30 Billion RMB Peripheral Vascular Market: Who Will Lead as Four Companies File IPOs and Billions Pour into R&D?

Cardiovascular disease has consistently remained the leading cause of death among both urban and rural residents in China. According to projected data from the "Summary Report on Cardiovascular Health and Diseases in China 2020," the current number of patients with cardiovascular diseases in China has reached 330 million. This substantial patient population has also driven the vigorous development of the domestic high-value cardiovascular consumables industry, with the vascular interventional high-value consumables sector serving as a forefront of innovation within China's medical device industry.

Vascular interventions can be categorized into three major fields: coronary intervention, neurointervention, and peripheral intervention. In 2021, China’s peripheral intervention industry entered a phase of commercial maturation, with multiple domestic peripheral intervention companies going public.We believe that the peripheral intervention market has a larger patient base and stronger growth momentum than the coronary intervention market; compared with neurointervention, peripheral intervention features diverse procedural techniques and offers broader market potential.

The existing peripheral intervention market, whether for peripheral arteries or veins, is dominated by multinational corporations. However, Chinese companies are rising rapidly, with multiple core products having achieved commercialization, signaling that the peripheral intervention sector is entering a critical period for domestic substitution.

At this critical juncture in the market’s development, VCBeat Research Institute has produced the “2021 Peripheral Intervention Report” through surveys and interviews with domestic vascular surgery experts, key participants in the peripheral intervention sector both in China and abroad, and R&D engineers. This report discusses the historical development of peripheral intervention in China, an overview of the peripheral intervention market, the current status and future trends in the treatment of peripheral arterial and venous diseases, as well as major products and key players in peripheral intervention. Drawing on extensive industry research and accumulated expertise, VCBeat Research Institute provides a detailed and in-depth analysis of the peripheral intervention industry, focusing on its classification, competitive landscape, market size, investment logic, and investment targets.

In this report, we present five directional conclusions regarding the peripheral interventional industry at its current stage.

1. Peripheral vascular disease is a highly prevalent condition that remains underdiagnosed and undertreated; the penetration rate of interventional revascularization will grow rapidly driven by the vigorous development of vascular surgery.

2. The current peripheral intervention market, encompassing both peripheral arteries and veins, is dominated by multinational corporations; however, Chinese enterprises are rising rapidly, with multiple core products having achieved commercialization, signaling that the sector is entering a critical period for domestic substitution.

3. The peripheral intervention market comprises three major categories: peripheral arteries, peripheral veins, and access consumables. Peripheral arteries account for the largest share, while peripheral veins are experiencing a higher growth rate.

4. In the field of peripheral venous interventions, off-label use is currently prevalent. Existing products fail to meet clinical needs, creating an urgent demand for the development of innovative products tailored to peripheral venous diseases.

5. Implant-free interventional solutions can avoid device-related organ injury and reduce the risk of bleeding, and are gradually becoming the mainstream approach in peripheral interventions.

Peripheral intervention primarily involves the blood vessels of the trunk and extremities, excluding the aorta, within the human circulatory system. Peripheral vessels are categorized into peripheral arteries and veins, and peripheral vascular diseases are accordingly classified into peripheral arterial disease and peripheral venous disease.

Peripheral vascular disease involves the peripheral blood vessels throughout the body, affecting hundreds of millions of patients.

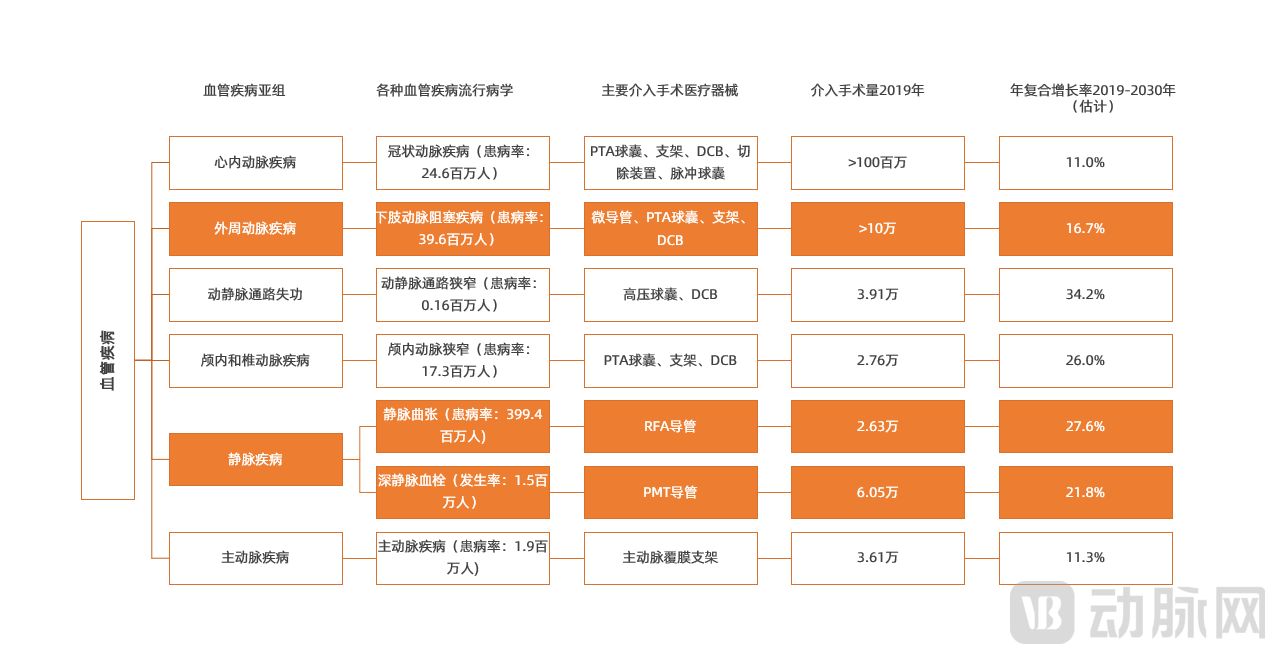

Epidemiological Overview of Major Vascular Diseases and Key Related ProductsSource: Acandis Prospectus; Prepared by VCBeat

Peripheral Artery Disease (PAD) refers to arterial diseases occurring outside the heart and brain. PAD is primarily characterized by the formation of atherosclerotic plaques in peripheral vessels such as the common iliac artery, femoral artery, radial artery, and brachial artery, resulting in vascular stenosis exceeding 50%. The consequences of PAD are severe, including intermittent claudication and amputation; it also increases the incidence of severe hypertension, renal failure, myocardial infarction, stroke, and cardiac death. Peripheral artery disease is the third leading cause of atherosclerotic vascular disease, following coronary heart disease and stroke.

Peripheral veins generally refer to medium- or smaller-sized veins located outside the thoracic and abdominal cavities, typically those in the head, neck, and extremities. Venous diseases are categorized into two main types: chronic venous insufficiency and venous thromboembolism. Chronic venous insufficiency primarily includes valvular incompetence, varicose veins, and post-thrombotic syndrome. Venous thromboembolism mainly comprises deep vein thrombosis (DVT) and pulmonary thromboembolism (PTE), with PTE predominantly arising from DVT.

Peripheral interventional therapy has been rapidly developing in China alongside the vigorous growth of vascular surgery. Peripheral interventional procedures are primarily performed within the field of vascular surgery.

History of the Development of Peripheral Artery Disease TreatmentSource: VCBeat

Vascular surgery is an emerging specialty that has been developing in China for only one to two decades. Although China started later than other countries, the field has experienced vigorous growth. Vascular surgery became an independent discipline only after the 1980s. After 2002, interventional therapy products began to be used in vascular surgery in China. Since 2005, Chinese vascular surgery has entered a new era of minimally invasive techniques and rapid development, with interventional therapies largely replacing traditional open surgeries. In 2012, there were approximately 230 hospitals in China with independent vascular surgery departments; most vascular surgery units were affiliated with general surgery departments, and the total number of physicians specializing in vascular surgery was fewer than 1,500. This shortage of specialists meant that many diseases, although easily identifiable, were difficult for physicians to diagnose, leading to misdiagnosis or missed diagnoses. Currently, however, there are more than 10,000 officially registered vascular surgeons in China. The development of vascular surgery in China is not yet saturated: while there are roughly 4,000–5,000 Grade A tertiary hospitals in the country, fewer than one-quarter have established dedicated vascular surgery departments.

The volume of interventional procedures for peripheral vascular disease (PVD) is growing at a rate as high as 15%. Although PVD affects a large population, its penetration rate for interventional therapy has historically been low. This is due to the disease’s prolonged course, with an extended asymptomatic early stage and clinical manifestations—such as changes in limb blood pressure and other symptoms—appearing only in late stages. In contrast, coronary artery disease benefits from higher awareness and treatment rates. Currently, PVD is experiencing rapid growth, with the compound annual growth rate (CAGR) of interventional procedures for both peripheral artery disease (PAD) and venous diseases exceeding 15%, significantly outpacing the growth in interventional procedure volumes for other vascular conditions.

Overall, the peripheral intervention market is a rapidly expanding and underexploited market.

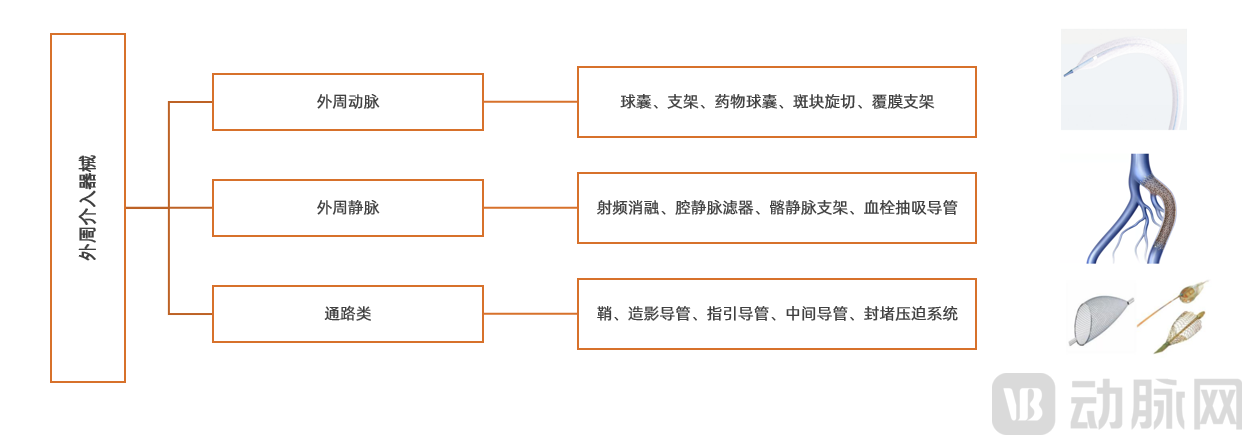

Classification of Devices in the Peripheral Intervention Market Source: VCBeat

Peripheral Artery Disease: A Major Healthcare Challenge in China

Peripheral arterial disease encompasses a broad spectrum, accounting for half of all vascular conditions.Peripheral Artery Disease (PAD) refers to arterial vascular lesions excluding those of the coronary arteries, intracranial arteries, and aorta, primarily involving lesions of the lower extremity arteries, carotid and vertebral arteries, upper extremity arteries, renal arteries, and mesenteric arteries.

Peripheral arterial disease has serious consequences, leading to intermittent claudication, rest pain in the lower extremities, severe hypertension and renal failure, carotid artery stenosis, etc.Over the 5-year natural course of peripheral artery disease (PAD), 10%–15% of patients experience cardiovascular death, and 5%–10% progress to critical limb ischemia (CLI). Early detection and intervention help improve prognosis. The 1-year mortality rate for CLI patients exceeds 50%, with a 5-year mortality rate of 70%; nearly half of cases require surgical intervention for limb salvage.

Among the many subsegments of peripheral artery disease (PAD), lower extremity artery disease (LEAD) is the most mature market segment.

Lower Extremity Artery Disease (LEAD) is the most common manifestation of atherosclerosis-induced peripheral artery disease, with lower extremity artery disease accounting for approximately 80% of all peripheral artery disease cases. Therefore, in the market strategies of major participants in the peripheral intervention market, the term "peripheral artery market" often refers specifically to lower extremity artery disease.

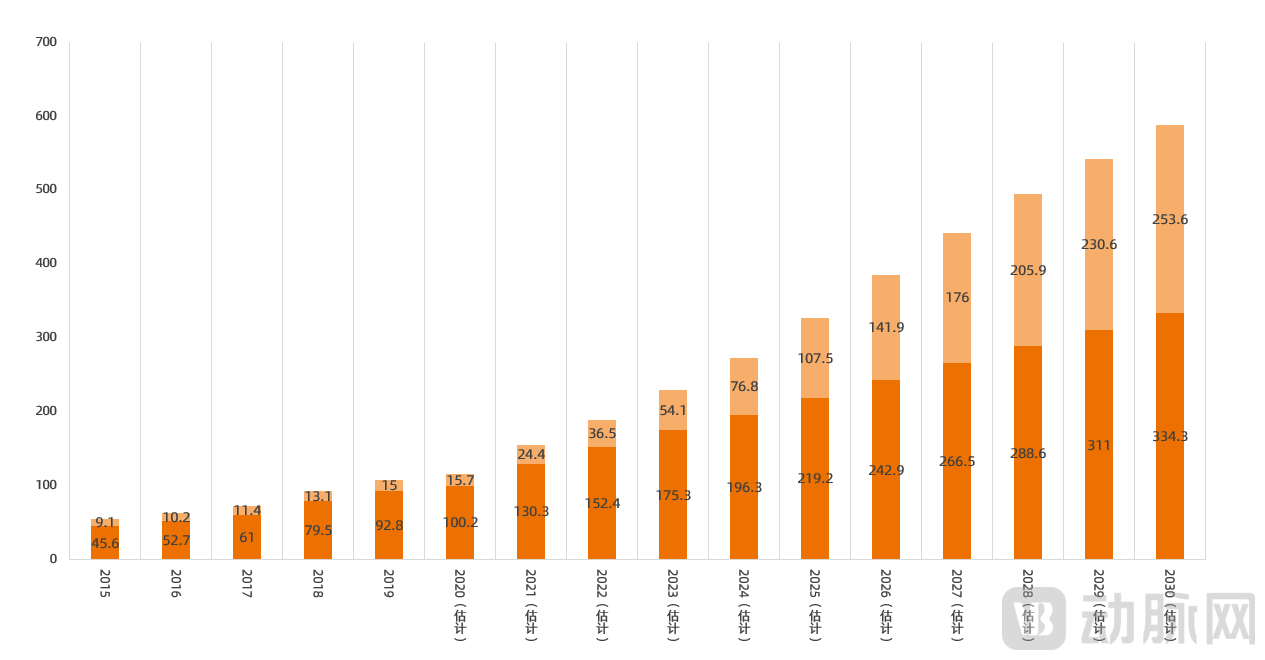

The current state of undertreatment for lower extremity arterial disease is gradually changing, with the number of patients receiving treatment for this condition expected to grow at a compound annual growth rate (CAGR) of 20.4% in the future.In the past, due to the insidious progression of the disease and the prolonged asymptomatic period in patients, few individuals with lower extremity arterial disease (LEAD) underwent interventional therapy. With the vigorous development of vascular surgery in China, advancements in imaging technology and its increased clinical application have improved the detection rate of vascular diseases. Coupled with improvements in public living standards and other factors, the treatment rate for LEAD has been steadily rising. The compound annual growth rate (CAGR) of lower extremity arterial interventional procedures in China was 18.5% from 2015 to 2019; the CAGR is projected to reach 20.4% from 2019 to 2024.

Historical and Projected Number of Lower Extremity Artery Interventional Procedures in China (2015–2030) (in thousands) Source: Prospectus of Genius Med, prepared by VCBeat

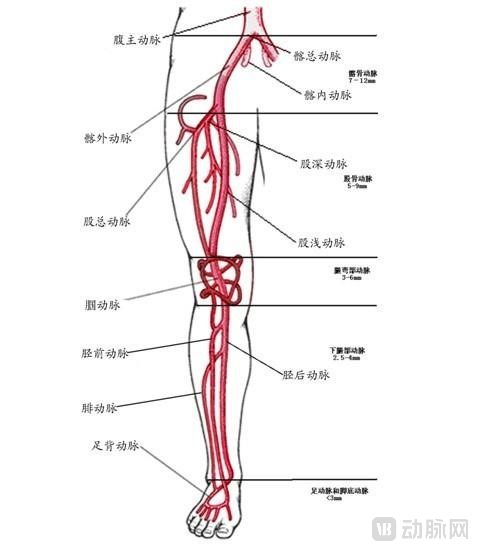

The lesions of lower extremity arterial disease are predominantly distributed in the femoropopliteal artery and the three infrapopliteal branches, often presenting as long-segment lesions, total occlusions, and severe calcification. Classified according to the anatomical location of the target lesion,Lower extremity arterial interventional procedures are generally categorized into above-knee and below-knee interventions.

Schematic Diagram of Lower Extremity Arterial Anatomy. Source: Merck Manual

Above-Knee InterventionIt primarily involves lesions of the superficial femoral artery (SFA) and the popliteal artery (PA). The superficial femoral artery is the main artery supplying blood to the lower leg and foot. The popliteal artery is located posterior to the knee joint; it is the continuation of the superficial femoral artery as it extends distally into the popliteal fossa, where it is termed the popliteal artery. Atherosclerotic occlusive disease of the femoropopliteal segment is a common condition in vascular surgery and represents the manifestation of systemic atherosclerosis in the lower extremities.

Below-the-Knee InterventionThis primarily targets pathologies of the tibial, peroneal, and dorsalis pedis arteries. Below-the-knee (BTK) arterial lumens are more slender, with smaller vessel diameters. In terms of etiology, diabetes is the primary cause of BTK atherosclerotic lesions. Hyperglycemia impairs active cellular uptake of nutrients and oxygen, hinders effective immune system function, and exacerbates systemic cellular inflammation, ultimately leading to delayed wound healing and ulceration in the feet, known as diabetic foot.

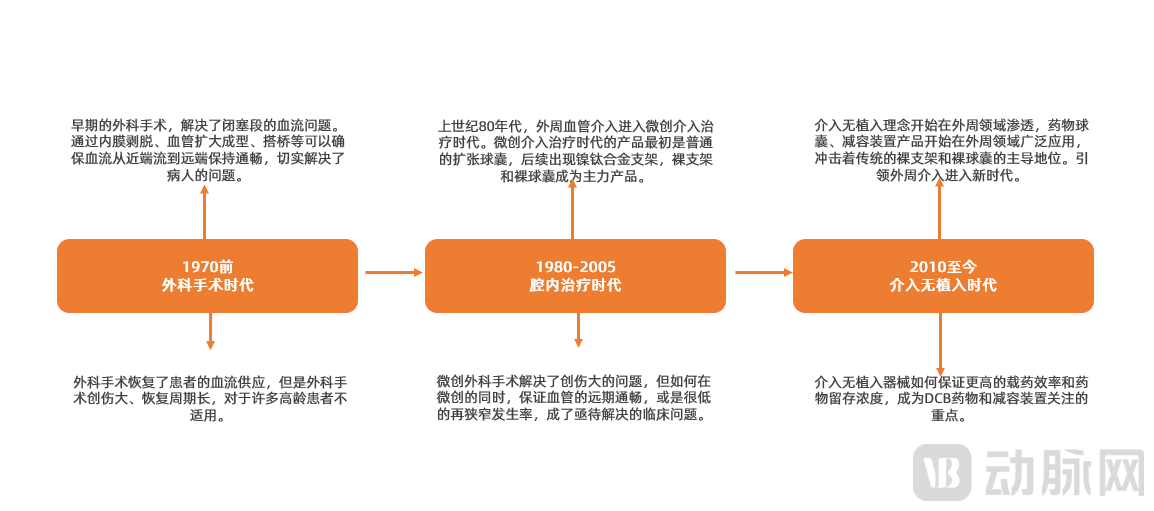

The treatment of lower extremity arterial disease (LEAD) has evolved through several eras: early surgical intervention, plain balloon angioplasty, nitinol stenting, and the era of drug-eluting device combinations. In the late 1980s, the treatment of peripheral artery disease (PAD) entered the endovascular intervention era. Driven by advancements in medical devices, endovascular therapy has surpassed traditional surgery in efficacy and gradually become the preferred treatment option for PAD.

After decades of development in endovascular intervention, a variety of products are now available for clinicians to choose from.

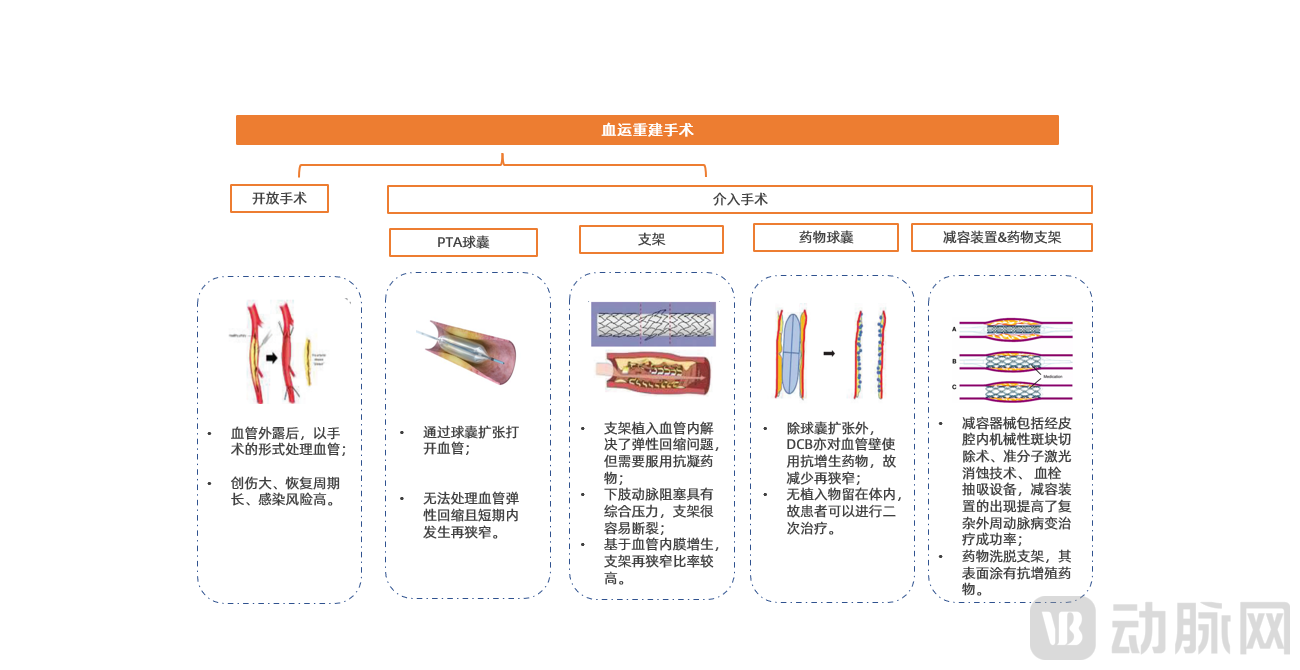

Currently, the primary endovascular treatment modalities in the field of peripheral interventions include percutaneous transluminal angioplasty (PTA), stent implantation, atherectomy, laser angioplasty, cutting balloons, drug-coated balloons (DCBs), and pharmacological thrombolysis or thrombectomy. Broadly categorized, interventional devices for revascularization can be divided into traditional bare-metal stents and plain balloons; drug-eluting devices such as drug-coated balloons and drug-eluting stents; and debulking devices, including rotational atherectomy, laser plaque ablation, mechanical thrombectomy, and orbital atherectomy. Clinical practice guidelines recommend different endovascular treatment strategies for various lower extremity arterial diseases. This report interprets the product recommendations outlined in the clinical practice guidelines for the diagnosis and treatment of peripheral artery disease.

Classification of Revascularization Procedures Source: VCBeat

In terms of the product landscape, traditional bare-metal stents and plain balloon catheters remain the mainstream products in the high-value consumables market for peripheral arteries; however, they are limited by their relatively high rates of restenosis.

Bare-metal stent

Bare-metal stents face significant challenges with in-stent restenosis (ISR). In peripheral vessels, the femoropopliteal artery is subjected to complex mechanical forces, including radial compression, axial shortening, torsion, and bending. Following implantation, stents not only affect the treated vessel segment but also exert mechanical influences on adjacent vascular segments. Particularly near joint areas, repetitive bending and folding predispose stents to deformation and fracture, thereby compromising vessel patency. The current bare-metal stent market is dominated by imported products, with limited participation from domestic manufacturers.

Plain Balloon

Plain balloon angioplasty is associated with a high rate of restenosis; therefore, PTA balloons are primarily used for predilation. A balloon dilation catheter consists of a balloon and a catheter shaft. It is mainly employed to treat peripheral arterial stenosis caused by thrombi or plaques. By inflating the balloon at high pressure, the inner elastic lamina is disrupted, and the plaque is compressed. This approach involves no foreign body implantation, offering simple operation and low cost. However, its limitations include an inability to fully overcome elastic recoil of the lesion, incomplete prevention of flow-limiting dissections, and a high post-treatment restenosis rate, leading to suboptimal prognosis. In terms of market landscape, plain balloon angioplasty is currently dominated by Medtronic, while multiple domestically produced products have already received regulatory approval.

Drug-Coated Balloon

Drug-coated balloons are balloon catheters coated with antiproliferative drugs. The antiproliferative drug currently most commonly used in peripheral drug-coated balloons is paclitaxel, which is released into the vessel upon balloon inflation. Drug-coated balloons are widely used in coronary and peripheral interventions in Europe. In China, clinicians currently have a high level of confidence in the efficacy of drug-coated balloons, with substantial clinical evidence demonstrating that they reduce restenosis after treatment.

DCB stands out in the treatment of above-the-knee lesions in the lower extremities, challenging the dominance of bare-metal stents and plain balloon angioplasty; in below-the-knee lesions, DCB is regarded as a breakthrough therapy.Drug-coated balloon (DCB) therapy, offering numerous advantages over traditional treatments, has seen a rapid increase in the volume of infrapopliteal interventions. DCB procedures are expected to account for the majority of lower extremity endovascular interventions. In 2016, the first domestically produced DCB product for lower extremity arterial intervention, manufactured by Acotec Scientific, was launched in China, marking the start of market growth from zero. According to data from Acotec Scientific’s prospectus: the number of lower extremity arterial DCB procedures rose to 12,000 in 2019 and is estimated to reach 105,000 by 2024 (including 25,000 infrapopliteal DCB procedures), representing a compound annual growth rate (CAGR) of 53.9% from 2019 to 2024. The volume is further projected to grow at a CAGR of 23.9% from 2024 to 2030, reaching 380,600 procedures by 2030 (including 153,500 infrapopliteal DCB procedures).

Currently, drug-coated balloons (DCBs) are used in 50% of lower extremity endovascular interventions at top-tier Grade A tertiary hospitals in China. It is projected that the national average usage rate will reach this level within the next three to five years. Furthermore, DCBs have been widely included in medical insurance reimbursement schemes, with nearly 20 provinces in China currently providing coverage for these devices. An analysis of the major peripheral vascular indications for DCBs suggests that the Chinese market is still in its early stages, offering substantial potential for growth. This report examines the market potential for DCBs in various clinical scenarios, including lower extremity arterial stenosis, renal artery stenosis, stenosis of arteriovenous fistulas for hemodialysis, and carotid/vertebral artery stenosis.

Drug-Eluting Stent

Drug-eluting stents (DES) consist of a stent and a polymer coating that binds the drug to the stent. The drug is an antiproliferative agent released from the stent onto the vessel wall. An auxiliary balloon on the DES facilitates stent expansion, and the stent remains within the vessel to exert its therapeutic effect. DES can address acute elastic recoil following balloon angioplasty, while the release of the antiproliferative drug is more controllable. Drug-eluting stents have been used for many years in coronary interventions and are only beginning to be applied in the treatment of lower extremity artery disease (LEAD).

Peripheral drug-eluting stents (DES) in China are dominated by imported manufacturers, and long-term prognostic data remain scarce. Currently, two drug-eluting stents are marketed in China: Cook’s Zilver PTX and Boston Scientific’s Eluvia. Both Zilver PTX and Eluvia use paclitaxel as the coating drug, but they differ in drug dosage. Zilver PTX features a direct coating without polymer or other components. In contrast, the Eluvia stent incorporates a polymer, with an adhesive layer between the polymer and the stent strut, enabling a significantly lower drug dose—approximately 1/20 to 1/15 of that in Zilver PTX, or about 0.16 µg/mm². Although multiple drug-eluting stents have been launched in the Chinese market, their approval dates are relatively recent, and long-term prognostic data are still lacking.

Decompression Devices

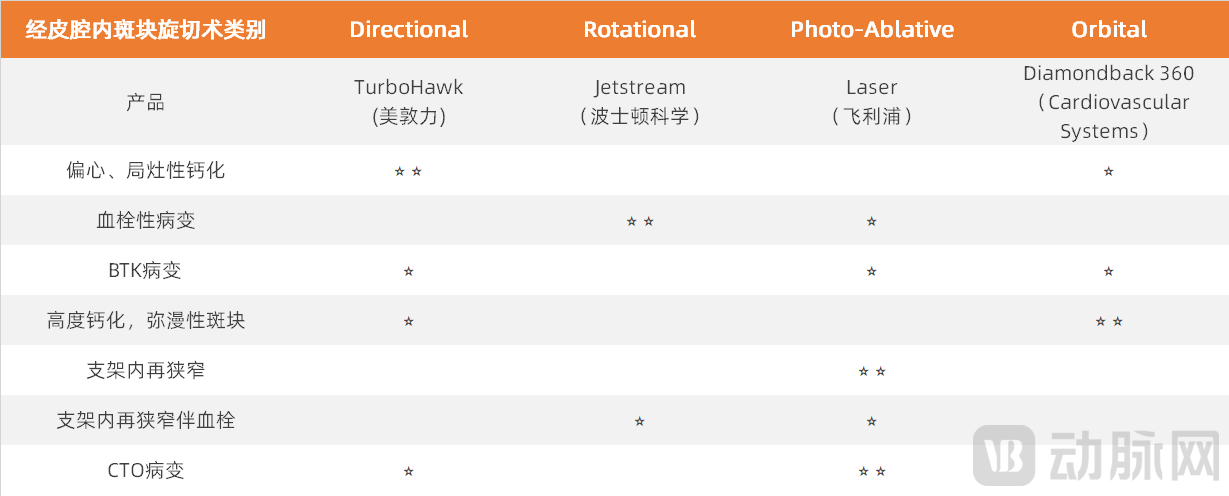

Driven by the clinical philosophy of "intervention without implantation" to reduce the incidence of restenosis following endovascular therapy, the concept of debulking has emerged. Debulking devices are designed to remove plaque from the vascular lumen. Currently, several debulking devices widely used in China primarily include rotational atherectomy (RA), directional atherectomy (DA), excimer laser ablation (ELA), percutaneous mechanical thrombectomy (PMT), and orbital atherectomy (OA). Different debulking devices operate on distinct principles and are indicated for specific types of lesions.

Rotational Atherectomy (RA) is known as the “diamond drill” navigating within blood vessels. The procedure utilizes a high-speed rotating burr to pulverize atherosclerotic plaques and calcified tissues in arteries into extremely fine particles. RA grinds plaques into microparticles smaller than 5 μm (compared to red blood cells, which are 6–8 μm in diameter). These microparticles can be degraded by the human mononuclear phagocyte system, thereby eliminating plaque from the obstructed vascular lumen. This technique is indicated for severely calcified lesions. The global peripheral rotational atherectomy market is experiencing robust growth, with Cardiovascular Systems, Inc. (CSI) dominating the field of peripheral arterial rotational atherectomy.No peripheral rotational atherectomy products are currently available in China; Acotec’s product is expected to be launched in 2023.

Directional Atherectomy (DA) is characterized by a cutting blade positioned on the side of the device, enabling directional excision of tissue, which makes it particularly suitable for eccentric lesions. This technique effectively removes plaque from the vessel wall, thereby improving luminal gain and plaque debulking. Taking directional atherectomy as an example of debulking technologies, Medtronic’s atherectomy system has been marketed in China for over a decade; however, it has not achieved widespread adoption.

Laser Plaque Ablation (ELA) works by using laser-generated energy to ablate plaque into small particles, thereby achieving volume reduction. Mechanical thrombectomy primarily removes thrombi rapidly through mechanical aspiration.

The report analyzes the applicable scenarios for different debulking devices and the key companies involved.

Atherectomy Devices and the Advantages of Each DeviceSource:Atherectomy for Lower Extremity Intervention: Why, When, and Which Device? Produced by VCBeat

Peripheral venous disease refers to a syndrome characterized by a series of symptoms and signs caused by abnormal structure or function of veins, which leads to impaired venous return and elevated venous pressure. Its main clinical manifestations include heaviness, fatigue, distending pain, edema, varicose veins, trophic skin changes, and venous ulcers in the lower extremities.

Venous diseases account for approximately 60% of peripheral vascular diseases, predominantly affecting the lower extremities, with their incidence increasing year by year.

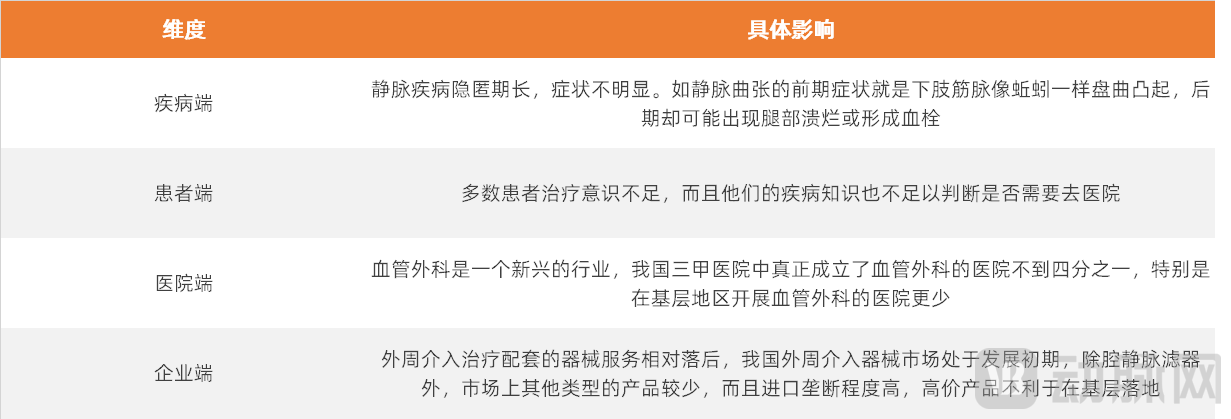

According to "China Cardiovascular Health and Disease 2020," the prevalence of lower extremity venous disease is 8.89%, representing nearly 100 million patients. In terms of patient population, China has 11.39 million patients with coronary heart disease, 13 million with stroke, and 8.9 million with heart failure; the number of patients with venous disease alone is several times higher than that of these other conditions. However, in terms of treatment rates, venous disease has the lowest rate among them. The treatment rate for surgical vascular diseases is low nationwide; for instance, only 0.2% of patients with peripheral artery disease received revascularization therapy, and the overall treatment rate for venous disease is even lower.

Factors Contributing to the Low Treatment Rate of Venous DiseasesSource: VCBeat

Common peripheral venous diseases in clinical practice mainly include varicose veins (VV), deep vein thrombosis (DVT), and iliac vein compression syndrome (IVCS).

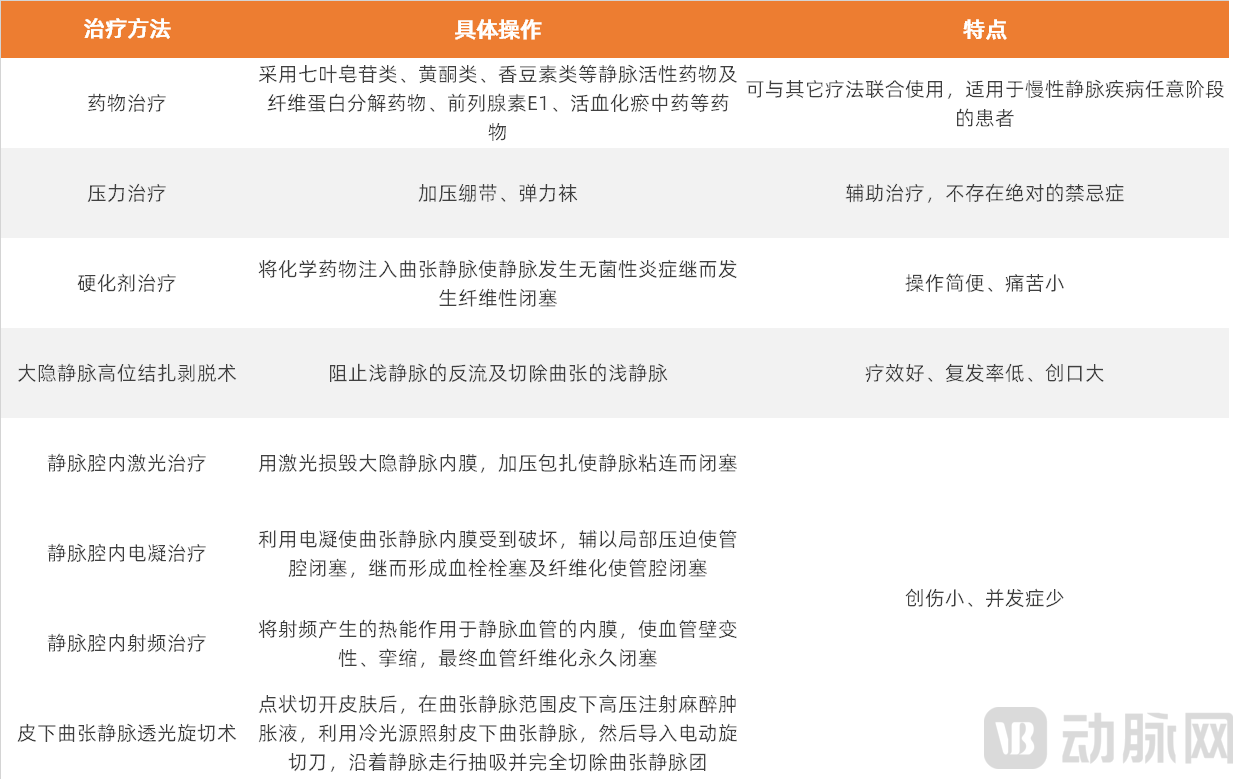

Varicose Veins

Varicose veins are the most common type of venous disease, characterized by high incidence and recurrence rates. "High ligation plus stripping of the great saphenous vein" is the traditional surgical treatment for varicose veins.

Radiofrequency ablation has become the mainstream treatment in recent years and is widely adopted in Europe and the United States. Clinically, radiofrequency ablation is suitable for vessels with larger diameters; however, its application is limited when treating small, tortuous veins, and patients with severe varicose veins cannot be managed with minimally invasive surgery alone. Therefore, to achieve better therapeutic outcomes, radiofrequency ablation can be combined with high ligation and stripping.

In addition to the aforementioned vein-ablative therapies, patients with varicose veins may undergo CHIVA (Conservative Hemodynamic Correction of Venous Insufficiency) surgery, a hemodynamic correction procedure that preserves the great saphenous vein. Following a detailed ultrasound-based hemodynamic assessment of the lower extremities, the surgeon ligates points of venous reflux and interrupts hydrostatic pressure columns, thereby reducing venous hydrostatic pressure in the great saphenous vein and its tributaries, altering lower-extremity venous hemodynamics, and ultimately alleviating or treating varicose veins. This technique was introduced to China by Dr. Zhang Qiang in 2011; however, due to the complexity of preoperative ultrasound assessment and the high technical difficulty of the procedure, its widespread adoption and training are expected to require several more years, grounded in hemodynamic theory and clinical evaluation.

The treatment of varicose veins has evolved from open surgical procedures to minimally invasive techniques, and now toward non-invasive approaches. SONOVEIN, the world’s first non-invasive robotic ultrasound system for treating varicose veins, has emerged as a groundbreaking innovation. It utilizes focused ultrasound to generate heat, causing the targeted veins to contract and seal shut. During the procedure, patients require neither needle punctures nor local anesthesia. Furthermore, the treatment leaves no scars, allowing patients to resume normal activities immediately afterward.

Deep Vein Thrombosis: The “Culprit” Behind Fatal Pulmonary Embolism

Deep Vein Thrombosis: The Invisible "Health Killer"Deep vein thrombosis (DVT) is a disorder of venous return caused by abnormal blood coagulation within the deep veins. It is primarily driven by three pathogenic factors: vascular wall injury, sluggish blood flow, and hypercoagulability. Consequently, pregnant women and patients undergoing orthopedic surgery are at heightened risk for developing DVT.

Treatment Options for Deep Vein Thrombosis: Percutaneous Mechanical Thrombectomy Offers a Minimally Invasive ApproachAnticoagulation is the cornerstone of deep vein thrombosis (DVT) management, as it inhibits thrombus propagation and facilitates spontaneous thrombolysis and venous recanalization. However, anticoagulation alone is insufficient for effective thrombus removal; therefore, thrombolytic therapy or surgical thrombectomy should be concurrently administered. Thrombolytic therapies include catheter-directed thrombolysis (CDT) and systemic thrombolysis. CDT involves the direct infusion of thrombolytic agents into the pulmonary arterial circulation via a multi-sidehole catheter, whereas systemic thrombolysis entails intravenous administration of thrombolytic drugs. Surgical thrombectomy encompasses both traditional open surgery and percutaneous mechanical thrombectomy.

Percutaneous mechanical thrombectomy refers to the percutaneous insertion of specialized thrombus ablation catheters into the vascular lumen to mechanically remove thrombi. These novel catheters are sophisticated automated mechanical devices capable of macerating, fragmenting, extracting, and dissolving thrombi. Compared with open surgery, this therapy offers advantages such as minimal invasiveness and favorable efficacy, and it has advanced rapidly in recent years. Furthermore, inferior vena cava (IVC) filters can be implanted to prevent free-floating thrombi from the lower extremity veins from migrating to the lungs and causing pulmonary embolism. However, long-term implantation of IVC filters may lead to complications such as recurrent venous thrombosis and infection. Therefore, routine use of IVC filters is not recommended for patients with deep vein thrombosis who are managed with anticoagulation therapy alone.

Iliac Vein Compression Syndrome: Caused by Venous Anatomical Structures

Iliac Vein Compression Syndrome, also known as Cockett Syndrome, refers to a syndrome in which the iliac vein is compressed by the iliac artery from its anterior aspect, leading to changes such as intraluminal adhesions, luminal stenosis, or venous occlusion, thereby causing iliac vein obstruction and a series of clinical symptoms. This condition is primarily caused by anatomical factors of the iliac vein. Clinically, Iliac Vein Compression Syndrome is classified into three stages: Stage I is characterized by simple venous compression without essential vascular changes, collateral formation, or other clinical symptoms; Stage II involves the formation of intravenous spurs; and Stage III is marked by iliofemoral venous thrombosis. Iliofemoral venous thrombosis is closely related to Iliac Vein Compression Syndrome, but it is not an inevitable consequence of common iliac vein compression syndrome. The number of patients with Iliac Vein Compression Syndrome is gradually increasing, with a significant growth rate. According to the prospectus of MicroPort Endovascular Tech, there were 700,000 cases of Iliac Vein Compression Syndrome in China in 2019, with a compound annual growth rate (CAGR) of 10.1% from 2019 to 2030. The number of cases is projected to reach 2 million by 2030.

Dedicated venous stents have become the primary interventional devices. For patients with iliac vein compression syndrome who are asymptomatic or present with mild symptoms, conservative management is typically adopted, including wearing compression stockings, improving lifestyle habits, avoiding prolonged bed rest or sitting, and taking anticoagulant medications when appropriate. For patients who subsequently develop lower extremity deep vein thrombosis, endovascular angioplasty with balloon dilation and stent implantation can be performed. Historically, arterial stents were commonly used in clinical practice to treat venous diseases; however, due to significant anatomical differences between arteries and veins, this approach was associated with a higher incidence of postoperative complications. With the continuous advancement of minimally invasive techniques, dedicated venous stenting has become the predominant clinical method for treating iliac vein occlusion.

In summary, venous diseases are characterized by a large patient population, significant long-term risks, and low treatment rates; minimally invasive interventional therapy will become the mainstream approach.

An analysis of clinical guideline treatment trends indicates that interventional therapy for venous diseases remains in its early stages of development globally. There are few clinical guidelines on venous diseases both domestically and internationally, highlighting an urgent need for updates and expansion.

Therapies for Chronic Venous Disease

In the market landscape for venous interventional devices, imports continue to dominate. Unlike the coronary stent market, which has evolved from “me-too” to “me-better” products, the venous intervention sector has yet to see truly mature offerings. There remains substantial room for innovation among domestic companies, particularly in thrombectomy catheters and venous stents.

Multinational corporations hold a leading position in the medical device sector, benefiting from industry-wide resource integration; however, few have prioritized venous intervention, resulting in less pronounced advantages in product iteration and upgrades. In contrast, domestic companies are focusing on the specialized niche of venous intervention, concentrating their efforts on innovative product development. Although the current peripheral intervention market in China features limited product diversity and no single company has yet established a comprehensive product portfolio, multiple enterprises are strategically positioning themselves in this direction, aiming to develop complete disease management solutions.

Domestic Brands Lead the Chinese IVC Filter Market, but Products Still Require Improvement.

Umbrella-shaped inferior vena cava (IVC) filters offer advantages in retrievability, allowing for prolonged implantation, but are prone to migration. In contrast, fusiform IVC filters are less likely to tilt within the body but have a shorter retrieval window, typically around two weeks. China offers a comprehensive range of IVC filter products, with domestic manufacturers holding a dominant market position. Currently, there are 10 IVC filters approved by the National Medical Products Administration (NMPA), including three domestically produced devices from Lifetech Scientific, Weihai Weixin, and Cossel Medical, each with one approved product. Lifetech Scientific’s Aegisy™ IVC filter commands a 56% share of the domestic market.

Currently, the application of inferior vena cava (IVC) filters still lacks prospective scientific data. Furthermore, non-standardized clinical use of IVC filters exists, which may lead to a series of complications such as thrombosis, thereby increasing the treatment burden on patients. Therefore, routine use of IVC filters is not recommended in clinical practice; their utilization should strictly adhere to relevant consensus statements and guidelines.

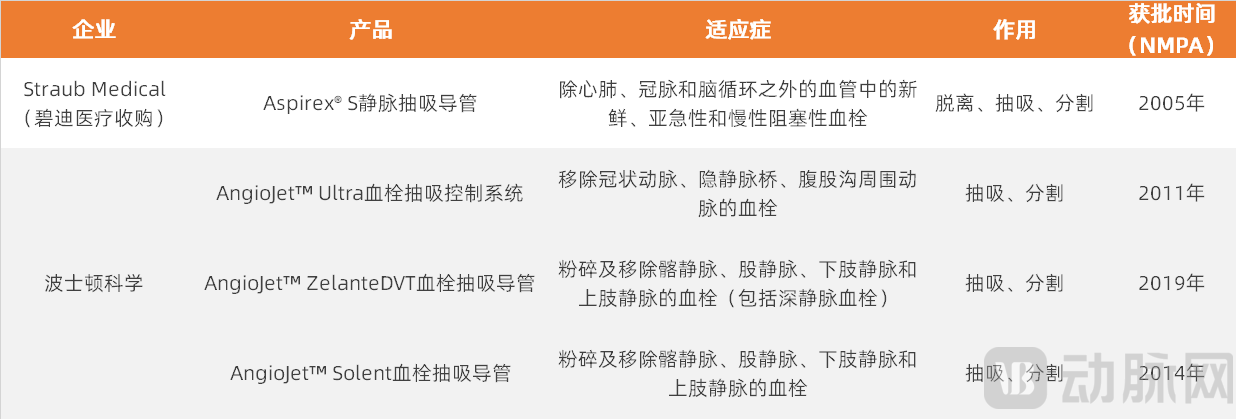

Absence of Domestically Produced Thrombectomy Catheters: New Catheters Require a Trade-off Between Efficacy and Risk.

Thrombus aspiration catheters are challenging to develop and present high technical barriers. These catheters utilize negative pressure to directly aspirate thrombi, making them suitable for larger and straighter blood vessels, with the advantages of broad indications and minimally invasive, high-efficiency performance. Thrombus aspiration catheters are indicated only for relatively fresh thrombi and cannot remove vascular plaques. Aspiration catheters have long been a key challenge in the field of mechanical thrombectomy, with their development consistently lagging behind that of stent retrievers. Clinically, there are stringent requirements for their kink resistance, intraluminal coating, and trackability. While they are widely used in the coronary field, only one domestically produced aspiration catheter has been approved for intracranial interventional procedures. In the peripheral thrombus aspiration market, Chinese brands are absent. All ten peripheral thrombus aspiration catheters currently approved by the NMPA are manufactured by foreign companies and were approved at an earlier stage. Although these catheters are indicated for peripheral use based on their labeling, most are used clinically only for coronary thrombus aspiration, with the exception of products from Straub Medical and Boston Scientific.

Approved thrombectomy catheters for peripheral veins,Source: National Medical Products Administration; Prepared by VCBeat.

Domestic and international companies are innovating in terms of the convenience, efficacy, and indications of novel aspiration catheters. Products from both Straub Medical and Boston Scientific fall under the category of novel mechanical thrombectomy devices. Unlike traditional single-function aspiration catheters, these new devices can simultaneously perform multiple functions, significantly enhancing the effectiveness of thrombus removal. However, while improving efficacy, such catheters also increase treatment risks. Innovative enterprises worldwide are currently inclined toward developing these types of novel devices.

Philips has launched the QuickClear mechanical thrombectomy system, which features an integrated, disposable vacuum pump and catheter for treating thrombi in peripheral arteries and veins. Unlike the bulky devices of traditional aspiration systems, its suction pump is handheld, offering significant miniaturization while maintaining robust aspiration performance. The system includes a 10F aspiration catheter that removes 59% more thrombus volume than an 8F catheter. This innovation enhances portability and ease of use, and the product has previously received FDA approval. Meanwhile, Penumbra, the global leader in aspiration thrombectomy catheters, has introduced Lightning 12, which combines the company’s latest-generation Indigo System CAT 12 aspiration catheter with Lightning Intelligent Aspiration. This integration enables physicians to optimize the thrombus removal process using the system’s clot detection mechanism. The FDA has previously approved the expanded indication of Lightning 12 for the treatment of pulmonary embolism.

Deep Vein Thrombosis Aspiration Catheters Poised to Expand Indications for Treating Pulmonary Embolism

The volume of aspiration procedures for deep vein thrombosis (DVT) in China is projected to reach 142,700 cases in 2024. This represents a market with significant potential, yet current product offerings remain far from sufficient. Domestic companies have been actively engaged in the research and development of related products, with major peripheral intervention players such as Acotec, JetMed, and Leo Medical all in the R&D pipeline, each focusing on distinct areas of innovation.

Xianruida’s peripheral thrombectomy aspiration system consists of a disposable suction connecting tube, an aspiration pump, and a thrombus aspiration catheter. It is used in percutaneous thrombectomy to treat thromboembolic pulmonary embolism and deep vein thrombosis of the lower extremities, making it one of the few domestically produced thrombus aspiration systems available for the treatment of pulmonary embolism.

The FDA’s approval of the Lighting 12 system for an expanded indication in pulmonary embolism (PE) underscores the feasibility of using thrombectomy catheters to treat deep vein thrombosis (DVT) and PE. Aortas’ thrombectomy catheter features a multi-segment design with sizes ranging from 4F to 9F, meeting the demands for arterial and venous thrombus aspiration in cases of extensive clot burden and thereby improving patient outcomes. In China, where few companies independently develop aspiration pumps, Aortas stands out as one of the few providers offering a comprehensive thrombectomy solution. The aspiration pump serves as a robust support component for the thrombectomy system, delivering sufficient suction power that surpasses traditional syringe-based methods. Aortas’ aspiration pump can continuously provide near-vacuum negative pressure and automatically adjust to pressure changes to minimize blood loss; this product received approval from the National Medical Products Administration (NMPA) in August 2021. According to NMPA data, domestically produced negative-pressure aspiration pumps for thrombus removal are scarce. This approval marks a critical step forward for Aortas in the field of mechanical thrombectomy, laying the foundation for subsequent approvals of its thrombectomy catheters.

Radiofrequency Ablation Technology Is Mature; Domestic Brands Are Poised to Emerge from Fertile Ground

Currently, three radiofrequency ablation catheters have been approved in China, all of which are imported products. Acotec, JetMed, and Hengrui Medicine have entered the radiofrequency ablation field, with their catheter products currently in the clinical trial stage.

Medtronic Has Built a Comprehensive Treatment Solution for Varicose Veins. In the Field of Radiofrequency Ablation, Medtronic Holds Absolute Dominance, with Its Radiofrequency Closure Catheter Being the First Product to Enter the Chinese Market. In 2015, Medtronic Acquired Covidien for Nearly $50 Billion, Thereby Gaining Its ClosureFast™ and ClosureRFS™ Radiofrequency Closure Catheters in the Peripheral Intervention Sector. Medtronic Developed Radiofrequency Ablation Catheters for Peripheral Applications Relatively Early, and Leveraging Its Corporate Scale, Its Ablation Products Maintain a Leading Position in the Chinese Market.

In addition to the ClosureFast™ system for treating superficial veins, Medtronic also offers the ClosureRFS™ radiofrequency catheter for treating perforator veins. While most companies focus primarily on superficial veins, Medtronic has developed a more comprehensive disease management solution. Since the launch of these two products, Medtronic has not introduced any new radiofrequency ablation catheters; instead, it is currently focusing on the VenaSeal closure system. Unlike traditional open stripping surgery and thermal ablation therapies, this closure system works by delivering a medical adhesive into the vein via a catheter to achieve venous occlusion. Although the product received FDA approval for varicose veins in 2015, its long-term efficacy remains to be validated, and it may not gain regulatory approval in China in the near term.

The application of radiofrequency ablation systems in the field of peripheral intervention in China is relatively limited. Intelligent innovation in these products will facilitate their market adoption and represents a strategic breakthrough for domestic companies. Beyond conventional radiofrequency ablation procedures, the integration of visualization and automated temperature control will inevitably raise the technical barriers to entry, thereby establishing a competitive advantage for manufacturers.

The ability to adjust output power during treatment is a feature of the EVRF radiofrequency ablation system. The radiofrequency ablation catheter from ZC Medical can also deliver radiofrequency energy to the heating element located in the distal treatment zone of the catheter, while simultaneously feeding back temperature data to the radiofrequency generator.

AcureMedical’s radiofrequency ablation system consists of a radiofrequency generator and a venous radiofrequency catheter. Many domestic players in the Chinese market can only manufacture radiofrequency ablation catheters and lack the capability to independently develop radiofrequency generators, which significantly reduces the competitiveness of their products. In addition, AcureMedical’s radiofrequency generator can automatically adjust output power, rapidly increase temperature, and automatically correct overheating to maintain temperature stability within the operating range. The product also features a low-output-voltage design and safety sensing capabilities, enhancing procedural safety. Furthermore, it measures and displays radiofrequency output power and connects with sensors in the catheter to provide real-time temperature monitoring during procedures. By integrating automation features into its adjustable radiofrequency platform, AcureMedical facilitates surgical operations for physicians.

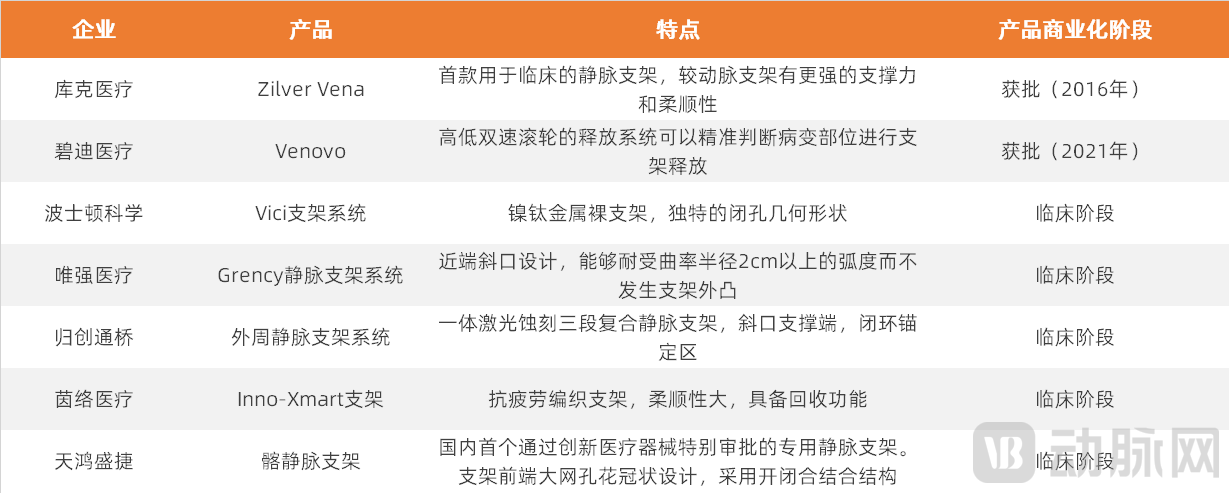

Iliac Vein Stents: Accumulated Strength Leads to Breakthroughs as Chinese Companies Secure Technological Leadership.

Significant Anatomical Differences Between Arteries and Veins; Lack of Dedicated Venous Stents in ChinaPeripheral venous stents can be used to treat occlusive diseases such as iliac vein compression syndrome or iliac vein stenosis. Until early 2019, there were no dedicated venous stents available in China, and arterial stents were commonly used as substitutes during interventional procedures. However, arteries and veins differ substantially in their anatomical structures: arteries have relatively smaller lumens, thicker walls, and greater elasticity, whereas veins have larger lumens, slower blood flow, and lower elasticity. Consequently, arterial stents may lack sufficient radial force to adequately expand venous lesions and may exhibit inadequate flexibility, potentially leading to complications such as thrombosis, vessel tearing, or perforation.

In China, there were 700,000 patients with iliac vein compression syndrome (IVCS) in 2019 alone, creating an urgent need for venous stents to address their treatment requirements. The development of dedicated iliac vein stents faces high technical barriers, as they must simultaneously meet requirements for compliance, radial force, and kink resistance. Located between the iliac artery and the spine, the iliac vein is subjected to repeated local compression from both structures; therefore, venous stents must possess sufficient crush resistance to dilate and maintain patency of the compressed vessels. Furthermore, given the curved morphology and complex anatomy of the iliac vein, these stents must also exhibit excellent flexibility.

Currently, there are two imported stent products approved in China, with five additional venous stents in clinical stages.

Domestic Iliac Vein StentsSource: National Medical Products Administration; prepared by VCBeat.

Venous disease is relatively complex, with risks of thrombosis and in-stent restenosis following iliac vein stenting. Moreover, as iliac vein stents are still in the early stages of development, long-term clinical data are currently lacking, and further evidence is needed to better understand patient prognosis.

Multiple Listed Companies Actively Expand Their Presence

Due to the high R&D complexity and costs associated with peripheral vascular intervention products, companies operating in the peripheral venous intervention sector tend to be of a certain scale. In the peripheral venous intervention market, alongside overseas players such as Medtronic and Boston Scientific, there are domestic enterprises including Acotec Science & Technology, Lifetech Scientific, Genesis MedTech, MicroPort Endovastec, and Leo Medical. Depending on their positioning and scale, each company pursues distinct business strategies. Leveraging their substantial market size and first-mover advantages, multinational corporations are committed to building comprehensive product portfolios.

Medtronic, Boston Scientific, and BD Medical, based in the United States with its advanced medical resources and strong backgrounds in the cardiovascular field, have extensively deployed in the peripheral intervention market. Through acquisitions, Medtronic’s two catheter products in the radiofrequency ablation field cover comprehensive solutions for superficial veins and perforator veins, while BD Medical has approved products in venous stents, filters, and aspiration catheters.

In the face of foreign monopolies in the peripheral venous intervention market and the demand for reduced healthcare costs, domestic companies have increasingly entered the peripheral intervention sector in recent years. Listed companies such as Acotec Scientific, MicroPort Endovastec, Lifetech Scientific, GeneTech, and Huitai Medical, along with innovative enterprises like InnoMed and Tianhong Shengjie, are actively participating in this space. Overall, China’s peripheral intervention market started later than its global counterparts and remains in a phase of rapid development. While domestic companies have made swift and significant strides in arterial interventions, most venous intervention products are still in the R&D stage. The venous intervention sector is expected to experience explosive growth in the coming years.

Major Players in China’s Peripheral Venous Intervention Market √ In Development ⚪ Approved Source: VCBeat Database, prepared by VCBeat Research Institute

The report selects Acotec, a leader in the peripheral vascular sector, as a domestic case study for analysis. Headquartered in Beijing, Acotec is an interventional medical device company primarily focused on interventional therapies for vascular diseases. In 2011, the company was acquired by Li Jing and entered the peripheral intervention industry, simultaneously initiating the research and development of PTA balloons and drug-coated balloons (DCBs). In 2016, Acotec launched its lower-extremity DCBs, AcoArt Orchid® and Dhalia™, for the treatment of femoropopliteal artery lesions. This product launch preceded similar competitors by four years, filling the gap in China’s peripheral market for DCBs and ending the long-standing reliance on imported products for peripheral vascular interventions in the domestic market. In 2019, Acotec broke through in the highly challenging therapeutic area of below-the-knee (BTK) stenosis by launching the AcoArt Tulip™ and Litos™ BTK DCBs. These products received FDA Breakthrough Device designation, becoming the first Chinese-developed medical devices to earn this distinction.

Acandis has developed a portfolio of interventional medical devices featuring world-leading technologies, particularly in the fields of drug-coated balloons and thrombectomy catheters. Moving forward, Acandis continues to deepen its expertise in the peripheral intervention sector, with a product pipeline covering three key market segments: peripheral arterial disease, venous disease, and vascular access consumables, providing comprehensive “intervention without implantation” solutions.

In terms of market coverage, Acotec started from scratch to create and cultivate the Chinese market for peripheral drug-coated balloons (DCBs), demonstrating strong marketing capabilities. In the second year following the launch of Acotec’s AcoArt Orchid® & Dhalia™, the usage volume of peripheral DCBs reached 8,000 units, rising to 15,000 units in 2019, with a compound annual growth rate (CAGR) of 36.9% from 2017 to 2019. Regarding hospital coverage, Acotec’s DCB products are available in more than 800 vascular intervention centers and over 90% of hospitals capable of performing peripheral vascular interventions in China.

In terms of revenue, Acotec has achieved continuous growth, with both revenue and gross profit doubling. In 2019 and 2020, Acotec Medical’s revenues were RMB 125 million and RMB 194 million, respectively, while the corresponding net losses were RMB 23.105 million and RMB 44.292 million. The company’s gross margins in 2019 and 2020 were 84.8% and 84.4%, respectively. R&D expenditures for 2019 and 2020 amounted to RMB 25.5 million and RMB 83.5 million, representing a 227% increase. Acotec continues to ramp up its R&D investment. The company’s first interim financial report after its listing also demonstrated strong performance potential. In the first half of 2021, Acotec reported revenue of RMB 140 million, a year-on-year increase of 106%, and gross profit of RMB 123 million, a year-on-year increase of 108%, achieving double-digit growth in both metrics. The company has consistently maintained a gross margin above 80%; during this reporting period, it rose by another 5 percentage points to reach 88.3%. As an R&D-intensive enterprise, Acotec recorded R&D expenses of RMB 61.375 million during the period, a year-on-year increase of 327.91%.

The above constitutes the main content of the report. The table of contents is as follows. Scan the mini-program QR code at the end of the article to read the full report for free:

I. Industry Overview: A High-Growth Potential Market

1. Peripheral Vascular Disease: Involves systemic peripheral vessels, affecting hundreds of millions of patients

2. Peripheral Interventional Therapy: Mainstream Treatment Modality, with Room for Improvement in Product Diversity

3. Peripheral Intervention Market: Dominated by Foreign Companies, Market Size to Reach RMB 30 Billion by 2030

II. Peripheral Arteries: The Main Battlefield in the Field of Peripheral Intervention

1. Peripheral Artery Disease: A Major Healthcare Challenge in China

2. Lower Extremity Arterial Disease: A Strategic Focal Point in Peripheral Artery Management

3. Classification of Lower Limb Diseases: Divided into Two Major Markets—Above-Knee and Below-Knee

4. Treatment Trends: DCBs Challenge the Dominance of Stents

5. Participant Analysis: Domestic Leaders Poised for Growth

6. Future Market Analysis: Vast Potential, Achievable Through Action

III. Peripheral Veins: The Overlooked Multi-Billion-Dollar Market

1. Peripheral Venous Disease: Large Patient Population, Low Treatment Rate

2. Disease Classification: The Three Major Diseases Draw the Most Attention

3. Treatment Trends: Moving Toward Endovascular Intervention

4. Interventional Product Analysis: Domestic Brands Are Still in the R&D Phase

5. Participant Analysis: Multiple Listed Companies Actively Expand Their Presence

6. Future Market Analysis: Amidst Fierce Competition, the Proactive Will Lead

IV. Peripheral Access: A High-Barrier Sector Dominated by Import Monopolies

1. Access Products: The First Step in Initiating Interventional Surgery

2. Market Landscape: Domestic Companies Face Technological and Brand Barriers

V. Overseas Cases: Pioneers from a Global Perspective

1. Medtronic: Under Pressure from Centralized Procurement, Peripheral Vascular Business Emerges as Growth Highlight

2. Boston Scientific: Strong Performance with Counter-Trend Growth in Peripheral Interventions

VI. Domestic Cases: New Forces in the Chinese Market

1. Development History: Becoming the Dominant Player in Peripheral Drug-Coated Balloons

2. Technology Platforms: Building Four Leading Technology Platforms

3. Core Products: Multiple Products Fill Market Gaps

4. Financial Analysis: Rapid Growth in R&D Investment

7. Development Trends: Intervention Without Implantation Is Gaining Momentum

1. Policy Environment: The Peripheral Intervention Market Enters a Golden Age of Development

2. Market Trends: Over 400 Million Patients Create a Multi-Billion-Dollar Blue Ocean Market

3. Product Trends: The "Intervention Without Implantation" Concept Gains Widespread Acclaim