Can Cash-Burning Healthcare Providers Escape the Customer Acquisition Trap as Costs Surpass $1,500 Per Lead?

Over the past year or two, healthcare service providers have truly been facing difficult times.

Data Source: Qichacha

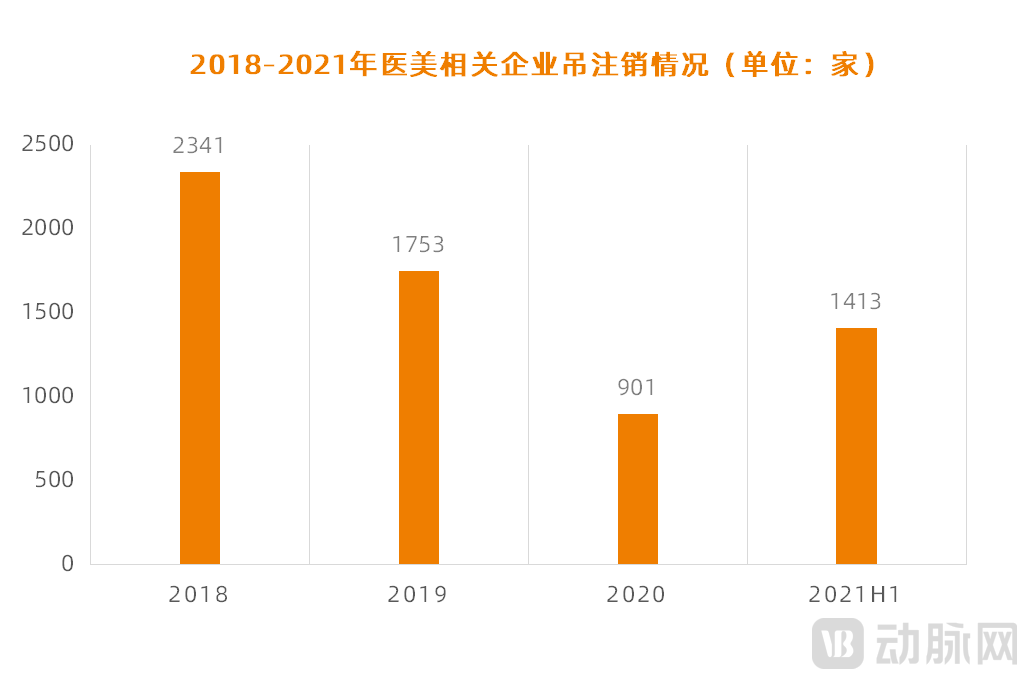

Take the typical medical aesthetics industry as an example.According to statistics from Qichacha, 1,413 medical aesthetics-related enterprises had their business licenses revoked or were deregistered in the first half of 2021, nearly 500 more than the same period last year. Amid the shadow of the pandemic, the wave of closures among medical aesthetics institutions is intensifying.

Amidst this surging tide, one cannot help but ask: Why has a widely recognized high-margin industry been driven to such a plight?

This is mainly “thanks to” the sky-high customer acquisition costs borne by medical aesthetic institutions.CSC Financial has found that in the total costs of medical aesthetic institutions, marketing channels and sales expenses account for 50% and 20%, respectively. After deducting all expenditures, including consumables, operations, and labor, the net profit margin of medical aesthetic institutions is generally only 1% to 10%.

Take Rayli Medical Aesthetics, which listed in Hong Kong at the end of last year, as an example.According to financial disclosures, Ruili Medical Aesthetics reported annual revenues exceeding RMB 100 million from 2017 to 2020, with gross profit margins remaining stable at approximately 50%. However, its net profit margin declined year over year, dropping from 15.4% in 2017 to 2.98% in 2020, indicating a further narrowing of profit margins.

The “chief culprit” behind this disparity is the high customer acquisition cost.According to the prospectus, Ruili Medical Aesthetics’ promotion and marketing expenses (online advertising and outdoor advertising) from 2017 to 2020 were RMB 15 million, RMB 23 million, RMB 23 million, and RMB 7 million, accounting for 40.8%, 50.8%, 46.4%, and 45.7% of the selling and distribution expenses for the respective periods; during the same period, staff costs (salaries and bonuses paid to sales and marketing personnel) accounted for 45.6%, 34.3%, 40.2%, and 40.5% of the selling and distribution expenses for the respective periods. In its prospectus, Ruili Medical Aesthetics acknowledged that it relies heavily on promotions, advertising, and online marketing activities to promote its brand and services.

If publicly listed companies are facing such challenges, small and medium-sized medical aesthetic institutions will find their situation even more difficult. However, these institutions are not isolated cases.Stomatology, Ophthalmology, Rehabilitation, Traditional Chinese Medicine, Reproductive HealthHealthcare service providers in other sectors are also being drawn into the “patient acquisition” vortex, with their room for survival growing increasingly narrow.

From Hundreds to Tens of Thousands: Why Is the “Price” of Customer Acquisition Soaring?

Customer Acquisition Is Becoming a Luxury Business.

Take Yonghe Medical, which is striving to become the first listed company in the hair transplant sector, as an example.As China's largest provider of hair transplant medical services, Yonghe Medical’s total revenue from hair transplants grew by 31.1% year-on-year from RMB 930 million in 2018 to RMB 1.22 billion in 2019, and further increased by 33.8% to RMB 1.64 billion in 2020, ranking first in the industry.

However, its net profit margin figures are “far from encouraging.” According to the prospectus, Yonghe Medical’s net profit margins for 2018 to 2020 were 5.7%, 2.9%, and 9.8%, respectively. Although there was an upward trend, all remained below 10%.

This is primarily due to Yonghe Medical’s substantial investments in advertising and marketing. It is reported that from 2018 to 2020, sales and marketing expenses accounted for 49.6%, 53.1%, and 47.6% of Yonghe Medical’s revenue, respectively, amounting to RMB 460 million, RMB 650 million, and RMB 780 million.A total of approximately RMB 1.9 billion was invested over the three-year period. Based on a total of 176,000 patients treated during these three years, Yonghe Medical’s average customer acquisition cost per patient amounted to RMB 10,795.

Such “astronomical prices” are not isolated cases; under current market trends, this is the norm across the entire healthcare service sector. This, however, has piqued our curiosity:"In today’s era of increasingly advanced internet technology, why is the cost of acquiring customers for healthcare service providers rising, despite their greater potential to reach users?"

This is, in fact, a continuous process of “getting hooked.”Xiao Zhenggang, Chairman of Yamei Group, a long-established aesthetic medicine institution, once broke down the numbers: “Before internet-based healthcare became dominant, medical aesthetic clinics primarily advertised through traditional media, with customer acquisition costs exceeding RMB 2,000. Later, due to Baidu’s paid ranking system, these costs rose to over RMB 3,000. As multi-dimensional marketing models emerged, costs climbed further. Currently, the industry has shifted toward a channel-based model, but market rebates have reached as high as 70%.”

In the past year or two, it has been the newly emerged customer acquisition platforms and apps that have been “singing a high tune” in the customer acquisition market.Most of them aim to reduce customer acquisition costs for healthcare service providers, gradually replacing intermediaries and channel brokers that charge exorbitant commissions.

However, this “original intention” did not last. A head of a large medical aesthetics institution told VCBeat, “After the emergence of medical aesthetics apps, medical aesthetics institutions abandoned channels and brokers, and directly placed advertisements on platforms to acquire customers. Taking into account advertising costs and transaction commissions, the customer acquisition cost for institutions has significantly decreased, often requiring only 200 to 300 yuan per customer.”

However, as medical aesthetics platforms and apps have driven out a large number of intermediary and broker-style beauty institutions, the customer acquisition costs for medical aesthetics institutions on these platforms have begun to rebound significantly. The most notable turning point occurred in 2019, when some medical aesthetics platforms simultaneously raised their advertising fees and commissions, with increases reaching as high as 120%. Taking the medical aesthetics institutions under its management as an example, the monthly advertising expenditure on several mainstream medical aesthetics apps amounts to approximately RMB 1.2 million to RMB 1.5 million.

In the first half of this year, his institution generated a monthly gross merchandise value (GMV) of nearly RMB 3 million through the platform. A 10% commission, referred to as the platform consultation fee, was charged on each completed transaction. Consequently, the total monthly payment to the medical aesthetics app amounted to approximately RMB 1.5 to 1.8 million. The return on investment (ROI) stood at around 1:2, significantly lower than the 1:8 ratio observed in 2018.

Knowing There Are Tigers in the Mountains, Why Do Healthcare Institutions Insist on Venturing Into Tiger Territory?

Given the high cost of customer acquisition, why are healthcare service providers still so “fond” of it?

This is, in fact, a matter of last resort.Unlike public hospitals, which enjoy inherent patient traffic from the outset, private medical service institutions operate as service-oriented healthcare providers. Since their services are not perceived as essential by individuals, these institutions cannot afford to remain passive; instead, they must proactively seek out clients in the market, ensuring that customers truly understand the value offered and are willing to pay for it.

On the other hand, unlike public hospitals that often see “one-off” patient visits, private medical service institutions require a more stable and predictable patient flow. This stability is built upon a loyal patient base, where positive word-of-mouth driven by treatment efficacy creates an aggregation effect, ultimately forming the core competitive advantage of these healthcare providers.

Although the quality of medical care should be prioritized, the adage “good wine needs no bush” clearly does not apply to healthcare institutions,Traffic must come first, followed by high-quality medical services.This unique industry characteristic dictates that “traffic” is their lifeline; whoever possesses a stable traffic base can gain a competitive edge in the industry.

However, accumulating traffic is no easy feat; in addition to one’s own efforts, it also requires leveraging certain “external forces.”First, the company itself primarily relies on its in-house marketing team or independently operates online channels such as WeChat Official Accounts, Xiaohongshu (Little Red Book), WeChat personal accounts, WeChat groups, and short-video platforms.

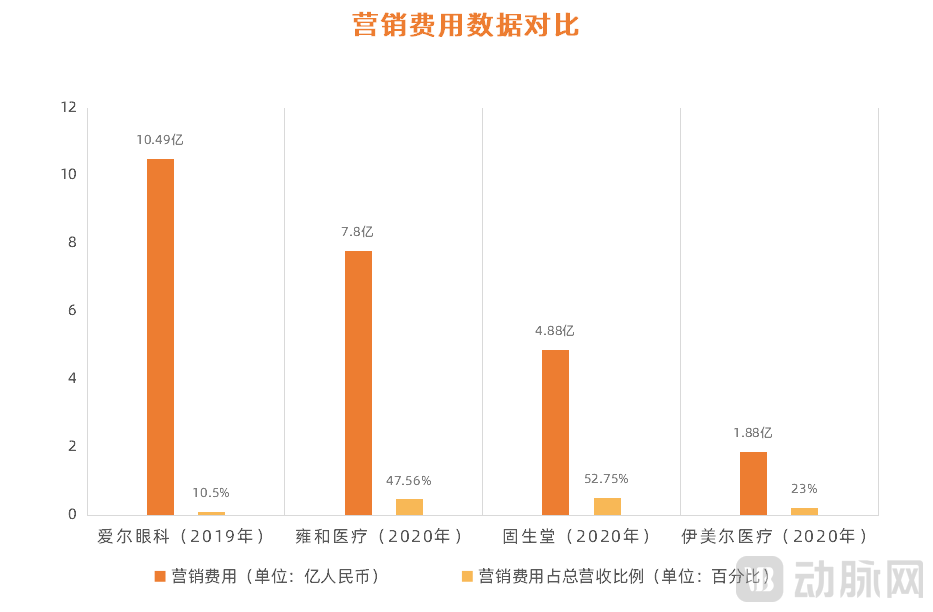

“External forces” refer to media platforms dominated by advertising and customer acquisition apps that have emerged in recent years. As the world’s largest chain of ophthalmic medical institutionsAier Eye HospitalFor example, under pressure to acquire customers and compete, Aier Eye Hospital has invested heavily in sales expenses, which amounted to RMB 405 million in 2015 and climbed to RMB 1.049 billion by 2019. Among these expenses, advertising and promotional costs accounted for the largest share, representing nearly half of total sales expenses.

Medical aesthetic institutions are more inclined to use medical aesthetic apps. A representative from a nationwide chain of medical aesthetic clinics stated, “We are fully aware that we have spent heavily on marketing over the years, which is clearly reflected in our financial statements. However, this is an unavoidable reality; since everyone else is doing it, failing to follow suit would cause us to lose competitiveness in the market. This situation is not entirely within our control. We have attempted to operate on our own proprietary platforms, but in practice, it proved extremely challenging. Despite considerable effort, the results were unsatisfactory. Over time, we have become dependent on customer acquisition platforms.”

This “dependence” is well corroborated by data from customer acquisition platforms. As a professional medical aesthetics service platform, So-Young Technology (NASDAQ: SY) derives its revenue primarily from information service fees—namely, merchant onboarding and advertising placement fees—and booking service fees, which refer to commissions earned from referral-driven service reservations.

According to its latest Q2 2021 financial report, the number of paying medical institutions reached 4,899, a year-on-year increase of 31.2%. In terms of specific revenue, SoYoung’s information service revenue amounted to RMB 360 million, up 53.8% from RMB 235 million in the same period last year; booking service revenue was RMB 91.1 million, down 2.8% from RMB 93.7 million in the same period last year; and the total transaction value of facilitated medical aesthetic services reached RMB 1.04 billion.

As can be seen, healthcare service providers’ investments in patient acquisition have indeed yielded results, but this has also placed a substantial financial burden on them.

Listed Companies That Emerged from the Cracks: What Did They Get Right in Customer Acquisition?

The healthcare services industry is not as “glamorous” as commonly perceived, with its most significant pain point being the difficulty of overcoming the “customer acquisition” hurdle. Only by adopting the right strategies for customer acquisition can companies emerge as industry leaders, achieve sustainable long-term revenue, and position themselves for an initial public offering (IPO), thereby becoming benchmarks within the sector.

Currently, healthcare service providers are experiencing a wave of initial public offerings (IPOs). Yonghe Medical, China’s largest hair transplant provider; Gushengtang, the country’s largest chain of traditional Chinese medicine clinics; and Yimeier Medical, the fourth-largest private medical aesthetics institution in China, have all filed their prospectuses this year. So, what have these healthcare service providers—either already listed or having filed their prospectuses—done right in terms of customer acquisition?

Aier Eye Hospital was established in 2003 and successfully went public in 2010. As the most representative “successful model” among medical service providers, Aier Eye Hospital has demonstrated remarkable performance in both influence and revenue figures. According to its 2020 financial data, the company achieved an annual operating revenue of RMB 11.912 billion, representing a year-on-year increase of 19.24%.

The reason it has managed to stand out and achieve profitability at scale can be traced back to Aier Eye Hospital’s innovative three-tier chain model. The so-called three-tier chain model refers to"Central City Hospitals -- Provincial Capital City Hospitals -- Prefecture-Level City Hospitals -- County-Level Hospitals"This tiered chain model assigns distinct functional roles to hospitals at different levels, thereby achieving a hierarchical diagnosis and treatment system.

In simple terms, the first-tier facilities are located in Shanghai and positioned as technical centers and referral hubs for complex cases; the second-tier facilities, established in provincial capitals, serve as profit centers; and the third-tier hospitals, set up in prefecture-level cities, function as “customer centers,” providing optometry and eyewear dispensing services along with diagnosis and treatment of common eye diseases to the broadest patient base, while referring complex cases to higher-tier institutions.

Generally, the smaller the city, the smaller the corresponding hospital scale. Aier’s tiered model can enhance both the breadth and depth of its brand while improving the efficiency of resource sharing. It is not merely a hierarchical operational structure; eye conditions that cannot be diagnosed locally can be addressed through remote consultations or directly referred to hospitals in provincial capitals or major central cities, thereby achieving seamless integration throughout the treatment process and enhancing therapeutic efficiency.

When you type “hair transplant” into a certain search engine, Yonghe always appears near the top of the results—all because it paid for that placement.

According to the prospectus, from 2018 to 2020, Yonghe Medical purchased search engine-related advertising services from Supplier A, its primary provider in this category, for RMB 119 million, RMB 169 million, and RMB 81 million, respectively, accounting for 15%, 15%, and 6% of its total annual procurement expenditures.

In addition, since 2019, the company has begun to increase its investment inOnline community promotion, promotion via social networking platforms, in that year, the Company purchased online community promotion services from Supplier G for RMB 25 million and social networking platform promotion services from Supplier F for RMB 32 million; in 2020, the Company procured online community promotion services from Supplier I for RMB 115 million and purchased services from Supplier F for RMB 29 million.

The Company’s top five suppliers are predominantly advertising and promotion service providers. Over the aforementioned three-year period, the Company’s procurement amounts from these five suppliers were RMB 186 million, RMB 280 million, and RMB 278 million, respectively, accounting for approximately 23%, 25%, and 20% of the total procurement amount in each respective period.

To acquire customers, in addition to spending hundreds of millions of yuan on marketing, Yonghe Medical also recommends to consumersFinancial Lending Platform. It is reported that, upon learning of the patient’s insufficient funds, staff at Yonghe Medical proactively recommended “medical aesthetic loans” and “medical aesthetic installment plans.” The loan platforms recommended by Yonghe Medical mainly include third-party financial platforms such as Yimeijian, Du Xiaoman, Alipay’s Huabei and Jiebei, and Meituan Borrowing.

On June 10, 2021, Gushengtang, a chain of traditional Chinese medicine (TCM) outpatient clinics, formally filed its listing application with the Main Board of the Hong Kong Stock Exchange, becoming the first medical service provider in the TCM sector to pursue an initial public offering (IPO).

According to the prospectus, Gushengtang has achieved substantial revenue growth over the past three years, with revenues in 2018, 2019, and 2020 amounting to RMB 726 million, RMB 896 million, and RMB 925 million, respectively, representing a compound annual growth rate (CAGR) of nearly 13%.

In terms of customer acquisition, Gushengtang has launched a WeChat Official Account and Mini Program to provide online appointment booking, consultation, diagnosis, and prescription services.Leveraging its extensive network of physicians, rich operational experience, and proprietary information technology infrastructure, Gushengtang serves a larger, cross-regional customer base through its own and third-party online platforms. Furthermore, by virtue of its proprietary platform, Gushengtang stores customers’ electronic medical records in a cloud-based Hospital Information System (HIS) to create comprehensive customer profiles, thereby facilitating follow-up services and long-term healthcare management.

However, the most significant highlight of Gushengtang lies in its pioneering adoption of the “OMO” business model.On one hand, the development of the company’s online healthcare services has enabled more efficient utilization of medical resources and expanded customer reach; on the other hand, it has allowed the company to strategically select cities for expanding its offline coverage based on metrics of online physician and customer engagement.

Benefiting from the deepening integration of the “OMO” (Online-Merge-Offline) model, Gushengtang has amassed a large customer base with strong stickiness and high loyalty. According to Frost & Sullivan, Gushengtang ranked first among all private TCM healthcare providers in China in terms of cumulative patient visits, which exceeded 7 million as of December 31, 2020. Customer loyalty and retention rates have continued to improve, with the customer return rate reaching 62% in 2020.

On August 3, 2021, Beijing Yimei'er Medical Group Co., Ltd., which claims to be the fourth-largest private medical aesthetics institution in China, submitted its prospectus in Hong Kong for a proposed listing on the Main Board of the Hong Kong Stock Exchange, with Haitong International serving as its sole sponsor.

In the early days of its establishment, to attract customers, the two founders, Wang Yong’an and Li Bin, carefully planned"The Hao Lulu Incident: China's First Artificial Beauty"Specifically, in that year, Yimei'er Medical partnered with CNN to launch the "Beauty Creation" project. By providing full coverage of Hao Lulu's cosmetic surgery procedures as a manufactured beauty icon, the initiative garnered widespread social attention and generated viral discourse, thereby enhancing public understanding of the plastic surgery industry.

According to reports at the time, Hao Lulu underwent cosmetic procedures on more than ten areas of her body in 2003 alone, including double eyelid surgery, eyelash extensions, rhinoplasty, mandibular angle contouring, breast augmentation, breast lift, buttock augmentation, skin rejuvenation, hair removal, and liposuction. The series of procedures lasted nearly 200 days and cost over RMB 300,000.

This was China’s first large-scale promotional campaign for medical aesthetics, with the concept of “artificial beauties” gaining nationwide popularity, which significantly boosted the promotion of Yimeier Medical.

Following the high-profile event, Yimei Medical established a team of sales consultants to further consolidate patient traffic.Launched the “Referral Program” mini-program, intensified O2O and video media advertising, while reducing spending on traditional ads to lower customer acquisition costs.

According to the prospectus, in 2018, Yimeier acquired 38,928 new customers with marketing expenses of nearly RMB 199 million, resulting in a customer acquisition cost (CAC) of RMB 5,111 per person. In the first quarter of 2021, Yimeier gained 14,050 new customers with marketing expenses of RMB 64.2 million, reducing the CAC to RMB 4,571 per person. Compared with previous channels such as newspapers, television, outdoor advertising, and referrals from beauty salons, targeted online promotions have helped Yimeier lower its customer acquisition costs to some extent, thereby securing a competitive advantage in the medical aesthetics market.

As can be seen, every healthcare service provider heading towards an IPO has invested considerable effort in customer acquisition and innovatively proposed various types of customer acquisition methods based on their business models. However, this does not mean that these "successful models" can be replicated as-is, because customer acquisition needs to be customized specifically according to the particular market environment.Precisely define your target customer base and employ the most efficient methods to identify high-potential paying users.

“AI” Will It Chart a Clear Path for Healthcare Providers in Patient Acquisition?

Looking back more than a decade ago, healthcare service providers were very conservative in their marketing efforts. Those with some financial resources would engage in broad-based advertising across various media platforms, while those just starting out relied mainly on offline promotion by sales teams. Even today, many healthcare institutions continue to use these traditional methods, which attests to their practicality.

However, times are changing, and so are customer acquisition strategies. In particular, the rise of “live-streaming e-commerce” over the past one to two years has injected new vitality into many healthcare service providers, allowing them to reap tangible benefits in patient acquisition.

Especially in the medical aesthetics sector, live-streaming sessions generating over RMB 100 million in revenue are becoming increasingly frequent.In September 2020, Alibaba’s Local Services Medical Aesthetics Live Streaming Festival announced that within just over a month, the platform had hosted more than 6,000 live streams. Over 50 million users tuned in to watch these medical aesthetics live broadcasts, resulting in more than 60,000 completed transactions and a gross merchandise value exceeding RMB 100 million.

In 2021, at the “Medical Aesthetics & Healthcare Industry Summit,” Wang Yajun, General Manager of Consumer Healthcare at Ele.me, also revealed that over the past year, Ele.me had achieved single-session medical aesthetics live-streaming sales exceeding RMB 100 million. Notably, during last year’s Double 11 shopping festival, 30% of medical aesthetics orders originated from late-night live streams.

However, the dividends from live streaming will not last long, primarily because the entire live-streaming sector is facing stringent regulatory oversight.On November 6, 2020, the official website of the State Administration for Market Regulation (SAMR) released the “Guiding Opinions of the State Administration for Market Regulation on Strengthening Supervision over Online Live-Streaming Marketing Activities,” marking the first official document specifically dedicated to regulating live-streaming marketing. The live-streaming sector of healthcare service institutions is poised to undergo an imminent transformative overhaul.

Following the live broadcast, “AI” may emerge as a new focal point for healthcare service providers in customer acquisition.

In recent years, artificial intelligence technology has advanced rapidly, largely due to breakthroughs in neural network algorithms. At the core of these algorithms is probabilistic inference, which leverages the nesting of countless functions, resulting in a “black box” computational process. With mainstream algorithms and frameworks being open-source, the greater the availability of high-quality data, the more efficient neural networks become.

While artificial intelligence has numerous application scenarios, healthcare stands out as the most significant in terms of funding volume.It is reported that in 2019, global funding for “Healthcare + AI” reached $4 billion, twice the amount of “Finance + AI,” which ranked second.

Regarding specific sub-sectors, AI technology is currently primarily applied in key areas such as pharmaceutical R&D and cancer screening. In terms of customer acquisition, the integration of these two domains remains in its early “development stage,” yet its potential and application value are promising.

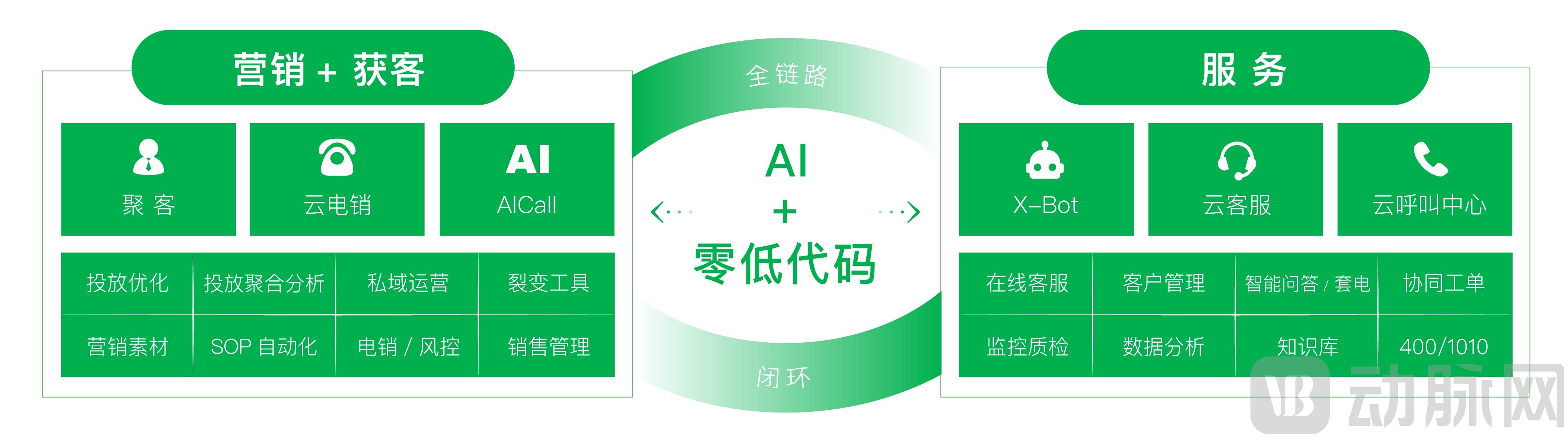

First, in terms of outreach, precision targeting is achieved through marketing tools and private-domain traffic pools.withNo. 1 Internetas an example. As a company dedicated to the research, development, and application of enterprise-level AI-powered sales and customer service platforms, Yihao Hulian has built an omnichannel, all-scenario integrated intelligent customer service platform. By optimizing the entire workflow—from marketing and customer acquisition to customer service and customer relationship management—it helps medical aesthetic institutions streamline their operations, reduce customer acquisition costs, and increase repeat purchase rates. This enables these institutions to efficiently address customer acquisition challenges and achieve digital and intelligent transformation.

Secondly, in terms of conversion, we establish a comprehensive service system to provide intelligent customer reception.One of the key drivers of conversion improvement lies in customer satisfaction with products and services, and one of the primary ways to enhance customer satisfaction is through customer service. As a vital link connecting enterprises and customers, customer service directly impacts brand image building and revenue growth.

As a leader in China's SaaS intelligent customer service sector,7moorBy leveraging intelligent systems and innovative solutions, we establish a comprehensive service framework for users that covers pre-sales consultation, in-sales follow-up, and after-sales support. This approach enhances the efficiency of manual service operations and improves service quality, thereby elevating the user experience and driving paid conversion rates.

Also standing at the forefront of this trend areShuming TechnologyLeveraging its extensive data foundation, artificial intelligence algorithms, and the terminal coverage of partner internet platforms, Shuming Technology can identify populations with strong demand for specific products. It then executes precision targeting through information terminals, private domain traffic platforms, and the channels of the three major telecom operators, achieving broad coverage, high reach, and high conversion rates.

Finally, in terms of growth and viral expansion, scientific management was employed to reduce costs and improve efficiency, thereby stimulating sustained user consumption.Taking “Ronglian Qimo Juke” as an example, it is a viral marketing tool based on the WeChat ecosystem, designed to achieve video-based viral dissemination through promotional campaigns, posters, and coupons. This approach rapidly reactivates existing customers and high-potential prospects, driving user acquisition and exponential growth, thereby continuously strengthening the self-sustaining capabilities of healthcare service providers.

It is worth noting that, at this stage, the vast majority of AI-driven customer acquisition platforms adopt“Pay-for-Performance”, which differs from the traditional “one-time payment” model, can significantly alleviate the financial pressure on healthcare service providers and offer them manageable room for growth.

Overall, “AI” technology primarily addresses precision in patient acquisition for healthcare service providers. This aligns closely with the three key elements of marketing—price, conversion rate, and promotion—and may offer a way out for healthcare institutions trapped in a vicious cycle of customer acquisition.