Beauty Device Sector Ignites Frenzy Among Investors as Tencent and Xiaomi Double Down

Investment institutions are intensively scrutinizing the beauty device sector.

Over the past year, investment firms that have already made moves include IDG Capital, Shunwei Capital, Honghui Capital, Fortune Capital, Tiantu Investment, Aoniu Capital, Xinpao Capital, and Sanqi Tiansheng.

Not only that,Tech giants are also eyeing this sector: Tencent and Xiaomi have both recently made substantial investments.

Notably,Unlike traditional investment and financing negotiations, the balance of bargaining power has shifted more toward the corporate side this time.“A high-quality beauty device company can even attract a dozen investment institutions,” said Guan Huiyun (pseudonym), an investment director at a financial advisory firm that has long focused on consumer healthcare, in an interview with VCBeat. “To get a seat at the table, investors need to demonstrate to company founders whether both parties can align in terms of distribution channels and upstream and downstream segments of the industry chain, rather than simply having capital.”

From this perspective, beauty devices are undoubtedly experiencing explosive popularity in the current capital market. However, in reality,Beauty devices, once the target of a capital frenzy, already experienced a surge in popularity several years ago.: Around 2017, Xiaomi Group, Shunwei Capital, Shenzhen Capital Group (SCGC), Northern Light Venture Capital, and Orient Fortune all made strategic investments in this sector. However, by the end of 2018, the beauty device market fell into a lull, with financing news becoming scarce.

Why has it suddenly surged in popularity overnight? What new narrative is emerging in the beauty device sector? What exactly are investment firms and tech giants seeking? And what does the future evolution of the industry look like? To address these questions, VCBeat conducted in-depth interviews with numerous industry insiders and investors, and performed a comprehensive analysis to shed light on the answers.

Beauty devices are not a new market segment.

From the perspective of the international market, Panasonic launched facial steamers in Japan as early as the 1980s. Since then, companies such as Clarisonic have successively introduced beauty devices with various functions, including facial cleansing brushes.Beauty devices in China began to gain widespread public recognition in the market primarily starting from 2015.

At that time, propelled by the reach of mobile internet, an increasing number of young people began to pay attention to and recognize light medical aesthetic products. “Compact and portable home-use beauty devices quickly gained popularity among young users due to their professional-grade cosmetic functions,” stated Guan Huiyun. For instance, radiofrequency (RF) beauty devices rapidly rose to prominence because they leverage the principle that collagen fibers in the dermis contract when exposed to specific temperatures, thereby delivering skin-tightening and wrinkle-reducing effects.

“Young consumers' fear of aging is the primary reason for the explosive popularity of these products.“A head of a medical aesthetics institution, who requested anonymity, told VCBeat that skincare products, devices, and medical aesthetic services marketed for ‘early anti-aging’ generally have the highest repurchase frequency. ‘Consumers are less price-sensitive when it comes to spending on such products.’ Furthermore, compared with the several hours often required for treatments at medical aesthetics institutions,”The convenience of at-home use has also become a significant factor driving young consumers’ choice of beauty devices.

However, it is important to note that although beauty devices possess medical aesthetic efficacy,"Since these products are categorized under home appliances in China, industry standards are still being refined, resulting in uneven product quality on the market."

Moreover, the underlying principles of beauty device technology are highly specialized, making terms such as “microcurrent,” “radiofrequency,” and “wavelength” difficult for consumers to understand. Consequently, purchasing decisions largely hinge on the effectiveness of marketing efforts, such as the prominence of product endorsers and recommendations from peers.This demonstrates that the beauty device industry is a marketing-driven business.

In response, various brands have continuously intensified their marketing efforts, driving a rapid rise in industry prosperity. Data corroborates the strong sales performance at that time; according to research data from Euromonitor International, on e-commerce platforms such as Tmall and JD.com,Personal care appliances, primarily beauty devices, achieved compound annual growth rates of 11% and 8% in 2017 and 2018, respectively.

Yet behind the emphasis on marketing,Most beauty device manufacturers have neglected product quality, leading to a rapid cooling of the entire market.Taking Fan Bingbing’s beauty brand, “FANBEAUTY,” as an example, after launching a new beauty device in March 2018, it quickly sold thousands of units driven by advertising effects. However, frequent issues such as unstable performance and overheating ultimately led to a collapse in the product’s reputation, resulting in significantly sluggish subsequent sales growth. During this period, consumer confidence in domestically produced beauty devices continued to decline, and investment activities in this sector became rare in the capital market.

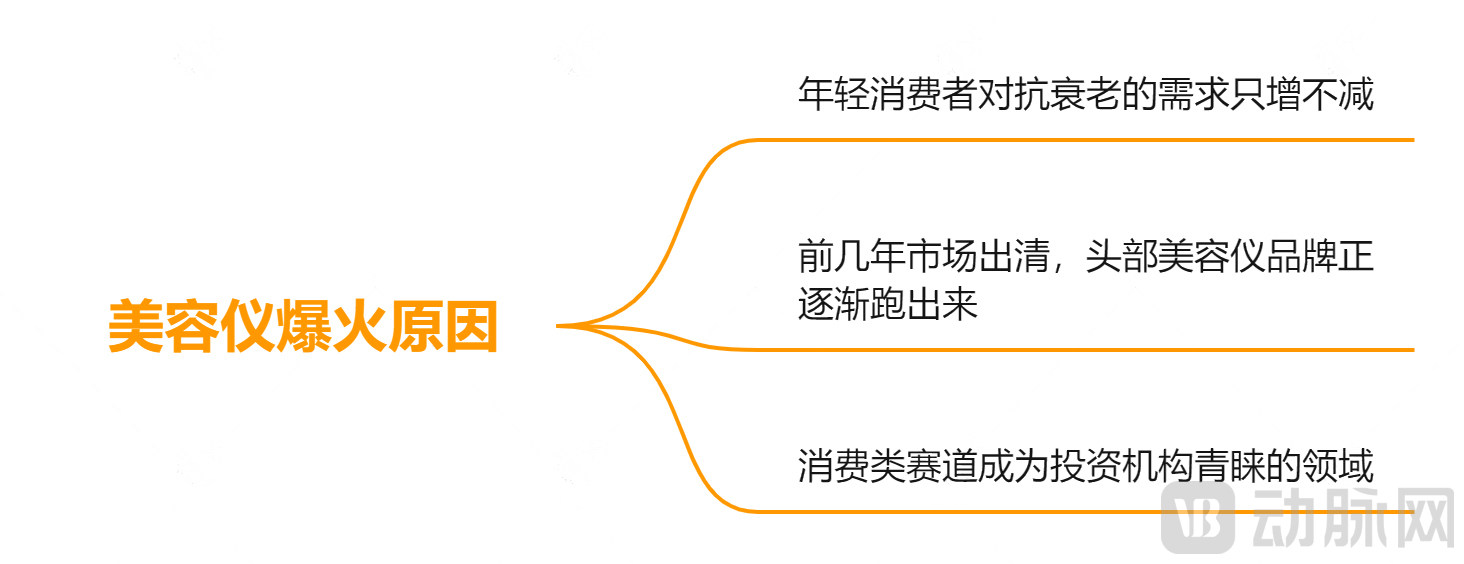

So why are a large number of investment institutions once again scrambling to acquire target companies in this sector this year?

“I believe the core lies in two points.First, demand for beauty devices remains strong and is growing rapidly. Coupled with the industry’s “cold spell” over the past two years, which has weeded out weaker manufacturers, high-quality brands are emerging. Second, the capital market currently holds a positive outlook on the consumer sector." said Guan Huiyun.

According to multiple investors, the industry holds a relatively optimistic view on the scale of China’s beauty device market, projecting it to reach RMB 30 billion within three years. Additionally, China’s current share of the global market is less than 10%, indicating substantial domestic demand. In the future, with the emergence of high-quality domestic brands, there is also significant potential for expansion into overseas markets. According to the “Research Report on Market Size and Development Trends of China’s Beauty Device Industry (2020–2026)” released by Zhiyan Consulting, the production volume of beauty devices in China is currently growing at a rate exceeding 20%.

In summary, the primary reasons for the renewed favor shown by investment firms and industry giants toward the beauty device sector are the ever-growing demand for anti-aging solutions among young consumers and the emerging trend of leading beauty device brands gaining market prominence.

The Surge in Beauty Devices Is Inextricably Linked to Aggressive Marketing by Merchants.

“Costs associated with celebrity and social media KOL endorsements, as well as expenses across various distribution channels, are ultimately passed on to consumers in the form of higher purchase prices,” Guan Huiyun told VCBeat. Among the multiple beauty device companies he surveyed,Many companies' marketing and channel expenses account for approximately 50% of their revenue.“Especially for companies that need to rapidly scale up their volume, the proportion may even far exceed this level in the short to medium term.”

Leading brands are no exception. According to the financial reports of Ya-Man, a publicly listed Japanese brand specializing in beauty devices, its advertising and business outsourcing expenses increased from ¥4.969 billion to ¥6.771 billion between 2016 and 2020. These costs accounted for 24% to 30% of total revenue, representing the largest expense category.

It is evident that the beauty device sector places significant emphasis on marketing and distribution channels. Consequently, many consumers are highly curious,For a beauty device priced at several thousand yuan, with half of its cost allocated to customer acquisition, can the product’s quality and claimed efficacy be guaranteed?Are Beauty Devices a Scam?

Before answering this question, it is important to note thatMainstream beauty devices on the market are primarily categorized into five types: ultrasound, microcurrent, radiofrequency, light spectrum, and oxygen infusion.

In terms of efficacy, ultrasound-based devices primarily provide facial cleansing and nourishment; microcurrent technology enhances muscle fiber tension to achieve a lifting effect; radiofrequency (RF) devices stimulate fibroblasts in the dermis to promote collagen regeneration; light spectrum therapy helps smooth fine lines and maintain skin vitality; and oxygen infusion therapies stimulate stem cell proliferation and division, accelerating wound healing and inflammation recovery.

“Ultrasound-based, spectroscopy-based, radiofrequency-based, and microcurrent-based devices already have relatively mature products on the market, whereas oxygen-injection devices represent an emerging category in recent years that still awaits market validation,” Guan Huiyun told VCBeat.Most beauty devices from leading brands do offer certain efficacy benefits and cannot be dismissed outright as mere “intelligence taxes”; however, the key issue lies in these brands’ need to manage consumer expectations.“The marketing-driven nature of beauty device manufacturers has led to allegations of excessive exaggeration in their promotional efforts. As a result, users have high expectations for the product’s efficacy, which often leads to a gap between expected and actual outcomes after use, making it difficult for them to be satisfied.”

Furthermore, due to low entry barriers, fierce market competition, and a mix of reputable and dubious players, a large number of products with mediocre or even poor efficacy have flooded the market. Last October, CCTV News’s “Weekly Quality Report” conducted an investigation into beauty devices and found that 6 out of 10 best-selling models exceeded relevant standards for nickel release, posing risks such as allergic reactions; additionally, 2 other models were found to carry a risk of low-temperature burns.

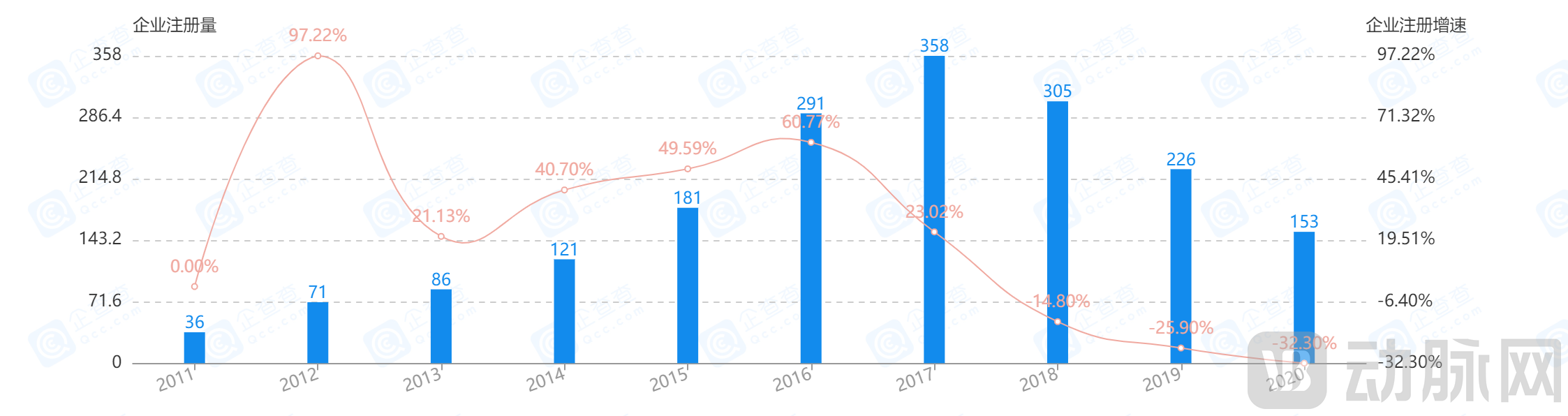

(Trends in the Registration of Companies Related to Beauty Devices. Image Source: Qichacha Professional Edition)

In other words,Overmarketing and the disruption caused by substandard products are the primary reasons why consumers perceive home beauty devices as a “scam.” Additionally, the absence of established industry regulations and standards for home-use beauty devices is a major factor hindering the building of consumer trust.

Earlier this year, the National Medical Products Administration (NMPA) began soliciting public comments on the “Guiding Principles for the Classification and Definition of Radiofrequency Aesthetic Products,” which classify radiofrequency-based medical aesthetic products as Class II or Class III medical devices. This move signals that the regulatory classification of radiofrequency aesthetic devices may be adjusted. Once industry regulations and standards are formally issued, the beauty device market is poised to embark on a path of healthy and sustainable development.

“It is quite difficult for consumers to evaluate the quality of products, as this involves specialized knowledge and entails a high learning curve. Therefore, raising the entry barriers for beauty devices and having regulatory authorities oversee compliance will significantly enhance consumer trust,” said Guan Huiyun.

As can be seen above,The current market landscape for beauty devices is heavily skewed toward marketing and distribution channels. However, as consumer awareness rises and industry regulations are introduced, the focus will gradually shift toward product quality and tangible efficacy in the future.From this perspective, it is not difficult to understand why capital and industry giants are vying for position in the beauty device sector at this juncture.

Currently, imported beauty devices still dominate the entire market in China.

This includes the US beauty device brand Clarisonic, which entered the Chinese market in 2012, as well as subsequent entrants such as Ya-Man, ReFa, Philips, Dr. Arrivo, Tripollar, Ulike, Notime, FOREO, and Smoothskin. Survey data from China Industry Information Online shows that none of the top ten beauty device brands by sales on Tmall during the 2019 Double 11 Shopping Festival were domestic brands.

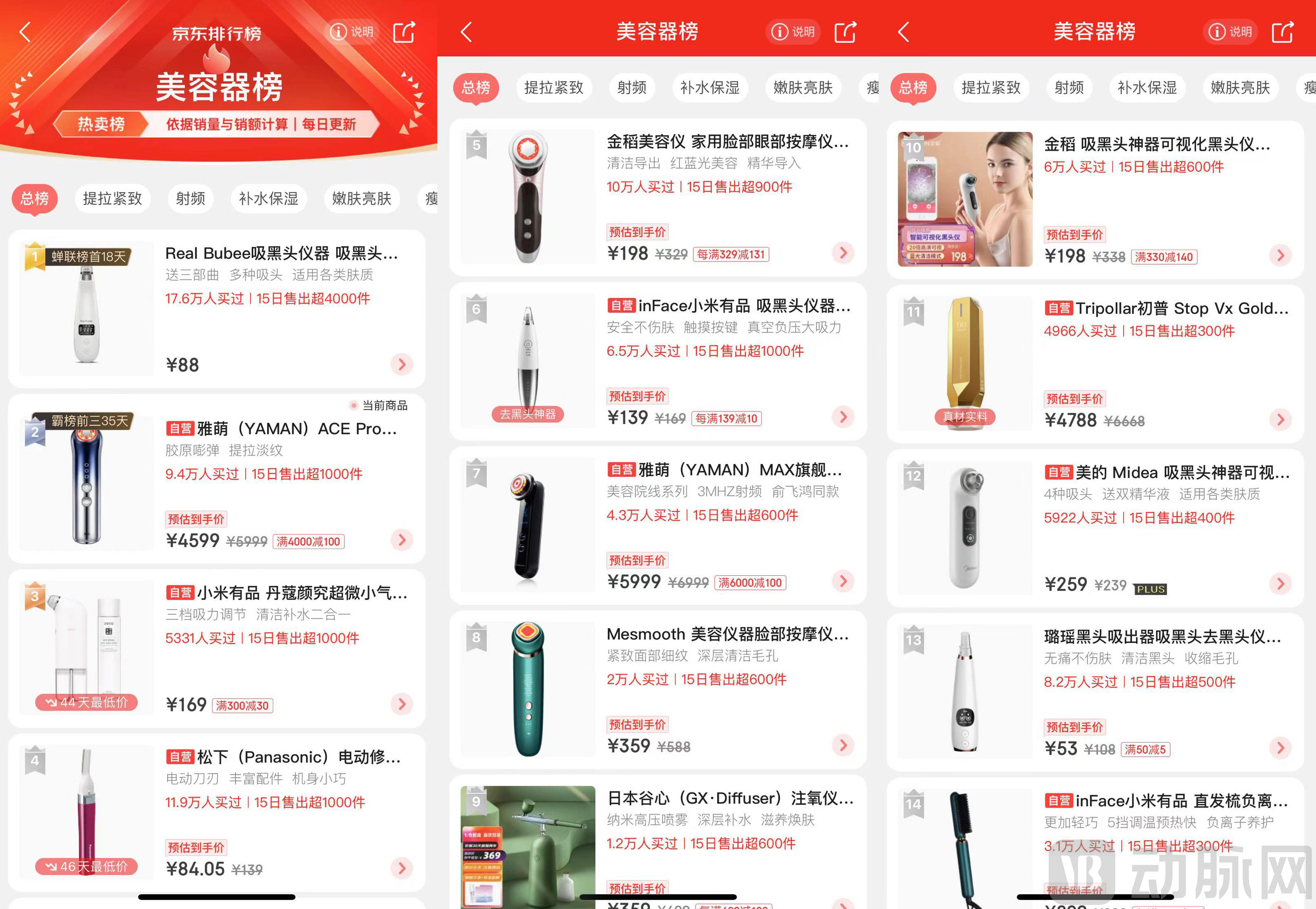

VCBeat conducted a search for major beauty device brands on the JD.com platform and found that some domestic brands, such as Xiaomi, Jin Dao, Landai Meiyan, Qucaotang, Bear Electric, COSBEAUTY, AMIRO, and Femooi, have begun to achieve strong sales, reflecting the rising trend of Chinese brands.

(Top-Selling Beauty Devices on JD.com Platform; Screenshot Date: October 9)

(Top-Selling Beauty Devices on JD.com Platform; Screenshot Date: October 9)

“With the influx of capital, domestically produced beauty devices may be on the verge of an explosive growth.” Guan Huiyun stated that due to China’s robust industrial structure, many raw materials and supply chains for imported beauty devices are primarily concentrated in China, giving domestic brands a cost advantage in production. “This creates room for domestic brands to replace imported products.”

Furthermore, the entry of tech giants such as Tencent and Xiaomi has created opportunities for domestic brands. This is primarily because these conglomerates, leveraging their advantages in distribution channels, user traffic, and capital, can provide significant empowerment to beauty device manufacturers. For instance, Xiaomi has been able to rapidly expand market reach for the beauty device brands it has invested in by utilizing its extensive distribution network and brand influence, thereby establishing user trust to a certain extent through brand endorsement.

However, the core competition in the beauty device industry still lies in the product, which includes technological R&D capabilities and user experience. “Therefore,For beauty device companies, innovation is their core competitiveness. First, product quality must be robust and deliver the claimed effects, which necessitates a strong emphasis on research and development. Second, the user experience must be excellent, enabling the company to lead in a specific niche category.“Guan Huiyun stated.

Take CosBeauty, a company invested in by Xiaomi this year, as an example. It has launched products such as ultrasonic ion beauty devices and hair removal devices tailored to specific consumer segments. In terms of product R&D, CosBeauty established the Institute of Precision Medicine in Shenzhen, entered into a strategic partnership with the Chinese Academy of Sciences to jointly establish the Joint Laboratory of Photomedicine, and maintained close collaborations with research institutions such as the School of Life Sciences at Tsinghua University and Southern Medical University. These efforts have continuously strengthened its interdisciplinary R&D capabilities in skin texture analysis, biotechnology, and ergonomics. To date, the company has obtained nearly 100 authorized patents, and some of its products have passed international authoritative tests and certifications, including FDA, CE, FCC, RoHS, human efficacy evaluation, and nickel release testing.

AMIRO, which Tencent invested in this year, primarily focuses on home-use, medical-grade beauty devices. This year, it launched a radiofrequency (RF) beauty device and a red-light hair removal device. In terms of product development, AMIRO has completed five domestic and international product tests, including those by SGS Switzerland, and collaborated with the Institute of Biomedicine at Tsinghua University to conduct a one-year safety validation. This validation encompassed three dimensions—cellular, animal, and human clinical trials—to ensure product safety. Furthermore, the products have gained recognition from professional institutions such as DXY Doctor, Peking Union Medical College Hospital, and beauty clinics in Japan and South Korea, thereby enhancing consumer trust in the brand.

It is evident that domestic brands are transitioning from a purely marketing-driven model to one driven by research and development, with greater emphasis on exploring niche consumer segments.“Domestic brands have made significant progress over the past two years, butWe still lag behind in optical components, electronic chips, and proprietary patented technologies, including invention patents.“Guan Huiyun stated, ‘The future development of domestically produced beauty devices requires strengthened collaboration with research institutes and top-tier organizations.’”

In today’s increasingly booming “appearance economy,” the beauty device sector is neither short of capital nor market demand; the core lies in delivering high-quality products. Therefore, from a long-term development perspective, domestically produced beauty devices must continuously refine their technologies and build strong brand images. This process will undoubtedly require considerable time to validate and demands sufficient patience from market participants.