Billion-Dollar Digital Chronic Disease Management Market Supported by 300 Million People: How Global and Chinese Leaders Are Operating

Since the pandemic, chronic disease management has remained a "trending topic" in the healthcare industry.

According to data from the VCBeat database,In 2020, there were 62 investment and financing events in China's digital chronic disease management sector, with a total financing amount of approximately RMB 10 billion, representing a year-on-year increase of nearly 60%.

In 2021, the market heat continued to rise. According to statistics,In the first half of 2021, financing for digital chronic disease management companies in China reached RMB 3.055 billion, a year-on-year increase of approximately 264%.

In this wave of investment, apart fromSequoia Capital, Matrix Partners China, China Renaissance, IDG Capitalin addition to increased investments from a host of well-known investment institutions,Tencent, Baidu, JD.com, Ping AnIndustry giants have also shown great interest in the field of chronic disease management, entering the market directly or indirectly through various approaches.

The primary market is undoubtedly hot, but the secondary market has not been “idle” either, with China’s first stock in this sector about to be born. On August 27, China’s largest provider of digital chronic disease management solutions—Zhiyun Health Technology Group(hereinafter referred to as “Zhiyun Health”) has formally filed its prospectus with the Hong Kong Stock Exchange, and the profile of the “Chinese model” in the field of chronic disease management is gradually becoming clear.

The emphasis on the “China model” stems from the fact that, in the field of chronic disease management, the “US model” was the first to emerge globally. Typical representatives include Livongo, the first publicly traded company in global mobile chronic disease management, and WellDoc, the first diabetes management software to receive FDA clearance.

Surprisingly, these “successful models” widely recognized by the industry have not flourished across China’s chronic disease management market. What are the underlying reasons? How have Chinese chronic disease management companies, diverging from the “U.S. model,” carved out localized pathways? Where exactly do the differences between the Chinese and U.S. chronic disease management models lie? To answer these questions, VCBeat has conducted an analysis of the chronic disease management sectors in both countries.

"The U.S. Chronic Disease Management Model" on the Fringes of Commercial Insurance

Before establishing a service model, it is essential to first identify who the actual “payer” is.

It is reported that the United States has a highly developed commercial insurance market, with a commercial insurance coverage rate as high as 80%. In the past two years, annual commercial insurance expenditures have accounted for 10% of the nation’s GDP. Among these commercial health insurance plans, 90% are provided by employers for their employees. Regarding payment, employers cover 80% of the insurance premiums, while employees are responsible for the remaining 20%.

Under such a system, insurers naturally aim to minimize medical expenditures for corporate employees. However, compared with healthy employees, those with chronic conditions account for the bulk of insurers’ payouts. Insurers must not only cover the costs of their current treatments but also face substantially higher expenses from hospitalizations if these conditions are poorly managed.Therefore, insurance companies will inevitably provide “priority protection” to employees with chronic diseases, aiming to minimize medical expenditures at the source.

From this perspective, insurance companies and employers (policyholders) actually share aligned interests. When insurers are confident that expenditures are reduced and controllable, they will inevitably return a portion of the benefits to employers in some form. Furthermore, for employers, improved employee health can reduce absenteeism and other work-related time losses.

As the first publicly listed company in the global chronic disease management sector, Livongo identified the pain points within the U.S. healthcare system from its inception and built a systematic solution around them.

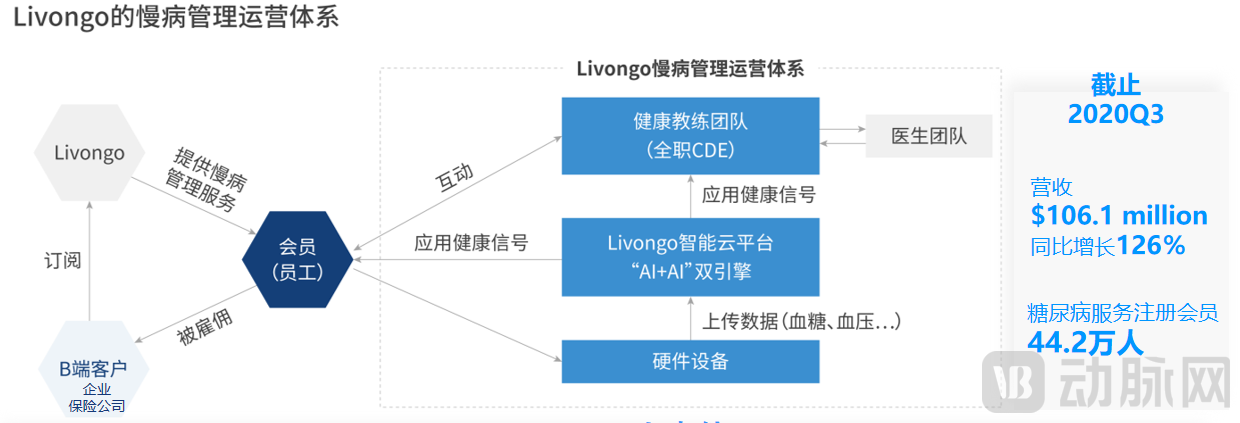

Figure 1: Livongo's Operational System for Chronic Disease Management

Specifically,In response to the demands of insurers and employers, Livongo introduced the concept of “Applied Health Signals.” Its business model primarily leverages an “AI + AI” intelligent system to provide integrated health management services for patients with chronic diseases, thereby addressing the challenge faced by U.S. commercial health insurers in controlling costs.

The AI referred to here is not the currently popular artificial intelligence in China; “AI+AI” actually stands for Aggregate, Interpret, Apply, and Iterate.

This is a continuous, iterative process. By leveraging hardware and human physiological data obtained from various channels, along with received feedback signals, Livongo can provide targeted guidance and recommendations to patients with chronic diseases. The program is continuously updated and refined during implementation. Through the integration and analysis of these data, Livongo helps members gain a deeper understanding of their conditions, thereby empowering them to engage more actively in health management.

In essence, Livongo has established a “B2B2C” business model, wherein the clients are enterprises that purchase health insurance for their employees, while insurers and pharmacy benefit managers (PBMs) serve as channel partners that help refer customers. The ultimate beneficiaries of Livongo’s innovative services are, in fact, the employees of these enterprises.

Unlike Livongo’s “indirect” approach, WellDoc has adopted a more direct service model.

As the only diabetes management software in the United States with FDA clearance, WellDoc primarily delivers virtualized services. It leverages clinically validated algorithms to extract and analyze users’ disease and health data, then generates personalized treatment guidance through automated processes on its digital platform.

In essence, WellDoc has broken away from the fixed model of traditional online healthcare service companies by “prescribing” its services, with physicians making the final decisions, much like they do for medications. BlueStar is a prescription-only product; its key distinction from conventional products lies in its integration with electronic health record (EHR) systems. It consolidates diabetes tracking data and user information obtained through BlueStar into the EHR, providing physicians with comprehensive data to support clinical decision-making and enable personalized chronic disease management.

Why China’s Chronic Disease Management Cannot “Import” the U.S. Model

Whether it is Livongo or WellDoc, their business models are very clear and simple, but this does not mean that both can be standardized “replicated” in the domestic chronic disease management market.

Taking Livongo as an example, under the U.S. commercial insurance system, it has a clear payer. However, in China, the payment landscape is still dominated by basic medical insurance and critical illness pooling, with out-of-pocket payments and commercial insurance serving only as supplements. Therefore, for domestic chronic disease management companies, targeting commercial insurers as their primary clients does not align with the current reality.

Focusing on WellDoc, it is evident that its prescription-based model relies heavily on physicians. However, in China, doctors’ primary focus is on clinical care, leaving them with little time or incentive to engage in patient health management. Furthermore, WellDoc’s approach of integrating with electronic medical records (EMRs) is not feasible in China, as EMR systems remain trapped in hospital information silos, preventing access to clinical data. Meanwhile, health insurance payers are already under significant financial pressure and are unlikely to cover services with uncertain outcomes. Given these factors, even without considering the inherent challenges and developmental limitations of the WellDoc model itself, there is no viable environment for its survival in China.

So, what are the true demands for chronic disease management in China?

This is, in essence, a continuous process of “trial and error.” In the field of chronic disease management, there was once a classic campaign. According to statistical data, during the 2015 boom in mobile health, the number of mobile health apps reached as many as 2,000, with over 700 being diabetes management apps—accounting for approximately 30% of all mobile health apps. This led to an intense competition known as the “Battle of Hundreds of Diabetes Apps” within the single-disease sector of diabetes.

During this period, market entrants primarily aimed to enhance the efficiency and outcomes of diagnosis and treatment for end-users (B2C), targeting consumers directly. However, the actual implementation yielded unsatisfactory results. This was mainly due to significant deficiencies in the diagnosis, treatment, and management of diabetic patients in hospitals, where the level of informatization was extremely low, making it difficult to accurately record and track patient data in real time.

After identifying the root cause of the problem, chronic disease management companies adjusted their strategies to focus on hospitals (the B-side), targeting pain points such as low efficiency and high error rates in hospital management processes, and began developing in-hospital information systems.

In the face of new market dynamics, leading apps such as Da Tang Yi, Zhiyun Health, Tang Yisheng (Diabetes Doctor), and Tang Hushi (Diabetes Nurse) are accelerating their exploration of business models, marking a shift in the diabetes market landscape from chaotic competition to an era of intense rivalry akin to the Warring States period.

With the rapid development of the mobile health market, the chronic disease management market is gradually maturing. “Pharmacies” and “insurance” are increasingly integrated into the chronic disease management ecosystem. Mobile chronic disease management companies are exhibiting diversified development trends due to differences in management mechanisms, and the closed-loop model of “physicians, patients, pharmacies, and insurers” has given rise to various service models in the field of chronic disease management.

Along this path, the demand for chronic disease management in China has also gradually become clear.First, low efficiency compromises the guarantee of medical services, leading to a significant decline in patients’ healthcare experience. Second, patient adherence is insufficient, with a lack of seamless continuity across the pre-, intra-, and post-treatment phases. Finally, health insurance coverage is inadequate; for instance, in terms of out-of-pocket payments, basic medical insurance and commercial insurance account for 54.7%, while self-pay constitutes 45.3%. There is an urgent need for chronic disease patients to have access to a more effective and cost-efficient payment solution.

To address these issues, “digitalization” may be the optimal solution. AsMs. Yang Wenlin, CPO and Vice President of Zhiyun HealthAs stated, chronic disease management in China is a sector urgently requiring digital transformation. This is evidenced by its large patient population, extended management cycles, and strong demand for personalized care. Through digital technologies, broad intervention can be achieved across multiple stages, including early-stage monitoring, follow-up management, and personalized chronic disease management services, thereby providing patients with convenient access to care across various service touchpoints.

Not Following the U.S. Model: How Should the “Chinese Example” of Chronic Disease Management Be Built?

China has the world’s largest population of individuals with chronic diseases. According to the Report on the Nutrition and Chronic Disease Status of Chinese Residents (2020), in 2019, deaths attributable to chronic diseases accounted for 88.5% of all deaths in China. With the accelerating pace of population aging, this proportion is projected to exceed a striking 90% by 2050. Effectively preventing and controlling chronic diseases and properly guiding patients to improve their personal health have become major challenges facing China’s healthcare sector.

Meanwhile, chronic diseases account for a substantial proportion of healthcare expenditures. In 2020, Chinese patients’ spending on chronic disease management amounted to approximately RMB 4.1 trillion, with the internet-based chronic disease management market sized at RMB 176.1 billion, representing 4.3% of the overall market.

This is a vast blue ocean. How exactly are domestic companies in this sector strategizing their market entry?

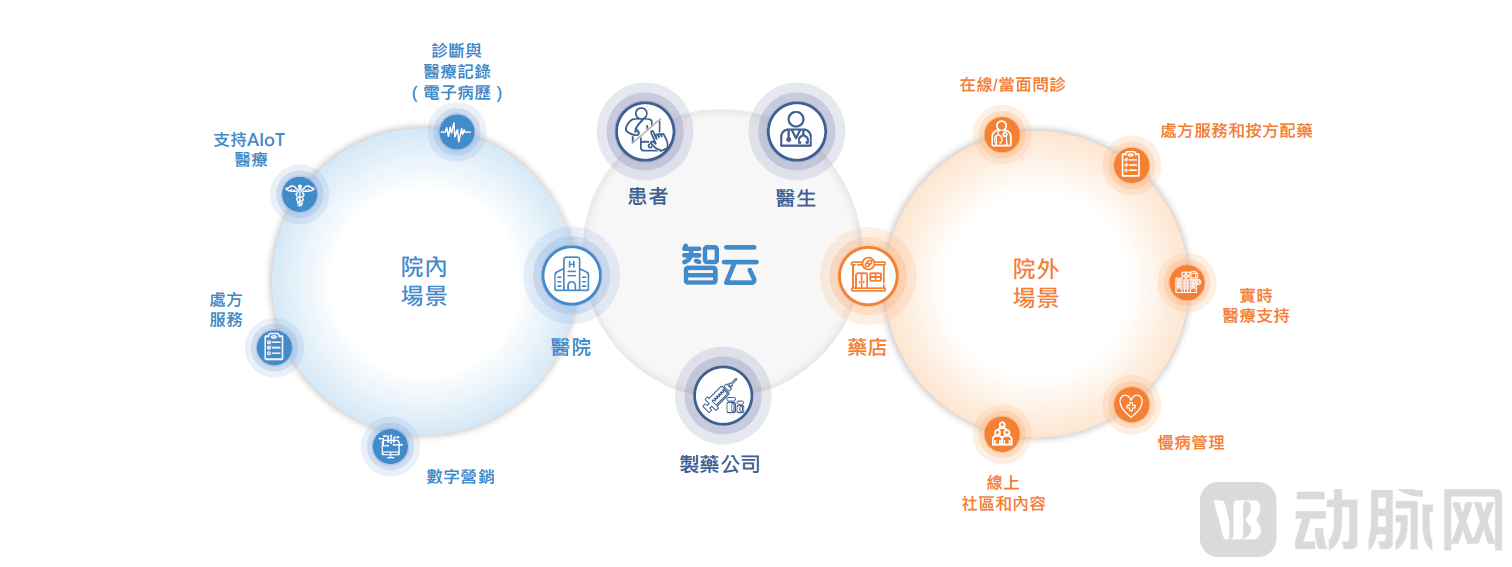

Take SmartCloud Healthcare as an example.As the largest provider of digital chronic disease management solutions in China,Zhiyun Health has established a unique integrated “in-hospital + out-of-hospital” service model, leveraging innovative and scalable solutions to create a powerful network ecosystem effect, thereby further enhancing the efficiency and capabilities of chronic disease management.

Specifically, to address the needs of hospitals, Zhiyun Health has specially developed “Zhiyun Yihui,” the SaaS-based chronic disease management platform with the highest coverage among mainstream hospitals in China, and “Zhiyun Internet Hospital,” the largest online communication and service platform for chronic disease patients, doctors, and hospitals outside clinical settings in China. The former focuses on building platforms for hospitals to enhance their overall operational efficiency, while the latter is dedicated to providing services to patients by strengthening doctor-patient communication to optimize treatment outcomes.

Figure 2: Zhiyun Health’s Business Model

Figure 2: Zhiyun Health’s Business Model

Regarding medications with long-term demand among patients with chronic diseases, Zhiyun Health has meticulously developed the most cost-effective pharmaceutical care service in China—the Zhiyun Health Pharmacy SaaS system, “Zhiyun Consultation”—based on the actual needs of patients and pharmacies. As Zhiyun Health’s third core product, it aims to enhance pharmacy operational efficiency and profitability by providing professional and compliant pharmaceutical and medical services to offline pharmacies. It also establishes and delivers 24/7 health management services across the pharmaceutical community, thereby enabling residents to more conveniently and affordably return to healthy living.

On the consumer side, Zhiyun Health has established a membership service system aimed at delivering multi-tiered health services that combine “platform-based consultations” with “community-based health management guidance,” thereby addressing patients’ precise, complex, and long-term practical needs and providing valuable medical services.

In addition, Zhiyun Health focuses on digital marketing services. By integrating information exchange across multiple scenarios, Zhiyun Health has successfully extended from the chronic disease management value chain to connect with the industrial side, including pharmaceutical and medical device manufacturers. This enables the identification and fulfillment of pharmaceutical demands, ensures the practical application of professional industrial services within hospitals, and establishes a monitoring system for the safe and rational use of drugs and medical devices.

It is evident that Zhiyun Health’s focus on chronic disease management remains centered on “empowerment.” By leveraging a digital platform and innovative service models, the company drives the efficient operation of its closed-loop service ecosystem, enabling physicians to manage patient health more conveniently and allowing patients to access optimal medical care.

This business model has attracted significant attention from the capital markets. To date, Zhiyun Health has completed multiple rounds of financing over its seven years since inception, raising a cumulative total of more than RMB 3.5 billion, with annual fundraising exceeding RMB 1 billion in both 2020 and 2021. Notably, several renowned domestic and international investment firms—including SIG, IDG Capital, CICC Capital, CMB International, and Matrix Partners China—have participated in more than two subsequent funding rounds, reflecting their continued confidence in Zhiyun Health’s business model.

“China-US Samples” Data Comparison: Whose Localization Path Is More Grounded?

Livongo, the first publicly listed company in the global chronic disease management sector, represents a typical “U.S. model.” In contrast, Zhiyun Health, which has filed its prospectus and is poised to become China’s first publicly listed chronic disease management company, embodies the “China model.” Due to differences in market systems, their business models differ significantly.

However, this is merely superficial; by examining the financial data, we can discern more concrete differences between the two.

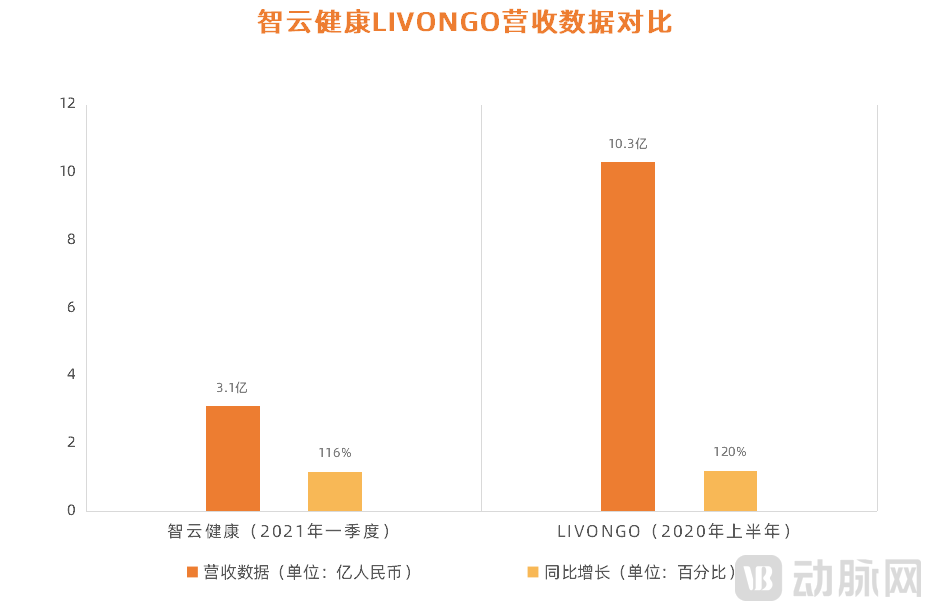

First, in terms of revenue, both are experiencing a period of rapid growth.According to the prospectus, Zhiyun Health’s revenue in the first quarter of 2021 reached RMB 310 million, representing a year-on-year increase of 116%. In comparison with Livongo, using pre-acquisition data as the baseline, Livongo’s revenue in the first half of 2020 was USD 160 million (approximately RMB 1.03 billion), reflecting a year-on-year growth rate of 120%.

Figure 3: Comparison of Revenue Data Between Zhiyun Health and Livongo

Figure 3: Comparison of Revenue Data Between Zhiyun Health and Livongo

Following the acquisition, Livongo has maintained its strong profitability, emerging as a new “growth pole” for Teladoc’s revenue. According to the semi-annual report released in August, Teladoc’s revenue for the first half of 2021 reached $957 million (approximately RMB 6.15 billion), representing a year-on-year increase of 126.83%.

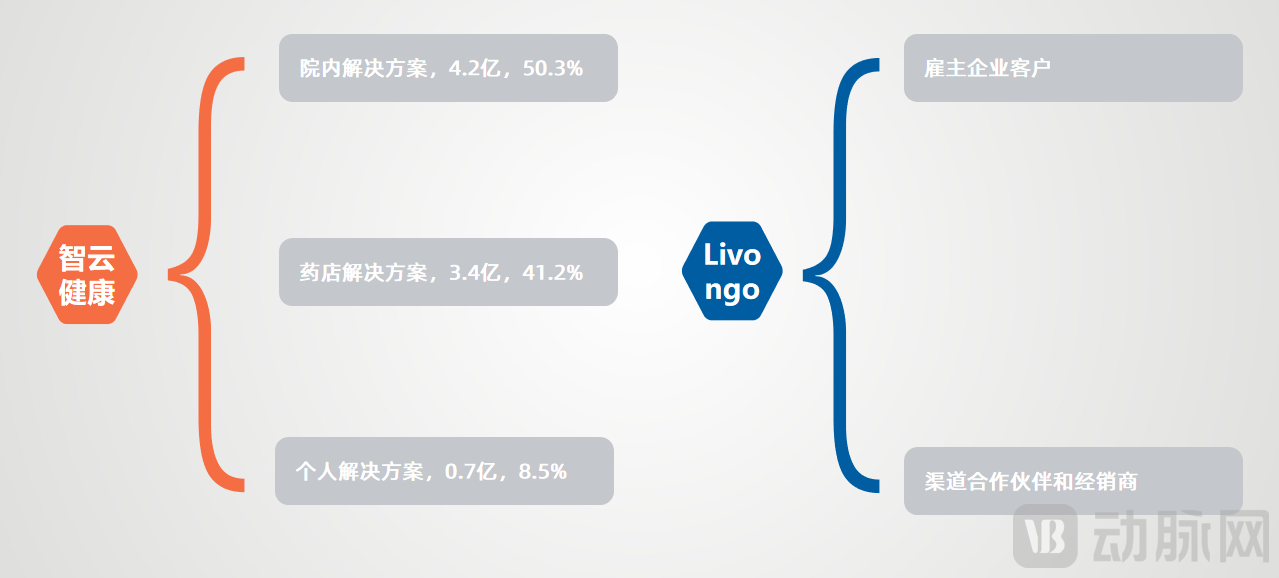

Secondly, in terms of profitability, Zhiyun Health relies on its three core business segments, whereas Livongo’s primary payers are employer clients.Zhiyun Health’s revenue streams are primarily derived from three segments: in-hospital solutions, pharmacy solutions, and personal chronic disease management solutions. According to the prospectus, in 2020, Zhiyun Health’s “in-hospital solutions,” “pharmacy solutions,” and “personal chronic disease management solutions” generated revenues of RMB 420 million, RMB 340 million, and RMB 70 million, respectively, accounting for 50.3%, 41.2%, and 8.5% of total revenue. Notably, in 2020, “in-hospital solutions” surpassed “pharmacy solutions” to become Zhiyun Health’s largest profit contributor.

Figure 4: Comparison of Payers between Zhiyun Health and Livongo

Figure 4: Comparison of Payers between Zhiyun Health and Livongo

Unlike iHealthCloud, Livongo’s current sales revenue is derived from employer clients that implement self-insured health plans. The top five channel partners—Express Scripts, CVS Pharmacy, Health Care Service Corporation, Anthem, and Highmark—account for 50% of total revenue. Additionally, Livongo has entered into cooperation agreements with two major pharmacy benefit managers (PBMs), Express Scripts and CVS. In terms of revenue composition, Livongo does not rely on individual users but rather on a limited number of channel partners and distributors, which contribute a significant proportion of its total sales.

Finally, in terms of growth drivers, “patient traffic” increased significantly, and Zhiyun Health added multiple paid services.Livongo’s membership fees continued to rise. By the end of 2020, Zhiyun Health’s in-hospital SaaS platform and “Zhiyun Health Pharmacy SaaS” had been adopted by 1,705 hospitals and 110,000 pharmacies, respectively, while the number of paying individual users increased to over 360,000.

Like Zhiyun Health, Livongo is also in a period of rapid business expansion. In the first half of 2020, the number of client organizations increased to 1,328, and the member base reached 410,000. Although this accounts for just over 1% of the diabetic population in the United States, the growth momentum is quite strong.

Beyond this, the two also differ in certain respects, primarily in their approaches to identifying new growth drivers.For Zhiyun Health, starting in 2020, an increasing number of medical institutions began paying for its SaaS system for chronic disease management. The heightened willingness of pharmacies to pay indicates their recognition of the company’s service model and has fostered long-term dependence on the platform. In addition, new business lines launched in 2020 included digital marketing services tailored for hospitals and membership services for individual users. These new ventures have been key drivers of Zhiyun Health’s revenue growth.

Livongo, on the other hand, focused on optimizing its membership fees. In terms of average annual revenue per member, Livongo’s figure rose from $573 in 2017 to $764 in 2019, and had already reached $392 in the first half of 2020, with the full-year total potentially exceeding $800. The increase in average annual revenue per member was driven by higher service fees. Prior to 2017, Livongo offered individual plans at $49.99 per month; however, by 2019, employers were paying $68 per month per employee. The rise in average revenue per user indicates that Livongo was able to raise prices without a significant increase in the number of members acquired from each company, which also demonstrates the growing effectiveness of its overall services and employers’ recognition of their value.

Whether it is Livongo, which took an early lead, or Zhiyun Health, which caught up from behind, both can be regarded as leaders within their respective market contexts. However, there is actually no competitive relationship between these two “strong players,” because at the current stage, the Livongo model is not applicable to the Chinese domestic market, while Zhiyun Health has no plans to expand into overseas markets and remains highly focused on China.

Perhaps as China’s commercial insurance system becomes increasingly mature, Zhiyun Health and Livongo will generate some synergy in overseas markets.