Why Did Orthopedic Stocks Surge Despite 82% Price Cuts in National Joint Implant Procurement?

On September 14, the national centralized procurement of artificial joints was finally implemented.

Price reduction remains the central theme of this volume-based procurement (VBP) program for artificial joints. The scope of products covered includes artificial hip and knee joints, with an initial annual intended procurement volume of 540,000 sets, accounting for 90% of the total demand from medical institutions across China. Based on 2020 procurement prices, the market size of the products involved in this procurement reaches RMB 20 billion, representing over 10% of the high-value medical consumables market.

A total of 48 companies participated in this centralized procurement, with 44 selected, resulting in a selection rate of 92%. The average proposed bid price for hip joints decreased from RMB 35,000 to approximately RMB 7,000, while the average price for knee joints dropped from RMB 32,000 to around RMB 5,000, representing an average price reduction of 82%.

Although the volume-based procurement process inevitably leads to a significant reduction in end-user prices, compared with the over 90% price drop seen in coronary stents during their first round of procurement,Industry insiders generally consider the centralized procurement of orthopedic artificial joints to be relatively “moderate.” Many companies have also stated that the prices in this round of procurement are within an acceptable range.

The stock prices of major domestic orthopedic companies also began to bottom out and rebound after the volume-based procurement (VBP) was finalized. Following the announcement of the VBP results, the stock prices of leading domestic orthopedic manufacturers that won bids reversed their previous downward trends and surged significantly. Weigao Orthopaedics and Double Medical hit the daily price limit ceiling after the bid opening for artificial joint VBP, while AK Medical and Chunli Medical saw increases of over 10%. Industry insiders have expressed optimism, stating thatThe post-centralized procurement rise in orthopedic companies’ stock prices reflects the gradual restoration of capital market confidence in high-value consumables.

Why Volume-Based Procurement Is a Storm for Coronary Stent Manufacturers but a Boon for Orthopedic Consumable Companies? How Will the Market Landscape of High-Value Orthopedic Consumables Change as the Price of Artificial Joints, a Key High-Value Orthopedic Consumable, Enters the “Thousands-of-Yuan” Era? VCBeat Analyzes the Latest Volume-Based Procurement for Orthopedic Products.

The national centralized volume-based procurement (VBP) of artificial joints is the second product category to undergo such procurement nationwide. The VBP for coronary stents has been implemented in clinical practice for over six months. Drawing on previous experience and lessons learned, the VBP rules must ensure that higher-quality products are used in clinical settings while also guiding winning bid prices to remain reasonable.

Why Hasn’t the Artificial Joint Sector Seen Drastic Price Cuts? First, the Rules Are More Reasonably Designed."Industry insiders stated that the rules themselves reveal the protection afforded to manufacturers by the volume-based procurement of artificial joints."

The rules for the volume-based procurement (VBP) of orthopedic artificial joints differ significantly from those for coronary stents. The national VBP for coronary stents relied solely on price bidding with simplified grouping. In contrast, the VBP rules for orthopedic artificial joints first categorize products into four major groups. Subsequently, based on three criteria—medical institutions’ procurement demands, enterprises’ supply capabilities, and product materials—products are further divided into Group A and Group B. To qualify for Group A, a product must meet all three of the following conditions: it accounts for the top 85% of hospitals’ intended procurement volumes; it covers the procurement demands of all prefecture-level cities within the alliance; and it is made of highly cross-linked polyethylene or highly cross-linked polyethylene (containing antioxidants).

“Group A has a larger volume and is the major group. The establishment of Group A and Group B serves to protect high-volume enterprises, preventing some companies from submitting abnormally low bids to win contracts.”

The moderation of centralized procurement is more evident in the elimination rates. Specifically, Group A exhibited lower elimination rates. The competitive landscape for hip implants—ceramic-on-ceramic, ceramic-on-polyethylene, and metal-on-polyethylene—saw selection ratios of 7 out of 8, 8 out of 10, and 8 out of 9, respectively. For knee implants, the ratio was 8 out of 10. Under the rules, companies in Group A could be reinstated if their bids were below the highest price in Group B. In this round of centralized procurement, 48 companies participated, with 44 selected, resulting in a success rate of 92%.

A securities analyst told VCBeat, “The low elimination rate meant that manufacturers did not significantly slash prices to win bids in the centralized procurement of artificial joints, resulting in relatively rational pricing from participating companies.”

The moderation of centralized procurement is also reflected in the differences in product pricing; compared with coronary stents,Accompanying services appeared for the first time in the centralized procurement of artificial joints.The bidding rules state that the declared price includes the prices of all components within the product system (including distribution fees for the product system, distribution fees for ancillary tools, and usage fees for ancillary tools), as well as fees for accompanying services.

This represents a significant change following the volume-based procurement (VBP) of coronary stents. Prior to VBP, manufacturers were proactive in distribution and provided intraoperative support; however, after VBP compressed profit margins for coronary stents, companies eliminated these technical support services to control costs. In this round of VBP, the pricing of ancillary services has also been included in the competitive bidding process.

In the traditional distribution model for orthopedic artificial joints, orthopedic companies often purchase third-party services to handle channel development and customer maintenance. These services also provide specialized support for orthopedic products to end customers, including preoperative consultation, logistics assistance, intraoperative technical support, cleaning and sterilization, and postoperative follow-up, thereby ensuring that the company’s products best meet surgeons’ operational needs. This expense represents a significant cost for artificial joint manufacturers. According to Weigao Orthopaedics’ prospectus, business service fees accounted for 68.73% of its selling expenses in 2020, totaling RMB 433.7905 million.

In this round of centralized procurement for artificial joints, the prices for ancillary services have also seen significant reductions, with the lowest price reaching RMB 50 per unit. Post-procurement, the prices for ancillary services generally range from RMB 100 to RMB 200.

Thresholds for enterprises were also established in the rules for the centralized procurement of artificial joints. Under these rules, the third requirement for inclusion in Group A, which commands higher usage volumes—namely, the provision of highly cross-linked polyethylene products—is intended to ensure that enterprises possess a certain level of competitiveness.

The main components of a hip prosthesis system include the femoral stem, acetabular cup, liner, and femoral head. In total hip arthroplasty, implants utilizing both a ceramic femoral head and a ceramic liner are referred to as ceramic-on-ceramic (CoC) systems, while those combining a ceramic femoral head with a non-ceramic liner are termed ceramic-on-polyethylene (CoP) or semi-ceramic systems. Highly cross-linked polyethylene (HXLPE) exhibits superior wear resistance; its wear rate is significantly lower than that of conventional polyethylene used in the past. The ceramic-on-polyethylene combination accounts for more than 50% of total hip arthroplasties in developed countries, making it the most widely used system in this procedure.

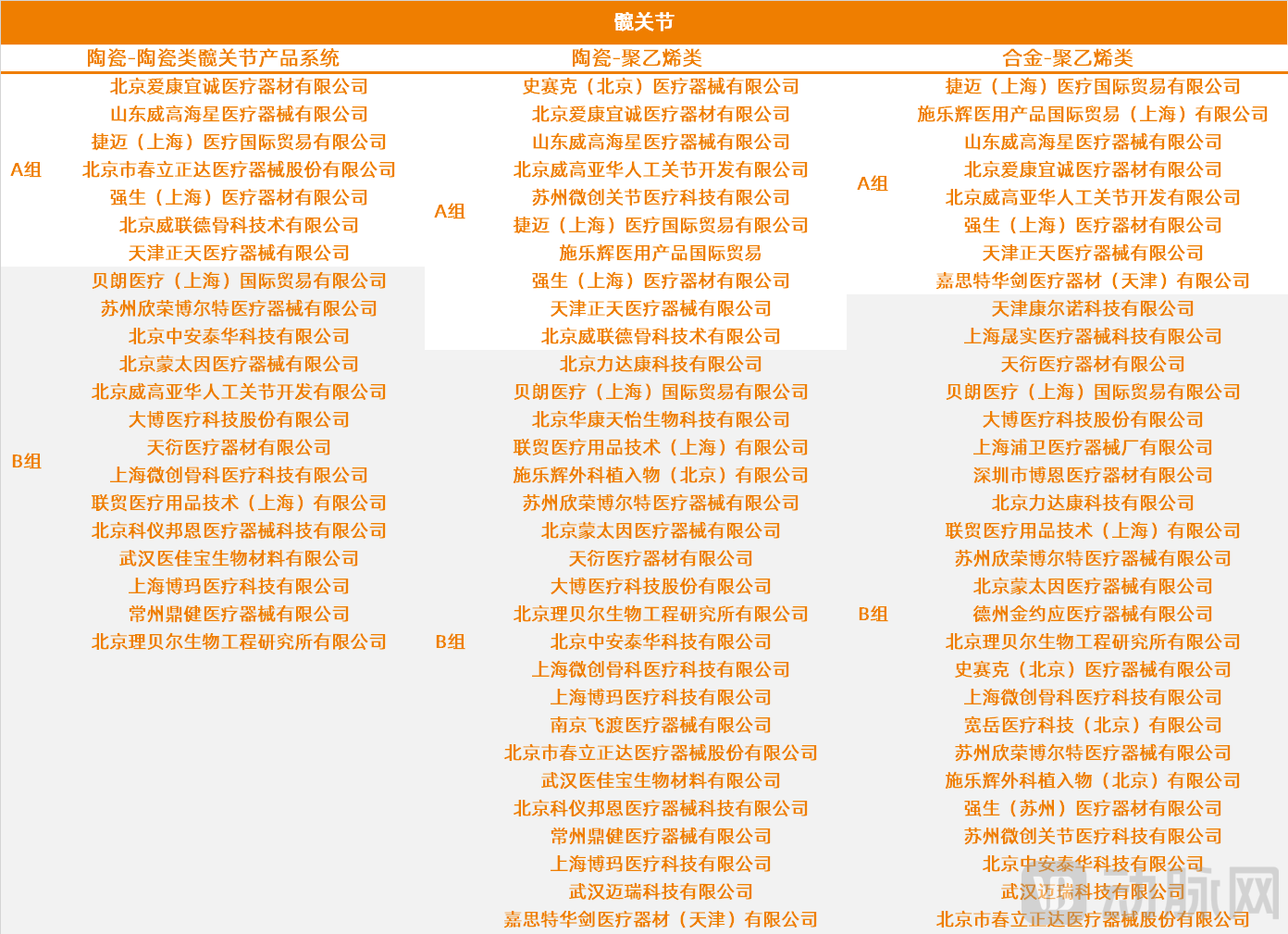

Winning Bidders for Hip Joints in the Centralized Procurement of Artificial Joints

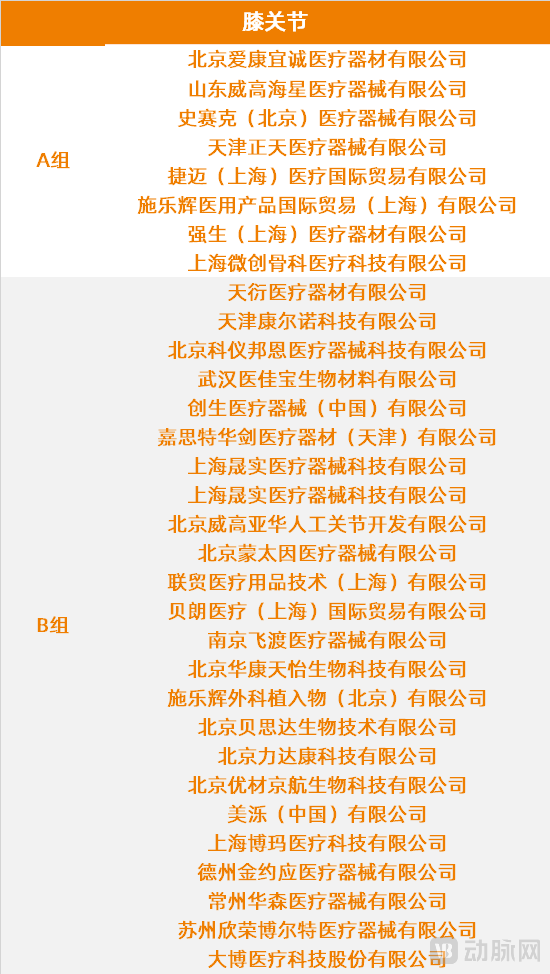

Winning Bidders for Knee Joints in the National Centralized Procurement of Artificial Joints

In addition to the regulatory benefits for enterprises, from the perspective of the long-term development of the orthopedic industry, volume-based procurement of artificial joints also helps promote standardized industry development.

On the one hand, volume-based procurement can drive a significant reduction in end-user prices, thereby facilitating an increase in industry-wide penetration rates.Currently, the growth of artificial joint replacement surgeries in China has not yet reached a plateau, and price reductions for these products can help increase their penetration rate among patients at the primary care level.

The volume of artificial joint surgeries is still experiencing rapid growth. The volume-based procurement policy, which has reduced the prices of artificial joints, can promote an increase in the penetration rate of joint replacement procedures. According to data from the Chinese Medical Doctor Association, there were 439,324 total hip arthroplasty (THA) procedures, 249,259 total knee arthroplasty (TKA) procedures, and 11,200 unicompartmental knee arthroplasty (UKA) procedures performed in China in 2018. According to data from the American Academy of Orthopaedic Surgeons (AAOS), the United States performed 370,770 hip replacement surgeries and 680,150 knee replacement surgeries in 2014. Relevant data project that the United States will perform 495,140 total hip arthroplasties and 1,078,359 total knee arthroplasties by 2020. Considering the differences in population size between the two countries, there is still significant room for growth in the number of artificial joint replacement surgeries in China.

The growth in surgical volume will also drive the expansion of the artificial joint market. High-value orthopedic consumables are categorized into four major segments: trauma, spine, joints, and sports medicine. According to relevant reports from Biao Dian Information, in China’s orthopedic implantable medical device market in 2019, the trauma, spine, and joint segments collectively accounted for 85.80% of the market share, with the joint segment ranking third at 27.77%. Joint implants are primarily used to treat conditions such as osteoarthritis, avascular necrosis of the femoral head, and rheumatoid arthritis. In 2018 and 2019, the market size for joint implant devices in China was RMB 7 billion and RMB 8.6 billion, respectively; it is projected to reach approximately RMB 18.7 billion by 2024.

On the other hand, the centralized procurement of artificial joints facilitates the transition of orthopedic consumables manufacturers toward standardization and scale, thereby enhancing the market share and competitiveness of leading domestic enterprises.Historically, in the multi-billion-dollar artificial joint market, domestic enterprises started later, allowing foreign manufacturers to dominate. Due to the relatively high technical barriers, complex manufacturing processes, and long service life after implantation, the joint implant market is currently dominated by imported products, with Chinese-made products holding a smaller share. Large foreign medical device manufacturers possess substantial capital, advanced technology, and concentrated talent, having accumulated decades of experience in the research and development of high-end, high-value medical consumables, thereby monopolizing the core technologies of major high-end products. Currently, domestic orthopedic medical device manufacturers need to procure raw materials such as PEEK rods, ceramic femoral heads, and liners, as well as advanced processing equipment like digital automatic sliding headstock lathes, from upstream foreign suppliers when developing and producing high-end products.

Taking raw materials as an example, the core raw materials for domestic orthopedic companies are all dependent on imports. Foreign manufacturers occupy the vast majority of the market share for materials such as medical ceramics, medical titanium alloys, PEEK (polyether ether ketone), cobalt-chromium-molybdenum alloys, and ultra-high molecular weight polyethylene.

Volume-based procurement of artificial joints helps drive an increase in the market share of domestic brands. Meanwhile, although volume-based procurement has reduced the gross profit margins of artificial joint products, it facilitates industry consolidation and benefits leading enterprises among Chinese manufacturers.

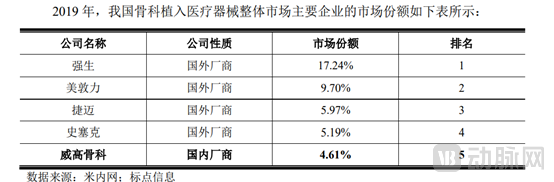

Currently, the domestic orthopedic market features a relatively fragmented competitive landscape, with industry concentration far lower than that of the global orthopedic industry.According to the prospectus of Weigao Orthopedics, based on the number of product registration certificates, there are currently approximately 370 manufacturers in China’s orthopedic medical device market, including about 270 domestic enterprises, resulting in a relatively fragmented competitive landscape. Although domestic companies outnumber foreign ones, most operate on a smaller scale and still lag behind multinational giants in terms of market competitiveness. Large multinational corporations from developed countries such as Europe and the United States continue to dominate the Chinese market, leveraging their strong technological advantages, brand influence, and capital strength, with a combined market share exceeding 60%. The artificial joint market is similarly dominated by imports; in 2019, four companies—Zimmer, Johnson & Johnson, Link Orthopaedics, and Smith & Nephew—accounted for more than 40% of the total market share. No domestically produced company held a market share exceeding 10%.

2019 Market Share of Major Players in China’s Artificial Joint MarketSource: Weigao Medical Prospectus

Volume-based procurement will undoubtedly force industry consolidation, change the current low concentration of the medical device industry, create brands with international influence, and participate in international competition. It is beneficial to advantageous manufacturers with larger operating scales and higher industry rankings within the industry.

Judging from the bid results, the elimination rate in the centralized procurement of artificial joints was not high, with a large number of successful bidders. The industry as a whole expressed broad satisfaction, creating the superficial impression that there were no losers.However, judging from the bidding results in Group A, AK Medical and Weigao Medical emerged as the biggest winners among the top three domestic manufacturers, securing winning bids across all products in Group A;Chunli Medical’s knee joint products failed to win bids in the tender. Among the three multinational giants, Johnson & Johnson and Zimmer Biomet secured winning bids for their entire Group A product lines; Smith & Nephew succeeded with its ceramic-on-ceramic hip joint systems. How will this outcome affect the market positions of key players in China’s domestic orthopedic artificial joint market?

For AK Medical, its low-price strategy has consolidated its leading position in the joint replacement market.Artificial joints are AK Medical’s core business. According to AK Medical’s 2020 annual report, its operating revenue in 2020 was RMB 1.035 billion, with revenue from orthopedic implant products—primarily joint replacements—amounting to RMB 1.007 billion, accounting for 97.26% of the total. Demonstrating a strong determination to secure market share even at the cost of significant margin compression in the national volume-based procurement (VBP) program, AK Medical quoted RMB 6,890 for ceramic-on-ceramic hip joint systems, the lowest price in this category. For ceramic-on-polyethylene hip joint system products, AK Medical also offered a low price of RMB 6,290. In the knee joint product system category, AK Medical continued its low-price strategy with a bid of RMB 4,599. This aggressive pricing strategy ensured that AK Medical won bids across all product lines in Group A.

Chunli Medical Suffers Major Setback with Knee Joint Loss; Joint Business May Face Pressure. Chunli Medical, another leading joint implant manufacturer, failed to win bids for its knee joint systems. In Group A of the hip joint category, only its ceramic-on-ceramic hip joint product system was successful. In the bidding unit for Group A knee joint systems, Chunli Medical submitted the highest quote at RMB 7,980, and this relatively high pricing led to its failure to secure the bid. The quoted price for Chunli’s ceramic-on-polyethylene hip joints was RMB 7,900, while that for ceramic-on-ceramic hip joints was RMB 8,000. Overall, its pricing strategy leaned toward the higher end. According to Chunli Medical’s 2020 annual report, its main business revenue in 2020 amounted to RMB 938 million, with joint prosthesis products accounting for 97.03% of main business revenue and spinal products representing 2.96%. As Chunli, whose core business focuses on artificial joints, did not win bids across all categories in Group A of this centralized procurement, its future business growth may rely more heavily on its spinal product line.

Weigao Orthopedics Adopts a Steady Approach, with Joint Business Share Set to Rise.Notable companies in this centralized procurement round also include Weigao Orthopaedics. According to 2019 data, Weigao Orthopaedics ranked third in the artificial joint market, yet it achieved a remarkable turnaround in the centralized procurement of artificial joints by winning bids across all categories in Group A. In terms of product portfolio, Weigao Orthopaedics has established comprehensive coverage across various sub-segments, including spine, trauma, and joints. According to its 2021 interim report, in the first half of 2021, Weigao Orthopaedics’ spinal products generated sales revenue of RMB 496 million, a year-on-year increase of 33.94%, securing the largest domestic market share for spinal products; trauma-related products recorded sales revenue of RMB 311 million, up 28.27% year on year; and joint products achieved sales revenue of RMB 260 million, representing a 37.75% year-on-year growth. It is anticipated that, leveraging its strong performance in the centralized procurement of artificial joints, Weigao Orthopaedics will capture a larger market share in the joint products segment in the future, thereby reshaping the competitive landscape of the joint industry due to centralized procurement.

Among imported brands, Johnson & Johnson is considered the biggest winner. The company secured winning bids across all categories in Group A for hip and knee joint prostheses. Johnson & Johnson holds leading market shares in orthopedic trauma, spine, and joint reconstruction. In 2020, its orthopedic medical device division generated $7.63 billion in sales revenue. In the Chinese market, Johnson & Johnson ranks first in market share for orthopedic implants.

In this volume-based procurement round, Johnson & Johnson strategically positioned itself with competitive bids: its ceramic-on-ceramic hip joint system was priced at approximately RMB 8,000; the ceramic-on-polyethylene hip joint system was also quoted around RMB 8,000; and the metal-on-polyethylene system exceeded RMB 8,000. For knee joint products, Johnson & Johnson’s quotes were relatively higher, surpassing RMB 7,000. Industry insiders regarded Johnson & Johnson’s pricing strategy as well-calibrated and reasonable, enabling it to secure winning bids across its entire product portfolio. This outcome positions the company more advantageously in future competition against other imported brands such as Zimmer Biomet and Stryker.

From a corporate perspective,Ultimately, companies that emerge as the final winners in centralized volume-based procurement (VBP) tend to have relatively rich product portfolios. A diversified product lineup serves as the foundation for mitigating VBP-related risks, while companies relying on a single product line face significant disadvantages in the VBP process. As high-value orthopedic consumables enter the era of centralized procurement, only a comprehensive and diverse product portfolio can ensure a company’s industry standing.Promoting consolidation and development within the orthopedics industry is also one of the original intentions behind the implementation of centralized procurement. Overall, the advancement of centralized procurement for orthopedic consumables is conducive to the long-term, healthy development of the orthopedic consumables industry and facilitates the transformation of orthopedic consumables enterprises toward standardization and scale.