PatSnap Releases 'Antibody-Drug Conjugates (ADCs): The “Biological Missiles” Insight Report' — Global ADC Innovation Enters Golden Development Phase

Recently, Patsnap, a SaaS provider for technological innovation intelligence, released the “Insights Report on ‘Biological Missiles’: Antibody-Drug Conjugates” (hereinafter referred to as the “Report”). The Report provides the latest insights into this field through four key modules: ADC technology and business models, global ADC development stages and market size, current status of global ADC patent landscapes, and analysis of leading global companies.

The report highlights that, first, global innovation in antibody-drug conjugate (ADC) therapies has gradually transitioned from an early period of “turbulent development” into a golden age. ADCs have become a key strategic focus for innovative pharmaceutical companies worldwide, with a new peak expected within the next three to five years. In terms of indications and target distribution, oncology remains the core area of focus; however, the emphasis has shifted from hematologic malignancies to solid tumors, with HER2 continuing to be a highly sought-after target. Second, innovative pharmaceutical companies are leading the ADC industry chain, reducing costs, complexity, and risks through an industrial model based on upstream and downstream collaborations. This has led to significant breakthroughs in the business model of the ADC industry. Third, the report provides an in-depth analysis showing that the rapid growth in ADC-related patent filings over the past decade signals intense future market competition. Patent portfolios and the geographic origins of technologies reflect the trend toward international competition in the ADC sector. Furthermore, the report offers a detailed examination of the technological development pathways and current status of two leading companies, Daiichi Sankyo and Seagen.

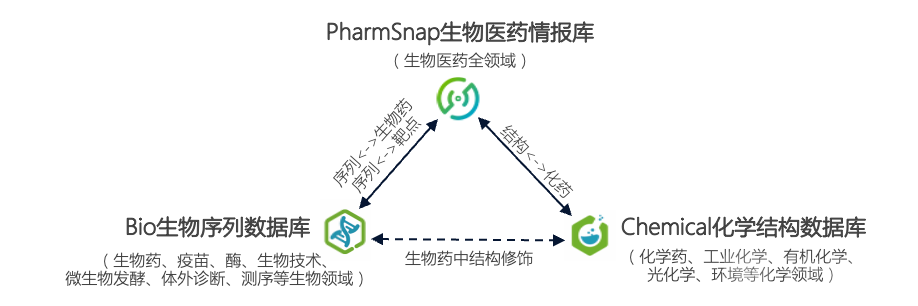

Driven by innovation in the biopharmaceutical sector, Patsnap has steadily increased its investment in biopharmaceutical product lines since 2015. It has successively launched a chemical structure search database (Chemical), a sequence search database (Bio), and pharmaceutical intelligence data (Synapse), thereby building a comprehensive suite of solutions for the biopharmaceutical industry. The company aims to establish an international public service platform dedicated to biopharmaceuticals. Currently, Patsnap serves nearly 1,000 leading enterprises in the global biopharmaceutical field.

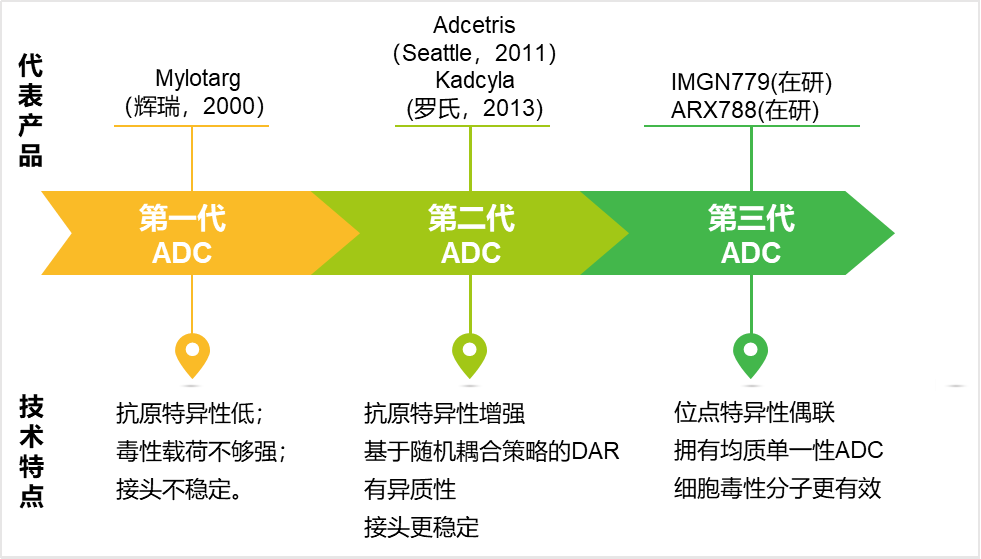

The concept of antibody-drug conjugates (ADCs) has a long history, first proposed by Paul Ehrlich in 1900. However, the development of the ADC industry has been fraught with challenges due to high technical barriers in synthesis, prolonged issues with off-target effects, and difficulties in identifying specific antigens. Over the years, scientists have conducted extensive trials and continuous iterations to optimize ADC synthesis, enhance safety, and reduce off-target effects and toxic side effects. As a result, ADC drugs have only experienced rapid development in recent years.

Figure 1: Technological Iteration of ADC Drugs (Compiled by PatSnap)

Innovative pharmaceutical companies lead the ADC industry chain, reducing costs, complexity, and risks through an upstream-downstream collaborative model. The industrial model for antibody-drug conjugate (ADC) therapies has achieved significant breakthroughs.

The report points out that the characteristic of ADC drugs, which combine large molecules and small molecules, results in a complex production process. This process mainly includes the preparation of monoclonal antibodies, linkers, small molecule drugs, ADC conjugation, purification, and final product manufacturing. The complexity poses significant challenges to the analysis, design, and manufacturing of their structures. It is difficult for individual R&D innovation entities to support the entire process of the ADC drug industry alone, highlighting the necessity of specialized platforms for ADC drug production. Consequently, the development of ADC drugs has also promoted the growth of CMO (Contract Manufacturing Organization) enterprises.

The ADC drug industry chain is primarily driven by upstream R&D enterprises, which outsource the specialized manufacturing of ADC drugs to CMOs and establish sales models through agreements with CSOs. For instance, the innovative biopharmaceutical company Seagen handles drug R&D and technology development; CMOs such as ABZENA and Novasep are engaged for the specialized production of ADC drugs, with the pharmaceutical company paying for manufacturing and process optimization costs. In the sales phase, Seagen licensed rights for regions outside North America to Takeda Pharmaceutical Company in exchange for sales royalties. This industrial model reduces the drug development costs for innovative enterprises, lowers the risks and complexities associated with drug manufacturing, and fosters collaboration and transactions among various companies.

To date, 13 antibody-drug conjugate (ADC) therapies have been approved globally. Between 2000 and 2016, only three ADC drugs were launched; however, in the past five years alone, ten additional ADC products have entered the market. An analysis of R&D pipelines among domestic and international companies indicates that ADCs have become a key strategic focus for innovative pharmaceutical firms worldwide, with a new peak in approvals anticipated within the next three to five years. Regarding indications and target distribution, oncology remains the core therapeutic area, although the focus has shifted from hematologic malignancies to solid tumors. While HER2 continues to be a prominent target, exploration of novel targets is becoming increasingly diverse.

Figure 2: Status of Globally Marketed ADC Drugs (Compiled by PatSnap)

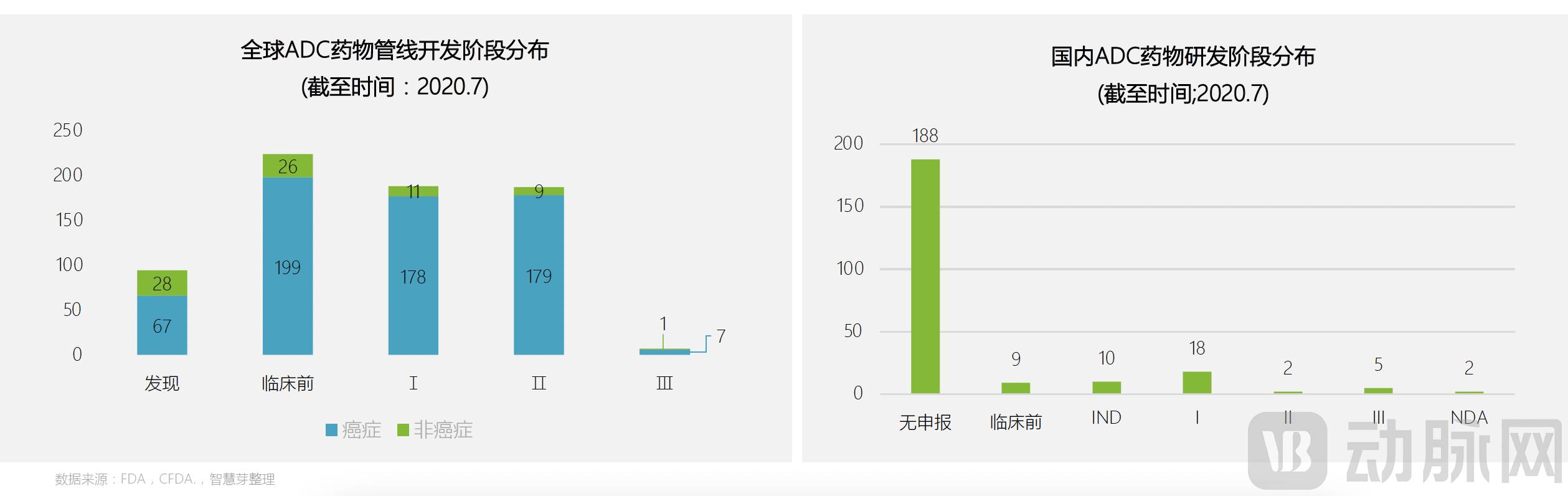

The report indicates that, in terms of the global R&D pipeline, data as of July 2020 show a relatively small number of candidates entering Phase III clinical trials. With 189 assets in Phase I and 188 in Phase II, this suggests that ADC drugs may usher in another peak of market approvals in three to five years. Notably, while oncology remains the predominant therapeutic area for global ADC development, ADC candidates targeting non-oncology indications are also experiencing sustained growth.

In terms of the number of R&D pipelines in China, most domestic pipelines are currently in the preclinical development and laboratory research stages, with a relatively small number having entered clinical trials, primarily concentrated in Phase I. Data from July 2020 showed that there were two ADC drugs already marketed in China, and three New Drug Applications (NDAs) had been submitted (Pfizer’s Mylotarg and Besponsa, and RemeGen’s HER2-ADC). On June 9, 2021, RemeGen’s HER2-ADC drug received marketing approval.

Figure 3: Global and Chinese ADC Drug Pipeline Distribution (Compiled by Patsnap)

According to publicly available market statistics, the sales of approved antibody-drug conjugate (ADC) drugs have shown significant growth momentum in major markets. In the United States, sales increased from $328 million in 2016 to $1.47 billion. In 2020, sales in the European and Japanese markets reached $581 million and $222 million, respectively. In terms of individual product sales, Seagen’s Adcetris and Roche’s Kadcyla both surpassed the $1 billion mark in 2019, gradually emerging as “blockbuster drugs.”

Based on the primary indications of the three ADC drugs already launched in the Chinese market, the future growth potential in the China region is substantial. RemeGen has partnered with Seagen to develop and commercialize disitamab vedotin, China’s first domestically developed ADC drug, with total potential revenues reaching up to $2.6 billion.

Furthermore, the report indicates that the market size for anti-HER2-negative breast cancer ADC drugs in China is projected to reach RMB 3.22 billion, while the market size for anti-CD30 lymphoma ADC drugs is expected to reach RMB 920 million, highlighting substantial market potential.

On August 8, 2021, RemeGen Co., Ltd. entered into an exclusive global license agreement with Seagen, a renowned international biopharmaceutical company, for the development and commercialization of its novel antibody-drug conjugate (ADC) disitamab vedotin. The potential total revenue from this transaction could reach up to $2.6 billion, setting a new record for overseas licensing deals involving a single drug product by Chinese pharmaceutical companies.

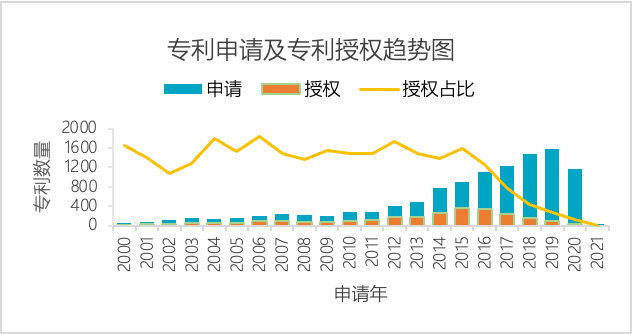

The report highlights that the rapid growth in ADC drug patents over the past decade signals intense future market competition, while patent layouts and regional sources of technology reflect the international competitive trends in the ADC drug sector.

The report indicates that the approval and market launch of the second-generation ADC drug, Adcetris, in 2011 significantly stimulated the enthusiasm and innovation quality of developers in the field of antibody-drug conjugates (ADCs). This was followed by a rapid increase in global patent applications related to ADC drugs over the past decade, with grant rates remaining consistently high.

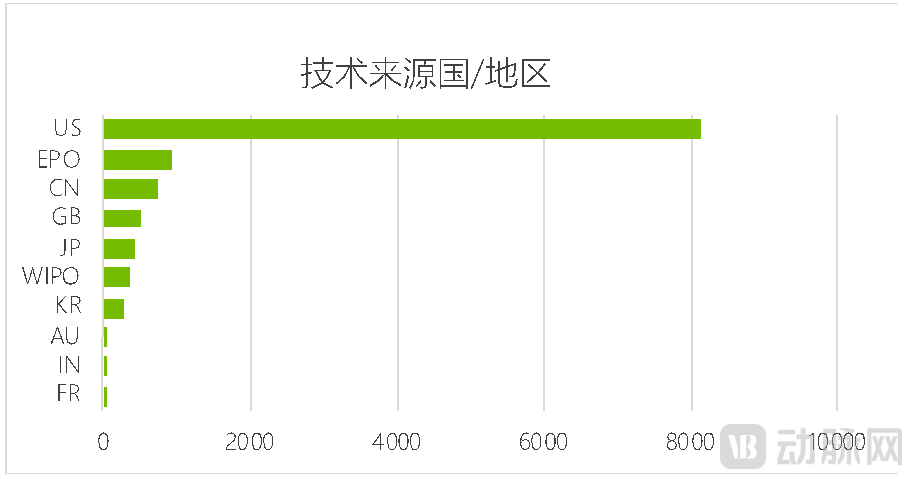

Whether viewed from the perspective of patent deployment regions or technological source regions, the United States remains the largest target market and source market for technology, fully reflecting the technological leadership of U.S. innovators in this field. In terms of the number of patents accepted by WIPO, innovators in the ADC drug sector are leveraging international patent portfolios to support the participation of their future products in global market competition.

The report indicates that in 2011, the second-generation ADC drug (Adcetris) was approved for market launch, and patent applications surged rapidly. To date, this significant growth trend has persisted. Due to the numerous technical challenges in ADC drugs that remain to be resolved or optimized, the patent grant rate has consistently remained high, reflecting the overall high quality of technological innovation in this field (see Figure 4).

In terms of the primary countries of origin for technologies in the antibody-drug conjugate (ADC) field, the United States ranks first with a patent application volume that far surpasses that of other countries. This fully reflects the robust technical strength and dominant position of the United States in this field, with few countries able to compete with it. Although China ranks third, like other countries, it still lags significantly behind the United States. This indicates a pronounced imbalance in national capabilities within the ADC drug sector, with substantial disparities between different tiers (as shown in Figure 5).

Figure 4: Global Trends in ADC Patent Applications and Grants (Source: Patsnap)

Figure 5: Distribution of Global ADC Technology Sources by Country (Source: PatSnap)

The report also provides an in-depth analysis of the technological development pathways and status of two leading companies, Daiichi Sankyo and Seagen. It highlights that Daiichi Sankyo’s DXd-ADC technology platform features multiple innovations and holds a globally leading position. The platform effectively balances the trade-off between efficacy and toxicity of antibody-drug conjugates (ADCs), with innovations in linker design, payload toxins, and conjugation technologies. Currently, more than six product candidates are under development using this platform, among which Enhertu has already achieved successful commercialization. The strategic patent layout for the platform safeguards core technologies and provides substantial support for future technical collaborations or licensing opportunities.

Seagen is characterized by its deep cultivation of core technologies and active pursuit of external collaborations, establishing itself as a star enterprise in the antibody-drug conjugate (ADC) field. As a biopharmaceutical company focused on developing antibody-based cancer therapies, Seagen has secured more than 10 global technology or commercialization partners. Among the 13 ADC drugs currently marketed worldwide, three were developed with Seagen’s involvement. Notably, Adcetris ended the 40-year stagnation in treatment regimens for refractory Hodgkin lymphoma and has become the new benchmark for first-line therapy of Hodgkin lymphoma. Meanwhile, whether regarding individual products or platform technologies, Seagen’s patent protection network remains at the forefront.

Driven by innovation in the biopharmaceutical sector, Patsnap has progressively increased its investment in biopharmaceutical product lines since 2015. It has sequentially launched a chemical structure search database (Chemical), a sequence search database (Bio), and pharmaceutical intelligence data (Synapse), thereby establishing comprehensive and robust solutions for the biopharmaceutical industry. Patsnap aims to build an international public service platform dedicated to the biopharmaceutical field. Currently, Patsnap serves nearly 1,000 leading enterprises in the global biopharmaceutical industry.

Figure 6: Patsnap’s Biopharmaceutical Product Solutions

About PatSnap

PatSnap is a SaaS provider of technology innovation intelligence, focusing on two major sectors: technology innovation intelligence and intellectual property (IP) informatization services. Leveraging artificial intelligence technologies such as machine learning, computer vision, and natural language processing (NLP), PatSnap delivers big data intelligence services to technology companies, universities and research institutions, financial institutions, and other organizations worldwide. PatSnap has built a comprehensive product portfolio centered on technological innovation and intellectual property, including the PatSnap Global Patent Database, Innosnap IP Management System, Insights Patent Analysis System, and Discovery Innovation Intelligence System.

Patsnap has served over 10,000 clients across more than 50 countries worldwide, covering over 50 high-tech industries such as universities and research institutes, biopharmaceuticals, chemicals, automotive, new energy, telecommunications, and electronics. Its domestic clients include Tsinghua University, Peking University, the Chinese Academy of Sciences, Sinopec, Haier, Midea, Xiaomi, CATL, XPeng Motors, DJI, WuXi AppTec, SenseTime, and BGI; its international clients include the Massachusetts Institute of Technology (MIT), the University of Oxford, Dow Chemical, Dyson, and Spotify.