2021 Internet Hospital Report: Core Trends Revealed Through Analysis of 1,140 Hospitals and In-Depth Surveys of 109 Institutions

Amid the normalization of epidemic prevention and control, online medical resources continue to expand. According to data from the National Health Commission, by June 2021, there were more than 1,600 internet hospitals across China. The emergence of online internet hospitals has been continuously transforming people’s lives, with online medical services gradually expanding beyond initial offerings such as online follow-up consultations and medication delivery. The integration of medical insurance reimbursement has further promoted the utilization of internet hospital services.

As the pandemic accelerates the entry of public internet hospitals into the market, what new changes have emerged in this sector? Following the large-scale involvement of public internet hospitals, how are they managing their operations? What innovative business models have enterprises introduced? And what changes might we expect in the future?

VCBeat and Eggshell Research Institute, in collaboration with the Yinchuan Internet Plus Healthcare Association, jointly released the "2021 Internet Hospital Report." The report conducted a questionnaire survey of 109 internet hospitals and analyzed data from 1,140 internet hospitals. Starting from the perspective that internet hospitals are gradually transitioning from peripheral tools to the core of healthcare, the study examines their service models and key construction points, aiming to provide new references for the industry.

According to data from the National Health Commission, as of June 2021, there were more than 1,600 internet hospitals across China. From the first internet hospital that emerged in 2014 to the current total of over 1,600, policy development has undergone new changes. Meanwhile, as internet hospitals are being launched at an accelerated pace, the environment for online medical services is also evolving.

From Directional to Operational: Local Regions Enter a New Policy Cycle

As of July 2021, a total of 150 policies related to internet hospitals had been issued nationwide in China (excluding Yinchuan; all others were national- and provincial-level policies), with the policy framework becoming increasingly comprehensive.

However, based on the rollout of policies across provinces in the three major categories—guidance, regulation, and payment—the industry has not yet entered a stable phase and remains in an expansion stage. Currently, some provinces have not yet issued detailed regulatory or payment policies, primarily relying on the relevant regulations of the National Health Commission (NHC) or the National Healthcare Security Administration (NHSA) for implementation, with a significant number of policies still in the trial period.

Meanwhile, certain policies governing internet hospitals have entered a new lifecycle. Many of the previously issued regulatory policies were provisional in nature, requiring subsequent adjustments based on actual implementation experiences. Notably, regions such as Sichuan, Hainan, and Ningxia have specified trial periods for their respective policies. Although policies in some areas have transitioned into a new phase, the majority remain in the trial stage overall. This leaves considerable room for innovative exploration by internet hospitals, provided they ensure medical safety, information security, and other critical safeguards.

Selected Internet Hospital Policies During the Pilot Phase, Source: Official Websites of Local Health Commissions and Healthcare Security Administrations

Furthermore, policies related to internet hospitals are evolving from directional guidelines to operational frameworks, with increased procedural details. In the first half of 2021, Hubei and Hainan provinces issued policies on prescription circulation, specifying the detailed processes for prescription transfer.

Rapid Growth of High-Quality Online Resources Makes In-Person Healthcare a Long-Term Demand

During the pandemic, a large number of public hospitals established internet hospitals, a trend that continued into 2021. However, while users rapidly congregated during the pandemic, the user base declined in the post-pandemic period. In the post-pandemic era, users’ long-term demand centers on substantive medical care.

On the supply side, public hospitals holding core resources are accelerating their market entry, leading to an increase in online healthcare supply.

According to data from the National Health Commission, as of June 2021, there were more than 1,600 internet hospitals nationwide. VCBeat Research Institute compiled a list of 1,140 internet hospitals through public channels (as of July 2021) to analyze their characteristics.

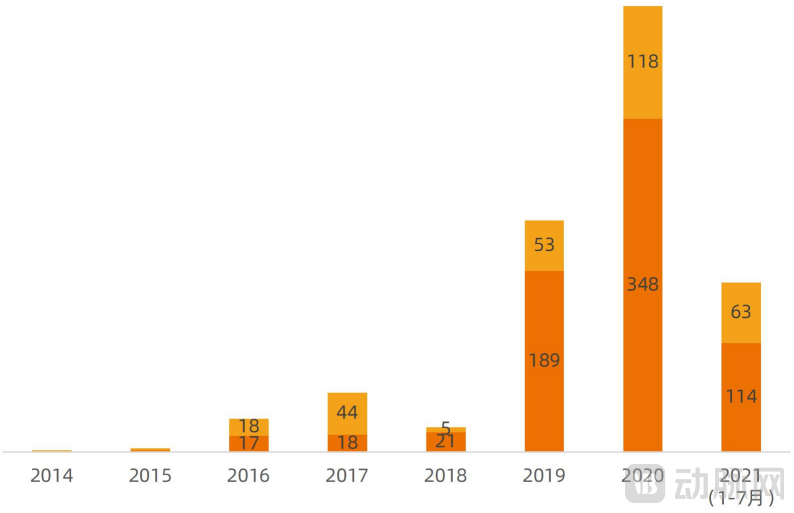

Over a longer timeline, internet hospitals have entered a phase dominated by hospital-led models since 2018. Data from the past three years show that the ratio of hospital-led to enterprise-led internet hospitals has remained roughly between 7:3 and 6:4, a proportion expected to persist in the future.

Leading Parties of Internet Hospitals Established Since 2014, Source: Local Health Commissions, Official Hospital Websites and WeChat Accounts, Chart by VCBeat

Note: Internet hospitals with unclear establishment dates are not included in the chart.

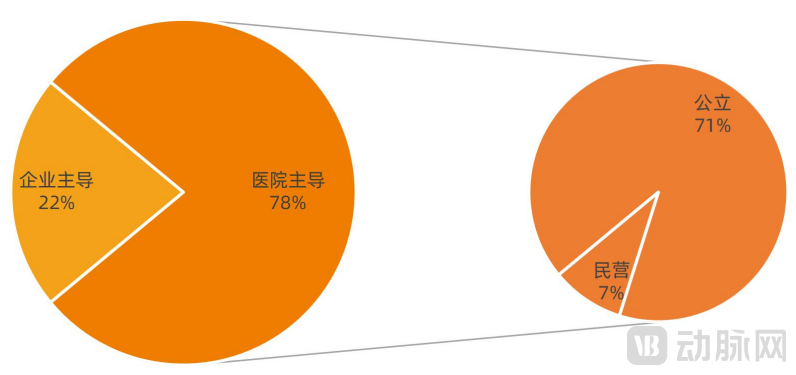

Among internet hospitals primarily established by physical hospitals, public hospitals constitute the majority. In particular, regions such as Beijing and Shanghai, which concentrate abundant high-quality medical resources, have accelerated their participation in the development of internet hospitals, with numerous top-tier hospitals joining this initiative. In 2021, Beijing established a regulatory platform for internet hospitals, thereby fulfilling the prerequisite conditions for approving internet hospital licenses. A number of hospitals that had previously only offered online consultation services connected with the regulatory platform and applied for internet hospital accreditation. According to incomplete statistics, by the end of July 2021, Beijing had 14 internet hospitals and dozens of hospitals approved to provide online consultation services.

Certainly, a number of outstanding private hospitals have also participated in the development of internet hospitals.

Overall Leading Parties of Internet Hospitals, Source: Local Health Commissions, Official Websites and WeChat Accounts of Hospitals, Chart by VCBeat

In terms of hospital classification, tertiary hospitals remain the dominant group. Among the 865 physical hospitals, 639 are tertiary hospitals, accounting for 74%, of which 488 are Grade A tertiary hospitals. According to the "Statistical Bulletin on the Development of China's Health and Wellness Undertakings in 2020," there were 2,996 tertiary hospitals nationwide in 2020, including 1,516 Grade A tertiary hospitals. Based on these figures, 21% of tertiary hospitals have established internet hospitals, and nearly one-third of Grade A tertiary hospitals have done so.

On the demand side, the pandemic attracted a large user base in the short term, while long-term demand post-pandemic centers on substantive medical care.

During the pandemic, internet hospitals attracted a large number of users; however, for users to develop more long-term habits, internet hospitals must be able to address their actual medical service needs and deliver tangible outcomes, rather than merely providing consultations that soothe emotions or answer questions.

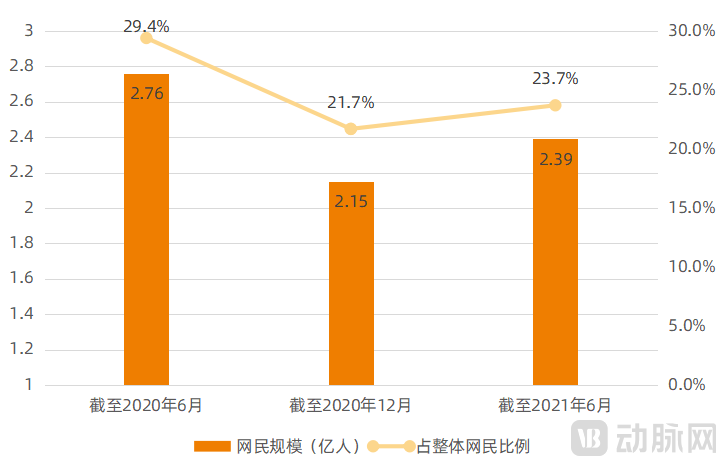

According to the 46th Statistical Report on China’s Internet Development released by the China Internet Network Information Center (CNNIC), as of June 2020, the number of online medical users in China reached 276 million, accounting for 29.4% of the total internet user base. Driven by the pandemic, growing user demand for online medical services has further accelerated the digital transformation of China’s healthcare industry.

According to the 47th and 48th Statistical Reports on China’s Internet Development released by the center, the number of online medical service users dropped to 215 million by December 2020. By June 2021, this figure had rebounded to 239 million; however, it still remained below the peak user base observed during the pandemic. This clearly demonstrates that online medical services experienced irrational, short-term demand surges during the pandemic period.

Changes in the Scale of Online Medical Internet Users, Data Source: China Internet Network Information Center, Chart Compiled by VCBeat

In the study titled “Survey on Follow-up Visit Experience of Tuberculosis Patients via Internet Diagnosis and Treatment Platform,” conducted by Beijing Chest Hospital, Capital Medical University, 131 tuberculosis patients who met the criteria for follow-up visits were selected as survey subjects. These patients had participated in online consultations between February and June 2020 and completed the entire process of internet-based diagnosis, treatment, and medication delivery. The questionnaire survey results showed that 26% of patients would prioritize online medical services after the pandemic, while 25.2% would choose in-person visits. This indicates that patients’ healthcare-seeking habits have not yet fully shifted to online platforms. The survey also revealed that over 50% of patients hoped to obtain follow-up consultations or remote prescription and medication delivery services through internet-based diagnosis and treatment, whereas only 42.5% sought pre-visit consultation services. This suggests that users expect substantive outcomes from online medical services.

Total Financing Reaches RMB 23.4 Billion, with Frequent Large-Scale Rounds; Industry Poised for a Wave of IPOs

Over the past year (with statistics starting from August 2020), there have been a total of 16 financing and M&A transactions in the primary market for internet hospitals (based on internet healthcare platforms that have established their own internet hospitals), with total financing reaching RMB 23.4 billion. In addition, JD Health went public on the Hong Kong Stock Exchange in December 2020, becoming the first profitable internet healthcare company to be listed.

Unlike in 2014, the inaugural year of internet healthcare, the current surge in capital interest is reflected not in the number of projects but in the size of individual investments. Large sums are concentrated in a select few projects, with approximately half of the financing rounds occurring at Series C or later, further highlighting the “winner-takes-all” effect. Most of these companies have established end-to-end services integrating medical care, pharmaceuticals, and insurance, with coordinated online and offline operations, while each has developed differentiated strengths in its core business areas.

Amidst the fervor in the primary market, enthusiasm among enterprises to rush into the secondary market has surged. In 2021, WeDoctor, Dingdang Kuaiyao, and Zhiyun Health successively submitted listing applications to the Hong Kong Stock Exchange. In August 2021, Yuanxin Technology also launched its initial public offering (IPO).

Given the current financing rounds and business maturity of major companies, the industry is poised for a wave of initial public offerings.

Healthcare Service Revenue Grows, Enhancing Medical Attributes

A review of the 2021 financial reports or IPO filings of several internet healthcare companies reveals that while pharmaceutical e-commerce remains the primary revenue source, these companies are expanding their online hospital networks and strengthening their medical and health service capabilities, leading to an accelerated growth in service-related revenue.

Strengthening Localized Offline Service Capabilities and Multi-Regional Deployment of Internet Hospitals Have Become the Mainstream

Building and operating internet hospitals in multiple regions has become a key strategy for digital health companies to strengthen their integration with offline medical resources, enhance localized service capabilities, and improve the conversion of offline patient traffic. It is also a fundamental prerequisite for enabling local medical insurance reimbursement.

Building and operating internet hospitals in multiple regions offers the following key values to digital healthcare companies:

First, strengthen the integration of offline medical resources. In China, medical resources are primarily concentrated in offline public hospitals. Collaborating with these hospitals to co-establish internet hospitals facilitates the digitization of such resources and enhances the diagnostic and treatment capabilities of online healthcare platforms.

Secondly, it can enhance the localized service capabilities of internet hospitals. Although internet healthcare companies can break through spatial limitations to serve patients nationwide, their offline service capabilities are relatively weak; when patients have needs for offline examinations, tests, surgeries, or hospitalization, platforms struggle to meet these demands. By establishing internet hospitals in multiple regions and strengthening cooperation with local medical institutions, they can connect patients with nearby offline services, thereby forming an integrated online-offline service capability.

Meanwhile, it can facilitate the mutual conversion of online and offline traffic. On one hand, physical hospitals have a large patient flow; by jointly establishing internet hospitals, some of these patients—particularly those with common or chronic diseases requiring follow-up visits—can be shifted to online platforms. On the other hand, internet hospitals can also direct online traffic to offline facilities, enabling precise patient triage for physical hospitals or departments and referring patients to the appropriate specialists.

Finally, given the localized nature of medical insurance, establishing internet hospitals within the corresponding pooling areas is a prerequisite for enabling local medical insurance reimbursement.

High Proportion of Drug Sales Revenue Remains Essential for Survival and Development in the Short Term

Revenue from pharmaceutical e-commerce and other forms of drug and medical device sales plays a significant role in the income of internet healthcare platforms. According to data released by the National Health Commission, by the end of 2017, the overall proportion of pharmaceutical expenditure (excluding traditional Chinese medicine decoction pieces) in public hospitals within pilot cities for comprehensive public hospital reform stood at 31%, having reached a reasonable level.

Compared with offline medical services, current internet healthcare primarily focuses on online consultations and the purchase of medications for follow-up visits related to common and chronic diseases. It has limited integration with diagnostic tests, laboratory examinations, and other offline services. For platforms that provide both medical care and pharmaceuticals, drugs naturally account for a significant proportion of their business. The sales of pharmaceuticals and medical devices represent a mature business model that generates continuous and stable cash flow for enterprises. This model was also a critical means of survival for companies before the emergence of mature business models in the internet healthcare sector.

Rapid Growth in Healthcare Service Revenue; Increased Healthcare Investment Becomes a Consensus

Although disclosed financial data from various companies show a high proportion of revenue from pharmaceutical sales, it is also evident that there is a growing consensus on increasing investment in healthcare service resources and strengthening service-oriented capabilities, with some of these investments already contributing to revenue growth.

Increasing investment in healthcare services is an inevitable step for internet healthcare companies to meet user demands. As the industry remains in its early stages and the development of healthcare service capabilities is just beginning, not all enterprises have demonstrated impressive financial results. Over time, the capabilities accumulated at this stage will become the driving force for their future growth.

Industrial Cluster Effects Emerge, Driving Down Investment Costs

Internet hospitals alone struggle to constitute an independent industry; however, due to their connectivity value, they can link enterprises across multiple segments, including pharmaceuticals, medical devices, insurance, consumer healthcare, and consumer wellness. Consequently, an industrial ecosystem can still take shape around internet hospitals. Currently, industrial clusters have already formed in four regions—Ningxia (Yinchuan), Hainan, Tianjin, and Sichuan (Chengdu)—with initial signs of cluster effects emerging. In terms of competitive advantages, these are policy-driven industrial clusters.

"Internet hospitals inherently possess the characteristic of transcending spatial limitations, yet there are still certain advantages to forming industrial clusters."

First, centralized approval facilitates policy breakthroughs. Looking back at the development of internet hospitals in Yinchuan before 2018, it followed a cycle of corporate clustering and institutional innovation. In 2018, internet hospitals received formal policy recognition. After various regions subsequently issued administrative measures for internet hospitals, the sector still faced inconsistent approval standards and uneven progress in the implementation of medical insurance coverage. Under the basic framework of the Administrative Measures for Internet Hospitals (Trial), some provinces and cities adopted a conservative stance toward enterprise-operated internet hospitals, resulting in few approvals and many rejections. Even in regions with an open attitude toward enterprise-operated internet hospitals, there were significant differences in detailed approval rules, particularly regarding the affiliated physical medical institutions, which often directly impacted the cost of corporate investment in construction.

When enterprises form clusters, it is possible to find a balance between their common demands and detailed approval regulations, thereby ensuring the smooth implementation of policies and the satisfaction of reasonable corporate requests.

Secondly, the pharmaceutical and medical device industries associated with internet hospitals have achieved economies of scale. While physician practice and patient consultations can be conducted online, the distribution of resulting pharmaceuticals and medical devices must rely on offline physical entities. Therefore, hubs for the internet hospital industry are poised to achieve scale in areas such as pharmaceutical and medical device distribution and warehousing, thereby supporting the industry’s sustainable development.

As internet hospitals have reached their current stage of development, in addition to focusing on “what has been done” within the industry, attention should also be paid to “how well it has been done.” To this end, this report investigates the current operational status of internet hospitals. The survey targeted internet hospitals that have already been established and are in operation across China. A total of 114 online questionnaires were distributed, and 109 valid responses were collected.

Resource Restructuring and Process Reengineering: Internet Hospitals Move Toward the Core of Healthcare

The Emergence of New Functional Departments: Breaking Down Physical Barriers

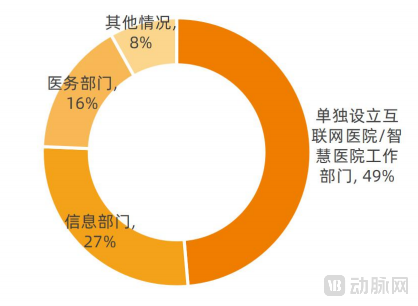

Surveys indicate that nearly half of hospital-led internet hospitals have established dedicated departments to manage their online operations. Physical hospitals are no longer limited to utilizing only their own physicians for practice, while corporate-owned internet hospitals are actively recruiting full-time doctors. The trend of medical resources transcending physical boundaries and flowing more freely is becoming increasingly pronounced.

Among hospital-led internet hospitals, 49% have established dedicated departments to oversee internet hospital operations. Nearly half are managed by either the Information Technology Department or the Medical Affairs Department, while 8% fall under other arrangements, such as Telemedicine Centers or Outpatient Departments. Within physical hospitals, the functional departments responsible for internet hospital operations are playing an indispensable role.

Operational Department of Hospital-Led Internet Hospitals, Chart by VCBeat

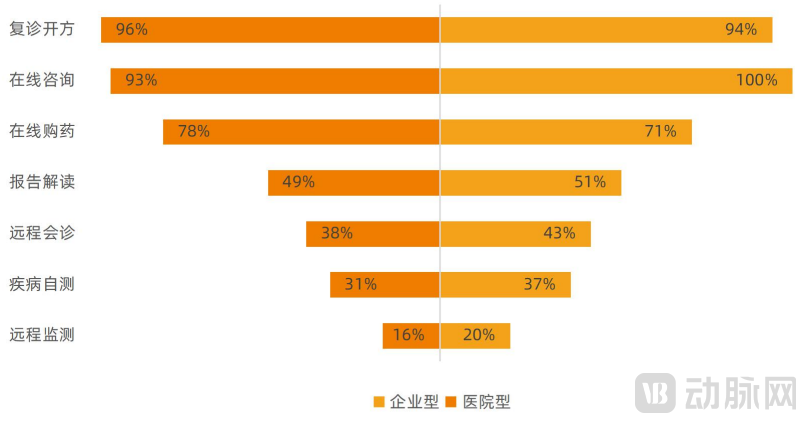

Service offerings are evolving from fragmented, single-item solutions to integrated, multi-service models, gradually moving toward the core of healthcare.

At its inception, the internet hospital facilitated the flow of medical resources and enhanced the efficiency of doctor-patient connectivity through online services, achieving significant success. Currently, internet hospital services are expanding from online to offline settings, with deeper integration between the two, thereby delivering more tangible health outcomes for patients.

Online Service Scenarios for Two Types of Internet Hospitals, Chart by VCBeat

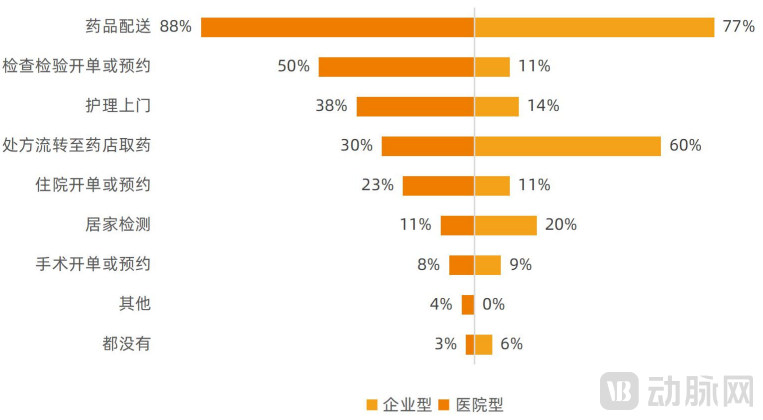

Surveys indicate that among services extending from online to offline channels, pharmaceutical delivery accounts for the largest proportion and is available through most hospital-affiliated and enterprise-run internet hospitals. In areas such as scheduling diagnostic tests and examinations, providing home-based nursing care, and arranging hospital admissions, hospital-affiliated internet hospitals have made significant explorations. Due to resource constraints, enterprise-run internet hospitals have yet to establish substantial connections in these segments.

The disease diagnosis and treatment process consists of multiple stages. Online services can demonstrate advantages in certain stages, and when integrated with offline services, they can unleash greater potential.

Service offerings of two types of internet hospitals extended to offline scenarios, chart by VCBeat

With the accelerated integration of online and offline services in internet hospitals, previously isolated service components can be better combined into bundled offerings that provide continuous care for specific diseases, such as chronic disease management packages, specialized disease management packages, and whole-course disease management packages. Currently, a large number of internet hospitals offer such continuous care services, with corporate-owned internet hospitals providing these services more extensively.

Surveys indicate that 51% of enterprise-operated internet hospitals offer ten or fewer types of transitional care services, with only 9% providing no such services. In contrast, up to 43% of hospital-operated internet hospitals do not offer these services.

For hospital-affiliated internet hospitals, since medical service items and pricing require regulatory approval, such services are typically provided in collaboration with third parties. In contrast, enterprise-operated internet hospitals are more proactive, as they can enhance patient payment conversion through service packages.

From the perspective of service content, enterprise-led internet hospitals offer a high degree of completeness in continuity care services, extensively covering consultations, follow-up visits, medication delivery, health records, patient follow-ups, and medical devices. However, diagnostic testing remains an area requiring supplementation. In contrast, continuity care services provided by hospital-led internet hospitals remain underdeveloped. Although these institutions are involved in multiple service areas with relatively balanced coverage, their depth of engagement in each area is insufficient.

On the surface, the overall service volume of current hospital-affiliated internet hospitals is not high. Compared with investments that often run into millions, it is indeed difficult to generate substantial returns in the short term; however, this is an inevitable stage in the industry’s development.

Patients have yet to develop habitual use of digital health services. Public hospital-affiliated internet hospitals, which dominate the sector and control core medical resources, are not only poised to seize broader growth opportunities as the industry expands, but also bear the critical responsibility of encouraging patient adoption and cultivating consistent usage habits.

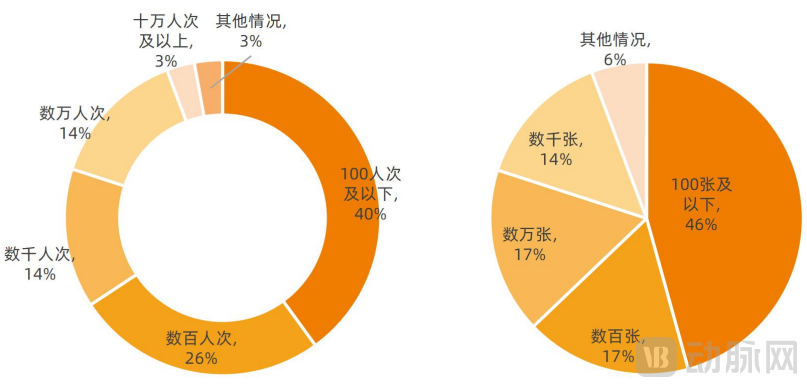

Daily Consultation and Prescription Volumes of Hospital-Led Internet Hospitals, Chart by VCBeat

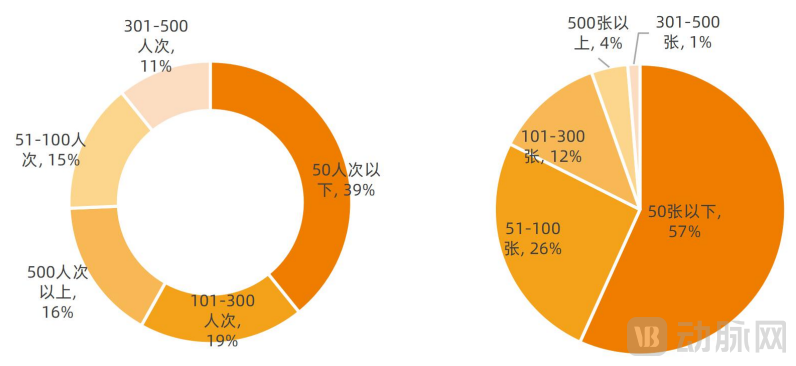

Among enterprise-owned internet hospitals, the majority are small-scale facilities. Due to significant disparities in scale and business volume among these institutions, this survey employed separate response options for consultation and prescription data, using tiers such as “under 100,” “hundreds,” and “thousands” as dimensional categories. Survey results indicate that small-scale internet hospitals with average daily consultations and prescriptions under 100 account for the largest proportion, at 40% or higher. A minority of enterprise-owned internet hospitals achieve average daily consultation volumes exceeding 10,000 visits, primarily those operated by leading internet healthcare companies.

Daily Consultation and Prescription Volumes of Enterprise-Led Internet Hospitals, Chart by VCBeat

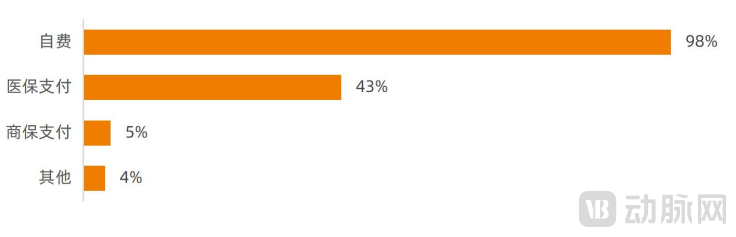

In this survey, 43% of internet hospitals already support medical insurance payments. Although the overall coverage rate has not yet exceeded 50%, it already demonstrates rapid expansion of medical insurance coverage, considering the timing of policy implementation and the launch dates of most internet hospitals. In contrast, the overall coverage rate for commercial insurance is extremely low, at only 5%, indicating substantial room for growth.

Overall Payment Structure of Internet Hospitals, Chart by VCBeat Institute

From a segmented perspective, the medical insurance coverage rate for hospital-affiliated internet hospitals is significantly higher than that of enterprise-operated internet hospitals, which still need to accelerate the improvement of commercial insurance payment systems. Survey data shows that 53% of hospital-affiliated internet hospitals have enabled medical insurance payments, compared to only 23% of enterprise-operated ones, with the latter concentrated in a few large enterprises. In terms of commercial insurance, 11% of enterprise-operated internet hospitals offer reimbursement capabilities, surpassing hospital-affiliated internet hospitals.

Differentiated Positioning: Hospital-Enterprise Collaboration to Enhance Benefits for All Parties

Among hospital-affiliated internet hospitals, those with third-party enterprises participating in operations demonstrate higher overall clinical data. Since continuity-of-care services constitute a key component of third-party operational involvement, this survey further reveals that hospital-affiliated internet hospitals offering such continuity-of-care services achieve better operational metrics than those that do not. Hospital-enterprise collaborative operation represents an important approach for both parties to establish differentiated positioning, fully leverage their respective values, and achieve mutual benefits.

Comparison of Average Daily Consultation Volume in Hospital-Based Internet Hospitals with and without Third-Party Involvement in Operations. Graphic by VCBeat.

Consultation volume and prescription volume are only two of the metrics used to evaluate the operational effectiveness of internet hospitals, and should not serve as the sole guiding indicators. Hospital-affiliated internet hospitals must also develop comprehensive operational evaluation criteria by taking into account factors such as their departmental structure and the number of physicians.

Meanwhile, hospital-enterprise collaborative operations are primarily suitable for general hospitals or other institutions that need to strengthen the cultivation of patient habits. For hospitals with high follow-up visit frequencies and strong patient demand, an increase in clinical volume does not necessarily require hospital-enterprise collaboration. For example, at Peking University Cancer Hospital, where the Information Department leads the internet hospital initiatives, the online follow-up visit rate has already reached 30%.

Academic research is an indispensable component of the medical field. Emerging subspecialties, in particular, rely on scholarly publications to disseminate research findings and exchange practical experience. The accelerated development of internet hospitals and the accumulation of consultation data have provided valuable materials for research in this area, especially for retrospective studies.

A search of the CNKI database revealed 250 papers with “internet hospitals” and “online medical consultations” as their primary themes published since 2014. The number of publications peaked in 2020, and based on the volume from January to July 2021, the total for the full year 2021 is projected to be on par with that of 2020.

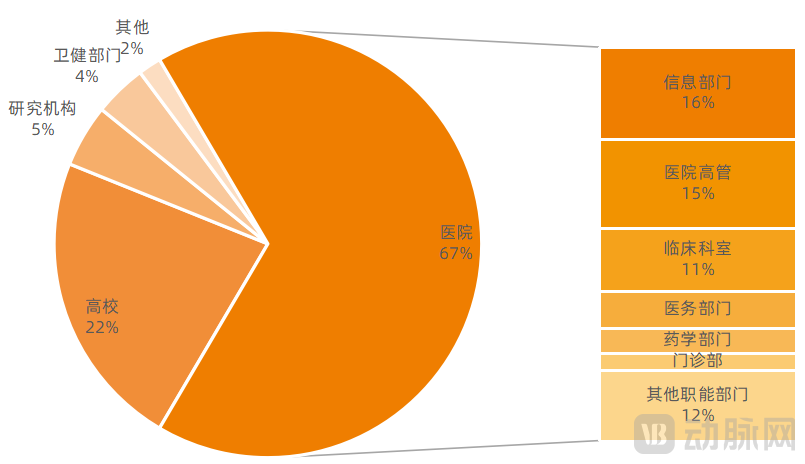

Who Is Most Interested in Research on Internet Hospitals? Based on the composition of authors (counted by first author) of these papers, 67% are from hospitals and 22% are from universities. In addition, authors from research institutions, enterprises, health departments, and academic societies have also published papers related to internet hospitals. As frontline personnel closest to patients, hospital workers naturally become the group conducting the most research on internet hospitals.

Among hospital-affiliated authors, who has conducted the most research on internet hospitals? Statistics show that professionals from information technology departments constitute the largest proportion among hospital authors. Hospital administrators (primarily presidents and vice presidents) are also major contributors to academic publications. In addition, 11% of clinical physicians have participated in research related to internet hospitals.

Sources of Authors of Internet Hospital Papers, Chart by VCBeat

Although scientific research is primarily concentrated in medical institutions, universities, and research institutes, its development also brings value to the industry. For example, it helps practitioners grow, especially doctors; provides empirical support for clinical work; and cultivates interdisciplinary talents for the industry.

In the future, internet hospitals will be deeply integrated into the healthcare system.

First, within the healthcare service system, internet hospitals can serve as platforms for tiered diagnosis and treatment, collaborating with physical medical institutions through mutual referrals. Internet hospitals precisely screen patients based on their symptoms; when examinations, surgeries, or hospitalization are required, patients are referred to physical hospitals for treatment. Upon completion of in-hospital care, patients are transferred back to online platforms for rehabilitation management.

Secondly, the industry’s development logic has gradually shifted from dimensions such as pure product sales and GMV growth to genuinely addressing patients’ diseases and improving their health outcomes.

Meanwhile, with the rapid development of the internet healthcare industry, corporate-run internet hospitals have already established numerous benchmarks. Since 2020, there has been a substantial increase in the establishment of public internet hospitals, and a wider variety of benchmark models are expected to emerge in the future.

Benchmark internet hospitals will increasingly emerge in Beijing, Shanghai, and Guangzhou, where high-quality medical resources are concentrated, large hospitals serve a significant number of out-of-town patients, and hospital informatization levels are high. Individual benchmarks will also arise within the industry, particularly among those who entered the digital health sector early; they will bring their third-party platform operational expertise to public hospitals, thereby promoting the development of internet hospitals.

Benchmarks emerging within the public healthcare system are more representative of the strength of the medical system, thereby driving deeper industry transformation.

The above summarizes the key contents of the report. The table of contents is as follows. Scan the mini-program at the end of the article to read the full report for free:

Chapter 1 Overview of Internet Hospitals

1.1. Policies Shift from Directional to Operational, with Select Regions Entering a New Cycle

1.2. Rapid Growth of High-Quality Online Resources, with Tangible Healthcare Becoming a Long-Term Demand

Chapter 2 Internet Hospital Market

2.1. Frequent Large-Scale Financing Rounds Signal an Upcoming Wave of IPOs in the Industry

2.2. Growth in Medical Service Revenue and Enhanced Medical Attributes

2.3. Industrial Cluster Effects Emerge, Driving Down Investment Costs

Chapter 3 Operations of Internet Hospitals

3.1. Resource Restructuring and Process Reengineering: Internet Hospitals Move Toward the Core of Healthcare

3.2. Differentiated Positioning: Hospital-Enterprise Collaboration to Enhance Benefits for All Parties

Chapter 4: Research on Internet Hospitals

4.1. A Surge in Academic Publications: Internet Hospitals Become a Research Hotspot

4.2. Active Enterprise Participation and Mutual Promotion among Industry, Academia, and Research

Chapter 5 Trends in Internet Hospitals

5.1. Deep Integration of Internet Hospitals into the Healthcare System

5.2. The development logic is gradually shifting from process-oriented to outcome-oriented

5.3. Emergence of Various Benchmarks Driving Deeper Industry Transformation