Sequoia, Hillhouse, Tencent, and Ant Pour Billions into China's Booming Health Insurance Sector — How Long Will the Frenzy Last?

The Health Insurance Sector Is Heating Up!

Since last year, financing in the health insurance sector has been continuous, with both the frequency and amount of funding rising steadily.

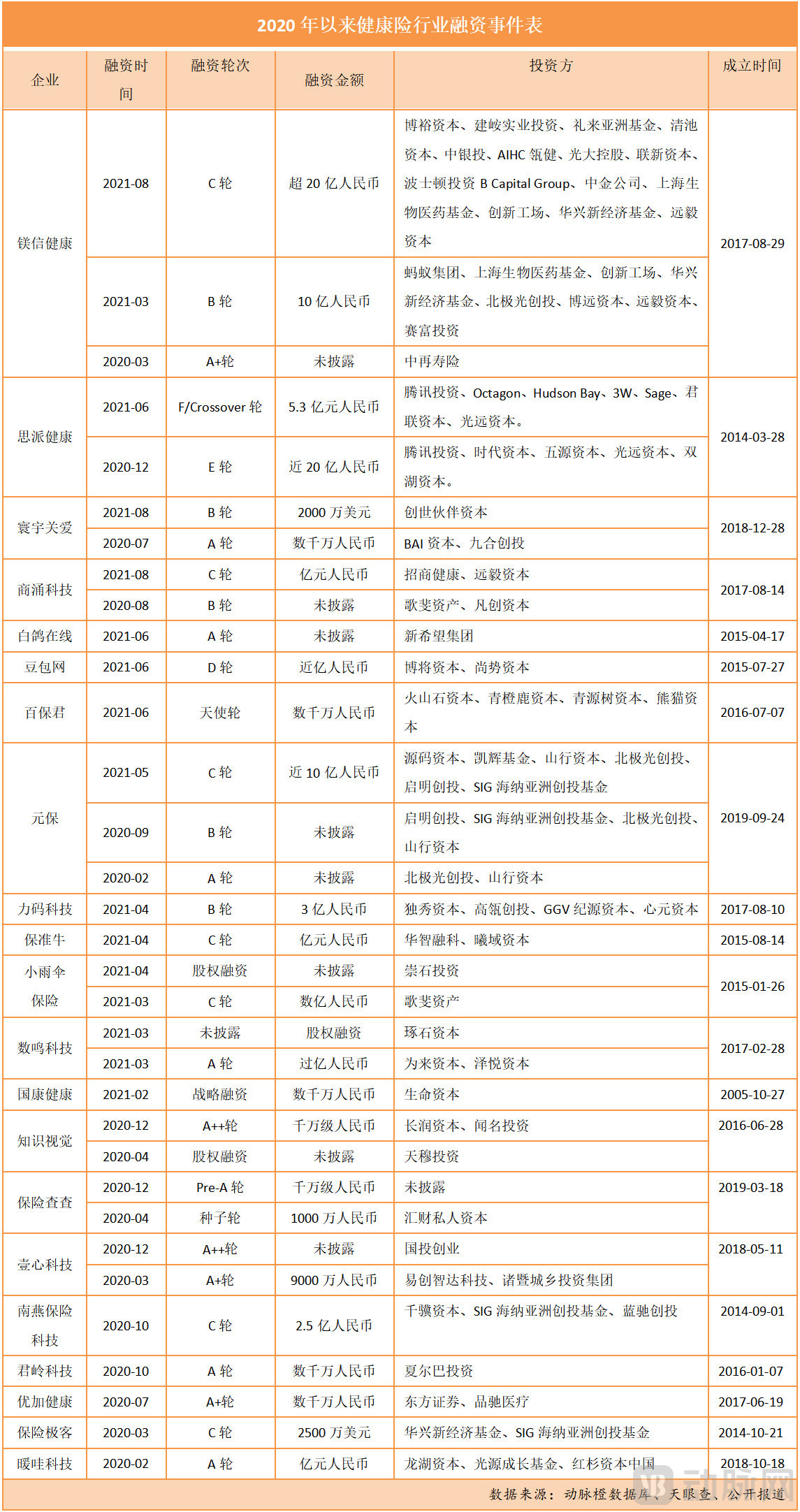

According to the data from the VCBeat database,Since 2020, there have been a total of 35 financing events in China’s primary health insurance market, with the total amount raised exceeding RMB 10 billion. Industry giants such as Sequoia China, Hillhouse, Tencent, and Ant Group have frequently appeared on the list of investors.

It is worth noting that within this surge of activity, capital is increasingly concentrating on leading enterprises. Over the past year, top players such as Sipay and Medbanks secured hundreds of billions in financing, accounting for more than half of the total funding amount. Meanwhile, companies including Yuanbao, Xiaoyusan Insurance, Nanyan Insurance Technology, Limake Technology, and Baoxian Jike have followed closely behind, with their financing scales continuing to expand.

In the secondary market, Waterdrop Inc., in which Tencent heavily invested across five funding rounds, went public in May and currently has a market capitalization of nearly RMB 10 billion. SiPai Health, which has secured multiple rounds of financing and also received multi-round investments from Tencent, filed its prospectus in August, reporting annual revenue of nearly RMB 2.7 billion.

It is evident that the pace of financing in the health insurance industry is accelerating, with capital flows increasingly concentrated among leading enterprises, and multiple companies are on the verge of going public.VCBeat has learned that the number of companies with annual revenues exceeding RMB 100 million has now reached double digits.

Amid the Frenzy of Heavy Bets, What Are Investment Institutions Really Gambling On? How Are Leading Companies Strategically Positioning Themselves? What Remaining Challenges and Pain Points Plague the Industry? And What Will Its Future Evolution Look Like? To address these questions, VCBeat has interviewed numerous industry practitioners and investors to shed light on the answers.

Health insurance is not an emerging sector; it is even somewhat traditional. Why has capital shown such intense enthusiasm for this sector in recent years, pouring substantial real money into it?

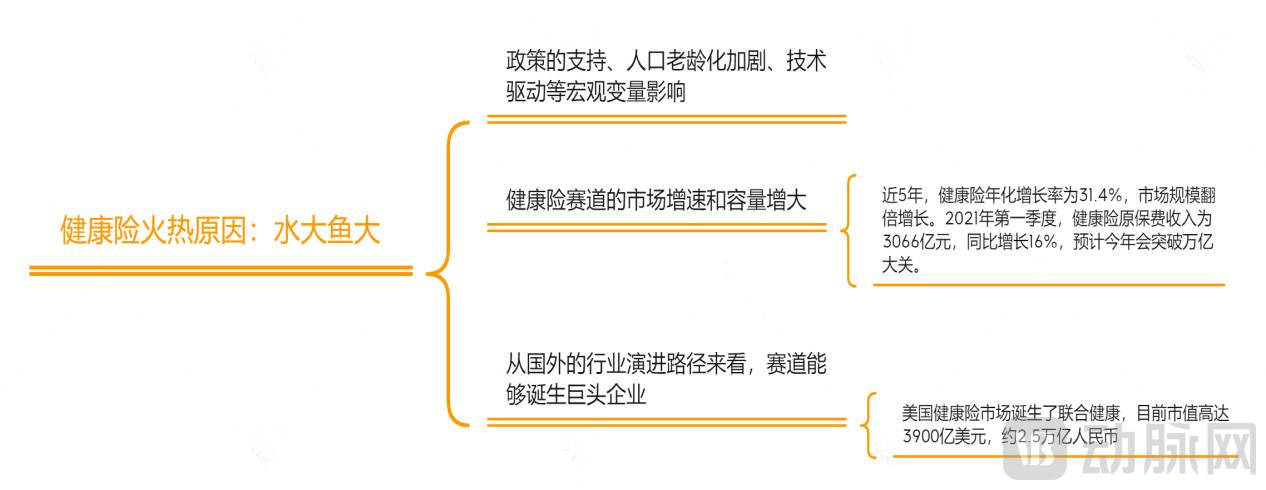

“The primary drivers remain the influence of macro-level variables such as policy support, accelerating population aging, and technological advancement,” said Wang Wei (a pseudonym), Deputy General Manager of the Product Development Department at a major insurance group, in an interview with VCBeat.This represents a massive opportunity driven by structural change; those who seize it have the potential to grow into giants with market capitalizations of tens of billions, hundreds of billions, or even trillions.”

Taking the U.S. health insurance market as an example, industry giants such as UnitedHealth Group have emerged. As a constituent of the S&P 500 Index, UnitedHealth Group has seen its stock price increase more than 15-fold over the past decade, with annual revenue exceeding $240 billion and a current market capitalization of $390 billion (approximately RMB 2.5 trillion). This valuation is three times that of Pinduoduo, a leading Chinese internet company, 1.6 times that of Meituan, and slightly lower than that of Alibaba.

“The situation in China is vastly different from that in the United States; therefore, direct comparisons cannot be made by simply applying the U.S. model. For example,”Given the extensive coverage of China's national medical insurance, commercial health insurance is not currently a necessity for the Chinese population.“Wang Wei stated, “However, the market growth rate and capacity of the domestic health insurance sector cannot be underestimated.”

According to data from the China Banking and Insurance Regulatory Commission (CBIRC), the original premium income for health insurance business reached RMB 817.3 billion in 2020, a year-on-year increase of 15.7%, with a growth rate significantly higher than that of other types of insurance. Notably, over the past five years, the compound annual growth rate (CAGR) of health insurance was 31.4%, doubling the market size. In the first quarter of 2021, the original premium income for health insurance amounted to RMB 306.6 billion, representing a 16% year-on-year increase, and it is projected to surpass the RMB 1 trillion mark this year.

In other words, the health insurance sector is a vast and lucrative market: with gross written premiums poised to exceed RMB 1 trillion and an annualized growth rate surpassing 30%, the overall market potential is highly attractive. Furthermore, based on the evolutionary trajectory of the industry in foreign markets, this sector has the capacity to produce giant enterprises.This is the core logic behind capital's frenzied bets.

With a sufficiently broad market and the opportunity to build large enterprises, what kinds of targets are favored by investors?

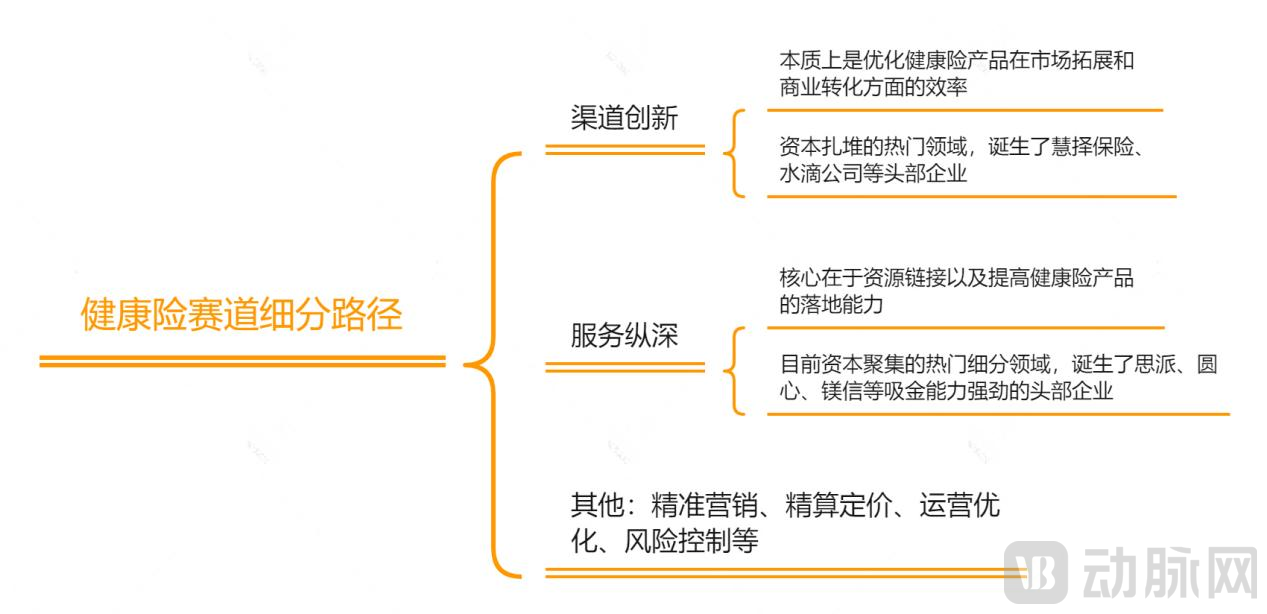

“The traditional health insurance market is a red ocean, with fierce competition and significant product homogenization,” a senior investor who wished to remain anonymous told VCBeat. As the market expands, an increasing number of participants have realized thatTo achieve a rapid breakthrough, it is essential to enhance overall efficiency by deeply cultivating proprietary competitive advantages in areas such as channel innovation, precision marketing, differentiated services, actuarial pricing, operational optimization, risk control, and the construction of medical service networks.

Consequently, building on these directions, numerous health insurance technology companies are exploring their own unique paths. For instance, Haorensheng Technology focuses on risk control, providing insurers and internet platforms with a closed-loop suite of health insurtech services ranging from product customization and digital risk management to intelligent underwriting and claims processing, as well as systematic health management. Similarly, Baoxian Jike (Insurance Geek) enters the market from the service side, concentrating on the group health insurance sector. By adopting a distinctive B2B2C model, it has established a comprehensive health industry ecosystem integrating “group insurance + healthcare.”

“Health insurance is a business model that relies on scale for its viability, with competitiveness hinging on pricing and the breadth or depth of its medical and health service networks.“said the aforementioned investors.”

It is precisely on this basis that capital has increasingly clustered around enterprises focused on channel innovation and deepening service offerings:Enterprises that innovate in distribution channels can rapidly scale up, significantly boosting revenue and valuation with the support of capital.; companies with deep service integration benefit from strong user stickiness, making it difficult for competitors to enter the market once the business model has been proven successful.“It’s not that other areas lack opportunities; it’s just that these two are currently hotter.”

Specifically, channel innovation refers to leveraging digital technologies to help insurance companies better market and sell health insurance-related products.Essentially, it optimizes the efficiency of health insurance products in market expansion and commercial conversion.; Service depth refers to helping insurance companies undertake the service components of health insurance, including medical care and health management, by linking resources from all parties in the pharmaceutical, healthcare, and insurance sectors.The core lies in resource linkage and enhancing the implementation capability of health insurance products.

For instance, Shuidi Inc., a publicly listed company, operates in the realm of channel innovation. Its business model leverages services such as Shuidi Chou to create insurance education scenarios and build brand equity, which are then monetized through Shuidi Bao. This approach enables insurance distribution channels to reach a broader target market, including individuals with protection needs in lower-tier cities (tiers 3–6).

According to its financial reports, Waterdrop Inc.’s revenue has been steadily increasing, reaching RMB 238 million in 2018, RMB 1.511 billion in 2019, and RMB 3.028 billion in 2020. In the first half of 2021, the company reported revenue of RMB 1.823 billion, a year-on-year increase of 36.57%, demonstrating strong commercialization capabilities. Prior to its listing on the secondary market, Waterdrop attracted significant investor interest, completing five rounds of financing with a total amount exceeding RMB 4 billion.

In terms of service depth, unicorns such as Simpai and Maginext, which have demonstrated strong fundraising momentum over the past year, are operating in this domain. “The fact that these companies have captured the majority of financing across the entire sector this year indicates that major institutional investors are shifting their strategies,” said a financial advisor who has long focused on health insurance. “Channel innovation was the hot topic in health insurance investment in previous years, with representative companies such as Huize Insurance and Shuidi Inc. already successfully listed. Therefore, investors are currently more inclined toward companies with deep service integration. Given the low industry concentration, there are more opportunities, and results are more visible in the short to medium term.”

Furthermore, from a market perspective, as companies pioneering channel innovation gradually mature, this sector will transition from a growth-driven market to a stock-based market, intensifying competitive pressures. Taking Huize Insurance as an example, its marketing expenses from 2018 to 2020 were RMB 94 million, RMB 164 million, and RMB 230 million, respectively, showing a year-on-year increase. Notably, the commission rate, which is the most critical factor supporting revenue, declined by approximately 9 percentage points in 2020 compared to 2019. According to the company’s announcements, this reflects Huize Insurance’s strategy to expand its scale continuously in response to market competition.

In summary, it is evident that within the vast and rapidly expanding market for health insurance, channel innovation and service deepening have emerged as the two most prominent trends. As leading companies have already established themselves in the realm of channel innovation, enterprises focusing on deepening service offerings are attracting increasing attention from investors.This is precisely the key reason why tens of billions of yuan in capital are pouring into this sector.

As health insurance ventures deeper into service provision, unicorns such as Si Pai and MedXin have attracted substantial capital inflows, drawing significant attention from the industry. People cannot help but wonder: What do these companies have in common? What are their respective competitive advantages? And why have they garnered such strong favor from investors?

Before answering this question, it is necessary to first understand:The integration of health insurance with medical resources, along with its convergence with health management, is becoming a major trend.

The concept of a “pharma-medical-insurance” closed loop has long been widely circulated in the venture capital and startup community. Its core logic lies in health insurance serving as the primary payer for medical services: by purchasing health insurance, users can have their expenses for medical treatment and health management reimbursed by commercial insurance companies, thereby forming a triangular closed loop among “healthcare providers–patients–insurance companies.”

Within this closed-loop service,Theoretically, health insurance product designers, armed with insights into user needs, can negotiate with pharmaceutical companies and healthcare providers to leverage scale for better pricing. As a result, health insurers benefit from reduced loss ratios due to improvements in users’ health conditions, while users enjoy more cost-effective services.In other words, the outcome can achieve a win-win situation for all parties involved. This aligns perfectly with the broader trend of the “Three-Medical Linkage” reform, which integrates healthcare services, medical insurance, and pharmaceuticals.

However, despite the appealing proposition, implementation has proven exceedingly difficult. Establishing drug reimbursement lists for commercial health insurance, building extensive pharmacy networks, differentiating services from social health insurance, and creating synergistic mechanisms among healthcare providers, pharmaceutical companies, and insurers all pose significant challenges that test the ingenuity of market entrants. For a considerable period, the “Healthcare + Pharmaceuticals + Insurance” model has remained largely conceptual.

At this point,The state is promoting the development of health insurance through policy support.For instance, last September, the General Office of the China Banking and Insurance Regulatory Commission (CBIRC) issued the “Notice on Regulating Health Management Services Provided by Insurance Companies,” which clarified that health management services could account for up to 20% of the costs in insurance products. The significance of this move lies in the fact that lifting the proportional restrictions on health management services allows insurers to increase their share, thereby strengthening the integrated nature of coverage and services in health insurance products and opening up greater potential for a closed-loop ecosystem encompassing healthcare, pharmaceuticals, and insurance.

Driven by policy initiatives, health insurance technology companies are continuously expanding their health management services. According to incomplete statistics based on publicly available information, more than 50 insurance companies currently include extended services such as health management in their products. Among these, disease green channels, family doctor services, and specialty drug coverage have become the mainstream offerings in the market.

In other words, the model of linking health insurance with healthcare and related services to create synergistic resource integration is currently at the forefront of industry trends, a direction aligned with that of unicorns such as Si Pai and Magin.Of course, there are similarities and differences in the specific approaches taken by each organization.

To elaborate,"In terms of 'medicine'"Since its inception, SiMai has focused on the field of oncology big data. According to its prospectus, its oncology clinical trial site management organization (SMO) business—the core revenue contributor within its Patient Research Services (PRS) segment—ranks first in China’s oncology drug development sector. Currently, it has assembled a rich medical resource network across more than 100 major cities in China, encompassing over 1,100 Grade A tertiary hospitals, 42,000 physicians, and 500 health examination institutions.

MediTrust Health entered this sector relatively late and is currently actively expanding its internet hospital operations. Its subsidiary, Kangfu Internet Hospital, is the first independently established internet hospital in the Hainan Boao Lecheng International Medical Tourism Pilot Zone. Leveraging high-quality “Internet+” medical services and a professional healthcare team, it effectively connects doctors with patients, integrates premium global medical resources, and provides comprehensive medical and health management services to patients.

In terms of "drugs", according to the prospectus, the scale of SiPai’s pharmacy benefit management (PBM) business is equivalent to that of China’s largest private specialty pharmacy, with revenue reaching RMB 2.482 billion in 2020. In relation to its clinical trial services, SiPai has established a Clinical Trial Business Group, serving more than 240 clients, including major multinational pharmaceutical companies, large domestic pharmaceutical firms, and emerging biotechnology enterprises.

Medicx Health’s Yaokangfu Platform, as a comprehensive patient healthcare service platform, provides “Internet + Healthcare” management services to patients. It has partnered with over 50 innovative pharmaceutical companies and more than 2,000 DTP (Direct-to-Patient) pharmacies, covering over 400 cities across China. The platform benefits over one million patients with cancer, chronic diseases, and rare diseases by delivering all-around, round-the-clock medication services. Additionally, it customizes diverse welfare innovations for patients through initiatives such as patient assistance programs, financial payment plans, and efficacy insurance schemes.

"In terms of 'risk'"In recent years, Si Pai has been actively developing special drug insurance and Huiminbao (inclusive supplemental medical insurance), engaging in deep collaborations with many domestic insurance companies. For instance, it has implemented inclusive supplemental medical insurance programs in multiple regions and launched a new generation of corporate health and wellness benefits solution—Si Pai Health Insurance. Through a model featuring proactive management by corporate physicians, Si Pai Health Insurance completes the commercial insurance closed loop of “insurance coverage–services–claims settlement” within Si Pai Health Tech’s self-built healthcare ecosystem.

Magene Health focuses on both patient populations and healthy individuals, driving continuous innovation in areas such as out-of-pocket payments, commercial health insurance, and city-specific inclusive insurance programs. Since 2020, Magene Health has been deeply involved in various city-specific inclusive insurance initiatives, including “Su Hui Bao,” “Xihu Yilian Bao,” “Hui Qu Bao,” “Hu Hui Bao,” and “Beijing Puhui Health Insurance,” covering more than 40 cities such as Beijing, Shanghai, Hangzhou, and Ningbo.

It can be observed that several unicorns share a common approach in business model development: establishing a closed-loop ecosystem integrating pharmaceuticals, healthcare services, and insurance. However, differences arise based on their respective corporate growth trajectories and core competitive advantages.: For example, Si Mai has accumulated experience in physician and medical network services, while MedXin has achieved breakthroughs in innovative payment solutions with a patient-centric approach.

In summary, the evolution of health insurance toward deeper service integration still faces numerous challenges, while the unicorns that have taken the lead have, through years of strategic layout, already articulated their own approaches.

As unicorn companies enter the later stages of financing, their initial public offerings are drawing nearer.

On the other hand, industry giants have also begun to establish or expand their presence in this sector. For instance, this May, JD Health partnered with Fosun United Health, JD Allianz Insurance, and several other insurance companies to jointly launch the “Home Medical Insurance” managed health insurance service. Centered on disease prevention and health improvement, this initiative integrates health insurance with JD Health’s medical services and health management capabilities, providing families with a one-stop, lifelong medical healthcare service and health protection solution.

For another example, in July this year, Ping An Health (formerly “Ping An Good Doctor”) launched a direct billing feature for commercial health insurance. Users insured under relevant insurance products can not only consult doctors and purchase medications through the Ping An Health app, but also enjoy zero out-of-pocket settlement convenience—consultation services and medication costs covered by the policy are settled directly between the platform and the insurer, enabling a “seamless” direct reimbursement experience for commercial insurance. This means that users can complete a series of steps, including medical consultation, medication purchase, and claim reimbursement, without leaving home, significantly streamlining the previously cumbersome settlement process.

As we can see, a growing number of health insurance companies are rushing toward initial public offerings (IPOs), while industry giants are accelerating their entry into the market. Does this mean that the health insurance industry has reached its inflection point?

“From the current perspective,The industry’s inflection point has yet to arrive. Capital can only accelerate companies in validating their business models, but whether this path will succeed ultimately depends on the enterprises’ innovation capabilities and business acumen.“Wang Wei told VCBeat.”

From the current industry perspective, the rapid rise of star enterprises such as Huize Insurance, Shuidi Inc., Si Pai, and Magnesium Trust indicates that the health insurance industry has achieved significant development. However, the sector still faces challenges, including low penetration rates and high loss ratios amid substantial business growth.

“From a long-term perspective, this is a sector with a long runway and substantial potential; however, there is still much ground to cover before achieving success,” said Wang Wei. “The industry as a whole has a weak foundation, with room for improvement in areas such as data sharing, standardized evaluation, and management capabilities. Innovative enterprises need to provide more and better products in their backend services.”

It is foreseeable that with the continuous development of health insurance, China’s medical and healthcare ecosystem will undergo new changes. Amidst these changes, increasing opportunities are emerging.

In this process, innovative enterprises that dare to continuously refine and break through amidst the tides of the times will also usher in their own moments in the spotlight.