importance of model animals to the reliability, reproducibility, and uniformity of final experimental results, a high-quality colony must adhere to strict controls over innate genetic traits, postnatal breeding conditions, microbial and parasitic status, nutritional requirements, and environmental factors. This entails a series of control and validation measures, collectively known within the industry as the Animal Facility Management System.

For most model animal suppliers, the animal facility management system comprises two major components: hardware and software. On the hardware side, there are high technical barriers to everything from site selection and renovation of animal facilities to the installation of four-stage filtration systems, full fresh-air ventilation modes, and biosafety-grade individually ventilated caging (IVC) systems; it typically takes at least one year to fully equip these facilities. On the software side, establishing robust and consistently operational processes—such as training for technical staff, oversight by area and facility managers, veterinary inspection protocols, supplier audits, quarantine of newly arrived animals, and monitoring of breeding colonies—poses significant challenges to the comprehensive capabilities of model animal suppliers.

In recent years, as the scale of services has continued to expand, domestic model organism companies have been strengthening their capabilities in animal facility management. For instance, Shanghai Model Organisms Center Inc. (Shanghai Biomodel) has established a state-of-the-art “Mouse Hospital.” Equipped with advanced instruments such as hematology and biochemistry analyzers, metabolic cages, in vivo mouse imaging systems, micro-CT scanners, and flow cytometers, the facility enables comprehensive testing of mice, including complete blood counts, blood biochemical parameters, metabolic indicators, and behavioral metrics. This allows clients to obtain timely analysis of experimental samples and mouse phenotypes. Furthermore, the Association for Assessment and Accreditation of Laboratory Animal Care International (AAALAC International) offers specialized AAALAC accreditation to enhance the standardization of animal facility management.

Moreover, Dr. Liu Dan, Partner at CDH VGC, told VCBeat that the greatest market demand and most pronounced shortage currently lie in high-end strains of laboratory mice that require complex genetic editing and breeding, such as humanized mice, immunodeficient mice, and specific disease mouse models (e.g., Alzheimer’s disease, non-alcoholic fatty liver disease). In contrast, the supply of basic mouse strains is relatively sufficient. However, the development, breeding, quality control, and delivery of high-end mouse strains require a longer timeframe. For instance, the Alzheimer’s disease mouse model developed by GemPharmatech has a research and development cycle as long as three years due to its high level of innovation.

Thus, it is evident that the technical and experiential barriers to entry in the model organism industry are by no means low. Consequently, despite rapidly growing market demand, most model organism companies are striving to expand production capacity, while users are also attempting to build in-house capabilities; strengthening the supply side of the model organism sector cannot be achieved overnight. In other words, the bullet that ignited the surge in demand for the model organism industry will continue its flight for some time. According to estimates provided by industry practitioners to VCBeat, it will take at least another 2–3 years for model organism production capacity to reach a level that barely meets market demand.

Humans began modifying mammals in laboratories to test hypotheses over a century ago.

The earliest homozygous allele mice were obtained through inbreeding in the laboratory by a professor at Harvard University in the United States. In the last century, with the invention and widespread application of antibiotics and vaccines, diseases such as cardiovascular disease and cancer replaced severe infectious diseases as the main causes affecting human health and mortality, thereby becoming the focus of medical research. Genetically modified model animals have rapidly developed in these hot areas. According to statistics, more than half of the current model animals are used in tumor immunology research, followed by metabolic diseases and neurological disorders. For over a century, rodents (such as rats, mice, hamsters, etc.), non-primates (such as rhesus monkeys), dogs, rabbits, zebrafish, and others have been widely used in experiments for basic science, clinical medicine, and new drug development.

Of course, the world’s most adept player in the field of laboratory animal models is Charles River Laboratories, which started out by acquiring farms with thousands of mouse cages. Leveraging its outstanding capabilities in drug safety evaluation, Charles River has risen to become one of the world’s leading CROs and even once considered acquiring WuXi AppTec’s subsidiary, WuXi Kongde (WuXi Biologics’ former entity or related party, note: contextually likely refers to WuXi AppTec’s preclinical division or a specific entity known as WuXi Kongde). To date, Charles River Laboratories remains the largest supplier of laboratory animal models, controlling more than 80% of the global market.

In China, the model organism industry has undergone a long journey from behind the scenes to the forefront. In its early stages, demand for model organisms was primarily concentrated within research institutes engaged in basic scientific research. Because the validation of underlying mechanisms was relatively straightforward and animal model construction mainly relied on simply modified mice, fragmented and singular demands resulted in slow industry growth. Consequently, the largest model organism companies in China today include domestic branches of overseas giants, such as Vital River Laboratories (a subsidiary of Charles River Laboratories), as well as startups founded by university professors who ventured into the commercial sector. For example, GemPharmatech was established by Professor Gao Xiang from the Model Animal Research Institute of Nanjing University, while Shanghai Biomodel Organism Science & Technology Development Co., Ltd. was founded by Professor Fei Jian from the Shanghai Research Center for Model Organisms. To this day, these companies remain the primary suppliers of gene-edited mice, rats, and cell lines for scientific research in China.

However, for the most part, model animal services represent a business segment that tends to diminish in strategic importance as CROs scale up and strengthen their market position. Objectively, model animals constitute only a small fraction of the drug development process. In earlier periods when requirements for animal models were relatively simple, well-resourced pharmaceutical companies could meet these needs by establishing in-house animal facilities, meaning the level of specialization was insufficient to support the formation of a complete industry. Subjectively, CROs need to grow; as they advance their product development and accumulate technical expertise, they must extend downstream to build competitive barriers.

Around 2015, with the rise of original innovative drugs and novel therapies, coupled with a continuous increase in clinical trial failure rates, the demand for more complex animal models emerged, fundamentally altering the underlying logic of the model organism industry. Specifically, preclinical studies increasingly require validation using mice with humanized targets or humanized immune systems. In particular, there has been explosive growth in the use of mice humanized for immune checkpoints, which are widely employed in the field of tumor immunology, and mice humanized for cytokines, which are frequently used in research on autoimmune diseases. Moreover, due to the growing shortage and limited availability of large experimental animals, mouse models have been assigned additional roles in efficacy evaluation. The trend toward more complex genetic editing in mice has significantly increased the average revenue per customer, thereby elevating the position of the model organism industry within the broader supply chain.

Starting in 2015, China’s rapidly expanding model animal industry experienced several years of homogeneous competition. This competitive landscape drove the price of CRISPR-based gene-edited model animals down to just over one-third of their original levels, eliminating many companies with weaker comprehensive capabilities and resulting in a more concentrated market structure.

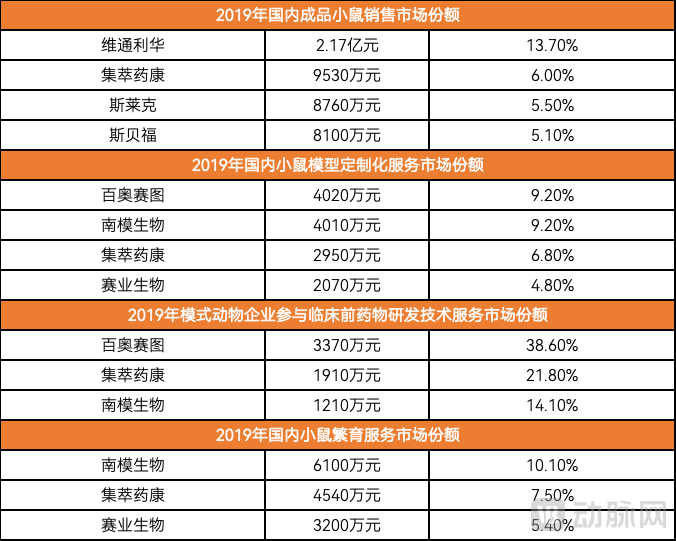

(Data source: GemPharmatech's prospectus)

According to 2019 statistical data, in the four major segments of the model animal market—namely, ready-made mice, customized mice, CRO services, and mouse breeding services—the leading companies collectively held a market share exceeding 20%. Among these, in the relatively newer CRO services market, the competitive advantage of leading enterprises such as Biocytogen, GemPharmatech, and Shanghai Model Organisms Center was most pronounced, with their combined market share approaching 80%.

However, as a lucrative business with gross margins of at least 60%, the model animal industry has seen intense competition among leading players vying for market share. For these top-tier companies, the primary tools for building competitive barriers are the diversity of mouse strains, the stability of mouse quality, and the speed of capacity expansion. Nearly every company is striving to expand its production capacity, pushing their capabilities to the limit in a synchronized effort.

For example, with a deep understanding of the genetic code of every gene in miceGemPharmatech, through its Spot Mouse Program, has rapidly expanded its portfolio of commercially available mouse strains to over 20,000. Prior to delivery, the company performs sequencing on offspring to verify genetic variants, ensuring model stability. Meanwhile, GemPharmatech has swiftly established subsidiaries in Changzhou and Guangzhou to leverage increased production capacity and meet growing market demand.Cyagen Biosciences pioneered a relatively aggressive market strategy within the industry, rapidly capturing the Beijing market vacated by Biocytogen and establishing an animal center in Gu’an, Hebei. Meanwhile, Biocytogen has extended its operations further downstream, transforming into a biotechnology company focused on the development of novel antibody-based drugs, and achieving remarkable success with its “Thousand Mice, Ten Thousand Antibodies” project.

With prices skyrocketing on one hand and aggressive market expansion on the other, the market ceiling for model mice remains surprisingly low.

According to the prospectus of Shanghai Model Organisms Center, Inc., the market size for model mice in China grew from RMB 1 billion in 2015 to RMB 3.3 billion in 2019, representing a compound annual growth rate (CAGR) of 34.7%. Driven by the robust development of life sciences research and new drug discovery, this growth trajectory is expected to continue, with the total market size for model mice in China projected to reach RMB 9.8 billion by 2024. However, capital market expectations for the model animal industry extend far beyond these figures. Based on estimates derived from historical equity changes disclosed in various companies’ prospectuses, Biocytogen Pharmaceuticals (Beijing) Co., Ltd. is currently valued at RMB 7.8 billion, GemPharmatech Co., Ltd. at RMB 8 billion, and Shanghai Model Organisms Center, Inc. at RMB 10.7 billion.

Therefore, more significant than the capital bubble is the shifting underlying logic of the model organism industry, driven by the fission of the pharmaceutical ecosystem and the fusion of corporate capabilities. For the model organism sector, future opportunities lie in the continuous outward expansion of industry boundaries, underpinned by the fundamental methodologies of model organisms. This industrial expansion can be further categorized into vertical and horizontal dimensions.

Vertical expansion refers to the strategy whereby leading traditional model animal companies extend their operations into upstream and downstream CRO services and new drug development, such as efficacy evaluation and in vitro and in vivo pharmacological services. In its functional efficacy service module, GemPharmatech is already capable of conducting in vivo efficacy studies using various mouse models, including LAG3 humanized, PD1 humanized, TIGIT humanized, and GITR humanized models. The revenue generated from this segment has been increasing year by year as a proportion of total revenue, rising from 5% in 2018 to 12% in 2020, making it the fastest-growing business segment. Furthermore, in its IPO fund allocation plan, GemPharmatech has explicitly stated that it will invest RMB 200 million to build a research, development, and translation platform for real-world animal models.

Notably, Shanghai Model Organisms Center (SMOC) offers more systematic phenotypic analysis services. For instance, it assesses changes in insulin levels in gene-knockout mice under fasting conditions to determine whether the target gene is involved in insulin regulation. It also conducts pharmacodynamic analysis and evaluation, such as establishing subcutaneous tumor models in humanized PD-1 mice and using these tumor-bearing mice to evaluate the anti-tumor efficacy of PD-1 antibody drugs. Additionally, SMOC provides other CRO services, including animal husbandry. Similar to GemPharmatech, SMOC’s CRO business segment has generated a steadily increasing share of revenue, rising from 9.56% in 2017 to 17.57% in the first half of 2020.

Having established its foothold in the market with model organisms, Biocytogen has directly embarked on new drug development. The prospectus reveals that two self-developed monoclonal antibody candidates, YH003 and YH001, have completed Phase II clinical trials and preclinical studies, respectively. Preliminary results from the Phase II clinical trial of YH003 demonstrated favorable safety and efficacy profiles, highlighting its potential to become a best-in-class humanized IgG2 agonistic monoclonal antibody targeting CD40. In preclinical efficacy studies, YH001 outperformed its competitor, ipilimumab (Yervoy).

An industry practitioner told VCBeat that model organism companies with extensive experience and a comprehensive product portfolio possess inherent technical advantages when expanding into CRO services. In the development of certain first-in-class novel drugs, animal models have become the most time-consuming and highest-risk segment of preclinical research; thus, constructing high-quality animal models may well account for half the success of preclinical studies. “The incremental investment required for model organism companies to enter the CRO space is minimal, necessitating only the addition of personnel with structural biology expertise to their technical teams,” the practitioner stated. Perhaps moving beyond the animal facility is simply the inevitable trajectory for model organism enterprises.

Horizontal expansion refers to the trend where emerging enterprises with strong technical and financial capabilities are incorporating a wider variety of animal species, such as cats, dogs, and pigs, into preclinical drug research models. This segment currently attracts the most intensive investment and financing activity within the model organism industry. An investor told VCBeat that their fund is committed to investing in model organism projects, noting that large animal models represent the subsector with the greatest growth potential and relatively reasonable valuations at present.

VCBeat has noted that pigs, dogs, and cats are currently the most frequently used animals in preclinical drug research. Among these, Sinogene Biotechnology, which has been deeply engaged in pet cloning for many years, has established China’s first gene-edited disease model dog—the APOE model—following its strategic focus on canine models, and has applied this model to clinical research. However, practitioners involved in large-animal model development have told VCBeat that, compared with small-animal models such as mice and rats, the use of large animals as model organisms still faces numerous technical challenges, including long breeding cycles, low and unpredictable fertility rates, more complex genetic backgrounds, markedly different husbandry environments, and poor cooperation during experimental procedures. “Furthermore, using monkeys, dogs, cats, and other animals for experimentation poses a short-term challenge to public perception,” another practitioner told VCBeat. “Most people would find it difficult to accept the sacrifice of hundreds of these animals in experiments, which undoubtedly constitutes an obstacle to industry development.”

Admittedly, the doubling of product prices and intense capital attention have given the model animal industry a hint of overheating. But beneath the bubble, we should focus more on the underlying logic driving the growth of this industry, which has long played a supporting role.