Global Healthcare Industry Capital Report Q3 2021: Startups Remain Vigorous Amid Sustained Investment Boom

I. Buoyed by the strong performance of IPOs in 2020 and large-scale M&A transactions, global healthcare financing in Q3 2021 continued the momentum seen in Q1: total funding reached a record high, marking the largest increase in nearly three years; there were 75 financing deals exceeding $100 million during the quarter, accounting for 8% of the total.

II. Global biopharmaceutical financing topped the charts, with digital health and medical devices neck and neck; meanwhile, the healthcare services market, dominated by third-party medical institutions and specialized hospitals, saw significant growth.

III. The digital health sector abroad is witnessing robust growth, with mental health companies attracting continuous investment amid the impact of pandemic control measures and challenges in returning to work, while differentiated competition intensifies. In China, frequent financing activities are seen in the medical device and consumables sectors, with the diagnostics field, represented by IVD, continuing to break records.

IV. Investment institutions worldwide have maintained strong enthusiasm for healthcare enterprises empowered by digital technology and innovative tech; RA Capital and Sequoia Capital China jointly set a new global record, with the number of investments in the third quarter of 2021 being 25% higher than the total for the entire previous year.

5. Jiangsu Ranks Among the Top 3 Hottest Regions for Financing in China, with Total Financing Volume Slightly Surpassing Beijing.

VI. Top 10 Most-Funded Companies in Q3 2021: Abogen Biosciences Leads Globally with $700 Million Financing; Two Chinese Healthcare IT Companies Make the List.

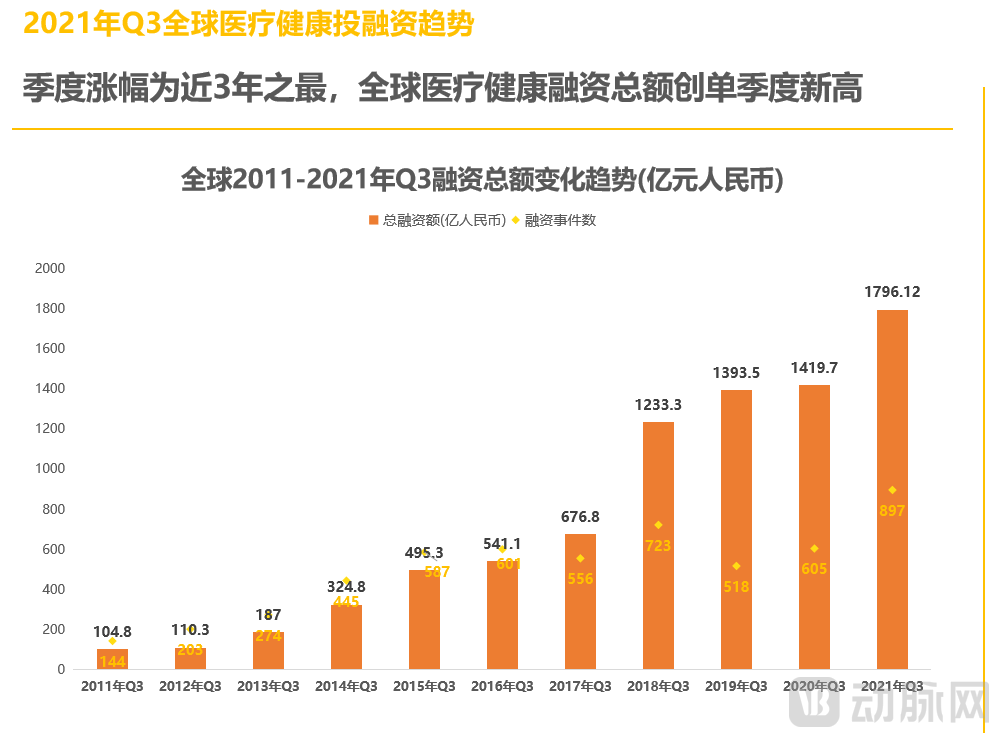

1.1 Quarterly Growth Hits Three-Year High, Global Healthcare Financing Reaches Record Single-Quarter Total

In Q3 2021, there were 897 financing deals in the global primary healthcare market, a year-on-year increase of approximately 45%, with the total financing amount reaching a record high of over RMB 179.6 billion. Compared to the surge in capital investment in the healthcare industry at the beginning of this year, capital cooled down in the third quarter: while the number of financing deals increased, the total financing amount decreased.

As epidemic prevention efforts and the resumption of work and production have advanced in stages, and as governments, industries, and the public have deepened their understanding of vaccines, online healthcare, health management, and AI-enabled solutions since the outbreak began, capital enthusiasm for the healthcare sector has remained undiminished. Compared with Q1, a greater number of promising, high-growth startups secured funding in Q3.

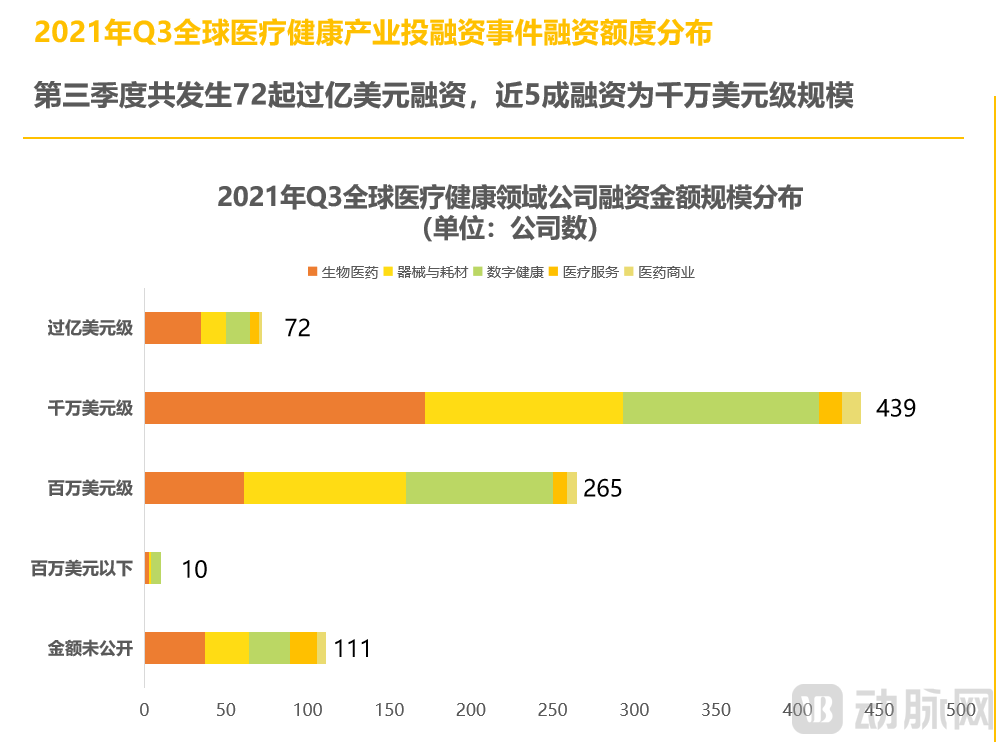

1.2 A total of 72 financing deals exceeding $100 million occurred in the third quarter, with nearly 50% of the deals valued at tens of millions of dollars.

In Q3 2021, there were 72 financing deals exceeding $100 million, accounting for over 8% of the total financing amount in Q3 and approaching half of the full-year total in 2020; nearly half of these deals involved companies in the biopharmaceutical sector.

Financing deals in the tens of millions of dollars were the most frequent. Unlike Q1, when biopharmaceutical companies dominated this segment, their lead in Q3 was marginal. Digital health and medical device companies followed closely, with comparable performance.

This trend is also evident in financing deals valued at over one million U.S. dollars. As small-scale financings are typically concentrated in the pre-Series A and Series A stages, this indicates that capital remains focused on startups in the medical device and digital health sectors during the current quarter.

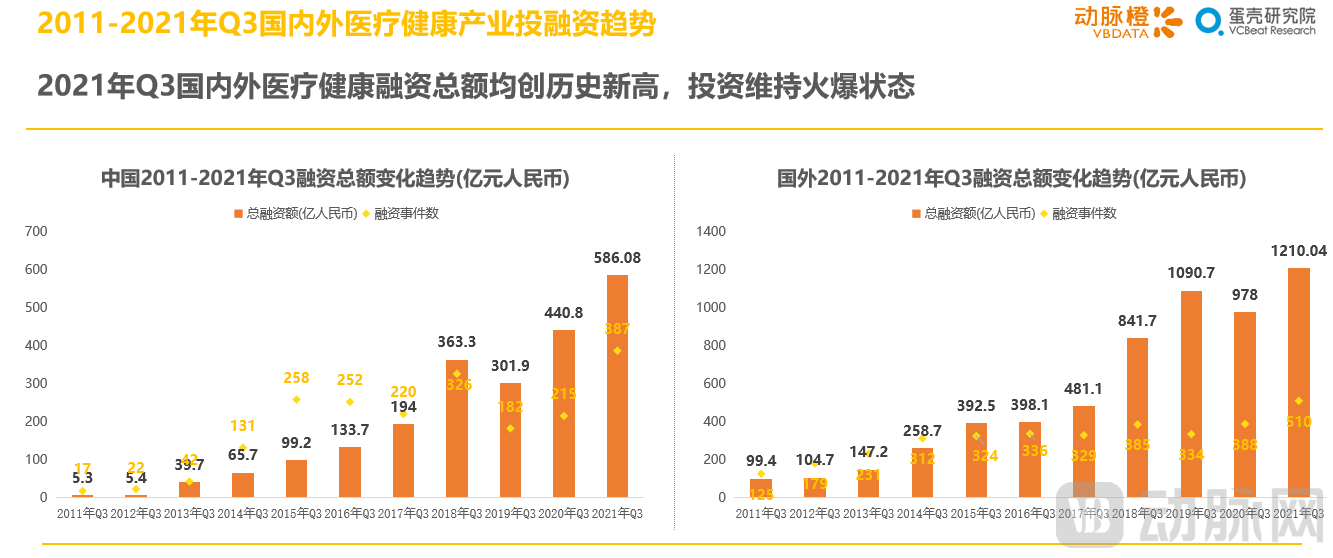

1.3 Total healthcare financing in China and abroad both hit record highs in Q3 2021, with investment activity remaining robust

In Q3 2021, the total investment and financing in China's healthcare industry reached a record high of RMB 58.608 billion, surpassing the figures for both financing volume and number of deals in Q1 of this year. Although the year-on-year growth was relatively moderate, domestic capital remained highly active in Q3 2021. It is worth noting that the financing amount and number of transactions already rebounded in Q3 2020, suggesting a potential turning point that reversed the relatively challenging fundraising environment for Chinese startups since 2018. The performance of China's domestic capital market in Q3 2021 undoubtedly reached new heights.

In Q3 2021, there were a total of 510 financing events in the overseas healthcare industry, with the total amount of financing reaching as high as RMB 121.004 billion. This was also the quarter with the highest total financing amount and the largest number of financing events to date; among them, there were 48 instances where single financings exceeded USD 100 million, and 35% of these were concentrated in Series B rounds.

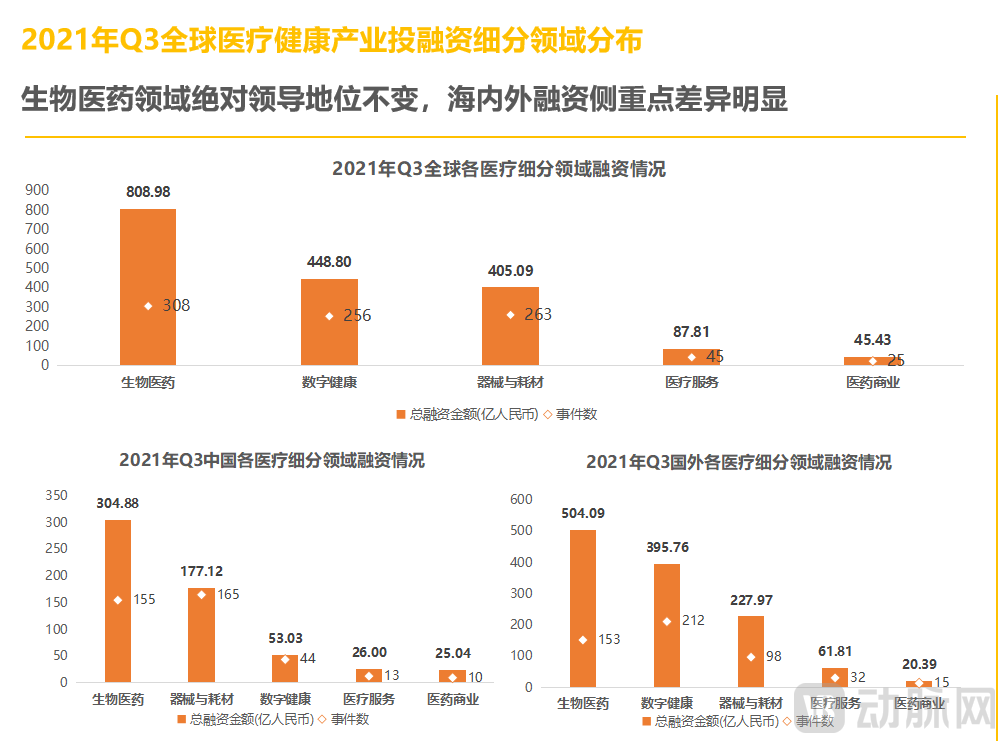

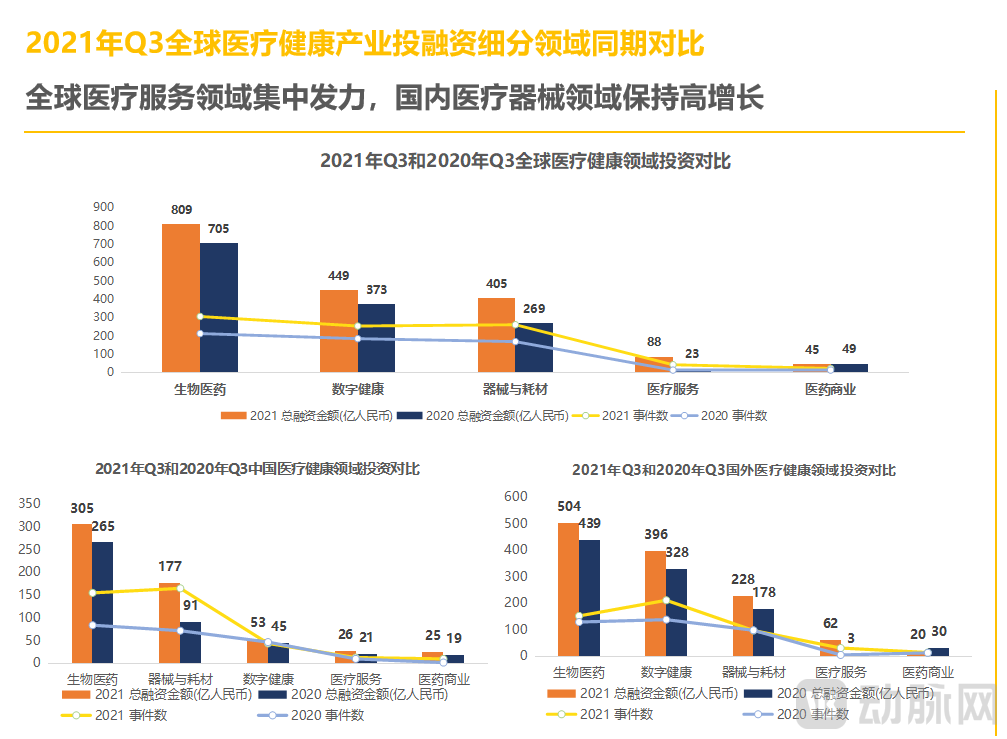

2.1 The absolute leadership position in the biopharmaceutical sector remains unchanged, with significant differences in financing priorities between domestic and overseas markets

In Q3 2021, the global biopharmaceutical sector led all subsectors with 308 transactions totaling RMB 80.898 billion. The digital health sector followed closely with 256 transactions, while medical devices and consumables ranked third.

Biopharmaceuticals remain the hottest sector for joint bets by investors both in China and abroad.

In China, the total disclosed financing in the biopharmaceutical sector amounted to RMB 30.488 billion. The medical device sector attracted significant capital attention in Q3, with 165 financing deals, surpassing the number of deals in the biopharmaceutical sector.

Abroad, funding priorities differ. In addition to the biopharmaceutical sector, which leads in total funding volume, the digital health sector recorded 212 financing deals with a total amount nearing RMB 40 billion, on par with the transaction value generated in the biopharmaceutical sector.

2.2 Global Healthcare Services Sector Intensifies Efforts, While China’s Medical Device Market Maintains High Growth

Compared with Q3 2020, financing across various subsectors of the global healthcare industry rose steadily in 2021, except for a slight decline in the pharmaceutical commerce sector.

In China, consistent with Q1, the total financing in the medical device sector increased significantly in Q3 2021, rising by 95% quarter-on-quarter. Financing activities were predominantly concentrated at the multi-million-dollar level, with 71 transactions driving up the overall funding volume. Notably, the in vitro diagnostics (IVD) segment demonstrated a greater propensity for securing substantial financing.

Furthermore, the number of financing deals in the global healthcare services sector increased by 282.6% year-on-year, with five deals exceeding $100 million. It is worth noting that in Q3 2021, companies securing financing in the healthcare services sector were primarily third-party service providers; enterprises aimed at reducing healthcare costs and streamlining care processes were more favored by capital.

2.3 Hot Topics in Global Financing: Biopharmaceuticals, Healthcare Informatics, Internet + Healthcare, IVD, and R&D and Manufacturing Outsourcing

In Q3 2021, tags such as biopharmaceuticals, healthcare informatics, Internet + Healthcare, and IVD garnered significant attention.

In terms of funding round distribution, Series A financing events occurred most frequently, with 266 cases, primarily concentrated in the fields of biopharmaceuticals and healthcare informatization.

A total of 38 financing events at Series D or later stages were recorded in Q3 2021. Notably, eight of these were Pre-IPO rounds, nearly triple the number from the same period last year, indicating that companies with scale and revenue levels suitable for public listing are increasingly sought after by capital investors.

3.1 RA Capital and Sequoia Capital China Fund Set New Global Record: Investment Count in Q3 2021 Was 25% Higher Than the Full Year of 2020

3.2 In Q3 2021, Domestic Institutions Outperformed Overseas Counterparts in Activity Within the Healthcare Sector

In Q3 2021, Sequoia Capital China was the most active investor in the global healthcare market, with 29 investments in a single quarter, marking its highest quarterly activity in the first three quarters of the year. Notably, Chinese investment firms demonstrated significant momentum this quarter, securing six out of the top ten spots globally. Compared to the first two quarters of the year, leading institutions’ enthusiasm for the healthcare sector continued to rise, with the total number of investments by the top 10 most active global investors increasing. Even Khosla Ventures, ranked tenth, made more than 10 investments during the quarter.

Notably, Sequoia Capital China Fund topped the list of most active investors in the healthcare sector in Q3 2021. According to incomplete statistics from VBInsight, Sequoia Capital China Fund has completed 270 investments in the healthcare field. Among these, Baiyang Pharma, a commercialization platform for pharmaceutical products, and Brii Biosciences, focused on innovative drug R&D, both successfully went public in 2021.

3.3 Domestic investment institutions favor innovative technology sectors such as mRNA therapeutics and AI-assisted R&D platforms

Sequoia Capital China made a total of 29 investments this quarter, surpassing Hillhouse Ventures in the cumulative number of deals during the first three quarters of the year with 62 completed investments, thereby setting a new record on the list of most active institutional investors.

YuanSheng Venture Capital and Lilly Asia Ventures tied for second place with 16 investments each in this quarter’s investment rankings, continuing to focus on early-stage startups.

In terms of investment preferences, domestic institutions in China largely favor companies linked to innovative medical technologies. Apart from some enterprises focusing on internet healthcare and medical informatization, those led by algorithm-driven innovative drug R&D, mRNA drug platforms, and AI-based medical devices have taken the lead, surpassing traditional pharmaceutical and medical device companies in their ability to attract capital.

4.1 Global: The US Leads Globally, with China and the US Accounting for 85% of Global Financing

In Q3 2021, the five countries with the highest total healthcare financing globally were the United States, China, the United Kingdom, France, and Germany.

Among them, the total financing in China and the United States still accounts for about 85% of the global healthcare financing. Although the number of financing events in the United States this quarter was less than that in China, it achieved a reversal with a total amount of $14.482 billion (approximately RMB 93.3 billion), which is closely related to the distribution of large-scale financing.

Furthermore, emerging healthcare players in Europe delivered particularly strong performance this quarter. Notably, total financing in the UK continued the upward trend seen in the first half of the year, far exceeding the combined totals of France and Germany.

4.2 China: Shanghai Leads in Total Financing Volume, Jiangsu Surpasses Beijing in Financing Activity

The top five regions for healthcare financing in China this quarter have remained largely unchanged compared to the previous two quarters. The five most active regions for healthcare investment and financing activities are Shanghai, Guangdong, Jiangsu, Beijing, and Zhejiang.

Shanghai topped the list this season with total financing amounting to approximately RMB 14.2 billion. Guangdong followed closely, ranking first in the number of financing deals with 81 transactions.

Notably, leveraging the spillover benefits from Suzhou’s biopharmaceutical industry hub, Jiangsu surpassed Beijing by a narrow margin this quarter to rank among the top three hottest domestic regions for financing.

4.3 United States: California Remains Dominant, with Massachusetts and New York Emerging as Secondary Hubs

In Q3 2021, California, USA, recorded a cumulative total of 113 financing deals, raising approximately $5 billion (about RMB 32.3 billion), nearing the combined total of Massachusetts and New York State, making it the most active region globally for healthcare venture capital investment transactions.

Moreover, Massachusetts, one of the most concentrated areas for high-tech industries in the United States, has surpassed New York to become the second-largest state for healthcare financing in the U.S., leveraging its robust strengths in industry-academia-research collaboration.

5.1 Top 10 Global Financing Amounts: Abogen Leads with $700 Million in Funding; Two Chinese Healthcare IT Companies Make the List

5.2 Top 10 Financing Amounts in China: Apart from Biopharmaceuticals, Domestic Capital Favors AI and Internet Technology Companies

Scan the mini-program QR code to read the report for free.