2021 Medical AI Report: Commercialization Progress and IPO Readiness of Medical AI Companies

Deep learning is a more complex form of neural network, featuring multiple layers of computational nodes or neural networks that collectively process data to produce final results. It offers scalability (the ability to handle large datasets using scalable large models) and hierarchy (performing automatic feature extraction from raw data through a process known as feature learning), enabling the construction of more complex concepts from simpler ones.

AI applications in the healthcare sector are extensive, yet they are predominantly concentrated on the provider side (H-end) to enhance service efficiency and reduce costs. A smaller portion focuses on the business side (B-end), delivering tailored solutions for pharmaceutical companies, insurance institutions, and other entities. Very few AI offerings are directed straight to consumers (To C), as individual users rarely demonstrate an intent to directly purchase AI-driven medical services.

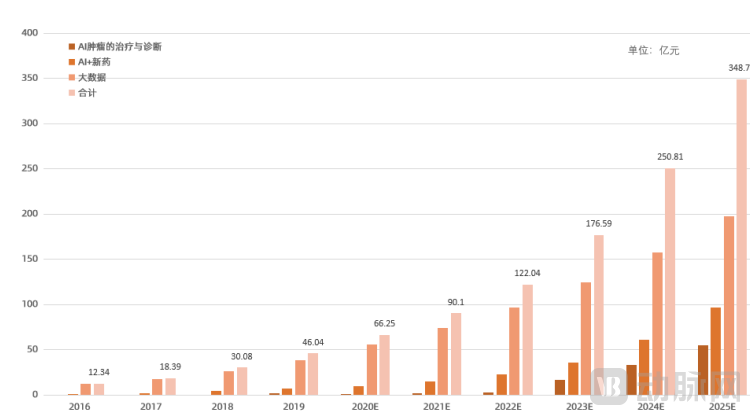

The total AI market size at the current stage can be roughly estimated by calculating the market sizes of three major sectors: Big Data + AI, New Drug Development + AI, and Oncology Diagnosis and Treatment + AI. Data shows that the combined market size of these three sectors totaled RMB 6.32 billion in 2020. With the expansion of product application scenarios and rising market penetration rates, the market size is projected to reach approximately RMB 22.56 billion by 2024.

At its core, AI is a data processing tool. Consequently, medical big data, which aligns perfectly with AI’s functionality, had already taken shape by 2016, reaching a market size of nearly RMB 1.2 billion, and maintaining a penetration rate of over 15% after 2018 (Source: Yidu Tech Prospectus). In contrast, AI-driven oncology diagnosis and treatment, as well as new drug development, began to mature in 2018 and have since experienced rapid growth at rates exceeding 30%. These sectors are projected to surpass the medical big data market size before 2030.

Market Size of Major Application Areas in Medical AI (Data Sources: Yidu Tech Prospectus, Frost & Sullivan, VCBeat)

The accelerated regulatory approval of AI-based medical device series has expanded the variety and penetration rate of medical AI products, attracting more capital investment; meanwhile, the maturation of AI-enabled genetic testing technology is driving rapid growth in the AI-driven new drug market, leading to a swift expansion of its market size.

The vast potential market size has attracted numerous emerging enterprises, while established players deeply rooted in the healthcare sector are also ramping up their investments in AI. According to the VCBeat database, there are currently over 500 companies developing proprietary medical AI solutions, with intelligent disruption permeating nearly every healthcare segment.

As the artificial intelligence industry continues to deepen its development, differentiation within the same sector is increasing. Using commercialization as the criterion, VCBeat Research Institute categorizes existing AI sectors into two groups: mature sectors and high-potential sectors. It analyzes the developmental maturity of all AI sectors and explores implementation strategies for future medical AI enterprises.

Mature sectors have achieved parallel commercialization both within and outside hospitals. In-hospital imaging applications are utilized by departments such as Radiology, Thoracic Surgery, Cardiology, Endocrinology, and Information Technology; in-hospital process solutions include Electronic Medical Records (EMR), Clinical Decision Support Systems (CDSS), and Quality Control. Out-of-hospital services, including patient guidance, consultation, health services, and customized knowledge graphs, have also achieved large-scale commercialization. In contrast, sectors such as laboratory testing, insurance, Traditional Chinese Medicine (TCM), medical aesthetics, and new drug R&D are considered high-potential areas; while they exhibit a certain degree of commercialization, they have not yet reached scale.

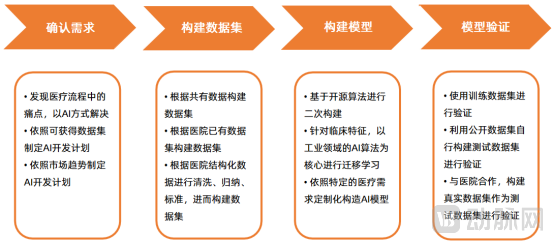

In the early stages of development in the medical AI sector, the selection of research targets generally follows two pathways. The first involves areas with high-volume demands but no existing solutions, such as imaging detection for pulmonary nodules and fundus examination. The second involves replacing traditional solutions with AI-based approaches, such as surgical planning for thoracic surgery and AI-driven electronic medical record (EMR) entry and quality control. As penetration rates gradually increase and development difficulties decrease, medical artificial intelligence will follow the former pathway to develop more products tailored to specific scenario needs.

Initial AI Product R&D Roadmap

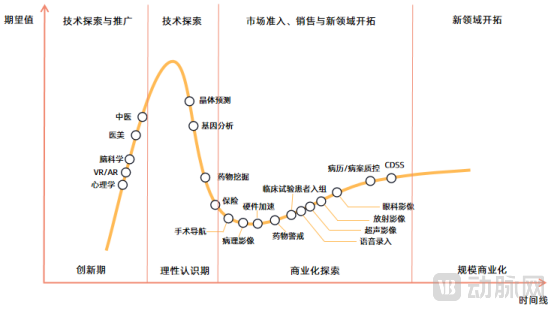

By analyzing factors such as technical capabilities, product performance, sales scale, and profitability across various sectors, VCBeat presents the current development status of each sub-sector in medical artificial intelligence in the form of a Gartner Hype Cycle, as shown below.

Healthcare AI Maturity Curve

After nearly a decade of development, the majority of sectors based on computer vision and natural language processing have matured and entered the phase of commercial exploration. However, no company has yet achieved profitability through the sale of medical artificial intelligence (AI) products; consequently, no enterprise has entered the stage of large-scale commercialization. During this period, medical AI companies that have not yet received review and approval certification from the Center for Medical Device Evaluation are occupied with clinical trials. Those that have obtained certification are focusing on including their products in regional medical pricing catalogs and accelerating market share expansion. Meanwhile, medical IT companies, which are exempt from such review and approval processes, are concentrating on product sales and promotion.

Given that the application of artificial intelligence in healthcare is deeply dependent on the medical field itself, and scenarios with widespread demand have been largely exhausted over several years of development, there are few tracks currently in the innovation phase. Sectors such as VR/AR and brain science are constrained by the pace of medical advancements and have remained in the innovation stage for many years; without breakthroughs in academic research, they will likely remain stagnant. In contrast, sectors like Traditional Chinese Medicine (TCM) and medical aesthetics are being driven toward digital transformation by supportive policies and rising consumer demand. Propelled by this demand, these sectors may rapidly advance into the commercial exploration phase within the next two years.

It is worth noting that since its emergence, medical artificial intelligence has faced the issue of "hype far exceeding reality." For instance, industry expectations for AI-driven new drug development have significantly outpaced its actual performance. In fact, the maturity level of artificial intelligence varies considerably across different stages of the new drug development process. Areas such as clinical trial patient management, involving companies like Yidu Cloud and LinkDoc Technology, and pharmacovigilance, involving Deepwise, are relatively mature. In contrast, domestic technologies in protein folding and crystal prediction remain far from practical application.

However, Insilico Medicine’s screening platform has already been commercialized through a subscription model priced at $100,000 per month, and Bristol Myers Squibb (BMS) acquired the development license for an immunomodulatory candidate drug discovered by Exscientia for $20 million (with the total deal value exceeding $1.2 billion), indicating a positive overall development trend for AI-driven new drug discovery.

Insilico Medicine’s relocation of its headquarters to China underscores the value of the domestic market. Given the substantial need for cost control in new drug development and the limited competitive landscape in China, the AI-driven drug discovery sector will continue to attract capital support over the long term and can still be regarded as a blue ocean market.

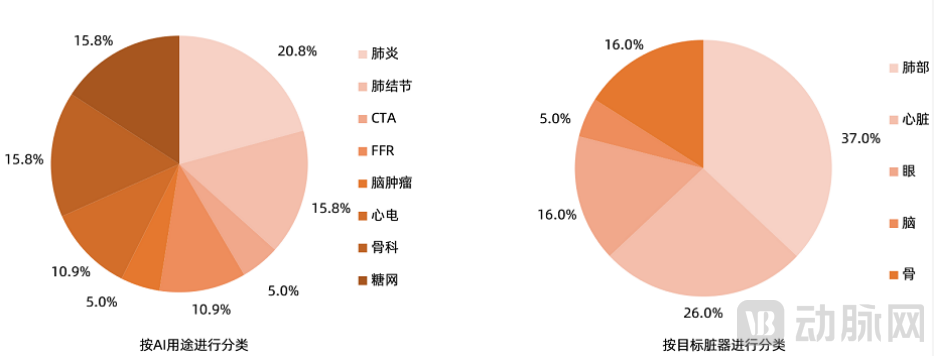

As of August 16, 2021, a total of 19 medical artificial intelligence devices had obtained Class III medical device certificates approved by the Center for Medical Device Evaluation of the National Medical Products Administration. Although obtaining certification does not guarantee commercial success, the medical AI CRO (Contract Research Organization) sector has gradually emerged as companies navigate the regulatory landscape through iterative exploration. Consequently, the costs and timelines associated with regulatory review and approval have become increasingly manageable, enabling enterprises to formulate more precise plans for their R&D pipelines and commercial promotion strategies.

By categorizing approved products based on their applications and target organs, we observed a certain degree of clustering among AI-based products. The drivers behind this distribution can be summarized into three factors: data, policy, and demand.

Classification of Mature Medical Artificial Intelligence Devices

(1) Data:

Data is the core factor determining the real-world performance of artificial intelligence (AI) products in medical imaging. Among approved products, diabetic retinopathy and pulmonary nodule detection represent the two AI product categories with the most abundant publicly available data. As early as 2018, the National Institutes for Food and Drug Control (NIFDC), in collaboration with partner hospitals, pioneered the establishment of standard databases comprising 623 cases of thoracic imaging and fundus imaging. Consequently, these two sectors attracted a massive influx of enterprises during the early stages of medical AI development.

Following the establishment of the AI Medical Device Innovation Cooperation Platform, the lead organization, Shanghai Shenkang Hospital Development Center, plans to establish eight major test sample databases for CT lung, CT liver, CT fracture, brain MRI, cardiac MRI, coronary CTA, ECG, and ophthalmology. Currently, six categories of AI have received regulatory review and approval, with CT liver and cardiac MRI likely being the next therapeutic areas to gain approval.

(2) Policy:

The scale of AI-based pneumonia products is closely linked to the COVID-19 pandemic. On March 5, 2020, the National Medical Products Administration and the Center for Medical Device Evaluation issued the “Key Points for the Review of Auxiliary Triage and Assessment Software for Pneumonia CT Imaging (Trial)”. The document specifies that software functions must include at least abnormality detection, quantitative analysis (e.g., lesion volume proportion, CT value distribution), data comparison (both manual and automated), and report generation. Among these, abnormality detection serves as a triage alert for suspected cases, while quantitative analysis and data comparison are used for disease assessment in confirmed patients. Furthermore, three requirements were proposed for training data:

i. In principle, the training dataset shall comprise no fewer than 2,000 CT images of COVID-19 cases; these images must be sourced from at least three medical institutions, including at least one institution located in an area severely affected by the epidemic; and the dataset must include CT images representing both the early and progressive stages of novel coronavirus pneumonia.

ii. Provide the data distribution of CT images for novel coronavirus pneumonia, taking into account population characteristics (e.g., sex, age), imaging stages (early, progressive, severe), data source institutions, and CT equipment specifications (e.g., manufacturer, slice thickness).

iii. Provide an analysis report on factors affecting algorithm performance, taking into account CT equipment, imaging-based staging, and similar clinical presentations.

(3) Requirements:

The research and development of artificial intelligence in the fields of cardiology, orthopedics, and diabetic retinopathy stems from China’s substantial demand for early disease screening and assisted diagnosis. According to data from Keya Medical’s prospectus, the number of coronary computed tomography angiography (CTA) procedures performed in China increased from 3.6 million in 2015 to 6.2 million in 2020, representing a compound annual growth rate (CAGR) of 11.7%. This figure is projected to further rise to 22.2 million by 2030, with a CAGR of 13.6% from 2020 to 2030. The penetration rate of CT-derived fractional flow reserve (CT-FFR) is estimated to reach 0.4% in 2021 (calculated as the proportion of estimated CT-FFR procedures relative to the total number of CTA procedures in China). By 2030, the total addressable market size for deep learning-based CT-FFR products in China is expected to reach 66.7 million procedures.

Demand-driven product development is a process of going from “0” to “1.” During the R&D phase, companies lack public datasets for reference and must collaborate with hospitals to acquire, clean, and annotate data, as well as build models (with some algorithms transferable from industrial applications). Although this type of artificial intelligence development poses significant challenges, obtaining regulatory approval can establish a robust competitive barrier.

Procurement has also advanced rapidly. VCBeat Institute compiled statistics on publicly tendered medical artificial intelligence products from August 26, 2020, to August 25, 2021, identifying a total of 132 relevant procurement records. Based on this data, we present the following analysis.

(1) AI procurement is primarily focused on medical IT, with imaging as a secondary focus

According to statistics from VCBeat, only 29 out of 132 procurement records were for AI-based medical imaging products, with the remainder being AI-driven healthcare IT solutions. This disparity is primarily attributable to the lower entry barriers for healthcare IT AI products, whereas AI imaging products, classified as medical devices, must obtain regulatory approval—including completion of clinical trials—before they can be adopted by hospitals.

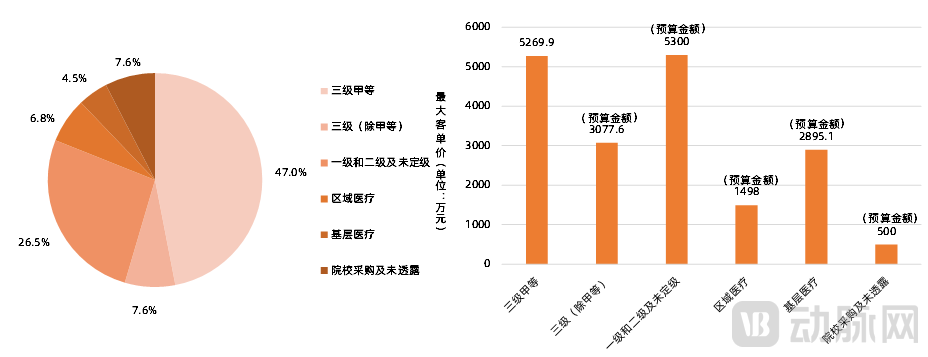

(2) Tertiary Grade A hospitals account for the highest procurement volume and the highest average transaction value.

According to statistics from VCBeat Research Institute, purchasing institutions include tertiary Grade A hospitals, tertiary and lower-tier hospitals, as well as regional medical centers, primary healthcare facilities, and professional academic institutions. Among these, tertiary Grade A hospitals account for the largest proportion, nearing 50%, followed by secondary and lower-tier hospitals. The unit price of all procurement projects ranges from RMB 100,000 to RMB 10 million. Notably, the "Smart Hospital" projects in tertiary Grade A hospitals have the highest unit price, reaching RMB 52.699 million. Similarly, the RMB 53 million budget allocated by secondary hospitals is also designated for "Smart Hospital" projects. This high total cost is attributed to the large quantity of artificial intelligence (AI) products and other items included in "Smart Hospital" projects, with AI products typically priced between several hundred thousand and several million RMB.

Statistics on Purchasers and Procurement Amounts of Hospital-Side Medical AI Products

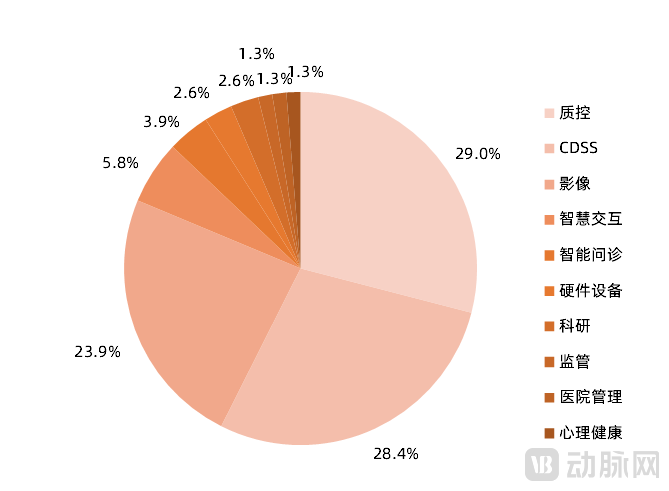

(3) AI-based quality control and CDSS are predominant, with auxiliary diagnosis of lung and chest imaging being the mainstream

According to statistics from VCBeat, among the publicly tendered medical artificial intelligence products over the past year, quality control and CDSS-based AI products predominated, accounting for 29% and 28%, respectively. AI-assisted imaging diagnostic products followed, representing 22.6%, with AI-assisted diagnostic products for lung and chest conditions experiencing the highest demand during this period.

Statistics on the Types of Medical AI Products Procured by Hospitals

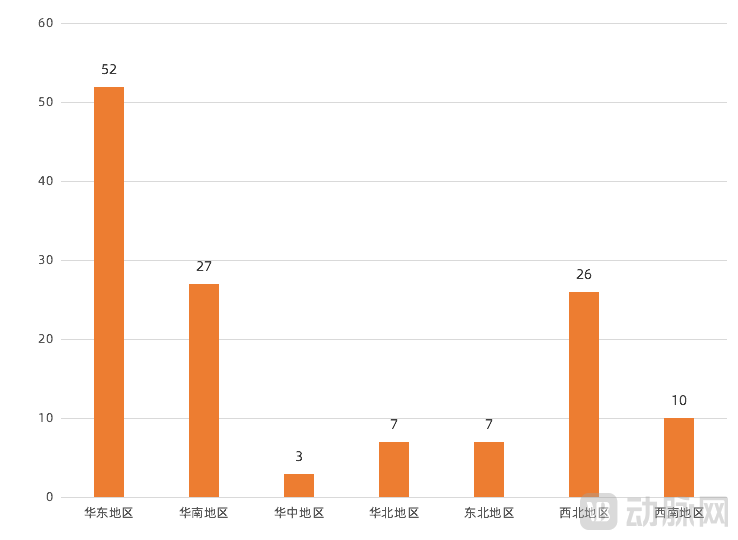

(4) Regional Distribution

According to statistics from VCBeat Research Institute, an analysis of the distribution of institutions purchasing medical AI products over the past year shows that East China holds a leading position. South China and Northwest China follow closely behind, but their procurement volumes are only half that of East China, while other regions exhibit relatively low demand for AI products.

Regional Distribution Statistics of Hospital-Side Medical AI Product Procurement

Support in East China stems from the open environment for smart hospital construction in Jiangsu, Zhejiang, and Shanghai. Whether in terms of electronic medical record (EMR) grading, interoperability certification, smart hospital service ratings, or the policy formulation and implementation of medical AI devices (such as those under the “New Infrastructure” initiative), this region remains at the forefront nationwide.

The pricing and sales models of medical AI products have a certain impact on their sales volume. Further analysis of procurement prices has revealed three major trends.

Distribution of Unit Purchase Prices for Hospital-Side Medical AI Products

(1) The average transaction value for medical IT applications is generally higher than that of AI-based imaging services.

Data indicates that medical IT applications, such as medical record quality control, Clinical Decision Support Systems (CDSS), and AI-powered research platforms, command relatively high average transaction values, with software procurement ranging from RMB 1 million to 3.5 million and exhibiting substantial demand. In contrast, AI-driven imaging services are priced between RMB 300,000 and 1.5 million, predominantly clustering around the RMB 1 million mark.

(2) AI for Imaging Services Seeks Diversified Sales Channels to Offset R&D and Marketing Costs

At the current stage, hospital procurement of AI-based imaging services is primarily concentrated in radiology departments, resulting in relatively limited demand. However, developing an AI medical device typically incurs sales and R&D costs amounting to hundreds of millions of yuan. To bridge this substantial gap, a reasonable approach is to shift from the traditional model of centralized hospital procurement to a per-case payment model. According to companies, while there is currently little difference in revenue between the procurement-based and per-case pricing models, the latter is expected to generate greater long-term revenue for medical AI enterprises.

(3) Policy interventions may help improve the sales performance of AI-based medical devices

As a novel innovation, AI-powered imaging services face significant challenges in hospital implementation and lack bargaining power. Hospitals, accustomed to traditional procurement models, are unlikely to accept procurement solutions with higher costs. Therefore, policy intervention is needed for medical AI to ensure long-term alignment between the price and value of AI-powered imaging services. On August 31, 2021, eight national ministries and commissions jointly issued the Pilot Program for Deepening the Reform of Medical Service Prices. Three key points outlined in the document will significantly impact the future sales of AI-powered imaging services.

Reviewing the developments over the one-year period from September 2020 to August 2021, the most significant change in medical artificial intelligence (AI) has been the transition from “chaos” to “transparency.” In August 2020, Unisound, a broad-spectrum AI company with extensive industry involvement, was the first to file its prospectus. It was followed by Yidu Cloud, a medical AI and big data company, which successfully listed on the NASDAQ on January 15, 2021, becoming the first medical AI company to enter the secondary market.

In 2021, Keya Medical, Airdoc (Shanghai), Infervision, and Shukun Technology each filed their prospectuses, disclosing business data to the public across three major AI-driven healthcare segments: cardiac imaging, fundus examination, and pulmonary diagnostics. As the medical AI industry enters its second half, with a clearer picture of corporate operations emerging, the competitive advantages that companies need to build are gradually shifting.

Compared with AI unicorns across various industries, medical AI companies have relatively lower revenue levels. Medical AI companies focusing primarily on medical imaging report annual revenues ranging from tens of millions to hundreds of millions of yuan. Those offering a broader portfolio—including medical imaging, health informatics, and pharmaceutical sales—achieve post-tax revenues in the range of hundreds of millions to billions of yuan (with a significant portion of their revenue derived from pharmaceutical sales). Meanwhile, among general-purpose AI companies that also operate in the healthcare sector, revenue from their medical AI business lags behind that of other industries. For example, iFlytek’s medical-related revenue in 2020 amounted to RMB 313 million, accounting for only 2.4% of its total revenue.

Summary of Operating Revenues of AI Companies (Unisound and CloudWalk Technology data covers January–June 2020)

Numerous factors influence the revenue scale of medical AI enterprises, including incomplete financial data statistics, low penetration rates, limited applicable scenarios, constrained procurement budgets, product types, the limited number of hospitals, and business models.

AI companies not involved in medical services typically have hardware sales of a certain scale, such as iFlytek’s voice recorders and SenseTime’s intelligent facial recognition terminals. This segment of sales reduces the gross profit margin of these AI enterprises but significantly boosts their revenue. In contrast, medical AI companies specializing in imaging, such as Keya Medical and Infervision, primarily offer software-oriented products like platforms and solutions, resulting in higher gross profit margins but relatively lower sales revenue.

Summary of Gross Profit Margins for AI Companies (Unisound and CloudWalk Technology: January–June 2020)

Despite differences in scale, most medical AI companies have seen their revenues multiply several times over in the past two years. In addition to Yidu Tech and LinkDoc Technology listed in the table, imaging-focused AI firms Infervision and Shukun Technology also experienced a multi-fold increase in sales revenue in the early part of 2021.

Infervision generated RMB 22.13 million in revenue in the first quarter of 2021, a year-on-year increase of 357% from RMB 4.84 million in the same period last year; Shukun Technology recorded operating revenue of RMB 52.62 million in the first half of 2021, a year-on-year surge of 681% from RMB 6.74 million in the corresponding period last year. Based on this trend, it is likely that an AI medical imaging company with annual operating revenue exceeding RMB 100 million will emerge in 2021.

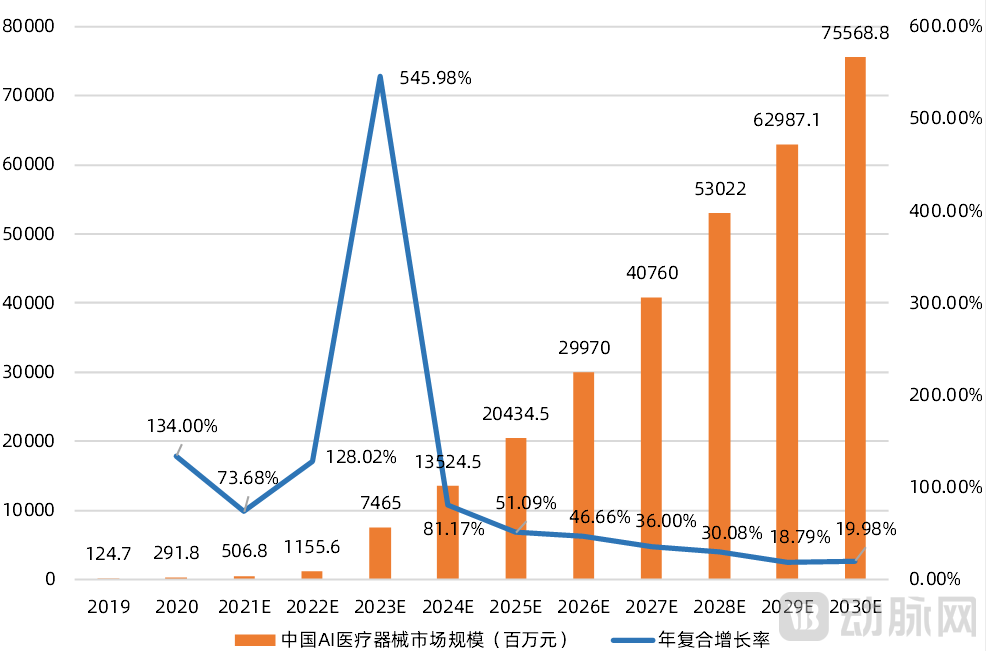

Market Size and Growth Trends of AI Medical Devices in China

Low penetration rates pose a challenge for AI enterprises, but also represent their opportunity. As healthcare institutions’ awareness of artificial intelligence continues to rise, the revenue scale of medical imaging AI is poised to experience exponential growth within the next decade.

For AI companies specializing in medical imaging, the pivotal point of trend transformation lies in regulatory review and approval. As indicated by the data presented earlier, once these companies successfully navigate the registration and market access process, their operating revenues show significant growth. Based on this trend, it is projected that the operating revenues of medical imaging AI enterprises will face two major leapfrog points in the future. The first leap stems from gaining approval for pricing inclusion, which signifies the formal integration of AI into medical imaging services, with fee-for-service becoming one of their primary business models; this represents a breakthrough in pricing. The second leap arises from securing reimbursement coverage under national health insurance, which means AI will officially adopt a strategy of trading price for volume, achieving an order-of-magnitude increase in utilization.

The above isReport Highlights: Table of Contents Below. Scan the Mini Program QR Code at the End to Read the Full Report for FreeText:

I. The Multi-Billion-Dollar Medical AI Market Faces a Turning Point

1.1 Market: Drug R&D, Medical Imaging, and Healthcare Informatics Form the Core Landscape of AI

1.2 Policy: Rating Determines Essential Demand, and Device Review Guidelines Drive Innovation

1.3 Trends: From Tertiary Hospitals to Grassroots Levels, from To-H to To-B

II. Over Half of the Sectors Achieve Commercialization, with the First Glimmers of Profitability Emerging

2.1 Mature Sector: Parallel Commercialization Inside and Outside Hospitals

2.2 High-Potential Segments: Commercialization Shifting Toward Out-of-Hospital Settings

2.3 Maturity: 11 Enter Commercialization Exploration

2.4 Development: Text-based AI Leads Imaging-based AI

III. Post-Market Access: Low Unit Prices Drive Exploration of New Business Models

3.1 Review: Three Major Factors Drive 19 AI-Powered Medical Devices to Obtain Certification

3.2 Procurement: Grade 3A Hospitals Account for 47%, Medical IT Sector Exceeds Two-Thirds

3.3 Unit Price: Fluctuating Around the Million-Yuan Mark, Imaging AI Seeks Pricing Approval

IV. High Gross Margins and Heavy R&D Investment Drive Multi-Fold Revenue Growth in Medical AI

4.1 Operational Data: Imaging AI Revenue Reaches the Tens of Millions, with Drug-Related Business Exceeding 100 Million

4.2 Cost Data: Sales Expenses Expand Several Fold, While R&D Proportion Relatively Shrinks

4.3 Clinical Data: Multicenter Clinical Trials Are the Prevailing Trend

4.4 Corporate Information: Benchmark Enterprises Lead Industry Development

V. Influx of Billions in Capital, with M&A and IPOs Becoming the Dominant Themes

5.1 Recovery: 108 Deals in 8 Months, Data Fully Surpasses 2020 Levels

5.2 Divergence: Imaging Financing Skews Toward Late-Stage, While AI Drug Discovery Attracts Fresh Talent

5.3 Trends: Significant Head-End Aggregation Effect, Medical AI Enters the Second Half