Who's Next in the Internet Healthcare IPO Surge?

The sudden outbreak of the pandemic has pressed the accelerator on the development of internet healthcare.

Since 2020, multiple companies in the internet healthcare sector have sequentially reached the initial public offering (IPO) stage. In December 2020, JD Health officially listed on the Hong Kong Stock Exchange; as the first profitable internet healthcare enterprise to go public, it significantly boosted industry confidence. In April this year, WeDoctor, which filed its IPO prospectus, sparked widespread industry discussion as the first listed digital healthcare company. At the end of August, Zhiyun Health, which submitted its prospectus for listing in Hong Kong, once again drew considerable attention from the industry.

Currently, the internet healthcare sector has already seen the listing of companies such as Alibaba Health, Ping An Health (formerly Ping An Good Doctor), and JD Health. As internet healthcare enterprises like WeDoctor and Zhiyun Health successively file their prospectuses, it is foreseeable that the sector is on the verge of a wave of initial public offerings.

Amid the current wave of internet healthcare companies going public, who will be the next to file an IPO application? This is a thought-provoking question. Yet of greater concern is why internet healthcare firms are now rushing to list on stock exchanges, and which types of such companies are likely to go public more rapidly.

Surging Demand and Strengthened Regulation: Internet Healthcare Companies Welcome a Wave of IPOs

Internet healthcare companies are poised to experience a wave of initial public offerings (IPOs). This judgment is based not merely on the aforementioned surface-level indicators, but is closely tied to the current development trajectory of the internet healthcare sector. The sustained growth in demand for online medical services, the increasingly robust regulatory framework, and the gradual maturation of internet healthcare enterprises have all contributed to this IPO surge.

Growth in Demand for Medical Services

First, from the perspective of medical services, obstacles to offline medical consultations during the pandemic accelerated the shift of patients to online channels and further stimulated demand for online medical services. After the epidemic stabilized, the continuous expansion of medical services helped maintain user stickiness and activity levels on internet healthcare platforms. Public demand for medical services has extended beyond hospitals to out-of-hospital settings and homes; however, many needs related to post-diagnosis, post-examination, post-surgery, and post-discharge care remain inadequately met. The growing demand for integrated online-offline medical services has further driven the development of internet healthcare enterprises.

During the pandemic, to prevent cross-infection resulting from in-person medical visits, a large number of hospitals suspended their outpatient services. However, many patients, including those with chronic diseases requiring long-term medication, still had substantial demands for medical services. Some public hospitals that previously lacked online operations launched internet-based diagnosis and treatment services by establishing their own internet hospitals or joining third-party internet healthcare platforms. Meanwhile, third-party internet healthcare platforms attracted more users by offering free online consultations during the pandemic. Recognizing the opportunities presented by the pandemic, internet platforms expanded from non-direct medical services into healthcare offerings such as online consultations, thereby reaching a broader user base.

However, as Zhu Shunyan, CEO of Alibaba Health, pointed out, most institutions are not well prepared to handle the surge in user demand. In his view, further expansion of services in the public health sector can address the decline in user engagement after the pandemic stabilizes, improve retention rates among users of online medical services, and attract new users to adopt convenient internet-based healthcare services.

Regulatory Policies Are Becoming Increasingly Comprehensive

Secondly, from a regulatory perspective, given the unique nature of the healthcare industry, both pharmaceutical sales and distribution within the internet healthcare sector and online diagnosis and treatment services require regulatory policies to guide corporate development. From the standpoint of regulatory policy, whether through the refinement of detailed rules or the guidance of strategic direction, the overall trend is favorable for the development of internet healthcare.

For instance, the relatively mature pharmaceutical e-commerce model is itself influenced by policies on “online sales of prescription drugs.” Last November, the General Office of the National Medical Products Administration publicly released the Measures for the Supervision and Administration of Online Drug Sales (Draft for Comment), which provided direction on the online sale of prescription drugs by permitting their online sale and the display of prescription drug information. In April this year, the General Office of the State Council issued the Opinions on Furthering Reforms to Streamline Administration, Delegate Powers, Improve Regulation, and Upgrade Services to Support the “Six Stabilizations” and “Six Guarantees,” explicitly stating that “prescription drugs, except those under special state management, may be sold online provided that the authenticity and reliability of electronic prescriptions are ensured.” The lifting of restrictions on online sales of prescription drugs holds significant implications for the internet healthcare industry.

In terms of medical services, obstacles to further development are being cleared away, whether through the standardization of online medical diagnosis and treatment services or the integration of health insurance reimbursement.

In July 2018, three administrative measures and standards concerning online diagnosis and treatment, internet hospitals, and remote medical services were issued. These regulations clarified that the scope of online medical services is limited to follow-up consultations for common diseases and chronic conditions; such services must be provided by medical institutions holding a “Medical Institution Practicing License”; and provincial health authorities are required to establish regulatory platforms for online medical services to oversee their implementation. These initiatives have provided a policy basis for the orderly conduct of business by internet healthcare enterprises.

During the pandemic, the Wuhan Healthcare Security Administration announced 18 measures to support epidemic prevention and control as well as routine medical care coverage. The most notable among these was the inclusion of “Internet+” medical services in the scope of medical insurance reimbursement. Various regions subsequently introduced policies to incorporate Internet-based medical services into medical insurance payment schemes, further driving user adoption of such services. In November 2020, the issuance of the Guiding Opinions on Actively Promoting Medical Insurance Payment for “Internet+” Medical Services further clarified specific measures for integrating Internet-based medical services into the medical insurance reimbursement system.

In June this year, the General Office of the State Council issued the “Opinions on Promoting High-Quality Development of Public Hospitals,” requiring public hospitals to shift from “scale expansion” to “quality improvement and efficiency enhancement,” strengthen innovation in systems, technologies, models, and management, and proposed increasing the proportion of medical service revenue (excluding revenue from drugs, consumables, examinations, and laboratory tests) in total medical revenue. This provides a policy basis and guarantee for many enterprises that collaborate with hospitals to deliver innovative services.

The implementation of policies on online sales of prescription drugs, the standardization of internet-based medical services, the integration of health insurance payments, and incentives to increase revenue from medical services have collectively accelerated the rapid development of internet healthcare as policy frameworks continue to improve.

Corporate development is becoming increasingly stable.

The growing demand for online medical services, coupled with increasingly comprehensive policy regulations, has further facilitated the development of internet healthcare enterprises. From the perspective of corporate development, how can we assess whether a company is gradually achieving stability? We may refer to another indicator: investment in the primary market. Companies with more stable development tend to attract greater capital attention and secure substantial investment.

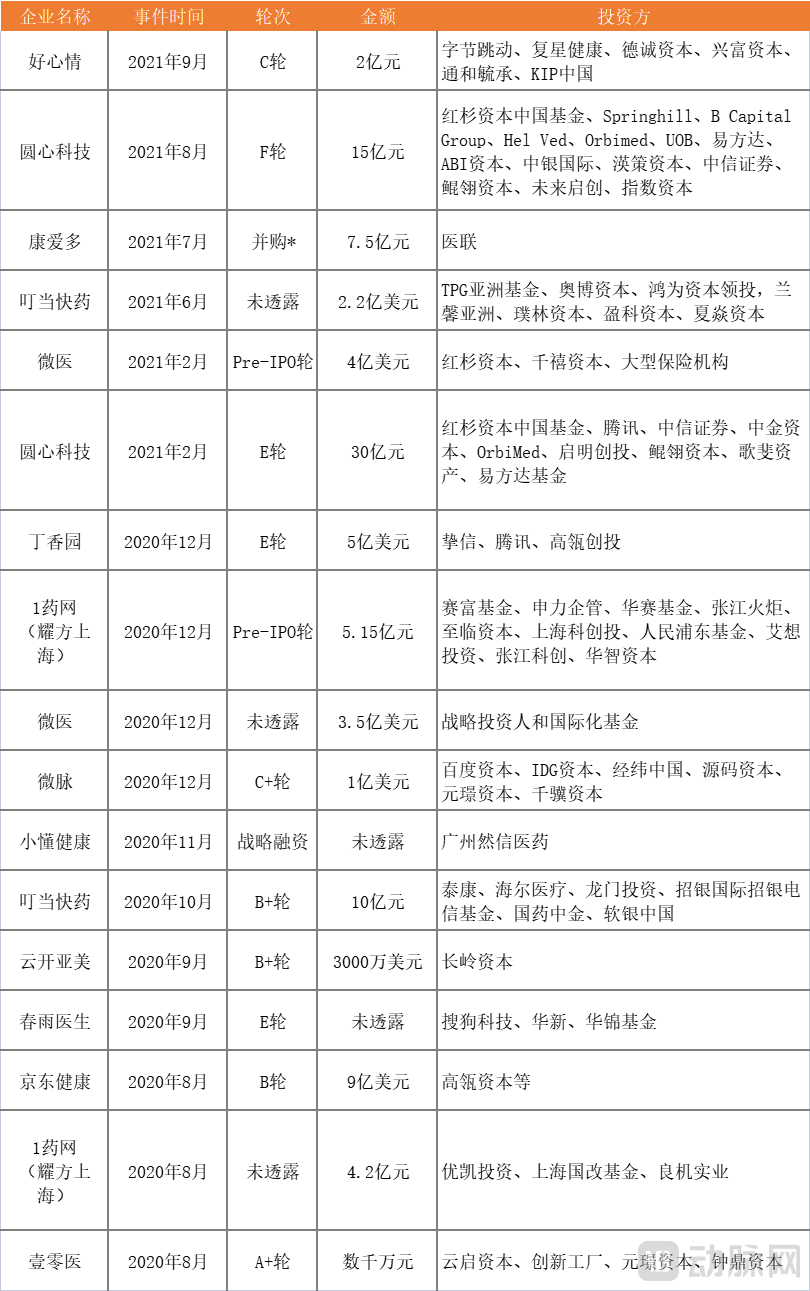

Statistics on financing and M&A activities in the internet hospital sector over the past year, based on internet medical platforms that have established their own internet hospitals. Source: VCBeat’s “2021 Internet Hospital Report”

According to data compiled by VCBeat, investment and financing activities in the internet healthcare sector continue to unfold, with leading companies securing larger funding rounds. Over the past year, most companies that received investment were at Series C or later stages; some companies have also expanded their business layouts through mergers and acquisitions. For instance, Weimai has reached Series C+, securing $100 million in December last year. Yilian, now at Series D, completed the acquisition of Kangaiduo for RMB 750 million this July. Dingxiangyuan, at Series E, raised $500 million. Chunyu Yisheng completed its Series E financing last September, with the specific amount not disclosed to the public.

Companies in later-stage financing rounds are frequently rumored to be on the verge of entering the IPO market. For some, plans to file prospectuses have already been scheduled; for instance, Yuanxin Technology, which completed its Series F financing in August this year, submitted its application to the China Securities Regulatory Commission (CSRC) in the same month and may list in Hong Kong. Moving into the secondary market has become their common choice, which can also be viewed as a natural outcome of the current development in the internet healthcare sector. The only remaining question is: what type of companies will be the next to go public?

Leveraging Superior Resources to Deepen Offline Hospital-Enterprise Collaborations

To analyze the types of internet healthcare companies that are likely to go public, we may need to look back at those already listed and identify certain similarities and differences among them.

Leveraging the Group’s Advantageous Resources

Alibaba Health, which released its annual report for the 2021 fiscal year this June, aims to further upgrade the “Internet + Healthcare” industry by building an online medical information community integrated with pharmaceutical and health services to address the pain point of medical information asymmetry. Last September, Alibaba Health rebranded and launched the Yilu App to further develop its online medical information community and tackle challenges related to healthcare information access and awareness.

Currently, the monthly active users of the Yilu App have reached 1 million. The annual active users of the Alipay Medical and Health channel stand at 520 million, providing a foundational guarantee for Alibaba Health’s construction of an internet-based medical information community. The number of active users on the Tmall Pharmaceutical platform has also reached 280 million. Leveraging the support of Alibaba Group, Alibaba Health can rapidly establish its business model, achieving a complete closed loop from awareness to experience in its internet medical information community and pharmaceutical health services.

Ping An Health (formerly Ping An Good Doctor), which aims to build a professional bridge between doctors and patients, mentioned in its interim report that its cumulative registered users have reached 400 million. Currently, Ping An Health is providing high-value medical and health management services to payers in the industry, including commercial insurance, medical insurance, enterprises, and individuals, through the HMO model. By delivering timely, high-quality, and efficient services, it enhances users' perceived value and stickiness, thereby generating platform bargaining power.

Ping An Group, long regarded as the backbone of Ping An Health, currently provides products and services to 230 million individual customers and 627 million internet users. Among its individual users, 62% also utilize services offered by the healthcare ecosystem. Ping An Health has achieved business synergy with Ping An Group. According to Ping An’s annual report, these users exhibit higher growth in both average contracts per customer and average assets under management (AUM) per customer compared to individual customers who do not use the healthcare ecosystem services.

Positioned as a “health management platform centered on the supply chain, leveraging medical services as its core offering, and driven by digital technologies to cover users’ entire lifecycle and all scenarios,” JD Health had reached 109 million active users as of June 30, representing an increase of 18.8 million from the end of last year, with daily consultations exceeding 160,000. Backed by JD.com, which boasts a large base of high-quality users with health and medical needs, JD Health benefits from strong synergies. Currently, JD.com’s annual active users have grown to 531.9 million.

On the other hand, JD Health is leveraging its robust pharmaceutical supply chain and continues to expand its network for specialty and innovative drugs, further strengthening its core capabilities and enhancing user experience. The logistics and delivery network of JD Group also provides additional support for the development of JD Health.

Obviously, the advantages of the group’s resources are not only reflected in user protection and other aspects; more importantly, they lie in the synergy between healthcare services and other business segments.

Offline Deployment of Hospital-Enterprise Collaboration

Earlier this year, wePostIt is pointed out that, with ample capital and a large user base, internet healthcare companies are accelerating their offline expansion.

On the one hand, public hospitals are accelerating their online presence, putting pressure on internet healthcare platforms; collaborating with offline hospitals has become a reasonable strategy to secure a steady user base. On the other hand, although internet healthcare services have been included in the scope of medical insurance reimbursement, coverage is primarily granted to internet hospitals that are locally integrated into the medical insurance system. The establishment of internet hospitals relies on physical medical institutions, which has further driven companies like Ping An Health to expand their offline hospital networks in cities such as Wuhan, Yinchuan, and Dongguan during the pandemic, thereby enabling integration with medical insurance payment systems.

Furthermore, online internet medical platforms themselves need to consider differentiated competition. To better manage patients and strengthen offline collaboration, providing differentiated offline service products has become a key factor for internet medical platforms to comprehensively consider.

Moreover, the inherent “seriousness” of the healthcare industry sets it apart from other sectors. To ensure that online medical consultations demonstrate their value through tangible outcomes and therapeutic efficacy, standardization of such services is of paramount importance. Companies like JD Health are increasingly collaborating with top-tier experts to establish standardized pathways for online disease diagnosis, treatment, and management.

Major internet healthcare platforms, driven by their own strategic considerations, have increasingly opted to deeply integrate offline resources and collaborate with health commissions. For instance, JD Health has signed agreements with cities such as Taicang in Jiangsu Province, while its “Smart Health Beihai” project in Beihai, Guangxi, is being progressively implemented. Ping An Good Doctor built and launched the Fuzhou Regional Internet Hospital Platform for the Fuzhou Municipal Health Commission, and other internet hospital platforms have also successively begun operations. Alibaba Health is actively partnering with offline public health authorities and hospitals, launching specialty centers on its Yilu platform, among other initiatives.

Similar characteristics can also be observed in WeDoctor and Zhiyun Health, both of which have filed prospectuses. Tencent, WeDoctor’s largest shareholder, commands a massive user base, and WeDoctor’s appointment registration services were once featured in the “Nine-Grid” section of WeChat. The involvement of leading domestic insurance institutions such as Taiping Insurance, Ping An Insurance, and Sunshine Insurance in Zhiyun Health’s funding has played a significant role in integrating its chronic disease management services, particularly for diabetes. Offline, both WeDoctor and Zhiyun Health are connecting with and covering hospitals across multiple regions.

For instance, Weimai, which introduced Baidu Ventures (BV) in its Series C+ round, can be expected to benefit from support in advantageous resources such as AI technology and search engine entry points. Similarly, companies closely affiliated with Tencent, such as Medlinker, Yuanxin Technology, and DXY, have all received backing in the form of traffic and resources from internet giants. Chunyu Yisheng, a somewhat special case, has seen investment from Sogou. With Tencent’s acquisition of Sogou now complete, Chunyu Yisheng will indirectly become part of Tencent’s healthcare strategic landscape.

Regarding offline business expansion, current internet healthcare companies have not made extensive disclosures. In their collaborations with offline public hospitals, these enterprises primarily focus on assisting hospitals in achieving internet-based operations or leveraging their own strengths to build an "Internet+" full-course management and service system centered around public hospitals. For example, Medlinker currently covers multiple disease specialties, including oncology, cardiovascular and cerebrovascular diseases, diabetes, and respiratory conditions, with hundreds of thousands of registered doctors providing home-based disease management for patients. Weimai currently operates in over 30 provinces, partnering with nearly 2,000 hospitals, and a large number of doctors on its platform offer various healthcare service SKUs.

These data may serve as a footnote to internet healthcare companies on the verge of going public.

The Second Half of Internet Healthcare: Moving Toward the Core of Medical Care

After years of development, internet healthcare has become increasingly standardized and has gradually moved from relatively peripheral services—such as appointment scheduling, medication delivery, and online consultations—into the core of medical care, which is oriented toward patient treatment outcomes.

As the supply-side resource, physicians play an undeniably critical role in the delivery of medical services. To better optimize patient care, internet healthcare platforms are gradually exhibiting two trends in their approach to “physician digitalization.”

One trend is to maximize the online presence of physicians.

This signifies intense competition among internet healthcare platforms for physician resources, which in turn hinges on how these enterprises manage their relationships with hospitals. In the process of transitioning physicians to online practice, companies that assist hospitals in improving quality and efficiency while further expanding their service scope undoubtedly possess greater opportunities.

This is not merely a matter of helping hospitals achieve in-house digitalization, build internet hospitals, and provide online access. The more critical issue lies in how to optimize resource allocation to realize disease and health management across the entire patient journey and life cycle. Most internet healthcare companies have indeed recognized this challenge; when building their ecosystems, they often choose to expand from the hospital side. For instance, Zhiyun Health installs its Zhiyun SaaS system in hospitals to help address in-hospital chronic disease management for patients, demonstrating its value through tangible results.

Founded in 2015, Yuanxin Technology has centered its operations on localized doctor-patient connectivity, gradually developing a business matrix that includes Miaoshou Doctor, Yuanxin Grand Pharmacy, Yuanxin Huibao, and Yuanxin Medical Technology. Currently, the company is building an out-of-hospital disease management network and an in-hospital digital smart service network. Leveraging these two networks, it provides patients with one-stop solutions for medical care, medication, and payment, featuring integration between in-hospital and out-of-hospital settings as well as online and offline channels.

Another trend is the reliance on evidence-based “digital therapeutics” to reduce dependence on physicians themselves.

The same symptom can lead to different disease diagnoses from Doctor A and Doctor B. This has been one of the most criticized issues on past internet healthcare platforms. Standardizing the diagnosis and treatment processes and pathways in online healthcare is a persistent commitment upheld by companies dedicated to rigorous medical practice—such as JD Health and Medlinker, which are developing standard operating procedures (SOPs) for disease management to regulate the online diagnostic and treatment process to the same standards as offline care.

Centered on the development of specialty-specific and digital disciplines, Medlink has established Standard Operating Procedures (SOPs) for online management of single diseases under the guidance of experts across various specialties. By integrating clinical guidelines and clinical pathways, these SOPs enable the provision of targeted treatment plans tailored to changes in patients’ disease progression.

There is still considerable room for expansion in the healthcare sector, both online and offline.

Hospital electronic medical record (EMR) data and real-world data (RWD) have not been effectively integrated, making it difficult to apply them in clinical treatment and rehabilitation. Hospitals face challenges such as insufficient medical staff, which hinders the continuous improvement of patient management compliance and effectiveness. These issues need to be addressed through more digital and intelligent solutions. While the adoption of internet technologies like artificial intelligence has indeed improved physicians’ efficiency to some extent, this is far from sufficient.

In 2021, the entire industry was abuzz with excitement over “digital therapeutics.” As intervention programs driven by software applications and grounded in evidence-based medicine, digital therapeutics can be used either as a standalone treatment or in conjunction with pharmaceuticals, medical devices, or other therapies to treat, manage, or prevent diseases. The emergence of digital therapeutics has revealed new opportunities and directions for the industry, and some internet healthcare companies have already embarked on profitable explorations in this field.

In May this year, Weimai and Miaojiankang, as the first Chinese enterprises to receive certification from the Digital Therapeutics Alliance (DTA), conveyed new messages to the industry. Addressing certain issues prevalent in hospitals, companies like Weimai have proposed a novel digital therapeutics architecture based on integrated in-hospital and out-of-hospital data. By linking public hospital electronic medical records (EMR) with post-discharge real-world data (RWD) from the “Weimai Comprehensive Management” service system, they provide patients with whole-course, full-lifecycle management services.

Miao Health has built a digital therapeutics platform for lifestyle intervention in chronic diseases, leveraging the integration of the Internet of Things (IoT) and artificial intelligence. Its digital therapeutics primarily target chronic conditions such as diabetes, hypertension, and medical obesity, with “active intervention technology” comprising key components including data collection, disease risk prediction and analysis, and health interventions.

Undoubtedly, the application of digital therapeutics serves to complement and optimize traditional treatment modalities, delivering significant value to patients, healthcare providers, payers, and pharmaceutical and medical device companies.

Unceasing Exploration of Healthcare Services

Behind the wave of IPOs among internet healthcare companies lies the fact that the industry has reached a certain stage of development. In the face of numerous internet healthcare firms rushing to go public, we should perhaps adopt a more balanced perspective. The issues worthy of our attention may lie in the following two aspects:

On the one hand, as internet healthcare initiatives in China progressively enter a more complex and advanced stage, it remains imperative for internet healthcare enterprises to engage in in-depth deliberation on how to reach the core of medical services. Specifically, they must provide outcome-oriented online healthcare services focused on treatment and management results, genuinely alleviate the burden on the healthcare system, and better facilitate health-to-disease management for users of internet healthcare platforms.

On the other hand, with the emergence of novel innovations such as digital therapeutics, how can we appropriately adopt these emerging solutions to better serve patients and gain broader acceptance among the patient population? How can we further explore the integration of emerging technologies with healthcare services?

These are all issues that internet healthcare companies need to reflect on and address.