The $7 Billion Bottleneck Segment: Who's Driving the Surge in Guiding Catheters and Wires Across Six Interventional Domains?

Reviewing the development trajectory of China's high-value consumables industry for vascular interventions, the domestic substitution of high-value consumables continues to advance into greater industrial depth.

Catheters and guidewires, previously regarded as the high-value consumables with the highest barriers in vascular interventions, are now witnessing a burgeoning trend of domestic substitution. As supportive devices, catheters and guidewires determine whether therapeutic products can be delivered to the lesion site during an interventional procedure, representing significant technical barriers. In coronary intervention surgeries, the cost of supportive devices accounts for more than 50% of the total expense.

Although supportive devices play a crucial role in every interventional procedure, with the market size for PCI supportive devices alone reaching RMB 20 billion in 2018, and despite the enormous demand for guidewires whose total output value rivals that of any single product category, the technical barriers and pricing margins established over many years have nonetheless failed to gain significant momentum in China during the several decades of interventional medicine development.

In 2021, the entire market for interventional support products began to experience explosive growth, attracting widespread attention across the industry. Huitai Medical, whose core business focuses on interventional consumables, delivered an impressive semi-annual report just half a year after its listing. Its coronary and peripheral intervention segments showed remarkable growth. In the first half of 2021 (H1 2021), Huitai Medical achieved operating revenue of RMB 380 million, a year-on-year increase of 99.4%, and net profit attributable to shareholders of RMB 110 million, up 186.2% year on year. Notably, revenue from its coronary intervention products rose by 154.8% year on year, while that from peripheral intervention products increased by 103.5% year on year, demonstrating astonishing growth rates.

Supportive devices are also attracting significant capital in the primary market. In 2021, many companies in the supportive device sector secured substantial financing, with total investments exceeding RMB 1.5 billion. Why do supportive devices represent a formidable challenge within the vascular intervention landscape? VCBeat has conducted an analysis of this sector.

Recent Financing Events for Companies in the Supportive Medical Device Sector

In a percutaneous coronary intervention (PCI) procedure, supportive consumables account for approximately 50%–60% of the total cost of PCI materials, excluding stents. The value of these supportive consumables is comparable to that of stents. With the implementation of centralized volume-based procurement for stents, the proportion of costs attributed to supportive devices in PCI procedures has increased further.

The reason why support devices account for a significant proportion in surgeries is that they serve as the vanguard in interventional procedures, akin to tunnel boring machines. With the assistance of support devices, therapeutic devices such as stents, tumor embolization materials, and interventional valves can safely and precisely reach the lesion sites in the human body for treatment. Therefore, support devices play a decisive role in the outcome of a surgical procedure.

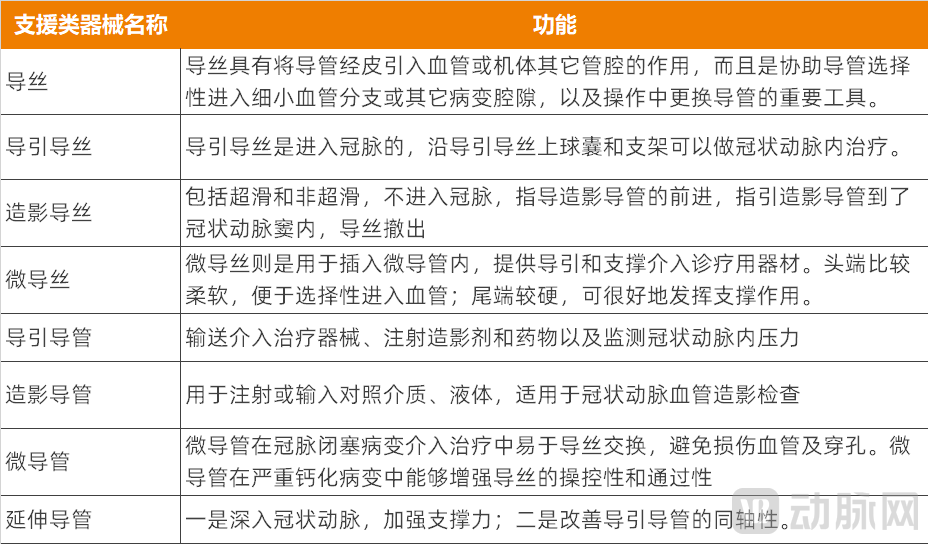

Support devices encompass a wide variety of types and can be categorized according to the surgical workflow: During the puncture phase, physicians require introducer sheath kits and puncture guidewires. In the angiography phase, angiographic guidewires and angiographic catheters are needed; the angiographic catheter navigates through the vasculature along the path established by the guidewire, serving to inject contrast media or fluids. During the access establishment phase, angiographic guidewires, guiding catheters, and guide wires are utilized; the guidewire directs stents and balloons to the specified lesion site, while the catheter provides a conduit for the entry of therapeutic devices.

Segmentation of Catheter and Guidewire Products Among Support Devices

Che Haibo, founder of the minimally invasive interventional medical device company CareRay Medical, told VCBeat that support devices can be categorized into four major types based on manufacturing processes:The first category is guidewires.Guidewires are categorized into guiding wires, support wires, and micro-guidewires. Micro-guidewires, which are used in conjunction with microcatheters to provide navigation and support for superselective interventional diagnosis and treatment, typically have a diameter of ≤0.021 inches.The second category includes sheaths and tubes.This includes arterial sheaths, venous sheaths, and, more importantly, catheters. Catheters are classified based on a 3.0 French (Fr) threshold: those smaller than 3.0 Fr are designated as precision microcatheters, while those larger than 3.0 Fr are referred to as guiding catheters.The third category is balloon-based devices, which include balloon catheters.The fourth category is the hybrid type,Including extension catheters, atrial septal puncture sheaths, and steerable sheaths, hybrid procedures are highly complex and require the integration of multiple techniques involving guidewires, catheters, and even balloons.

Support devices can also be categorized by different application scenarios. These devices are primarily used in coronary intervention, oncology intervention, cardiac electrophysiology, neurointervention, peripheral intervention, and interventional therapy for structural heart disease. Although the technical principles of support devices are similar across these major scenarios, different diseases entail distinct anatomical structures and pathophysiological states, thereby imposing varying requirements on support devices.

Coronary InterventionThis is the most mature sector in the development of endovascular interventional therapy, with as many as 10 types of supportive devices used in coronary intervention procedures. Among the diverse range of supportive devices, catheters and guidewires account for a significant proportion of the output value. According to Frost & Sullivan data, based on 2018 sales revenue, micro-guidewires and guiding catheters ranked first and second in sales among supportive devices, achieving RMB 780 million and RMB 535 million respectively, with market shares of 25.9% and 17.8%.

Oncology InterventionDuring treatment, interventional oncology procedures involve inserting specialized needles, catheters, and other devices into tumors or associated ducts to perform interventions such as catheterization, drug administration, drainage, and arterial embolization for tumor management. In interventional oncology, microcatheters and microwires can navigate through tiny vessels with diameters less than 1 millimeter, meeting the precision requirements for targeted embolization.

NeurointerventionThe types of supportive devices used are similar to those in coronary interventions. The neurointerventional procedure involves femoral artery puncture, under X-ray fluoroscopy, advancing a thin catheter into the vessels supplying the brain or intracranial vascular branches. Then, through a guiding catheter, a thinner and more flexible microcatheter is selectively navigated into the relevant intracranial arteries to reach the lesion site directly. Key products in neurointerventions—microwires and microcatheters—are characterized by extremely high technical barriers, with foreign brands capturing nearly 95% of the market share.

Peripheral Intervention, the supporting devices used include steerable catheters and balloon dilation catheters.

Structural Heart DiseaseIn interventional procedures, support devices are also required. Taking TAVR as an example, the procedure requires support devices such as a delivery catheter system and a crimping/loading system. The valve is compressed to the appropriate diameter using the crimping/loading system, loaded into the delivery catheter system, and then delivered to the target location in the aorta for treatment.

In Cardiac Electrophysiology TherapyAblation therapy requires delivering high-frequency electrical energy via a catheter to a small area of cardiac tissue, thereby neutralizing irregular signals generated by arrhythmogenic tissue and restoring normal cardiac rhythm. Supportive devices used in cardiac electrophysiology procedures include transseptal puncture systems, hemostasis valve-equipped introducer sheaths, steerable delivery sheaths, and balloon angiography catheters.

Historically, the market perceived the supportive medical device sector as having limited capacity, making it difficult for large companies to emerge. However, in recent years, the broad market prospects of supportive medical devices, which span multiple sectors, have begun to come into focus.

Although support devices have a lower unit price compared to therapeutic products, they span multiple sectors. Support devices are required in coronary intervention, neurointervention, peripheral intervention, tumor intervention, and electrophysiology. The total number of surgeries involved exceeds 3 million, far surpassing the capacity of any single sector.

Based on the surgical volume in 2020, it is estimated that China performed approximately 1.4 million percutaneous coronary intervention (PCI) procedures, with supportive devices accounting for about 80% of the costs in PCI surgeries. The number of oncology interventional procedures exceeded 800,000, with supportive devices representing nearly 50% of the associated costs. These two major markets constitute the core battleground for supportive devices. In addition, the electrophysiology market saw over 240,000 procedures, with supportive consumables accounting for more than 60% of the costs. In rapidly growing emerging markets such as neurointervention, peripheral intervention, and transcatheter aortic valve replacement (TAVR), the surgical volume reached approximately 600,000 cases; except for TAVR procedures, the cost share of supportive devices exceeded 50% in all these areas.

In terms of surgical volume, coronary intervention and oncology intervention are the primary battlegrounds for supportive devices, while growth in other niche segments is also substantial. According to industry estimates based on 2019 figures, the market size for supportive devices in coronary intervention was approximately RMB 6 billion; the market size for oncology intervention, calculated at ex-factory prices, was around RMB 1.2 billion; and the market sizes for supportive devices in peripheral and neurointervention were each approximately RMB 2 billion.

How Will the Support Device Market Grow in the Future? According to forecasts by Everbright Securities, the potential end-market size for support devices across major segments—including coronary intervention, neurointervention, peripheral intervention, and electrophysiology therapy—is expected to exceed RMB 50 billion in 2025. The compound annual growth rate (CAGR) from 2019 to 2025 is projected to reach 7.42%. This RMB 50 billion estimate does not include the application of support devices in the oncology intervention market; conservatively, the total addressable market could surpass RMB 50 billion.

In this vast market worth RMB 50 billion, catheters and guidewires represent the highest-value segment, a domain also dominated by imports.In the past, although supportive consumables played a crucial role in surgical procedures similar to stents, the market for supportive devices was dominated by imports, unlike the highly localized stent market. Multinational corporations such as Terumo, Medtronic, Abbott, Merit Medical, and Boston Scientific accounted for over 80% of the market size.

Particularly microcatheters and guidewires among supportive consumables. A microcatheter is a thin-walled, small-diameter catheter used for minimally invasive endovascular therapies, assisting physicians in crossing thrombi prior to any balloon angioplasty or stent implantation and providing support for contrast-guided wires. Microcatheter technology presents high barriers to entry; leading international brands achieve wall thicknesses of only 0.03 mm. According to Frost & Sullivan, Japanese and American brands accounted for 94.7% of the market share in the higher-barrier microcatheter segment in 2018.

The long-standing monopoly on catheter and guidewire products stems from the near absence of domestic technical reserves for raw materials in China, with core technologies predominantly held by Japan. The high-precision equipment required for processes such as guidewire grinding and welding is also largely controlled by Japanese and American companies. For China’s high-value vascular interventional consumables industry, the past two decades of development initially focused on entering the market through stent products, which have relatively lower barriers to entry. Only after accumulating sufficient technological expertise has the industry begun to make inroads into high-barrier segments.

An entrepreneur stated that in the past, supportive medical devices had high technical barriers. No one was developing high-barrier supportive devices; it was akin to trying to carry Mount Tai to leap over the Bohai Sea—something impossible to achieve, not merely a matter of unwillingness.

In recent years, the market for supportive medical devices has been undergoing changes. Domestic products are beginning to rise, and a number of companies that have mastered core technologies have started to participate in the market, filling multiple gaps in domestically produced single-item products.

In recent years, domestic companies have entered the market with products that have relatively lower technical barriers, such as angiographic guidewires and angiographic catheters, and have gradually expanded their product portfolios to include guiding catheters, guiding wires, microcatheters, and microwires. Recently, domestically produced neurointerventional microwires and catheters, which feature higher R&D barriers, have also received regulatory approval, filling a gap in the Chinese-made product landscape.

Supportive devices have high technical barriers. In the past, supportive devices were considered a niche segment within the industry where China had virtually no technological reserves.

In what aspects are the technical barriers of support devices reflected? In a report, Everbright Securities pointed out that support devices have high technical barriers. From the perspective of guidewires, core process pursuits include support force, compliance, trackability, maneuverability, tactile feedback, and visibility. Support force: the force required to bend the guidewire when a perpendicular force is applied; Compliance: the ability of the guidewire itself to adapt to changes in vascular curvature; Trackability: the ability of the guidewire to follow the anatomical structure of blood vessels; Maneuverability: the ability to transmit torque from the proximal end to the distal tip of the guidewire; Tactile feedback: the sensation at the proximal end of the guidewire regarding contact with objects and their characteristics at the distal tip; Visibility: partial radiopacity of the guidewire, facilitating its localization within the body.

Catheter and guidewire technology is akin to fitting Mount Sumeru into a mustard seed, requiring the integration of numerous manufacturing processes into miniature devices.

Che Haibo, founder of Kerecis Medical, pointed out: “In fact, the most fundamental barrier lies in therapeutic insight, which requires a deep understanding of surgical procedures and thorough knowledge of anatomical structures and clinical needs across different surgical scenarios. Taking catheters as an example, their performance characteristics include trackability, radiopacity, pushability, kink resistance, torque control, and device compatibility. However, the specific requirements for each parameter vary depending on the usage scenario, necessitating differentiated prioritization. Meanwhile, only by fully mastering the underlying technology can one determine how to leverage engineering solutions to meet clinical demands.”

For domestic enterprises, the current challenge is to break through in areas with high technical barriers and large market volumes, including products such as precision micro-guidewires and super-selective microcatheters.

Beyond domestic substitution, what are the innovative directions in the high-barrier sector of supportive medical devices?

From a technical perspective, a major direction of innovation for supportive devices is the development of hybrid devices.Hybrid devices are often developed in response to surgical needs, with a greater focus on changes in local hemodynamics and the microenvironment, thereby enabling more precise and standardized assistance during procedures. Examples include steerable microcatheters, sensor-equipped devices, or instruments that modify local hemodynamics. This represents a major future direction.

Another major direction is the development of delivery systems for large implants,For instance, in the case of TAVR products, there are stringent requirements for the delivery system, including controlled deflectability and flexibility. Currently, domestically produced products in China remain largely underdeveloped in this regard, making it a significant area for future development. Taking Medtronic as an example, the company has reduced the profile of its TAVR delivery system to 14F, representing a substantial advancement. In contrast, most domestic systems in China are typically 18F or even larger.

In the RMB 50 billion market for supportive medical devices, who will become China’s Terumo? Currently, multiple domestic companies have begun to focus on this market and are establishing areas of competitive advantage.

The domestic company with the highest market share in the field of coronary intervention is Kangdelai Medical Devices. According to Kangdelai's prospectus, Kangdelai ranked first among domestic brands and seventh among all brands in the PCI support device market in 2018, with a market share of 3.1%.

From a product perspective, Kangdelai specializes in PCI support devices. Its product line covers the entire PCI procedure. Kangdelai Medical’s primary support devices include single-use guiding catheters, guidewires, microcatheters, balloon dilation catheters, hydrophilic-coated guidewires, and angiographic guidewires. These are mainly used to provide access channels for the introduction of interventional and diagnostic devices during coronary intervention procedures, and the company’s product portfolio already covers the complete process of PCI surgery.

Another domestic leader in the field of PCI-support devices is Huitai Medical. According to Huitai Medical’s prospectus, the company is primarily engaged in the research and development, manufacturing, and sales of electrophysiology and vascular interventional medical devices, with a focus on electrophysiology and coronary access products, while prioritizing the development of peripheral and neurointerventional devices. Among domestic brands in China’s coronary access market, it ranks fourth; among all brands, it ranks 13th, with a market share of 1.3%.

In the electrophysiology field, Huitai Medical’s supporting devices include transseptal needles, radiofrequency ablation catheters, and mapping catheters. In the vascular intervention field, Huitai Medical’s supporting devices include sheath introducer sets, guidewires, guiding catheters, and guide wires.

In the primary market, several companies specializing in support devices have secured substantial financing. Likecare Technology completed a Series B financing round worth hundreds of millions of yuan, entering the neurointerventional market with its support devices. CareRay has established a dual portfolio of tumor intervention and support products, completing a Series C+ financing round co-led by Hillhouse Venture Capital and Yuansheng Venture Capital. Mapitech is dedicated to the research and development of interventional access products such as guidewires and catheters, with multiple products already receiving registration certificates.

Although domestic companies have intensified their R&D efforts in interventional guidewires and catheters in recent years, the resulting products are predominantly low-end and low value-added. There have been few breakthroughs in high value-added medical catheters and guidewires designed for specialized clinical applications. However, it is noteworthy that several companies have recently obtained regulatory approvals in high-barrier segments, marking a significant breakthrough in the supportive device market. Vascular interventional high-value consumables represent the most dynamic segment within China’s medical device industry. With the growth of domestic manufacturers of supportive devices, the market is expected to reach a major turning point, accelerating the import substitution of these devices with domestically produced alternatives.

References:

Can Domestic Microguidewires for Neurointerventional Procedures Achieve Import Substitution? — Yi Xiu Shen Jie Shuo