Time to Rethink Valuation Models for Private Healthcare Service Companies

In recent years, driven by multiple factors such as policy support, industry development, and consumption upgrades, private medical services have begun to assume increasingly important responsibilities and social functions.

However, with the recent successive introduction of regulatory policies, new doubts have emerged in the capital market regarding private medical services: Given that medical services possess a strong public welfare attribute and the public medical service system dominates the sector, how should private medical services be positioned? And how should their value be assessed?

Taihe Capital believes that pursuing equity will be the main direction of future reforms, but private healthcare will undoubtedly play an increasingly important role in China’s healthcare system.Unlike the "demand determines supply" logic prevalent in other industries, the healthcare services sector is a classic example of "supply determining demand": while the public's need for medical and health services is virtually unlimited, the core resource of physicians capable of providing diagnosis and treatment is limited, resulting in a perpetual scarcity of high-quality healthcare services.

The “impossible trinity” of healthcare services—namely, the inability to simultaneously satisfy the three core elements of “broad coverage/accessibility,” “economic cost,” and “service quality.” Public healthcare systems must ensure accessibility while striving to minimize costs, thereby inevitably compromising quality to some extent. Consequently, the demand for higher-quality medical services must be met by the private healthcare sector.

On one hand, private healthcare services are becoming increasingly important; on the other hand, there is still no consensus in the capital market regarding the valuation of healthcare service assets. Against this broader backdrop and supply-demand structure, the value of private healthcare institutions needs to be reexamined, and the value of “people” within the healthcare service sector—often overlooked in the past—should also be reassessed.

Core Viewpoints of This Article:

The healthcare services industry features““Asset-Heavy” + “Operation-Intensive”dual attributes, which pose significant difficulties and challenges to traditional valuation systems; based on past financing and acquisition cases, the majority of the premium for healthcare service assets stems from human capital;

When valuing healthcare service enterprises, it is essential to recognize the value of human capital, as professional services delivered by this capital generate economic value; furthermore, scalable expansion can also be achieved through technological and financial leverage.

Effective leverage is a prerequisite for achieving scale expansion, including:Prioritize organizational management and build a talent pipeline; leverage technological means to enhance digitalization; make rational use of external financing and equity incentives for partners.

M&A integration capabilities will become the cornerstone of expansion; leading enterprises need to build robust middle- and back-office capabilities.

Advice for Entrepreneurs: ImplementationRobust talent pipeline development, establishment of multi-specialty rather than single-specialty practices, and construction of a pyramid-shaped institutional network, digital empowerment can effectively reduce labor costs and improve the efficiency of diagnostic and treatment services.

There are several common practices currently used in the market to assess a company’s value. For instance, multiples such as P/S (Price-to-Sales), P/E (Price-to-Earnings), and EV/EBITDA (Enterprise Value-to-Earnings Before Interest, Taxes, Depreciation, and Amortization) are frequently employed to value publicly listed companies. On one hand, these multiples help determine whether a company is overvalued or undervalued; on the other hand, they also serve as reference points for valuing private companies in the primary market. Many enterprises rely on the valuation benchmarks of their publicly listed peers within the same industry when raising capital.

However, for the healthcare services industry, valuing a privately held company is not as straightforward as “simply applying multiples.”

The chart below shows the comparable multiples (EV/EBITDA, i.e., Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization, a widely used corporate valuation metric) of major listed healthcare service companies in the secondary market for Hong Kong stocks. It can be seen that there are huge differences in comparable multiples among healthcare service enterprises: some are as high as nearly 400 times (Kangjian International Medical), while others are even lower than 10 times (Honghe Renai Hospital). This difference is not only due to different markets and tracks, but also exists among similar types of enterprises (such as C-MER Eye Care with 219 times and Zhaoju Eye Care with 31 times).

The types of healthcare service institutions are complex, with significant variations in business and revenue models. This leads to divergent market valuations for companies with different operational characteristics and at different stages of development. Generally, comparable valuation multiples for listed companies within a given industry (such as industrial manufacturing or consumer goods) tend to fluctuate within a specific range, maintaining overall equilibrium without excessive disparity. However, the current variation in comparable multiples among publicly listed healthcare service companies far exceeds that observed in other industries.

At its core, the secondary market has yet to reach a consensus on “how to value healthcare service assets.”This is a pain point in the healthcare services industry and a common dilemma currently faced by startups within the sector: the lack of consensus on market valuation of companies inevitably hinders the development of early-stage ventures.

This approach is not viable; instead, we can take an alternative route by extrapolating from typical M&A cases that have already occurred in the primary market, which may help identify the core value of healthcare service companies. Compared with the approach of “inferring primary market dynamics from the secondary market,” the key differences in the comparable M&A transaction perspective include:

▶ The establishment of transaction consideration in the primary market should not only take into account the seller’s business foundation and growth potential, but also give greater weight to the buyer’s transaction objectives; the premium may arise from both parties.

▶ The scope and qualifications of acquisition targets in the primary market vary significantly. Under the current regulatory environment, many high-quality private companies are unable to pursue public listings and capitalization. Therefore, evaluating all targets from an M&A perspective can provide a relatively objective reflection of the overall market conditions, avoiding the "survivorship bias" inherent in inferring primary market valuations from secondary market data (listed companies are inherently industry leaders; using their valuation multiples to back-calculate values for companies still in developmental stages would likely yield overly "optimistic" results).

▶ Behind every M&A deal lies protracted due diligence and multi-party negotiations. Compared with the fast-changing secondary market, the final outcome of an M&A transaction more accurately reflects the market’s long-term valuation consensus on the company.

Taihe has reviewed the larger and more typical M&A transaction cases from the past few years:

As can be seen, in these typical M&A cases, the transaction premium accounts for as high as 70%, 80%, or even over 90% of the total transaction value—this is the most significant difference between the healthcare services industry and other sectors: rather than focusing on the tangible net asset value of the acquisition target, buyers place greater emphasis on the company’s “intangible” value and are willing to pay a substantial premium for such “intangible value.”

To identify new methods for value assessment in healthcare service institutions, it is essential first to clarify what constitutes these “intangible values” and how we can accurately evaluate them.

For M&A cases in general industries, these “intangible values” are ultimately recorded as “goodwill” under standard accounting practices. In most cases, goodwill represents the premium that the acquirer is willing to pay for the target company. This premium may be attributable to the target’s long-standing history and prestigious reputation within the industry, or to its control over certain specialized factors of production, which grant it a significant competitive advantage over its peers.

In short, these “intangible values” are more akin to describing “brand value.”

However, the healthcare services industry is a highly specialized sector. Assets in this industry possess the dual characteristics of being “capital-intensive” and “operationally intensive.” In addition to tangible assets, there exists a critical component of “human capital” that, while vital, has not yet been effectively quantified.

In the industrial era, physical capital—represented by land, buildings, and equipment—was the most critical factor of production. In contrast, in the knowledge economy, human capital has become a scarcer and more vital factor of production due to its possession of advanced knowledge, skills, and experience. Typical enterprises include consulting firms, law firms, and investment banks.

This is especially true in the healthcare services sector, where physical assets continue to play a significant role,However, human capital, represented by physician resources, carries greater weight in value assessment and commands higher premium levels for enterprises.

Taihe believes that, based on past financing and acquisition cases, the vast majority of the premium in the value of healthcare service assets, beyond tangible assets, stems from human capital. Therefore, we propose the following equation:

Healthcare Service Asset Value = Physical Assets + Human Capital

For healthcare service providers, tangible assets include land, buildings, equipment, and leasehold improvements. Traditional valuation models tend to assess value and determine price based on the monetization of these tangible assets, specifically by using historical cost or replacement cost. While this approach aligns with accounting cost measurement principles and simplifies calculations, cost does not equate to value. Much like how a real estate developer’s costs for acquiring land and constructing buildings do not necessarily reflect the final selling price of the properties, the same principle applies here.

Beyond physical assets, it is professional service providers such as physicians that endow healthcare service enterprises with greater value.

In the healthcare services industry, most products and services are delivered by physicians, physician assistants, nurses, and other professionals. During laboratory testing, diagnosis, and treatment, these skilled practitioners leverage their expertise and experience to address patients’ health concerns, thereby creating value.

In the typical M&A cases mentioned earlier, the acquisition premium beyond net assets generally averages around 80%. We tend to define the value of this portion asHuman Capital.

Unlike physical capital, human capital is a special form of capital because human beings possess initiative and can continuously accumulate experience and knowledge. Meanwhile, division of labor and collaboration within an organization can create network effects among individuals, enabling self-value enhancement and generating returns that are multiples of the initial investment.

Simply put, human capital is defined as the sum of knowledge, skills, patents, experience, and influence that generate economic value.

Unlike valuation based on physical capital, which calculates historical costs from an input perspective, valuation based on human capital calculates future returns from an output perspective, as commercial value is generated by people.

Physician resources are the scarcest factor among healthcare service assets. The valuation of such scarce factors should consider their opportunity costs and newly generated profits. Human capital represents the labor compensation for embodied professional services; therefore, the valuation of human capital should be calculated by discounting future wage earnings to their present value.

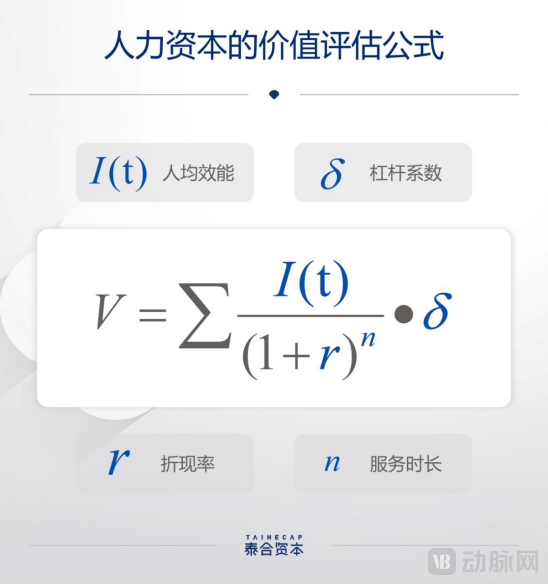

How is it calculated specifically? Taihe believes that this formula can provide a relatively fair assessment of the human capital value of healthcare service enterprises:

Per Capita Efficiency

Per capita efficiency can be narrowly understood as per capita output, i.e., the ratio of total operating revenue to the corresponding total headcount, and is commonly used to measure the labor productivity of a production unit.

However, healthcare services possess several distinct characteristics: the industry is highly non-standardized; it carries significant social attributes; and physicians, as the core factor of production, face specific learning curves within their respective departments and subspecialties. Therefore, we need to evaluate physicians’ expected productivity on an individual basis, focusing on average daily patient volume and personal growth expectations. Generally, higher physician productivity correlates with greater daily patient volumes, thereby increasing the corresponding value of human capital.

Discount Rate

Similar to the discount rate used in discounted cash flow calculations, the discount rate here represents the rate at which per capita productivity over the projected future period is converted into present value.

Service Duration

Due to the high degree of non-standardization in medical services, physicians gradually build their personal brands during service delivery, leading to a phenomenon where patients remain loyal to the individual doctor rather than the medical institution. Therefore, the duration of service not only reflects the fulfillment period of physicians’ labor contracts but also demonstrates the organizational management capabilities of medical institutions from the perspective of workforce mobility. For this factor, the core metric to focus on is the employee turnover rate.

For an industry that relies on human professionals to deliver specialized services, achieving scalable expansion is a core concern for both practitioners and investors.

As can be seen from the above formula, personnel efficiency capacity, discount rate, and service period can roughly outline several dimensions of human capital. However, for chain medical service institutions aiming for scale, relying on human capital to achieve scalable expansion requires leveraging levers to iterate from linear growth to exponential growth. Leverage coefficients come from three categories: labor leverage, technology leverage, and capital leverage.

Leverage Coefficient (Delta, δ) = Labor Leverage × Technology Leverage × Capital Leverage

Labor Leverage: The proportion of time invested by professionals in different positions per unit of service

A complete clinical care journey encompasses appointment scheduling, check-in upon arrival, initial physician consultation, laboratory and diagnostic testing, diagnosis and treatment, payment processing, and follow-up visits. The total time required for the entire process is considered as 100%. Physicians are primarily involved in three key stages—initial consultation, diagnosis and treatment, and follow-up visits—which collectively account for up to 40% of the total time. The remaining 60% is typically handled by nurses, physician assistants, administrative staff, or operational support personnel.

By establishing a well-structured talent pipeline, enterprises can enhance specialized division of labor and operational collaboration, thereby minimizing physicians’ capacity waste due to non-clinical tasks and idle waiting time. This allows physicians to focus more on patient care, achieving a two- to threefold increase in daily diagnostic and treatment efficiency, and ultimately enabling more comprehensive and higher-quality coverage of the patient population.

Technical Leverage: Efficiency Gains in the Same Diagnostic and Treatment Service Driven by Technological Iteration

In traditional diagnosis and treatment, the process primarily relies on physicians’ experience and repetitive manual labor. Today, with technological innovations, intelligent hardware and software have been widely adopted in the healthcare sector, including assistive robots and clinical decision support systems. These technologies enhance diagnostic accuracy and improve efficiency across the entire care pathway. To some extent, they also compensate for the limited experience of junior and mid-level physicians, shorten the clinical learning curve, and elevate the overall service capacity of medical teams.

Let us take clear aligner therapy as an example. Traditional orthodontic treatment relies on manual judgment and intervention, with each consultation lasting approximately 40 minutes and management based entirely on the clinician’s tactile feedback and experience. On one hand, the heavy reliance on experience creates implicit barriers related to seniority and case volume, contributing to a significant shortage of orthodontists. On the other hand, the lengthy treatment workflow, coupled with the lack of quantifiable and visualizable data, creates communication barriers between doctors and patients, thereby reducing patient compliance and satisfaction with care.

Through digital enhancement, existing clear aligner technology can reduce the time per clinical session to approximately 5–10 minutes, equivalent to an eightfold increase in treatment efficiency. Furthermore, the availability of more immediate imaging data and visual analytics facilitates smoother communication between doctors and patients.

Capital Leverage: Primarily categorized into three types: external financing, internal equity incentives, and inorganic mergers/acquisitions.

▶ External financing (including equity and debt): drives improvement in asset return efficiency

The healthcare services industry requires substantial upfront investment, making it difficult to achieve rapid scale expansion solely through internal cash flow. Meanwhile, the development cycle for healthcare service assets is lengthy, typically taking 8–10 years to reach a certain scale. Companies can enhance capital turnover efficiency through external equity or debt financing, leveraging financial instruments to accelerate growth and thereby achieve rapid scaling.

▶ Internal Equity Incentives: Securing Long-Term Commitment from Physician Partners

ESOP (Employee Stock Ownership Plan) is a mechanism for pricing human capital and enabling participation in the distribution of corporate benefits. In this way, enterprises can replace short-term profit sharing with long-term management rights sharing. From the perspective of physicians, the partnership model itself represents a transformation of production relations, replacing traditional employment relationships with a partnership structure.

Equity incentives possess leverage because the value of equity inherently incorporates expectations for future growth, allowing companies to achieve greater operational cost savings with relatively smaller equity incentive expenditures, thereby resulting in a higher level of leverage. Many chain healthcare service providers adopt a physician partnership model, using long-term equity incentives to retain top-tier physicians over the long haul, rather than relying on short-term performance metrics for rewards and penalties. This approach helps prevent physicians from becoming overly profit-driven and engaging in distorted practices merely to boost short-term revenue.

▶ Inorganic Mergers and Acquisitions: Driving Economies of Scale in Expansion

Traditional healthcare services have relied on the expansion of offline institutional networks to achieve growth, depending entirely on opening new stores or facilities. Each individual store experiences a long ramp-up period, resulting in largely linear growth. However, once a company’s organic growth reaches a certain stage, sustained expansion requires inorganic growth through mergers and acquisitions (M&A) and integration, thereby achieving significant economies of scale and improved operating profits.

For example, offline institutions are highly complex to operate, and most chain medical institutions receive auxiliary support from their headquarters. For regional chain medical institutions of average scale, the headquarters typically maintains extensive back-office support departments, including IT, HR & Training, Supply Chain, Customer Service, Finance/Tax/Legal, and Marketing & Sales. Routine headquarters operating expenses generally account for 10–15% of the group’s total revenue. These fixed costs can be directly replaced through mergers and acquisitions (M&A) integration with a more efficient management system. As a result, M&A integration can achieve a reduction in operating costs and an increase in operating profits in the short term.

In summary, Taihe believes thatWhether it is investors’ valuation of healthcare services or entrepreneurs’ operational management of medical institutions, human capital should be given greater priority in decision-making.

In terms of specific operations, entrepreneurs can address gaps and weaknesses in their medical service institutions by focusing on the following areas.

Build a Talent Pipeline and Leverage Human Resources Effectively

As previously mentioned, clear delineation of responsibilities and collaboration among physicians, physician assistants, nurses, and administrative support staff across different stages contribute to improved overall process efficiency. Generally, a physician-to-physician assistant/nurse ratio between 1:2.5 and 1:3 is considered reasonable for maximizing operational productivity. An excessively high ratio may lead to ambiguous role definitions and insufficient focus on physicians’ core duties, while an overly low ratio suggests that certain critical processes may not be led by physicians, posing potential risks.

Multi-specialty Setup to Enable Cross-Selling

Multi-department setups are not only applicable to multi-specialty medical service institutions but also to single-specialty providers such as those in medical aesthetics and dentistry. This approach allows for further refinement of service scenarios and target populations (e.g., pediatric dentistry, adult dentistry, with further subdivisions within adult dentistry into implants, orthodontics, and prosthodontics). By focusing on distinct specialized services or specific patient pain points, these institutions can facilitate mutual conversion between departments and patient groups, thereby enhancing user stickiness and reducing customer acquisition costs.

Taking multi-specialty practices as an example, once a trust-based relationship with family users is established within pediatric, obstetric/gynecologic, or internal medicine departments, the conversion of other family members to adult care or consumer healthcare services can be achieved at a lower customer acquisition cost, or even without additional investment. This demonstrates a significant cross-selling effect, especially when compared to the approximately 25% sales expense ratio typical of single-specialty medical service providers.

Tiered Institutional Network Layout to Achieve Tiered Diagnosis and Treatment

From clinics to outpatient departments and then to hospitals, a single clinic or outpatient business model cannot meet the diverse needs of patients at different levels. If healthcare institutions can establish a “pyramid-shaped structural network” within a city, comprising “small-scale hospitals + comprehensive outpatient centers + health clinics,” with each type of entity offering distinct diagnostic and treatment capabilities, and further integrate online and offline services to cover family-based medical care and daily health maintenance within a defined area, they can optimize patient triage and maximize the utilization of medical resources.

For healthcare service providers, the greater challenge lies in selecting appropriate geographic locations and suitable institutional categories, thereby driving patient and consumer flow among their own facilities.

Building a Middle and Back-End System to Effectively Support Business Operations

Beyond clinical expertise, the effective utilization of business operations teams can help healthcare institutions control overall costs. The clinical care process is inherently meticulous; every aspect—from the duration of each step, to individual patient prescriptions, and pre- and post-consultation communications—serves as an entry point for cost control.

Here, “cost” encompasses not only direct material expenses such as pharmaceutical and consumable usage, but also increases in management costs arising from doctor-patient conflicts and overtreatment, as well as reductions in customer acquisition costs driven by patient recognition and word-of-mouth referrals. Therefore, in addition to a professional medical team, specialized management by a business operations team is equally essential.

Technology Empowerment: Achieving Digital Transformation

Finally, institutions should leverage digital technologies to optimize and reshape their service systems, thereby enhancing the overall service capability and efficiency of their outlets.

Technology can deliver many new experiences and services, such as auxiliary diagnostic systems at the front-end of medical care, AI-powered treatment planning support systems, and intelligent medical devices. These innovations help physicians improve efficiency and ensure quality across screening, diagnosis, treatment, and follow-up stages, while also replacing redundant labor through technological iteration, thereby further enhancing the marginal economies of scale in clinic-based services.

In the middle and back-office systems, continuous digital upgrades can achieve a high degree of integration between business and financial systems. As large volumes of continuous data from patient appointments, diagnoses, treatments, and payments accumulate, precise customer profiles can be developed. These accurate customer profiles enhance upstream "sales-driven procurement" capabilities, enabling institutions to more precisely control supply costs and uncover profit margins. They also allow for more precise downstream health management for patients, thereby increasing customer Lifetime Value (LTV) and strengthening customer stickiness.

Author:

Liu Zeyuan

Director, Taihe Capital

Holds a Master’s degree in Economics from the London School of Economics and Political Science. Earned dual bachelor’s degrees in Economics and Finance from Case Western Reserve University in the United States.

Representative cases: Distinct HealthCare, Dongfang Qiyin, United LiGe, and Side Sunshine.

He is primarily responsible for private equity financing and M&A transactions at Taihe Capital in the fields of consumer healthcare and medical technology. Prior to joining Taihe Capital, Mr. Liu worked at iCapital, Accenture, and McKinsey & Company, focusing on private equity financing transactions and strategic consulting services in the healthcare sector.